@RajeevJ This is something weird, they have updated their previous data somehow… The current data on the site shows this. So this then sort of changes the outlook… Any views? How can they modify older data like this? Is this a normal practice?

Is there any actual numbers available from any listed company about the prevalent prices?

past 10 years financials looks good with good cash generation and reduction in debt. but the annual reports doesnt give any picture of how this growth is achieved and sustained going further . ( are we only depended on price realization of camphor for growth)

below are some basic questions i have - i’ve write the same to company . It would be great, if anyone can help me with the any responses .

quantities sold and price realization per unit for the last 10 years (atleast for a couple of years) ?

Why there is huge sales fall in 2016 (30%) and huge sales growth in 2019 (76%) - Is the growth sustainable ?

What are the raw material procured by company ? is it gum terepentine or pine tree ?

from where did the company sourses the raw materials ? domestic or exports or any backward integration ?

What pricing contracts are placed with raw materials procurement - how did the commodity fluctuations effect the pricing?

What pricing contracts are placed with customers (B2B) - how did the commodity fluctuations effect this?

Are there any measures taken to reduce the power and fuel expenses ?

Other Manufacturing expenses are risen 3-4x in last 10 yrs - when compared with sales - what is the reason behind this ?

Is there any remuneration policy in place for Management personnel ? I see salary is always delivered as fixed component with no varibale (performance) component ?

exponential rise in the remuneration of promoter’s son Akshay from 6 Lakhs to 360 lakhs (age -31 years) from 2016-17 to 2019-20 . How is this remuneration linked to company’s performance - any rationale for the calcualted amount ?

Dujodwala Resins & Terpenes Ltd - promoter owned company . What are the business activities this company involved in . Is it a competitor to Managalam Organics ?

why there are fluctuations to the rent paid to “Dujodwala Resins & Terpenes Ltd” ? 500 lakhs (2017-2018) to 150 lakhs (2019-2020 )? Is there any change in nature of contract ? what is this rent for ?

Many thanks to all for providing insightful discussion . special thanks to @phreakv6 & @RajeevJ .

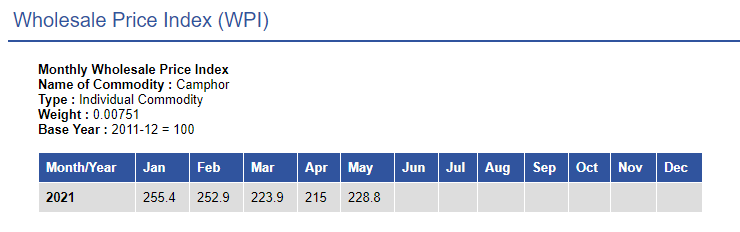

@RajeevJ sir, as per WPI data camphor prices reduced by 15% in May 2021. Will this affect the margins of camphor companies, especially Mangalam going forward? Can we assume the reason of reduction in camphor prices due to lockdown or covid second wave. Awaiting your thoughts on this.

