In a recent Ola update (move OS 4) Ola replaced mapmyindia and introduced Ola maps.

Can this change harm mapmyindia?

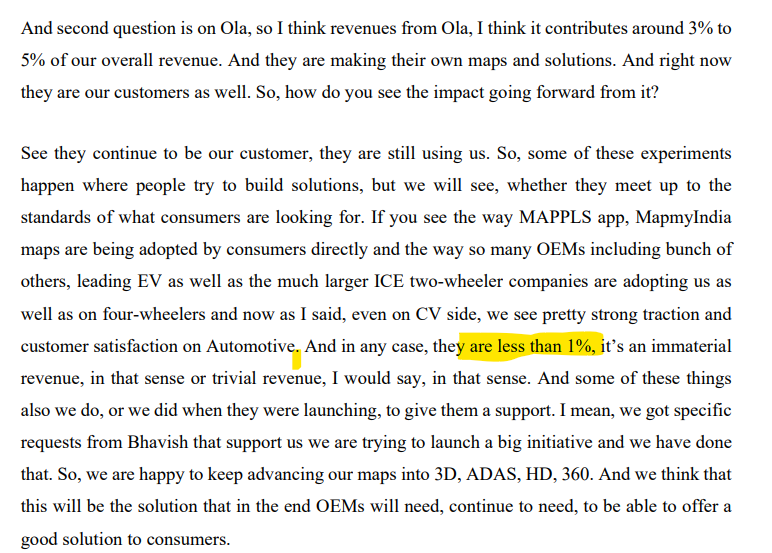

@Mohit_Jariwala revenue from Ola is below 1% so no major impact. below is from Q2FY24 transcript.

1 Like

yeah, that’s great.

But right now my question is in this sector any vehicle company builds its maps then this is a major drawback for mapmyindia. Right now the company gets premium as a monopoly company but slowly I think so there is no monopoly is their for Mapmyindia. Is my thinking right?

2 Likes

Yes your thinking is right. However, we should also account for what is most efficient way for an OEM. Thats why Auto ancilliaries exist as they can do it in more efficient manner and OEMs can focus on marketing and brand building. Also can Ola sell this map to other OEMs, for industrial uses (drone, automation), e-commerce (Amazon, Zomato). That will be bigger risks.

But you raise a valid point. Never say never. We shall keep an eye.

disclosure: I am invested and no transaction in last 30 days.

5 Likes

Agree never say never and anything is possible.

Though with the amount of data points that one needs to capture, issue continuous updates, and build additional features etc. it will be very difficult for someone to develop a similar platform… even if someone builds - very difficult to build use cases across multiple industries…

And for any auto company, it would be a case of going away/ ‘diworsefying’ from their ‘core competency’…

Disc - invested

3 Likes

100% agree.

Adding more point to it. Ola maps will not be that accurate.

Plus the real monopoly will come to map India (Not sure whether people can presently update the mappls or not), once community start getting update like people can update the Google map

1 Like

KEY HIGHLIGHTS FROM THE CON CALL FOR Q3 :

Positive Points:

- MapmyIndia achieved a significant milestone of surpassing INR 100 crores in quarterly total income for the first time, marking a substantial growth trajectory.

- Q3 FY’24 revenue reached an all-time high of INR 92 crores, exhibiting a remarkable 36% year-on-year growth.

- EBITDA in Q3 FY’24 surged by 38% to INR 38.6 crores, with a robust year-to-date growth of 32% to INR 116.6 crores, reflecting strong financial performance.

- Year-to-date PAT stood at a robust INR 96.2 crores, showcasing a 21% year-on-year growth, with a PAT margin of 32%.

- The company demonstrated resilience and maintained a healthy cash reserve of INR 516.1 crores despite dividend payouts.

- Continuous improvement in IoT-led EBITDA margins from 6.3% in Q1 to 10% in Q3 indicates effective execution of the IoT business strategy.

