The Co. is a pioneer in the field of Pine chemistry. It is a chemicals manufacturer of Terpenes & Synthetic resins. Contrary to popular perception, these products are “natural”, derived from the Pine tree. They are not linked to crude & so are unaffected by its volatility.

Camphor is the primary product of the Co. It is a naturally derived product that burns completely, leaving no residue. It is widely used for religious purposes in the domestic market. It is also used for Hygiene & Medical purposes. Its potential is huge, if one considers the fact that while in India more than 90% of camphor is used for religious purposes, in China of the total camphor used, more than 90% is utilized for hygiene / medical purposes!

Camphor presents a large retail opportunity to the Co. to forward integrate & diversify into an FMCG player. It has come out with its own brands:

“Mangalam” – camphor tablets for religious purposes.

“Campure” – home care products like air purifiers & camphor sticks / cones

“Cam +” – health care products like pain relief spray, balm, nasal inhaler etc.

The Co. is aggressively marketing these products through various retail channels including e-commerce. I have bought these products from Amazon & personally used them! Here are links to the products at Amazon.

The Co. website also throws valuable insights.

http://www.mangalamorganics.com/

The Co., recently entered into a strategic alliance with a French Co. M/s. Les Derives Resinques & Terpeneques (DRT), wherein the Co.’s products will be manufactured under DRT’s technical guidance & DRT would use its global network to market them on a world wide basis. This arrangement can potentially catapult the Co. into a totally different league in a relatively short period of time. While the Co. is in the process of getting product approvals in the export market, going by the growth in sales with improved profitability seen in Q1 of the current year, it’s quite possible that the Co. may have started domestic supplies to DRT. (Link to DRT’s website https://www.drt.fr/en.html )

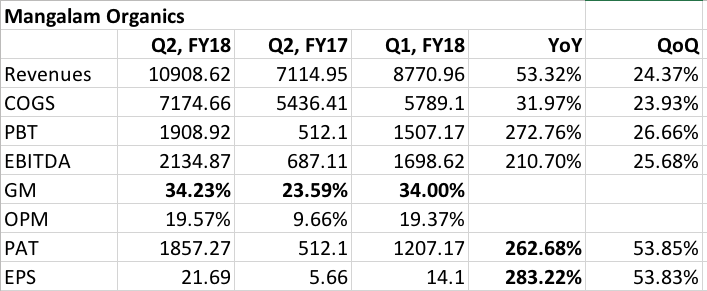

Mangalam Organics has done sales & PAT of 88Crs & 12Crs respectively in Q1 of the current year. The quarterly results chart is given below. The feedback from a few shareholders who attended the AGM held recently is that these margins are sustainable going forward. In fact , historically Q1 has not been a strong qtr. The Co. could end up doing Sales & PAT of about 350Crs & 42Crs for the current year 2018-19. The current market cap of the Co. is about 308 Crs. with Debts of about 40 crs. The Co. is still sitting on spare capacity & any future capex is still about 24 months away.

Concerns: The game changer for the Co. is the tie-up with DRT, which is still at an early stage. That is one concern, though the arrangement is a win-win for both as DRT also benefits by having a far cheaper manufacturing base in India. Another concern is that the diversification into value added products is still in its infancy & could go awry.

| (in Cr.) | Jun-18 | Mar-18 | Dec-17 | Sep-17 | Jun-17 | FY 17-18 |

|---|---|---|---|---|---|---|

| Income Statement | ||||||

| Revenue | 87.71 | 56.42 | 78.36 | 71.15 | 38.30 | 244.24 |

| Other Income | 0.27 | 0.49 | 0.26 | 0.28 | 0.22 | 1.25 |

| Total Income | 87.98 | 56.91 | 78.62 | 71.43 | 38.53 | 245.48 |

| Expenditure | -71.53 | -49.41 | -71.85 | -65.37 | -34.97 | -221.59 |

| Interest | -0.54 | -0.30 | -0.40 | -0.81 | -1.04 | -2.56 |

| PBDT | 16.45 | 7.50 | 6.77 | 6.06 | 3.56 | 23.89 |

| Depreciation | -1.37 | -1.83 | -1.74 | -0.94 | -1.00 | -5.50 |

| PBT | 15.07 | 5.68 | 5.03 | 5.12 | 2.56 | 18.39 |

| Tax | -3.00 | -2.72 | -1.21 | – | – | -3.93 |

| Net Profit | 12.07 | 2.96 | 3.82 | 5.12 | 2.56 | 14.46 |

| Equity | 8.56 | 9.05 | 9.05 | 9.05 | 9.05 | 9.05 |

| EPS | 14.10 | 3.13 | 4.21 | 5.66 | 2.83 | 15.82 |

| CEPS | 15.70 | 5.28 | 6.14 | 6.69 | 3.93 | 22.05 |

| OPM % | 18.75 | 13.30 | 8.64 | 8.52 | 9.29 | 9.78 |

| NPM % | 13.76 | 5.24 | 4.87 | 7.20 | 6.69 | 5.92 |

Disc: Invested.