Circuit Filter for Mangalam Organics Ltd changed from 10 % to 20% w.e.f. 08 October 2020 as per BSE link. https://www.bseindia.com/markets/equity/EQReports/sur_Price_monitoring.aspx?expandable=6

2 Likes

Oriental Aromatics concall (on researchbytes) says that camphor was major driver of revenue as well as margins in Q2 with both RM prices softening and demand rising as people praying more and more during the trying times of COVID-19. Q2 may turn out to be stellar for Mangalam as well, if trends are secular.

2 Likes

Import Data shows that Gum Turpentine import price per kg is reduced by 50 % in FY-21-Q2 , when compared with FY-20-Q2 prices, and also the imported qty has increased by 7 % on yearly basis, which indicate that the industry is showing growth in demand, so one can expect decent margins for Mangalam in current qtr.

1 Like

Further, Oriental NP margin was around 9 % in Q1-FY-21 V/s 16 % NP Margin of Mangalam in Q1, both on lower sales base .

In Q2 , Oriental NP Margin was 17 % , almost doubled, on sales becoming normal , considering that it has a more diverse product portfolio. So on similar basis , NP margin of Mangalam can be significantly higher in case the sales returns to normal levels. Going by the concall of Oriental, there is no reason why Mangalam should not have normal sales in Q2 , as the industry trend has been positive.

7 Likes

Attaching the transcript of the Oriental Aromatics Earnings Concall Highlights.

As mentioned by @saket105, the Camphor market is doing rather well for itself & the good times look sustainable.

6 Likes

The top line and profits have almost doubled quarter on quarter and it is trading at cheap valuation. Seems like there is tremendous increase in demand for camphor.

1 Like

@sarthakkumar19_

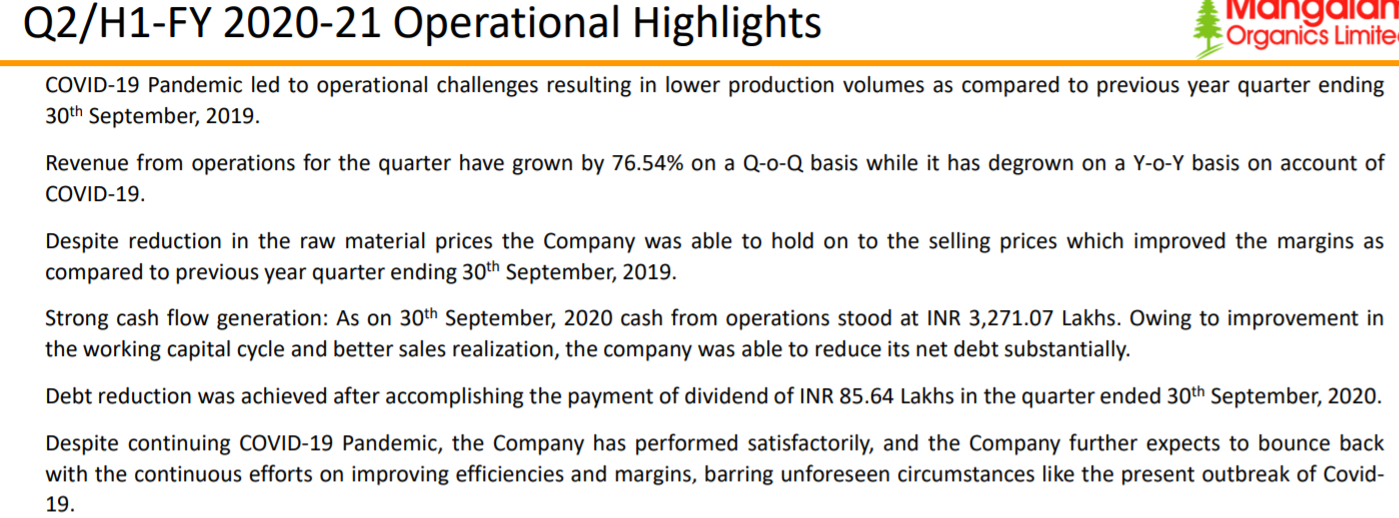

I was expecting a higher top line & thereby a better set of numbers as I was confident of the margins being sustained. The Investor Presentation prepared by the Mgt. is very useful in understanding the results. I am posting the relevant portion below. The Covid situation is only gradually improving even though the lockdown has ended. Hopefully, the improvement will continue & gather momentum in Q3.

