Disappointing results

Sales down to 80 crores and Profit to 5 crores

Disappointing results

Sales down to 80 crores and Profit to 5 crores

QoQ view

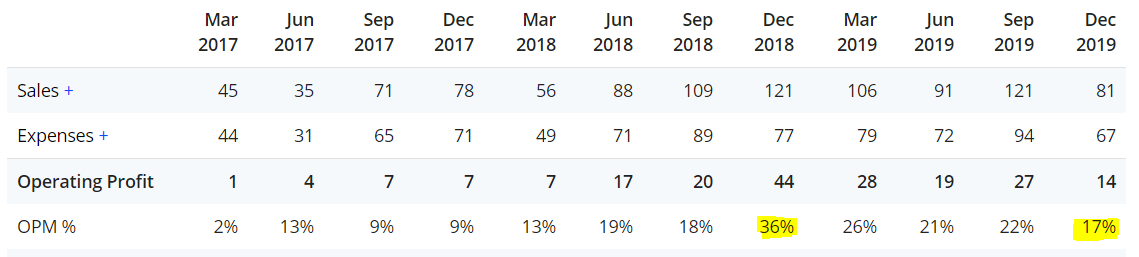

Sales down by 30+% ( 120 cr to 80cr)

Total exp down by 28+%(98cr yo 70cr)

Profit down by 35%+(24 cr to 15 cr as 5 cr being Excp item)

So in Q3 made 15 cr on 80 cr sales

In Q2 made 24 cr on 120 cr sales

Similar profit profile…key is Why sales are hit - need mgmt commentary, which is missing in results.

Kanchi results tomorrow- will clarify if all players are under water or one off issue with Mangalam

Two points to share from above posts :

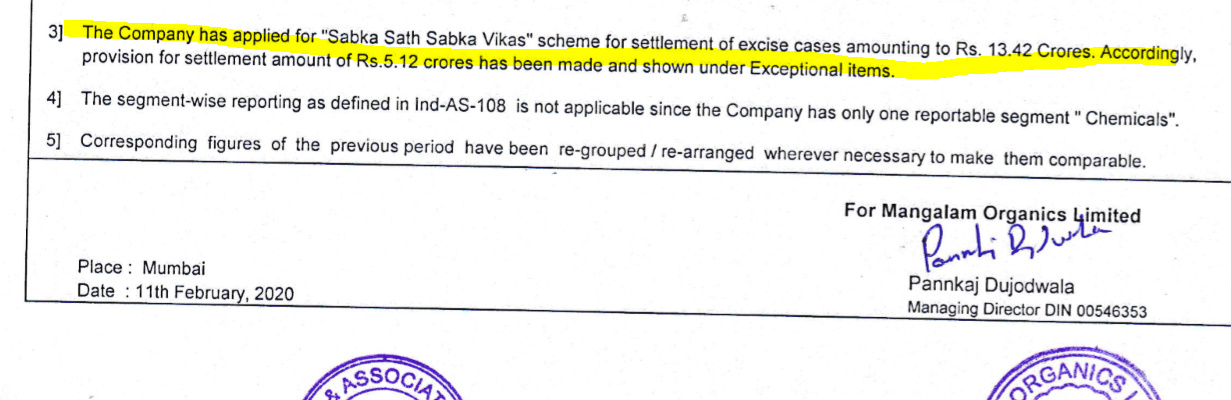

TAX and Death are inevitable in past company hasn’t paid the taxes and deferred but TAXMAN ghost hunted back however company has saved whopping 8.30 crore but it is not a good practice to deferred the tax theses scheme is occasionally. comes in to play .

