For that will need to see subsidiary’s annual reports on the company’s website

1 Like

Promotor bought 320124 qty shares worth 17.83 cr from open market at ₹557 on 2nd Sept 2024

7 Likes

Recently researched this stock and my views -

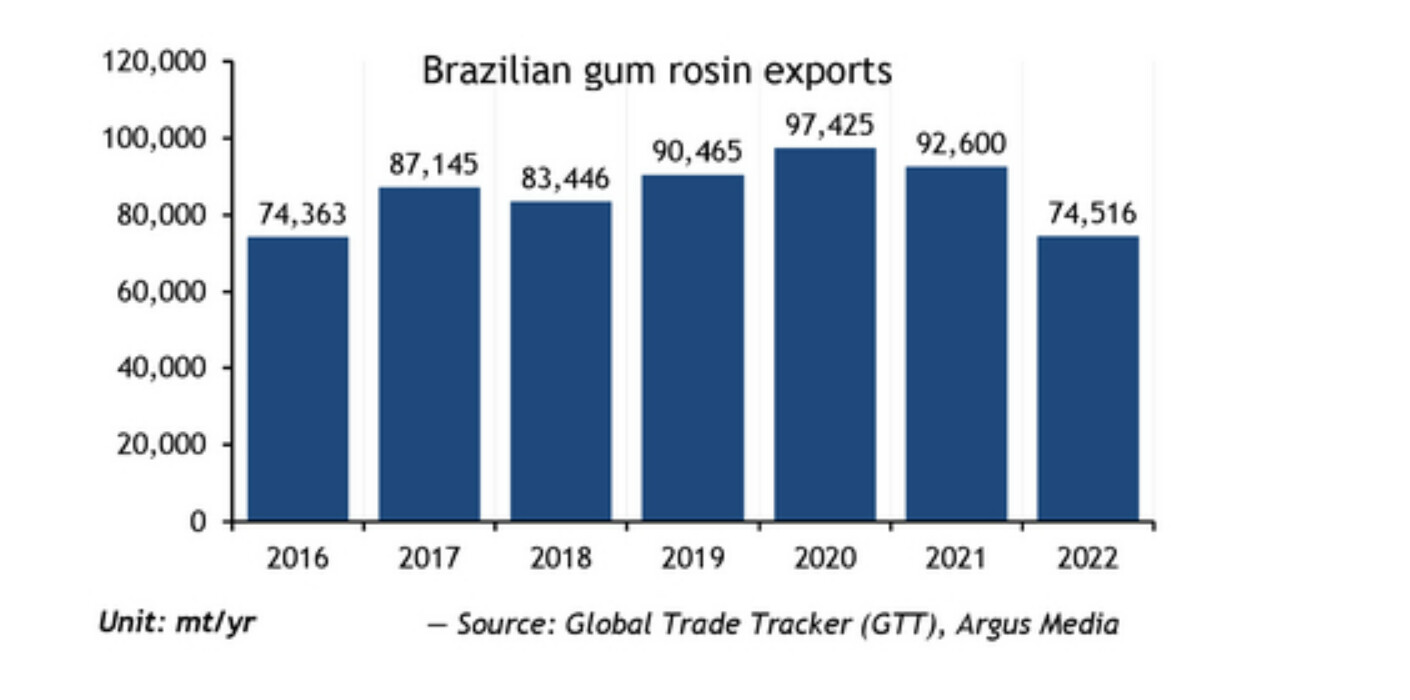

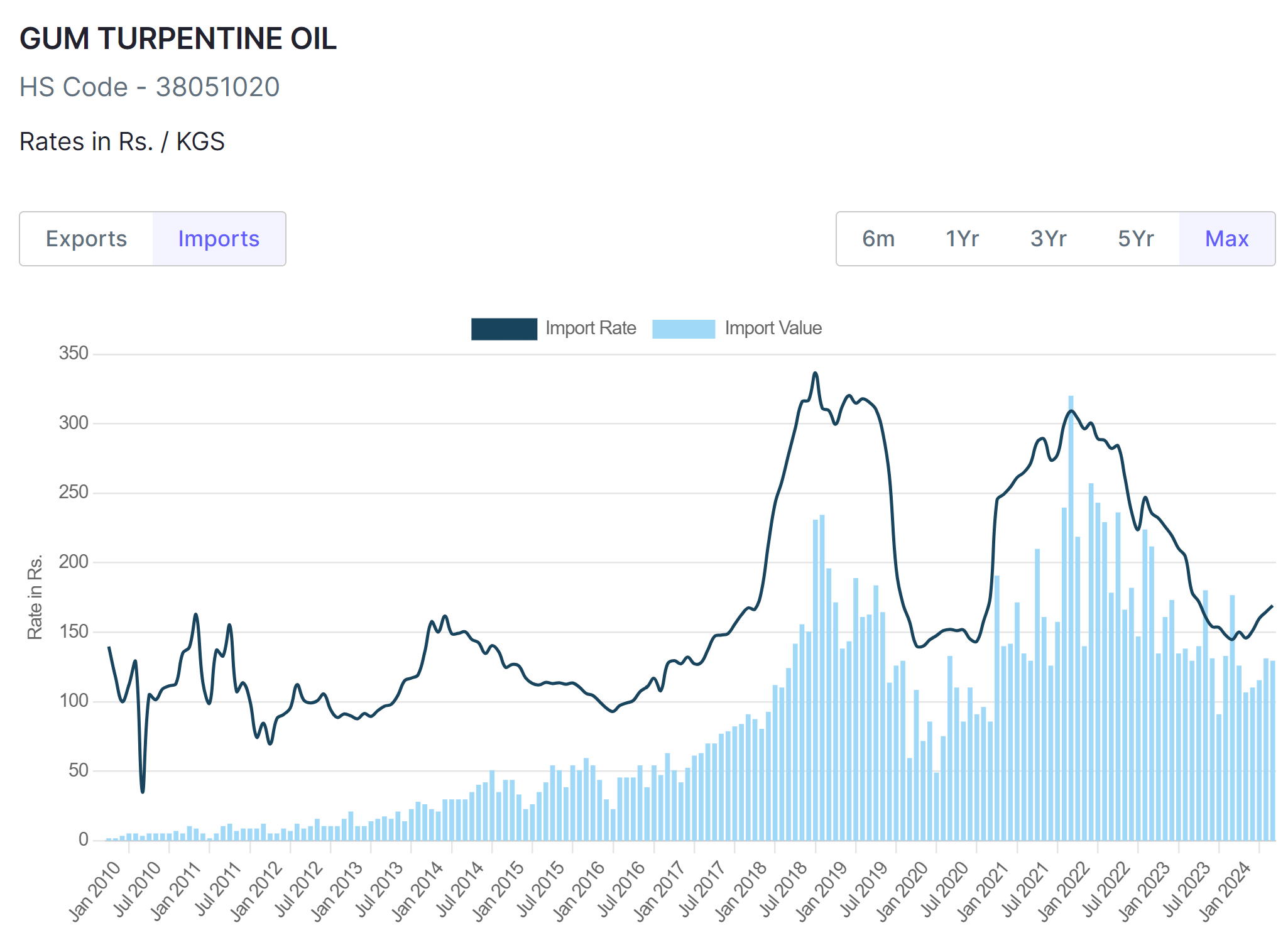

Pine Rosin (which comes from Pine tree tapping industry in Brazil) is going through a sharp downturn. Brazil pine oleoresin supply to fall further in 2024 | Latest Market News This has reduced supply of raw materials in the synthetic camphor supply chain. Lower Pine Rosin production implies lower Gum Turpentine which goes into Camphor production. This is why the cycle is turning. The last upcycle was from mid 2016 to mid 2018.

If we go through the article I shared above - “With selling prices sometimes below production costs throughout this year, many smaller pine oleoresin suppliers have ended forest lease agreements. Even if pine oleoresin prices increase, allowing for higher margins, it would take time for the producers which left the market to reactivate the forests and increase availability to the market. Reactivating a forest takes about six months as tappers need to prepare the extraction of the raw material months in advance, according to a source.”