- Drone Business Potential: The company sees significant potential in its drone business, highlighting recurring revenue opportunities through continuous inspections and monitoring.

- Upselling Opportunities: There are multiple upselling opportunities within the drone business, including additional services like analytics and software stack upsells, providing potential for revenue growth.

- Strategic Investments: Investments in companies like KOGO and Indrones are seen as strategic moves to enhance the company’s ecosystem and capabilities, particularly in areas like AI-powered travel assistance and drone technology.

- Strong User Engagement: The consumer mapping business, particularly the Mappls App, has shown strong user engagement, indicating potential for growth and revenue generation.

- Customer Retention: The company boasts high customer retention rates, particularly in the automotive sector, which provides a stable revenue stream.

Negative Points:

-

The clarification regarding EBITDA calculations raised concerns about transparency and accuracy in financial reporting.

-

The significant increase in marketing and business promotion expenses from INR 20-25 crores to INR 50 crores in Q3 raises questions about cost management strategies.

-

Despite promising growth prospects, the revenue contribution from consumer advertisement income remains relatively small and uncertain.

-

The uncertainty surrounding the exact revenue share from EVs in the auto segment raises concerns about diversification strategies and market penetration.

-

While engagement with the government for digital transformation initiatives is positive, the revenue contribution from government contracts remains limited and highly selective, ranging between 5% to 10%.

-

Early Stage Deployment: Despite potential, the drone business is still in early stages with certain customers, indicating a longer timeline for revenue realization.

-

Monetization Uncertainty: There’s uncertainty regarding how the drone business revenue is being monetized, with a mix of hardware sales, service provisions, and solution integrations, potentially leading to complexities in revenue forecasting.

-

Marketing Expense Impact: Additional marketing expenses have been absorbed in the Map-led segment, potentially impacting short-term profitability.

-

Hardware Revenue Stagnation: Hardware revenue in the IoT segment has remained flat over the last few quarters, signaling a need for reassessment of sales strategies to drive growth.

-

QIP Status: The planned Qualified Institutional Placement (QIP) is still pending execution, which may affect the company’s ability to raise capital for future growth initiatives.