Our markets tend to over emphasize the importance of the previous corresponding quarter & if the current quarter is relatively subdued, its taken to be a not so good set of nos. The flip side is that the Co.'s previous Q3 was very subdued & by the same token the Q3 numbers of the current year, whenever they come, will be perceived to be very good!

8 Likes

Key Takeaways :

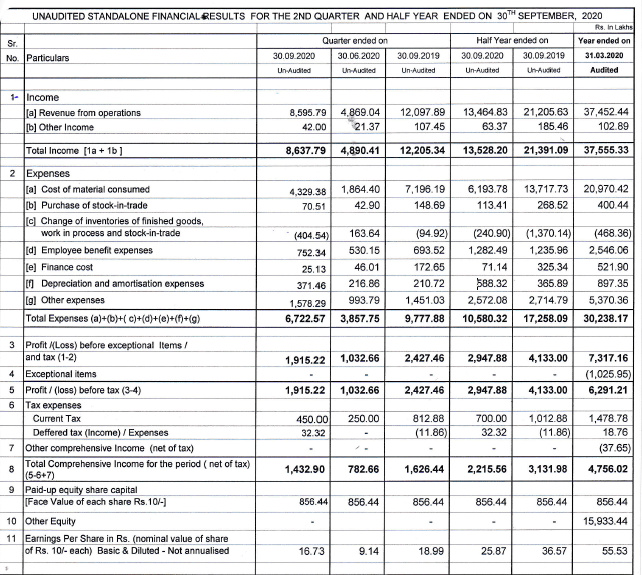

- Top Line lower than expected.Q2 2020 is ~29 lower than Q2 2019.

(June’20 is not the right quarter to compare Revenue, considering Lockdown. Sep’19 is better comparative)

-

Increase in Depreciation over Q1 2020 is ~ 1.54 Cr. Does not contribute to cash outflow. Hence positive.

-

Finance Cost has reduced by ~45% over last Qtr. Entire benefit is contributing to profit and might result in better dividend, if no further expansions planned.

-

Margins are in line with Q1 2020.

-

Reduction of debt has been a highlight this HY. Reduced from 17.4 Cr to 0.4 Cr. This seems to be during the end of Qtr, so further reduction in Finance Cost can be expected.

During these unprecedented times, where most of the businesses are struggling to manage Working Capital, Management has managed to Reduce Trade Receivable, increase Trade Payable and yet presented an increased Cash Flow. This is after reduction of debt to historical lower levels. Working Capital Management has been really excellent and needs to be appreciated.

Now, the eyes should be at Sales for coming Quarter, as that’s the only section where Management needs to focus. Remember, they are yet to utilize their capacity.

Disc : Invested.

6 Likes

Increasing demand of pharmaceutical industry is anticipated to prove an opportunity for the global synthetic camphor market. An increase in the production of paints & coatings has impacted positively on the use of synthetic camphor in the LAMEA region.

1 Like

Mangalam has again changed the Product Mix and got the Consent approval from MPCB vide dated 11th November 2020 which overrides earlier consent order 08.05.2020 which has been mentioned in earlier thread.

Camphor Capacity increased from 550 MT/Month to 1250 MT/Month. Growth Potential becomes very huge considering the prices of camphor. Largest capacity in Industry with big clientele

Sodium Acetate capacity also increased from 500MT/Month to 1250 MT/Month.

Attaching herewith MPCB order for reference.MPCB order 11.11.2020.pdf (3.7 MB)

12 Likes

Kudos to @Pranshinv for digging out this important data point .

Apologies for the somewhat basic question,

Where can we track the input raw material prices and current camphor prices ?

Any pointers to these will be helpful !

Regards,

Abhijit.

4 Likes

Thanks @Pranshinv

- They have got revised permission. But what is their capacity to produce?

- Do we know current production vs max limit provided by MH POLLUTION BOARD?

Appreciate your help

Thanks

1 Like

Camphor: One of the Few FDA-approved Chemicals with Natural Medicinal Properties

Being an FDA-approved chemical, camphor is gaining immense demand in most of the medicinal, healthcare products, which is predominantly driving growth of the camphor market.