Please note the exports of Pine Rosin now is the lowest in the last decade. Low exports coincides with cyclical bottoms in Camphor and Gum Turpentine prices.

Now, coming to why Mangalam Organics, the company’s retail products are growing at a rapid rate. A consumer brand with 160cr sales and growing 60% YoY is probably worth 500-700Cr in valuation, compared to the total market cap currently which is 550Cr. The company has also doubled capacity recently and capacity wont be a bottleneck in the upcycle. At peak capacity utilization in an upcyle, revenue will be ~800-1000Cr. If margins are similar to last upcyle which was around 20-25%, book value for Mangalam Organics will double in 2-3years. In last upcycle, the stock traded at 5-6x Price to Book Value at Peak. All this is contingent on the cycle turning for a few quarters.

17 Likes

Camphor prices are on uptick since start of this year and it is also understood that they are diversifying to B2C which should bring more certainity to business, then what explains muted Q1FY25 results (i.e. no growth and not a significant margin expansion). Would be great if anyone tracking this company can take it up. Thanks.

1 Like

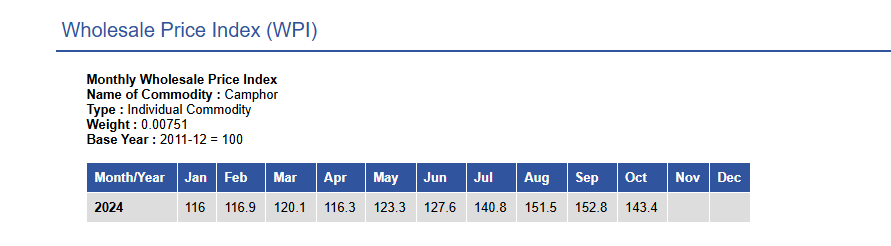

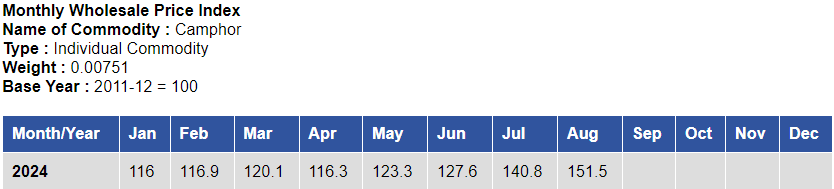

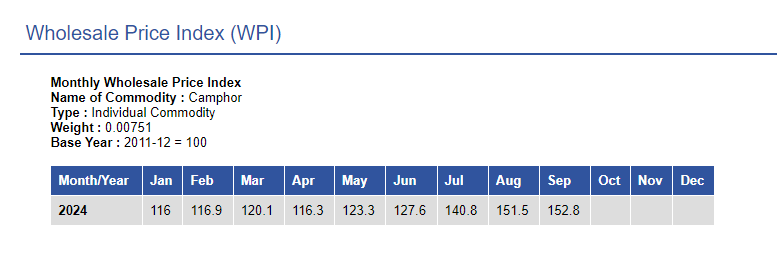

Based on data given above, camphor price index was ~120 in Q1FY25, ~160 a year ago and 215 two years ago. Only in Q2FY25 has the rise started happening.

1 Like

Thank You. Stock has been butchered, is it only because it moved to Stage 2 and it is low float? It has slipped below promoter latest buying price. Even that price didn’t act as support. If you are tracking this co, any thoughts on business performance for Q2 and rest of this year. Can B2C give a boost to their nos. and margins? Will camphor price increase help their margins? Would be helpful. Thanks

3 Likes

This may give a better perspective

5 Likes

It will be important to track inventory days here post Q2 results

1 Like

Do we see any correlation between share price and camphor prices month on month?

