@RajeevJ thank you sir for providing the details.

Camphor’s northward journey continues! Perhaps now quoting at fresh all time high.

Good times in store?!!

14 Likes

For some reason its not reflecting in the quarterly performance of Mangalam. Where as its was very well visible for kanchipuram. Does any one know the reasons?

1 Like

Is there any possibility of hiding actual numbers for the purpose of increasing promotors holdings from open market  ? So far promotors could raise up to 55 % and they are increasing their holdings for last two years at maximum yearly permitted limit i.e 5% . Still they have room to increase the holding .

? So far promotors could raise up to 55 % and they are increasing their holdings for last two years at maximum yearly permitted limit i.e 5% . Still they have room to increase the holding .

Even online sales contributes only 5% of topline, products are very visible in almost all platform like Dmart,Jiomart,More,Bigbasket,Amazon,Flipkart.

Interestingly they are introducing new products like camphor based mosquito repellent liquid , sanitizers etc… Factors like present capacity , price realization ,online presence , entry to aromatic chemicals all looks so promising to this company

But nothing is reflected in numbers and share price so far . let us wait n watch .

2 Likes

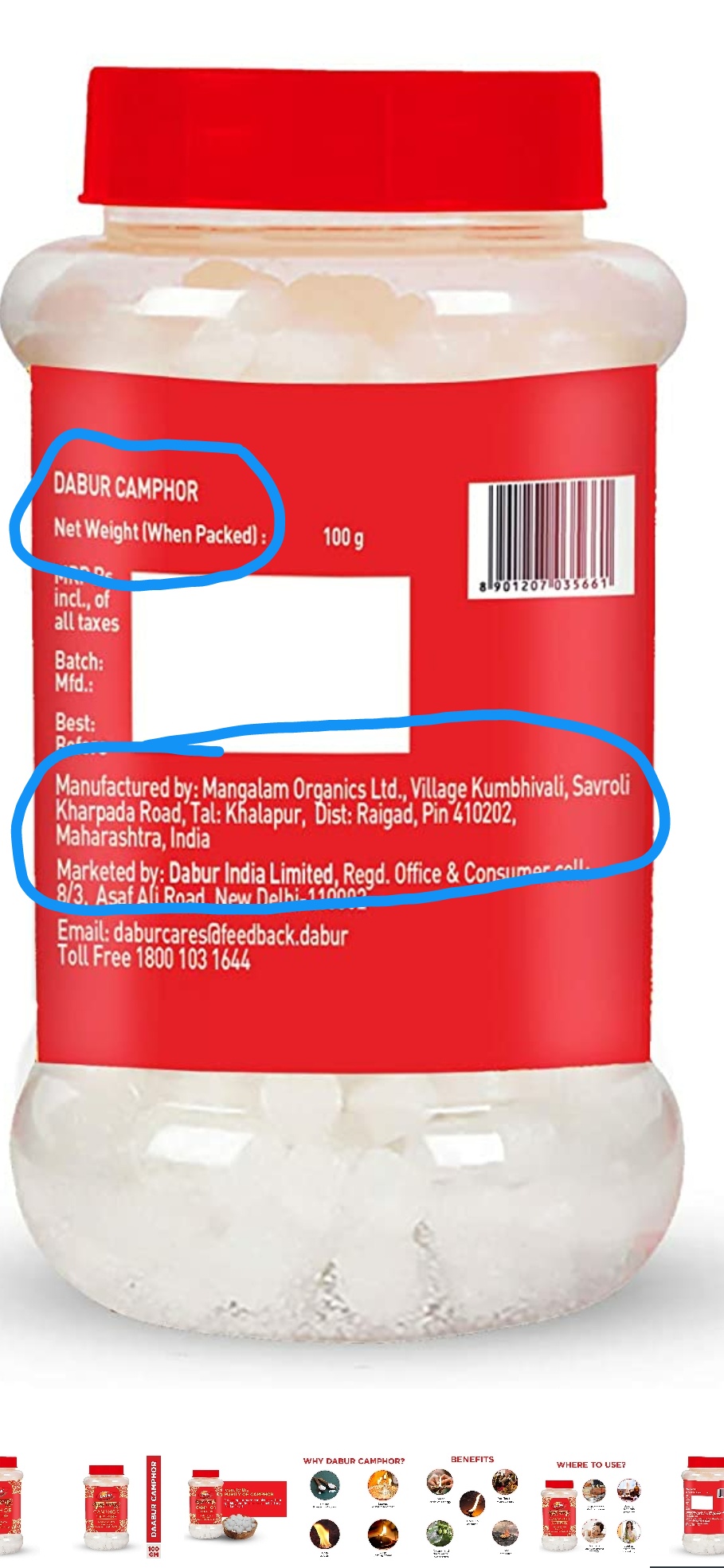

Emami is one the major clients of Mangalam for Synthetic Camphor.