6 Likes

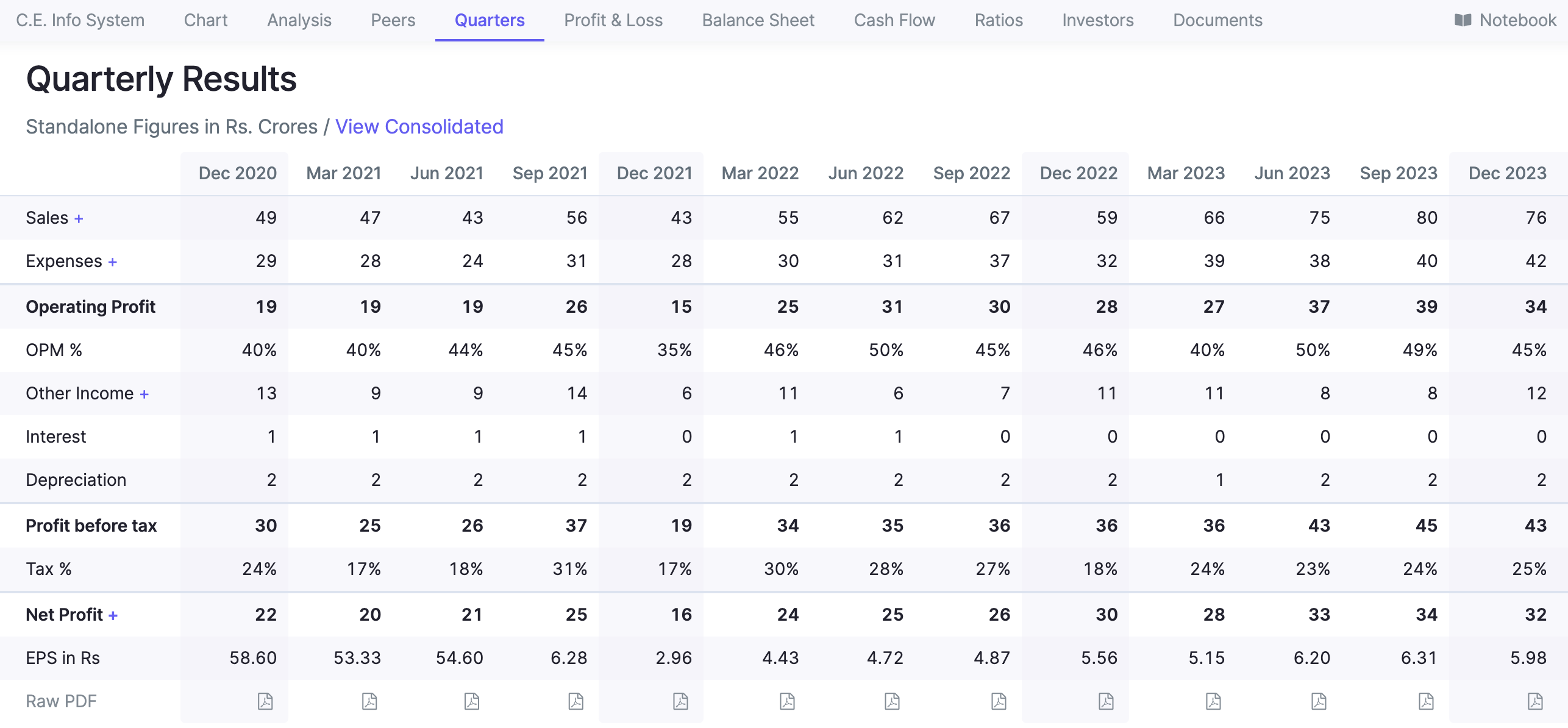

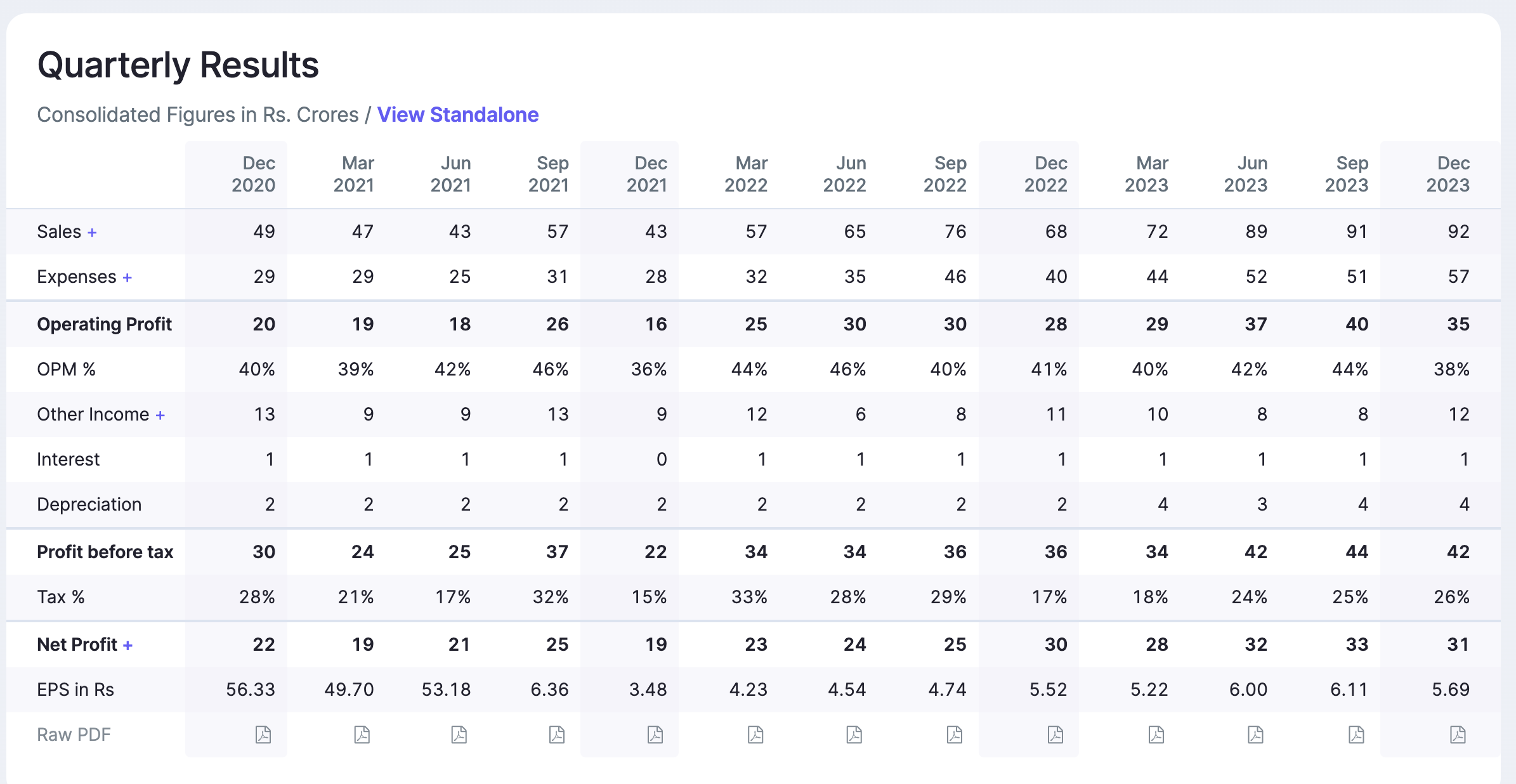

@Akshay_Jain2 1st point mentions milestone of INR 100 cr in quarterly income, but 2nd point says 92 cr for Q3. Arnt both these points contradictory?

Also, as per screener, revenue in Q3 is 76+12 cr = 88 cr.

So we have 3 different numbers for Q3 - 100cr, 92cr and 88cr.

1 Like

You are watching standalone numbers.

If you look at consolidated number total income is 92 cr + Other Income(12cr) which is total 104 cr.

In screener click on ‘View Consolidated’

1 Like

Promoters are starting company in a related field

Why would promoters start a company in a related field on their individual name and not on the name of the company ??

Plus, the owners also recently sold stake in the company… Another negative sign…

Infact the institutional shareholding is also low… Another negative sign…

Little is known about the management of the company… I hope the intentions of the management are clean…

7 Likes

when hearing management interviews or concalls, doesnt look like it…

The new company would be doing consulting business using the data of mapmyindia…

Consulting is a high profit business with no loss potential… I feel that is wrong as this profit should not go to the new unlisted company but rather to mapmyindia…

3 Likes

Yeah I too have these concerns with the company, why should promotors float a new company in related area, see 2 issues here:

- Related party issue

- Split of focus

2 Likes

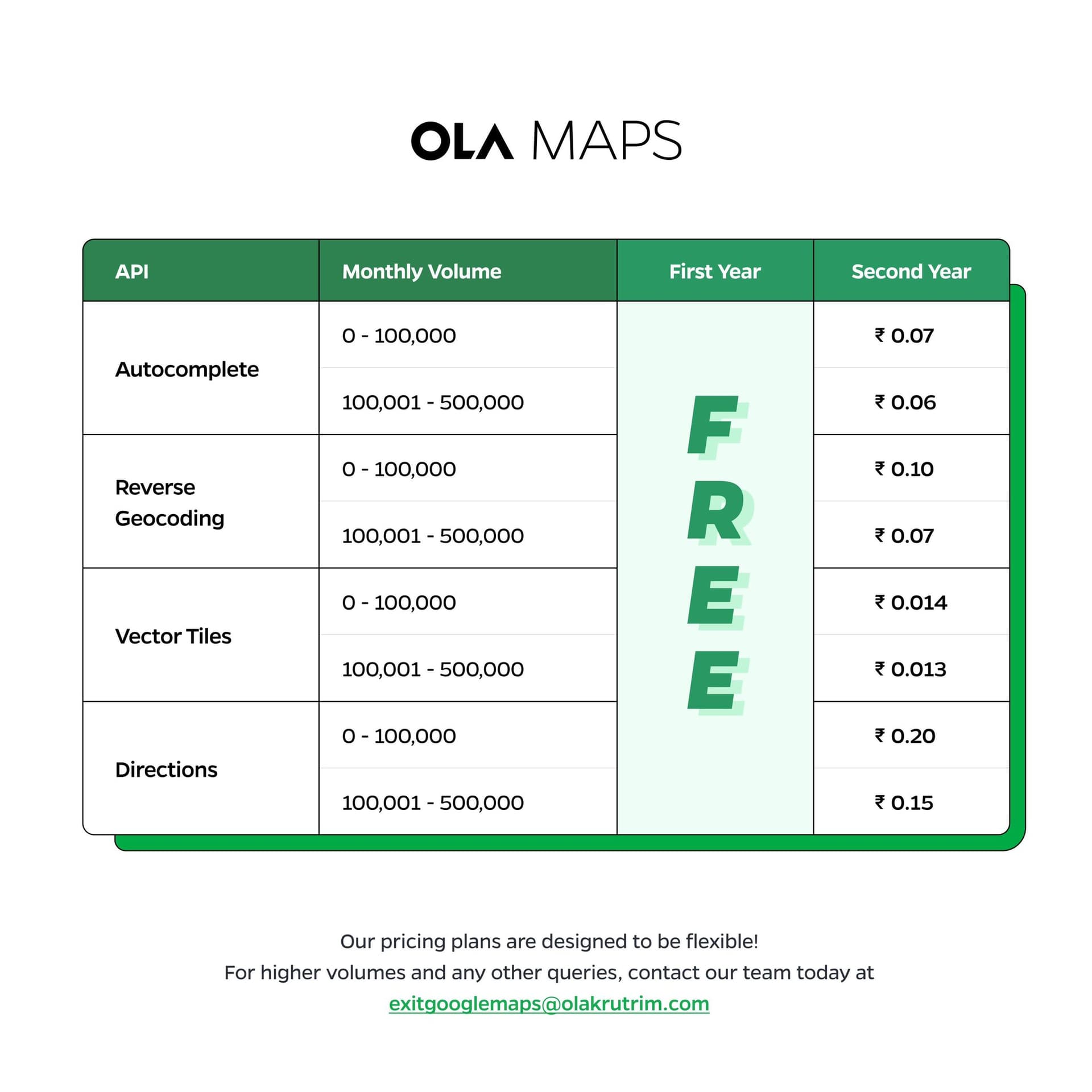

Currently Ola also entered into maps and providing one year free for developers.