@RajeevJ, can you please find out what went wrong with Q3 results? Sales are down by whopping 33% and profits are down by 86% YoY and there is no management commentary or investor presentation or con call with investors ![]()

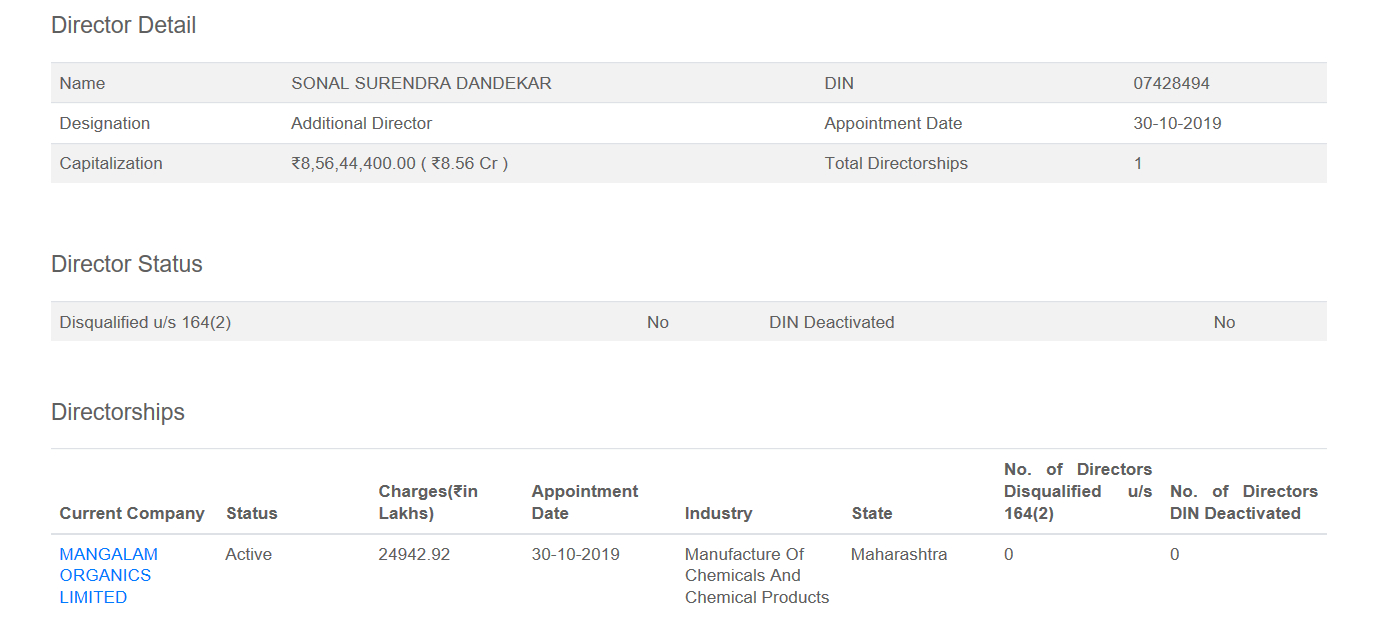

Management was very bullish during the AGM so it would be interesting to note what made this almost 180 degree turn of fortunes… Resignation of newly appointed independent director is also a cause of worry (as she has joined just 4 months back)

Disclosure : invested and highly concerned…

@Dialwealth any commentary on the results and future outlook for the company/industry?

No surprise camphor prices were coming down since 4 months this was expected …

Isn’t this bit of overreaction from the market?

One bad quarter and stock is down 36% in 2 days and will probably be down around 50% by the end of the week.

Should this quarter’s result be treated as the new normal for the company’s earnings trajectory?

Not overreaction, cycles turn viciously. Look at sterlite Tech, when the cycle turned markets are unforgiving. One needs to be very vigilant. Peak margins and unsustainable valuations are a lethal combination.

Disclosure

Sold this 2-3 months ago

Pure commodity products even if they are B2C would continue to have such variable results. Good Presentation by Oriental Aromatic today -

Their clients are global leaders in the aroma/perfume industry IFF, Firmenich etc.

Kanchi results are decent and not that bad (Link)

So this phenomenon is specific toMangalam where sales have declined sharply.Is it possible for someone to contact the CS and get the details?

Also, this should give some comfort that the industry dynamics hasn’t changed for bad drastically.