Pharmaceuticals Industry will Create Lucrative Opportunities for Camphor Market Players

6 Likes

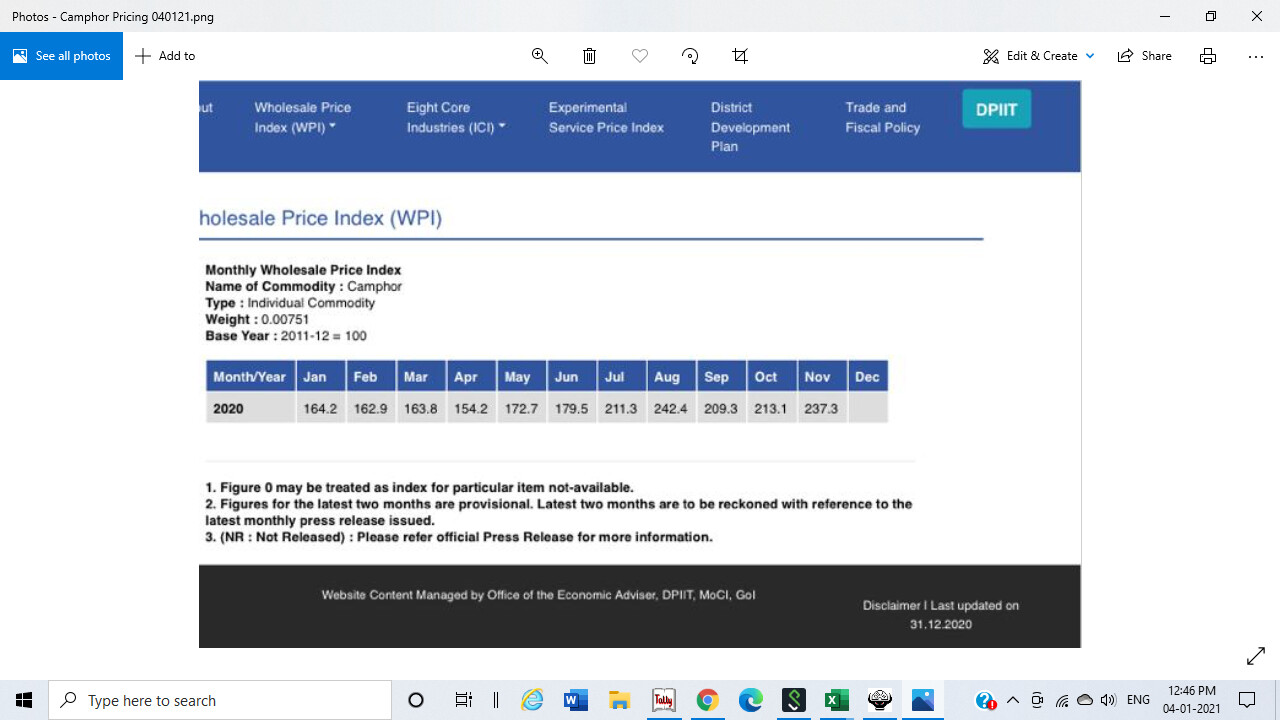

Camphor prices are quoting near all time highs, so all camphor manufacturers should have a very decent Q3, hopefully with the benefit of increased capacities. AS correctly mentioned by @Pranshinv, the capacity increase from 550 MT to 1250 MT could come be a game changer for Mangalam.

It would be great if the Mangalam mgt. came forward and notified the exchanges of all MPCB orders & changes in the product mix so that the entire investor community could benefit. Lets hope that greater transparency is part of the positive changes that Mangalam mgt. is trying to bring about in the Co.

11 Likes

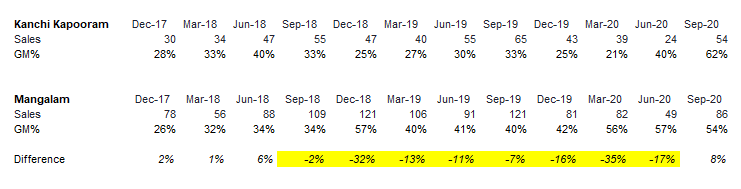

Gross margins for MOL have been consistently higher than Kanchi Kapooram since Sept-18. This could be explained by backward integration, higher B2C mix etc.

But in the most recent quarter, KK had a GM of 62% which was 8% higher than MOL. Could anyone throw some light on what would explain such a huge jump in gross margins for KK?

4 Likes

Kanchi’s material cost was 8% lower than Mangalam in the last quarter. I understand that Kanchi’s coming quarters will be better due to cost competitive advantage.

2 Likes

Sir, I derived the Gross margins from the same source as you pointed out! I was trying to understand factors behind this considering both are pure commodity plays of same commodity and still their margins are quite different.