Products such as Zandu Balm which uses Camphor as a raw material is getting huge demand in rural areas.

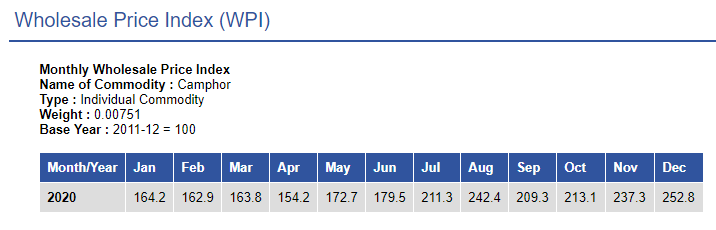

It is also reflecting through Camphor prices which are all time high.

It can convert into numbers for Mangalam in the December 2020 quarter mostly.

Eagerly watching December 2020 quarter.

7 Likes

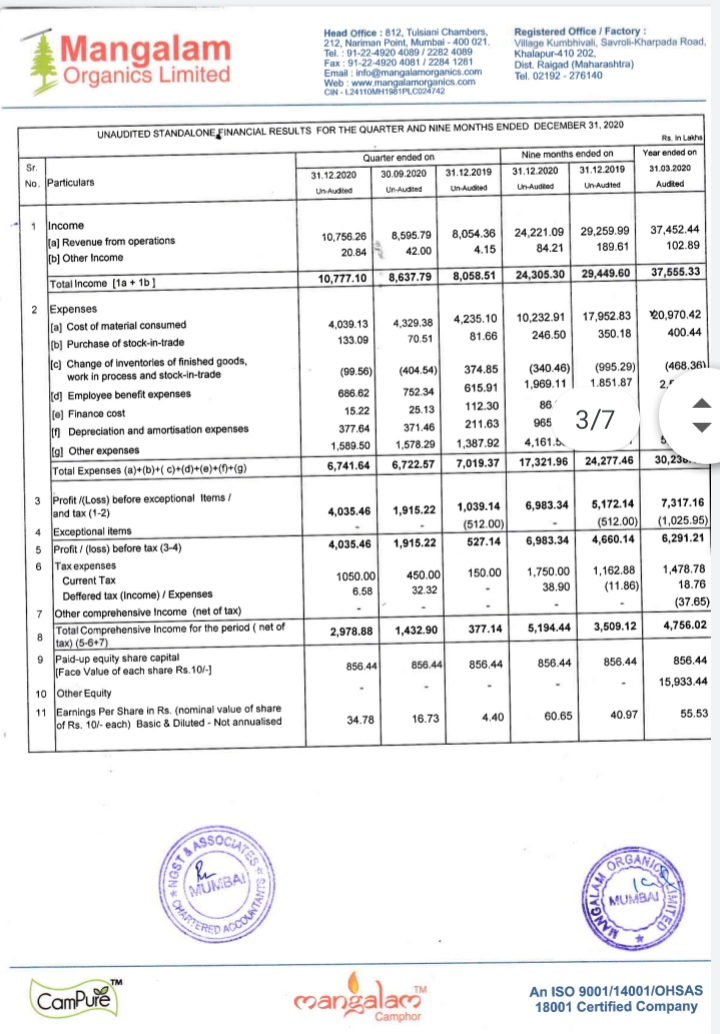

Excellent Q3 numbers by Mangalam. Camphor price increase is clearly visible in results.