Trend reversed from Aug,23rd, promoter bought 4% of the companys mcap at the time, shakeout happened after making new high of 720 and currently back in stage 2

2 Likes

Inventory will be from Q1 when the average price was 20% lower than Q2

It might lead to inventory gain for sure. That would be camphor price impact on P&L. How much inventory they can reduce will reflect revenue growth, which will be dependent on B2C business performance and festive season impact.

1 Like

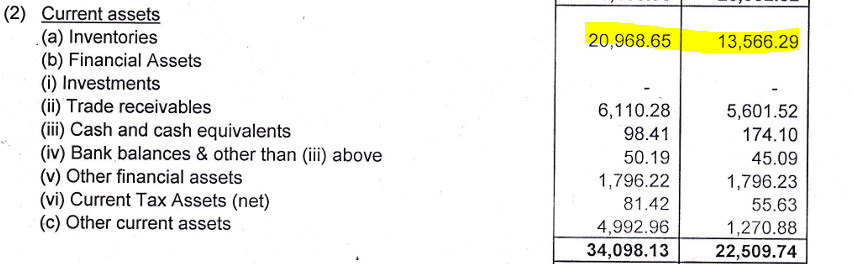

While the bottom-line looks decent YoY. The company is either loosing market share, or the demand has not picked up. Could there by any other reason for spike in inventory? (numbers are Mar 2024 vs Sep 2024)

3 Likes

Yes results don’t match up, neither increase in camphor price increase reflected in margins, B2C business improvement not reflected in topline / margins. High inventory indicates not enough demand. There is no con call conducted by management, so it is all guess work and hope at this point.

