I have good reasons to believe Mangalam will be out of docks now and would start benefiting from the investments it made in B2C biz. Shift in retail is never easy but if done well, always profitable.

Keeping fingers crossed, I tried the room freshner did not find it to be great . Ordered other stuff too delivery awaited.

Invested

How long since you ordered and awaiting delivery? invested as well and built more positions.

Tried all the products, the products appears nice with the signature fragrance of camphor

This new line will re rate the stock

Margin expansion

Top line expansion

Improvement in roce

And more drivers

Invested

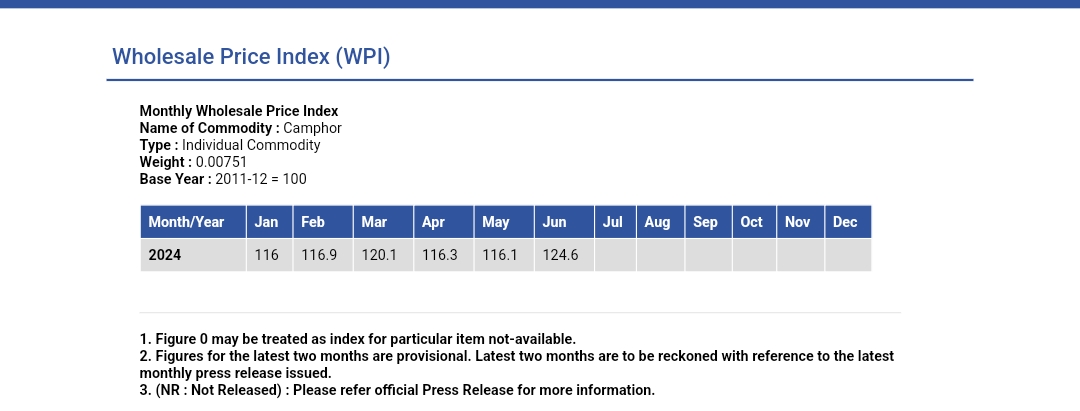

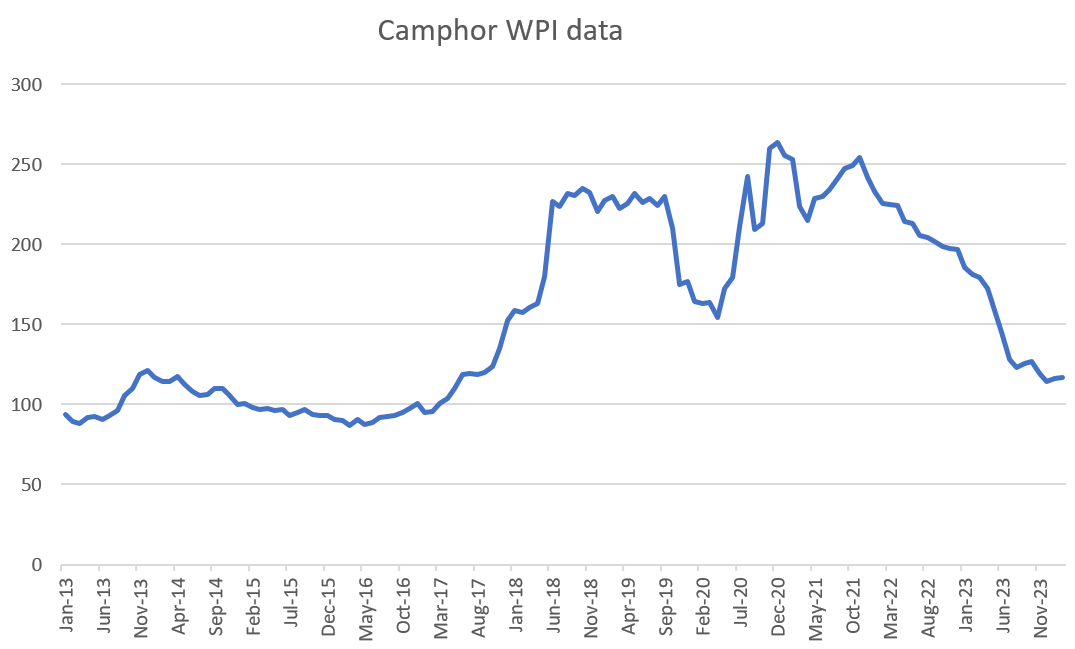

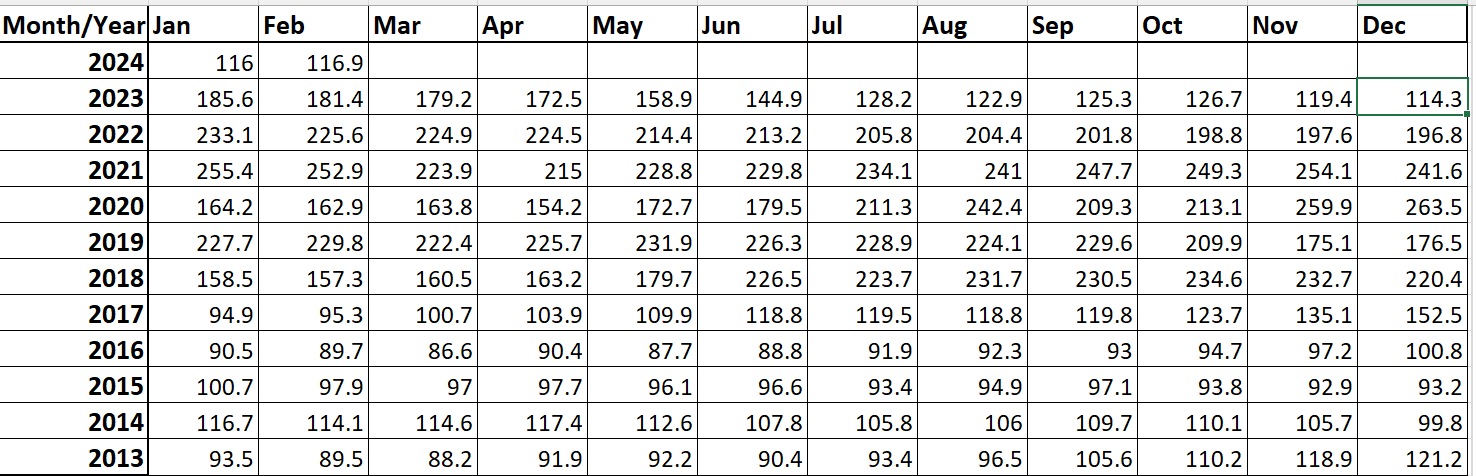

Updated data of Camphor WPI. WPI having bottomed out at 114 Dec 23 have started to move up. However hard to say if the upmove is transient or sustained

The 3 listed camphor companies (mangalam organic, kanchi karpooram and oriental aromatic) hit upper circuit yesterday. Any recent good news for the industry?

The story here is that most of the key RM for Camphor comes from imports, specifically from Brazil.

Due to poor prices, pine farmers chose to prepare fewer trees for pining in this crop cycle. As a result, inventories of this RM have fallen, and from April, demand has suddenly come back for aroma chemicals.

Based on my best guess, camphor WPI should be around 130-135 in April, but the high demand season for camphor begins from July onwards. If current RM pricing trends continue, we could see a very good price cycle for camphor.

Disclosure: invested in Privi, Mangalam and Kanchi. These form some 10% of my portfolio. Transactions in the last 30 days.

Can someone share the gum turpentine realisations as of now ? Margins for camphor makers depend on gum turpentine realisations.

Price resumed downward trend or its stabilizing at 115-120