Revenue up by 33% at 107.56 Crores -YoY basis

PAT up by 666% at 40.35 Crores -YoY basis

PAT up by 107% at 29.78 Crores -QoQ basis

EPS at 34.78 up by 690% -YoY basis

EPS at 34.78 up by 108% -QoQ basis

Hope PE will get re rated soon. Awaiting views from @RajeevJ sir and @Pranshinv

11 Likes

Investment thesis/stories are converting into numbers finally !

| Particulars | Sep-18 | Dec-18 | Mar-19 | Sep-20 | Dec-20 |

|---|---|---|---|---|---|

| Sales | 109.09 | 121.43 | 106.4 | 85.96 | 107.56 |

| Expenses | 89.01 | 77.13 | 78.85 | 63.26 | 63.50 |

| Operating Profit | 20.08 | 44.30 | 27.55 | 22.70 | 44.06 |

| Operating Profit % | 18% | 36% | 26% | 26% | 41% |

Sales - There is lot more scope for sales to increase from here as the demand for camphor is intact. Company has not yet utilize the capacity expansion which they have increased in October 2020 from 550 MT/ month to 1250MT/month. The above sales is very much achievable in the existing capacity of 550MT/month.

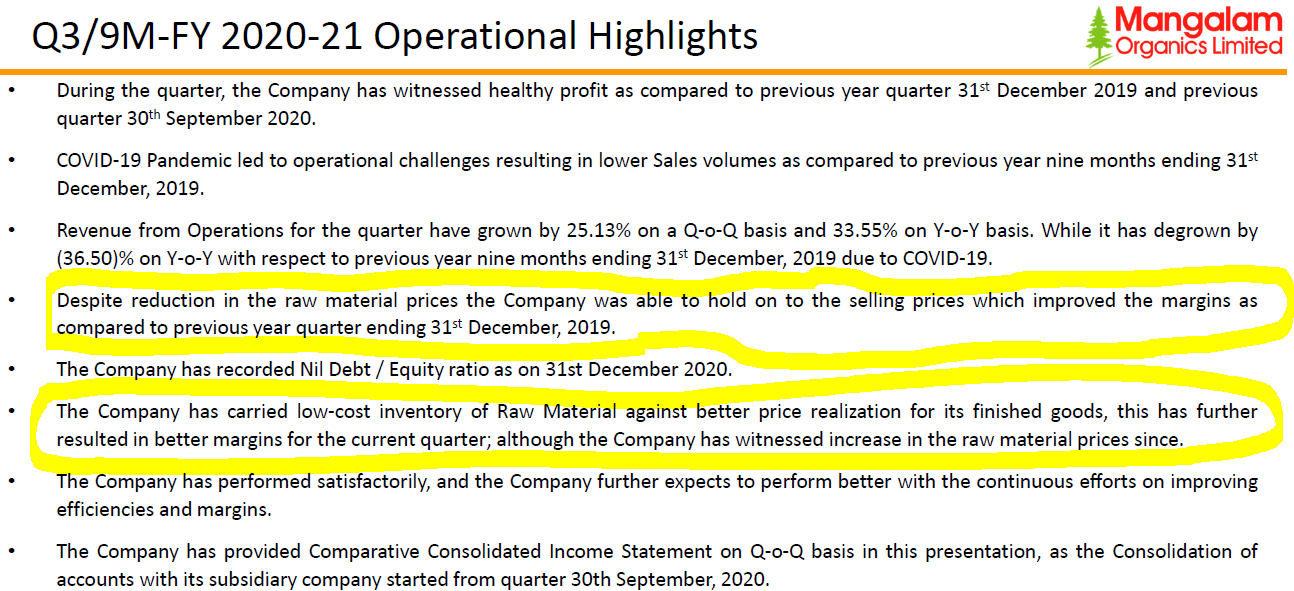

Margins - Operating Profit /Margins are the highest in any particular quarter the company has ever achieved in its lifetime. One of the reason for increase in margins is the demand they are getting in the retail segment /or B2C sector and other derivatives products growth and other reason can be the raw material inventory carrying at lower prices.

Sales can be increased considering capacity utilization and margins will correct a bit but still it will get offset through increase in sales. Even though margins will correct 8-10% from here still margins are very good .