From historical PE band perspective, Mangalam has traded between 3-4 PE and current PE is at discount to the average PE

Disclosure: Tracking position, Not sure to sell or hold

Kanchi’s sales down by just 7% which is great considering the low camphor prices although its margins were low at 16% vs 21% (QoQ) and 19% (YoY). June expansion is again a good indicator for now assuming some of these operational costs are factored.

Had mailed their CS yesterday. No reply yet.

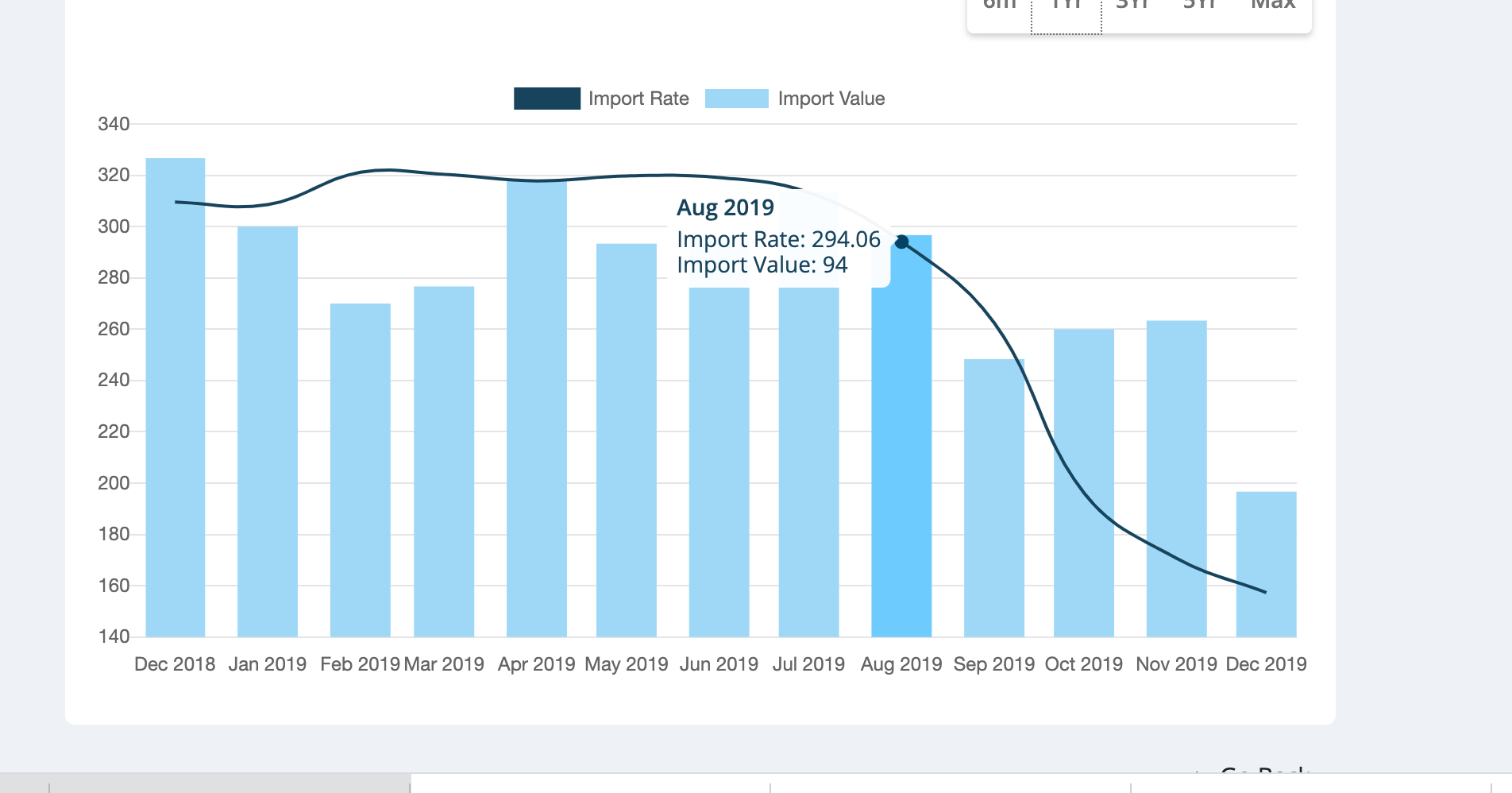

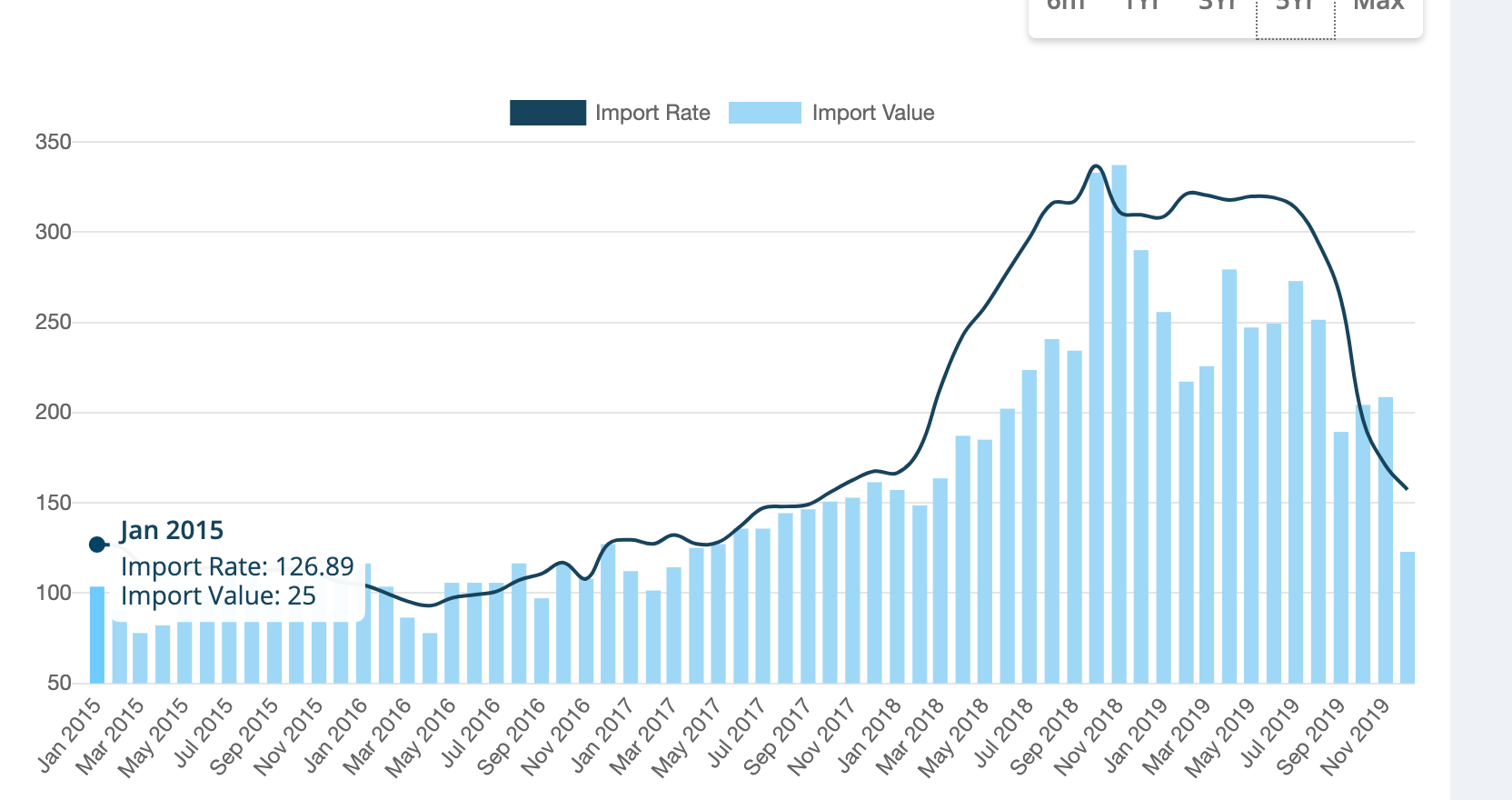

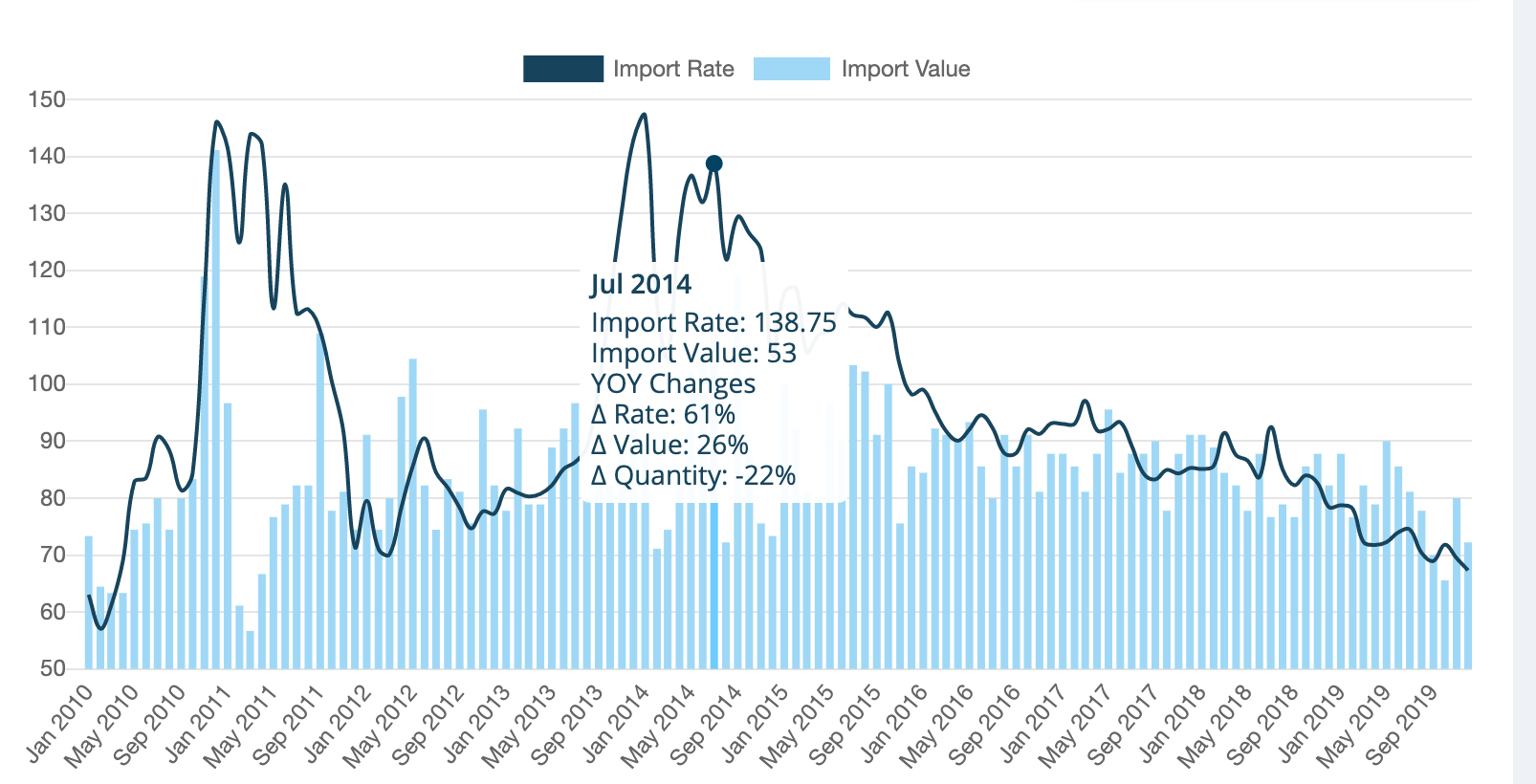

Since some of the members cite downturn in Camphor cycle as the reason for Mangalam’s poor performance, can anyone please quantify how much prices have corrected? Based on commerce ministry website, import/export volume and value has not changed so drastic as to cause this kind of a result for Mangalam.