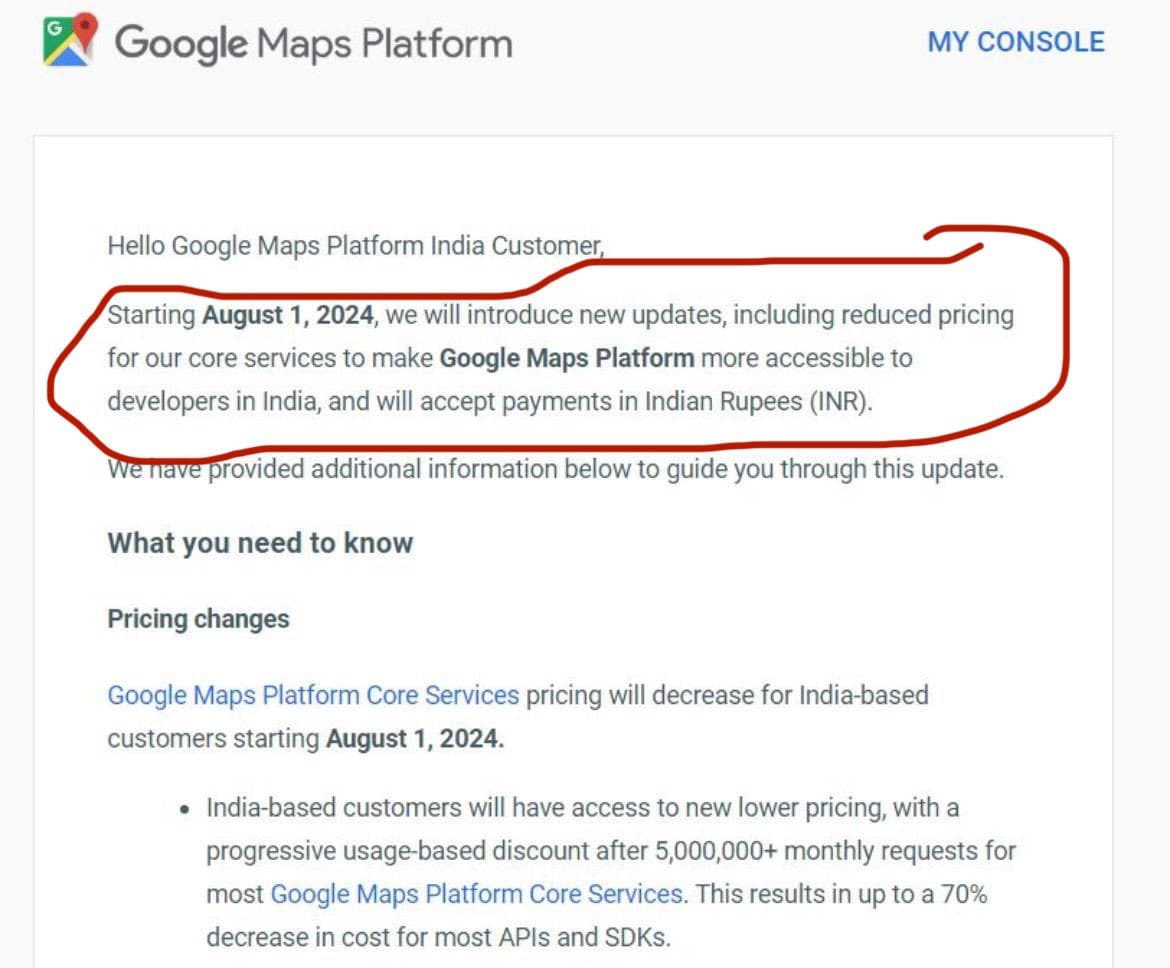

And Google maps decreased pricing for India-based customers up to 70%.

Will this impact MapMyIndia?

1 Like

I felt something is fishy when the promoter sold stake just couple of days after Goldman Sachs raised guidance, hence already sold half of my holdings when tis news got out. I think they saw ola and google maps trying eat their share in maps business beforehand. And these steps are goanna hamper the business of mapmyindia as maps business is their major contributor and other businesses like IOT still don’t add much to bottom line. Let’s see what management has to say on this. Eagerly waiting for concall to take a decision on remaining of my holdings in the company.

4 Likes

Three points -

-

ola maps is using open streetmaps vs developing their own maps solution. I dont think it will be scalable or will have adoption

-

Google maps pricing might have a v minor affect as google maps cant be used for commercial purpose

-

Selling stake of around 1% doesnt meaning anything is fishy. Promoters stake is > 51%. And 1% was sold for philanthropy.

4 Likes

Does mapmyindia develop their own map solution?

Can you please share source on ola using OSM, my hunch is ola will get real time traffic data from their fleet

4 Likes