9 Likes

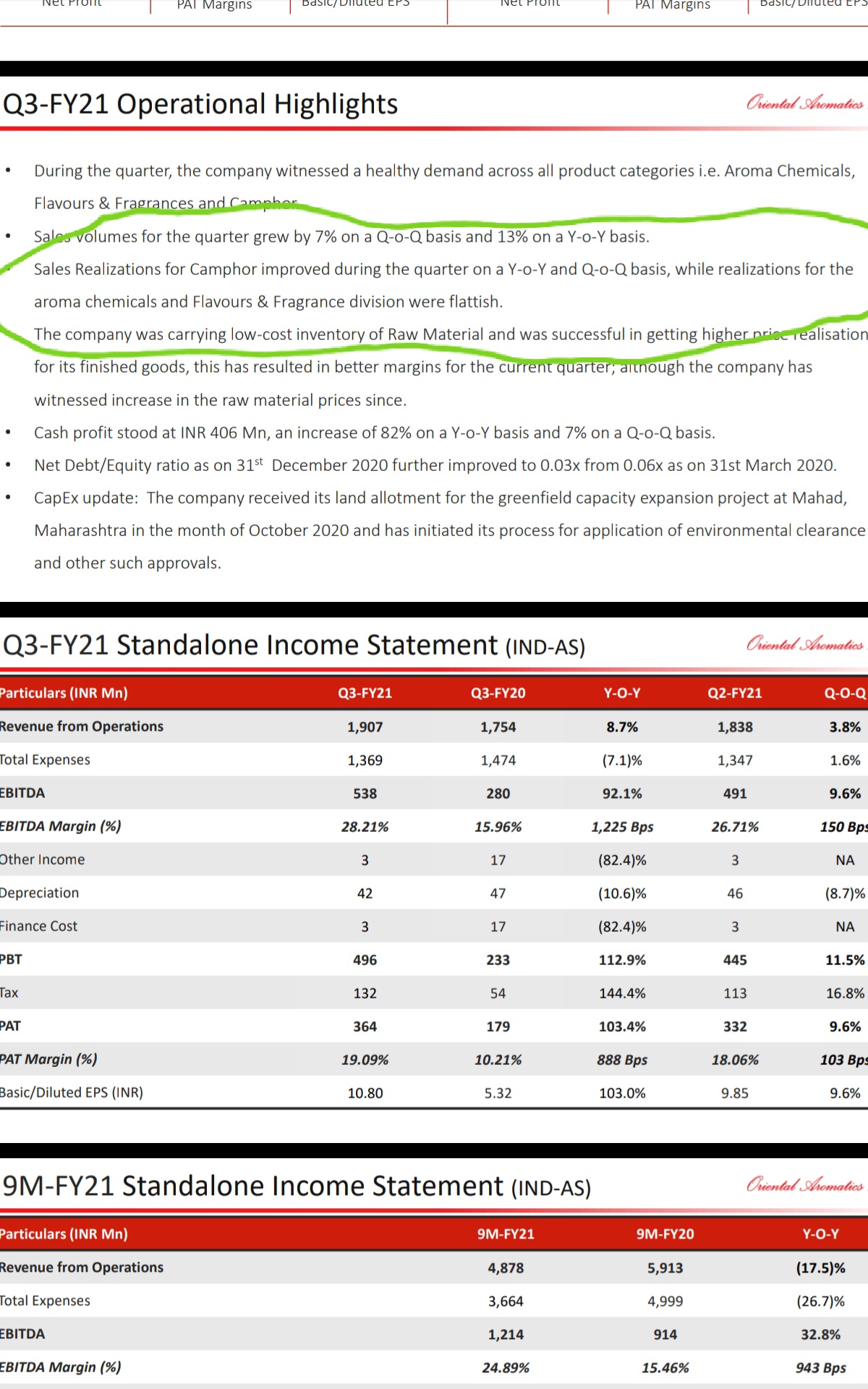

Excellent margin performance and as much as we wish they will normalize soon.

Low price carrying inventory seems key reason to high price realization- similar is the case for oriental aromatics - they were transparent in calling this out. At the same time they have hinted at raw material price on uptrend as well - it will be key to monitor camphor and raw materials prices hand in hand to get combined picture.

Sustainability of sales growth is key , unable to get that confidence yet, like many of things here( promoter buying, better communication, capacity increase, retail brand push) and it will take some time to get that consistency in place.

Exited in March meltdown in losses, re-entered in Q2. Plan to book some profit around ATH.

7 Likes

While the results are quite impressive , I don’t see any investor presentation this quarter

It would have been good if the management had clarified on the progress of the B2C aspects or even a breakdown of the sales pie would have helped.