Isn’t that’s how any cyclical play would end? HEG, Graphite, Rain, Avanti, Textile, sugar stocks and what not.

3 Bullshit filters to use in commoidty businesses:

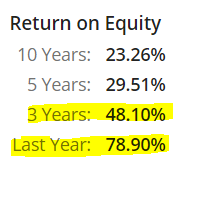

Peak ROE is dangeorus. Just think about it. ROE of 78% doesn’t look sustainable at all. There’s only one way to go for ROE’s from these level.

Peak Margins margins have already been falling for the last 4 quarters. Enough fundamental reason for exit.

To top it all of:

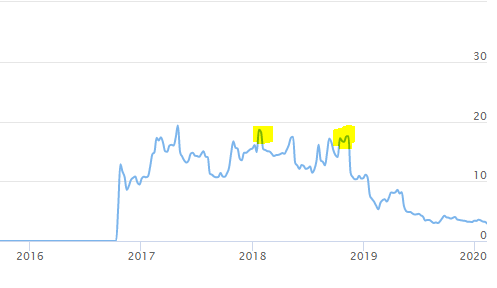

Peak valuation This is the P/e band of Mangalam Organics.

Dislclosure- was invested a while ago. But, the sheer numbers changed my mind. Better to change your mind than to be left with no seat when the music stops.

These cyclicals may be bottoming out, just a thought, as many are fearful to even think of them.

Gum Turpentine Oil prices declined from INR 300 per kg in Aug 2019 to INR 150 per kg in Dec 2019. Based on Indiamart quotes, prices have declined even further in the current quarter to INR 135 per kg. I believe this is the primary driver of lower camphor realizations - as a commodity manufacturer, Mangalam has been forced to pass on the benefit from reduction in input prices to its customers. On the positive side, Mangalam has been able to maintain gross margins at 40% even in Q3.

This drop in prices has been precipitated by:

Since 2017, the sharp hike in GTO prices has compensated pine tree tappers for the low realisations of Gum Rosin. However, the fall in prices of GTO and Gum rosin make gum tapping and processing unviable at the moment. Refer the conference call transcript of Kraton Corp below:

"That turpentine fraction has obviously come off significantly in value. More in line with quite frankly the historical relationship between gum rosins and gum turpentine. And, yeah, we would presume that all else being equal, that that ought to bring some disciplined decision making and behavior back to that marketplace.

In fact, we try to track that on a – if you will a real-time basis, and our own internal analysis suggests that there’s just not a lot of incentive right now to be tapping trees. And one thing I want to mention too, I think it was from the prior question, but is probably important to this discussion. The question was asked about our business. But you need to understand that the majority of turpentine, whether gum or CST-derived, really ends up in the aroma space for fragrances and flavors. And that’s really important, because obviously that’s a very high-end application."

(Kraton Corp (KRA) Q3 2019 Earnings Call Transcript | The Motley Fool)

If prices of both GTO and GR stay at the current depressed levels, pine tapping will not be sustainable in CY2020. As can be seen below, GR demand and hence prices are in a secular decline since 2013 and unless crude spikes above 80 USD per barrel, it is unlikely to revive

Therefore, either GTO realizations will rise before next pine tapping season or gum harvesters will decrease their output.