2 Likes

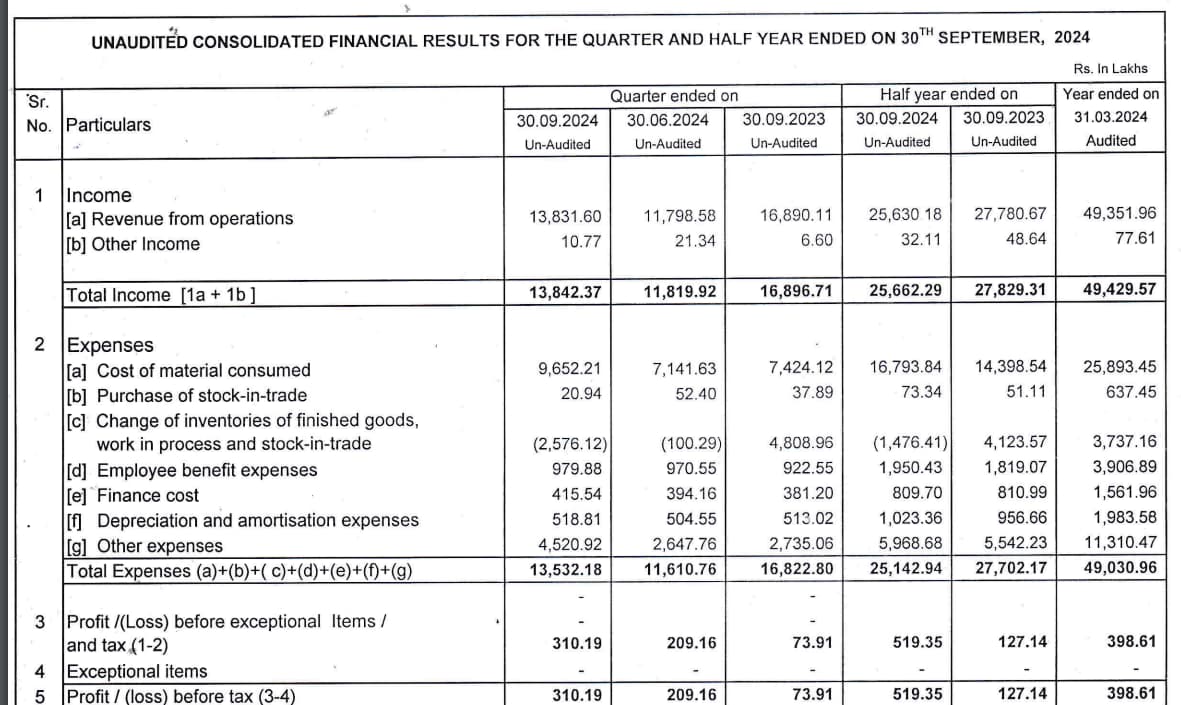

Consolidated revenues have declined in Q2 vs same quarter last year but gross profit is much higher at Rs 67 crore vs Rs 46 crore. Expenses have increased from Rs 37 crore to Rs 55 crore (hopefully in brand/marketing for B2C) so EBITDA is only slightly higher. Fixed assets are up 4X over the last five years so revenue growth should also show up at some point with higher volumes and increasing camphor prices.

Disclosure: Invested

1 Like

This might be due to inventory build up before festive season?

1 Like

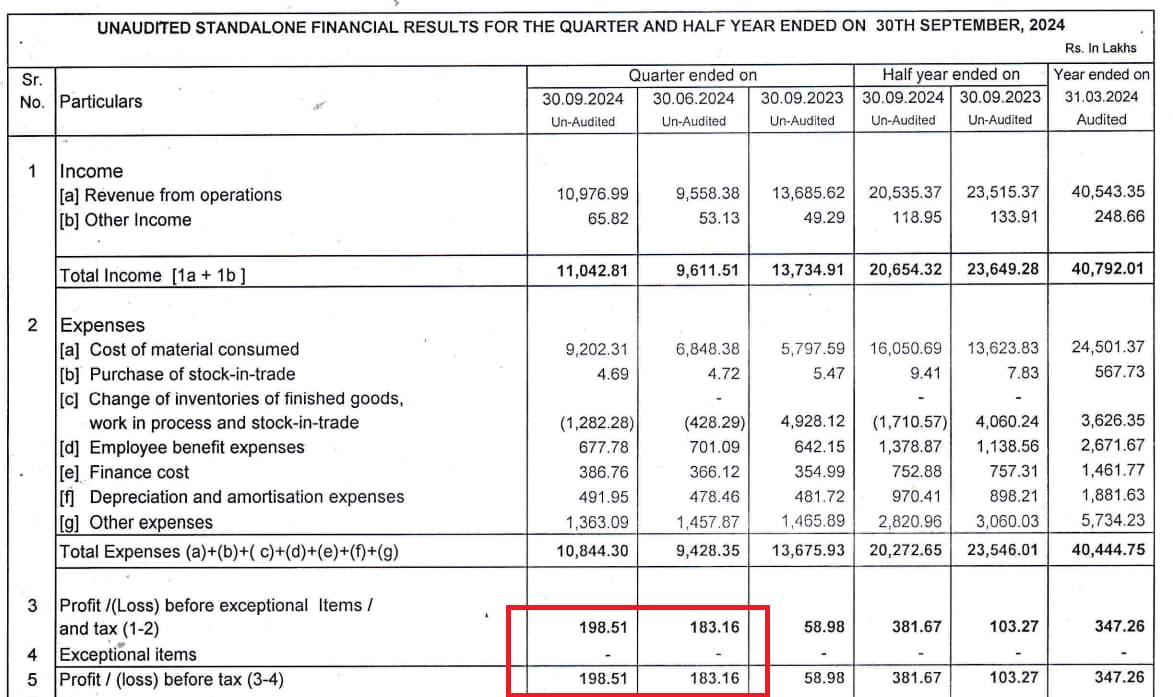

Results do seem underwhelming and probably driven by the underperformance in B2B segment. As per the investor presentation, B2C is not part of standalone financials. As per the results, standalone profitability has hardly budged from Q1Fy25 nos - INR 198 lakhs PBT in Q2FY25 vs INR 183 lakhs in Q1FY25. Probably couldn’t renew contracts / get hikes from large institutional buyers. Even presentation emphasizes primarily on RM cost reduction as profitability driver. Additionally, couldn’t come across if their plant is US FDA approved, something that players like OAL and Privi emphasis upon, wherein they manage some premium for quality.

1 Like