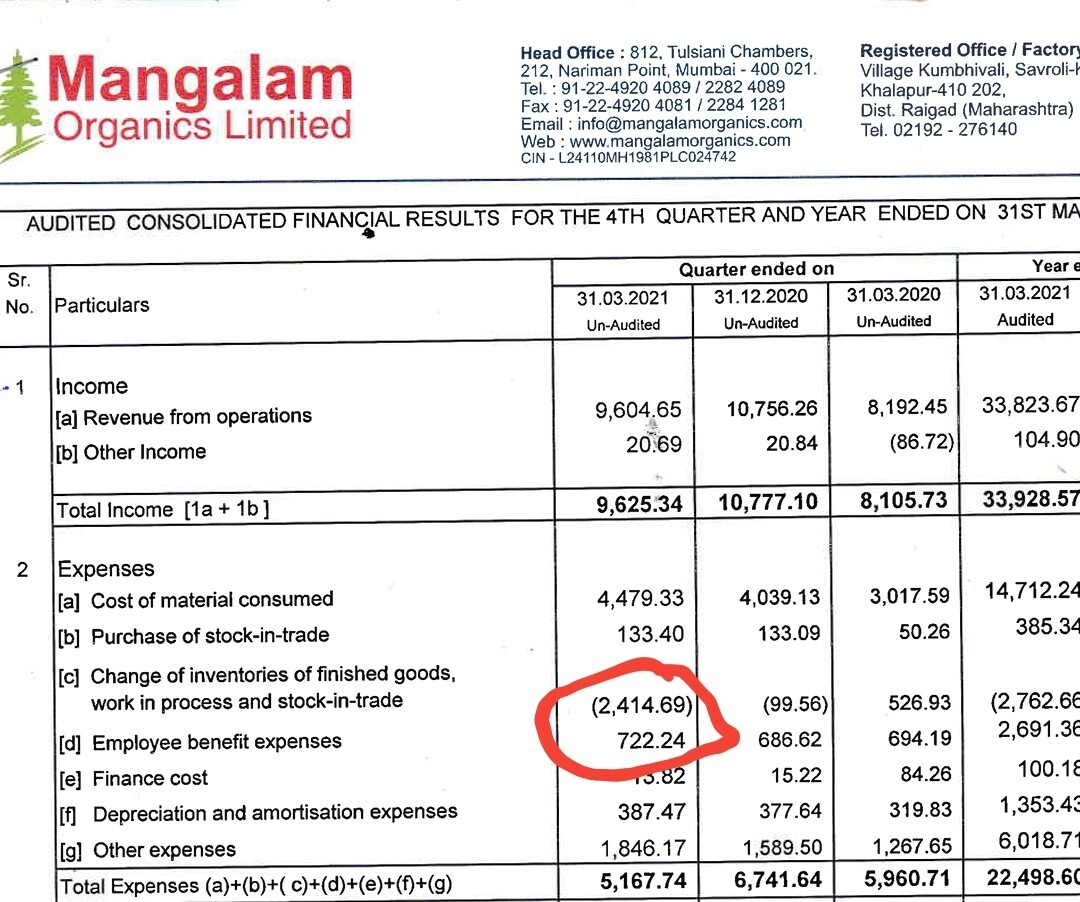

I have been in exit mode in Mangalam for the last several months. It was more of regular profit booking than anything else, though what did play on my mind was that the investment of 90 odd crs. carried out over two years was not reflecting in the numbers, so you really begin to wonder. Despite higher camphor prices, the Co. could not ramp up sales.

It is however quite possible that it finally begins to reflect in Q4 numbers with a vengeance, but as I had a biggish investment, I was a bit uncomfortable living on hope of camphor prices sustaining & the Co’s ability to scale up. Most importantly, I was getting the opportunity to exit at decent prices. Profit booking is always very satisfying!