It would be also nice if someone on this thread can comment on the reason of the rise in camphor prices and hence help us deduce where we are in the camphor cycle.

Disc : Invested

Mangalam Organics came out with a good set of Q3 numbers. As mentioned by the mgt. at the AGM, the impact of the expansion will only begin to reflect in the numbers from Q4 this year. In Q3 the Co. was still in the process of getting back to pre Covid levels in terms of volumes. The volumes were probably higher a year ago when it did Sales of 120 crs in Q2 of last year when camphor prices were lower. This means that Sales could potentially double from here in the next couple of qtrs with increased capacities coming into play.

The Camphor prices have been on a steady rise in the last couple of years with normal periodic corrections along the way, but the trajectory is clearly upwards. In this scenario it is rather unlikely that the prices could revert to levels of a year ago. That is the bear case scenario, but even if that be the case, the higher Sales would more than compensate for higher profits.

Who is to say that prices could not go higher or settle at the current levels which is an equally likely possibility. In such a scenario the numbers could get far more interesting than in the bear case. I leave it to individual investors to extrapolate them!

The trading window for the Promoters has also opened. They have till end March to increase their stake through creeping acquisition if they are indeed looking to do so as they did in the last two years.

12 Likes

Investor Presentation Q3FY21 results.

Highlights of Q3FY21 performancemangalam q3fy21 investor presentation.pdf (1.8 MB)

6 Likes

Thanks for starting this thread and bring all top quality contributers here. Hope we are moving towards achieving the purpose.

Both Kanchi and Mangalam doubled the capacity in almost similar timeframe and other unlisted big players are also there in same business. What’s the main reason for this huge demand of camphor? probably unorganised small companies forced to shutdown their business during pandemic otherwise some shift in application of camphor like pharma,hiegiene etc…? With the added capacities in market . Do you think this margin is sustainable ?

2 Likes

Difference between standalone and consolidated revenue is only 5 lakhs. Does that means Campure brand is contributing only 5 lakhs in revenue? and Campure is currently making 11 lakhs loss?

2 Likes

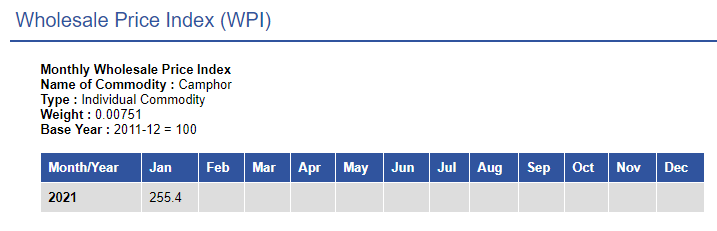

Camphor prices continue their upward movement. Normally prices start to correct after the festive season, but they continue to inch higher this year. The change seems more structural.

22 Likes

Signs of sustained volume growth can beat the operators and usher in a sustained rally to correct the valuation mismatch. Outtake of pharma grade camphor is going to be the key. Retail/FMCG play is a pretty long term one, however private labeling is promising for short to medium term.

Disc: invested.

3 Likes

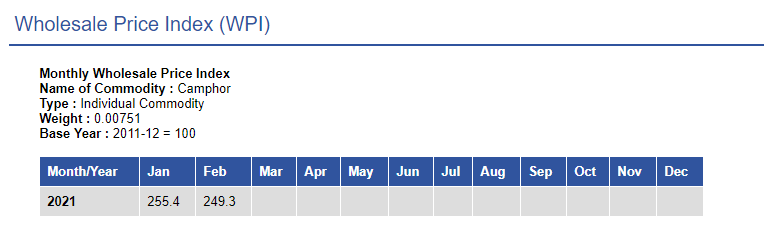

@RajeevJ Would you be able to extract Feb21 prices? Not sure from where do you fetch it from…

It is not yet updated on https://eaindustry.nic.in . You can search for WPI at the bottom left section.

Disc: Invested.

2 Likes

Camphor pricing continues to be strong and seems to be stabilizing around the 250, despite the fact that the festive season is behind us.

13 Likes

Thanks Rajeev.

During Investor Discussion for Kanchi, Management told that the raw material price have shot up significantly, which would be impacting the margins.

Can we also find the raw material price movement during the period?

1 Like