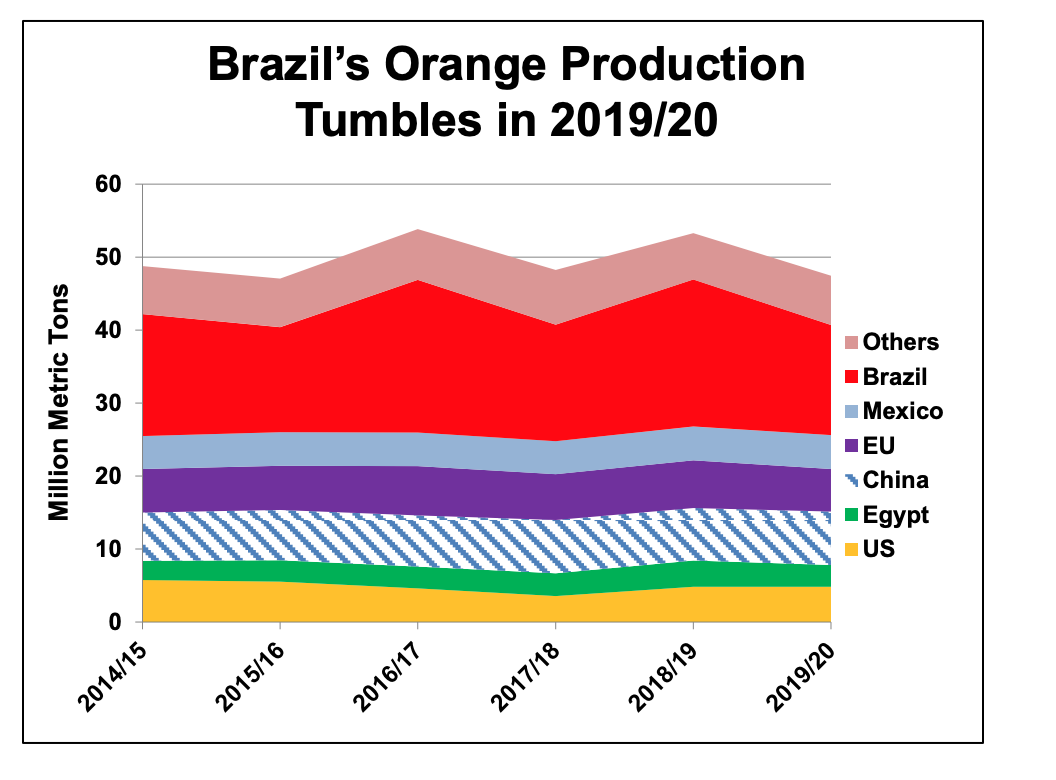

Moreover, after the bumper crop in CY2019, Brazil’s orange crop is expected to decline by 25% in CY2020, while US is expected to increase by just 1%.

This will once again trigger limonene shortage and consequently demand for dipentene - thereby driving up GTO prices.

The above trends combined with DRT revenue + new capacity for pharma grade camphor and terpene derivatives + rapid scale up of retail foray + ability to maintain 40% gross margins at any price of GTO makes me feel that at the current price, the risk/reward ratio is favorable.

Disc: Invested

Compared to Kanchi which was not affected?

Everytime I visit Dmart I go to their camphor section to check the date of manufacture of Mangalam camphor (50g, 500g etc). For the last 3 months their products don’t seem to be attracting the crowd. This I infer from the date of manufacture which is August 2019 and no newly manufactured bottles are coming in.

Also, this week I noticed that Dmart has started stocking camphor from Cycle (agarbhatti brand). Its date of manufacture is quite recent- Dec 2019.

Will check price/unit of each brand and update this thread. Will also give an idea about the magnitude of correction in camphor price.

Update on 21 Feb:

New batches of Mangalam Camphor have arrived in DMart (Airoli, Navi Mumbai).

There is no difference in the MRP between those manufactured in Sep 2019 and Jan 2020- Rs.195/100g. After discount, DMart offers it for Rs.149/100g. If memory serves right, DMart has not reduced their selling price over the last 3-4 months.

Cycle camphor is available in only one size and weight of the product is not mentioned on the label.

A point worth noting is that Mangalam camphor has BEST BEFORE duration 10 years whereas for Cycle camphor it is 3 years.

please anyone can tell me how much camphor is sold by company in branded lable ?