@rakeshrocks1111

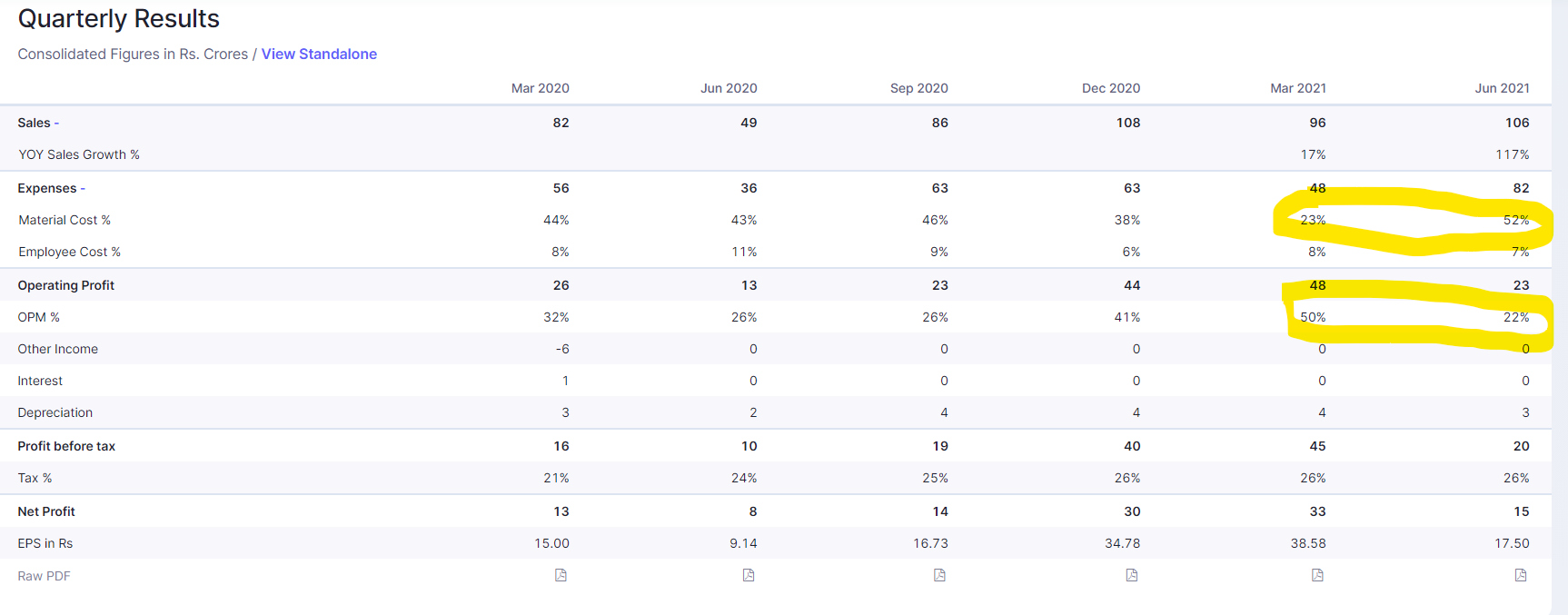

I have been invested in kanchi karpooram. It had a great run until now. Do you think the coming quarterly results (Q4) will be similar to the last two quarters results (Q2 and Q3) for both Mangalam and kanchi?

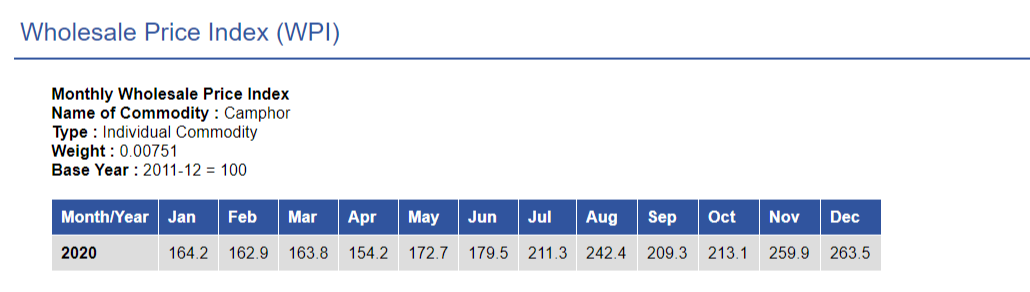

Camphor prices increased 6.4% MoM in May. Noticed one thing - In the picture posted by @mishraanoopam , March price is 247.2. But when I check the website it shows 223.9 for March.

Similarly there is a difference between Feb price in pic posted by @reacharjunr and @mishraanoopam . Am I missing something or prices were corrected by ministry? If so how reliable this data is.

Sharing my learning from Mang organics as investor.

This is a micrcap and has very volatile price movement for various reasons which are not easy to live with if higher allocation - requires very different temperament and risk mgmt.

Ticks many right boxes on valuations, mgmt increasing stake, Camphor industry potential and so on - easy to get tempted with esp with current bull phase

Narrative change between commodity- Commodity to FMCG - B2B with low pricing power and so on…

Generally do not follow technical on charts - low accuracy and confidence due to volatility hence frustrating at times

All in all lost some money in first attempt - H2 2019 to H1 2020, made decent multiples in H2 2020 to H1 2021 and exited fully. For some of us ( early phase in investing or only few years in mkt) , there are probably better opportunities elsewhere and one can slowly play these type of themes starting small with strong risk mgmt( easily said than done).

Margin of safety is very important in such scripts I.e. entry point is key.

NSE listing alone is an enough trigger to unlock value in a normal bull market. If the bullish sentiments prevail, this counter will mint money in time. As the Board already approved NSE listing, the clock is ticking.