Even reviews are not that good as of now.

Only advantage it has is , it’s in pantry due to which discount levels increase than the listed prices.

What could be the reason for recent downfall of prices? Any big change in fundamentals?

Not sure. But have heard that camphor prices have been in correction mode.

Disclosure- sold one month back

1 Like

Mangalam Pure Camphor Tablets for Puja, Aarti, Meditation (500g X 1 Pouch) https://www.amazon.in/dp/B00ZR6KXUE/ref=cm_sw_r_cp_apa_i_iON7DbTFBVY7S

Retail camphor prices if anything seems steady…

2 Likes

The Mangalam promoters have been gradually increasing their stake, first by not participating in the buyback & later by buying in tranches of about 36,000 & 1,60,000 shares, thereby taking their holding from about 47% to 52%. I suspect that so long as the promoters are looking to add themselves, they are not too unhappy with pressure on the share price while they accumulate. In fact, it suits them.

13 Likes

There was ONLY one buy this year by promoter, only 0.43% of total equity (36,000 shares) was traded @ Rs 511 so around the historical PEAK.

https://trendlyne.com/equity/insider-trading-sast/all/MANORG/2709/mangalam-organics-ltd/

BUT yes, promoter holding was 47% as on March 2018 and is now 52%.

Thanks! There is ANOTHER deal for 2% i.e. 1,60,000 shares on 16-Sept by promoter @ 314 around.

Found this deal on BSE website, like you show. ![]()

1 Like

This stock is very attractive from a value perspective but the technical trend is negative. I want to enter but not sure when to enter (Maybe wait for trend reversal?) EV/EBITDA: 2.43 => If camphor prices just hold for 3-4 years, we would get back the entire market cap in earnings itself.

Every player in industry seems expanding capacity due to high price. Kanchi expanding 3X, Mangalam 2X and so on. If this phenomenon is playing worldwide, camphor price may drop like anything.

So if demand is not increasing in same trend, it’s very difficult to hold up commodity price.

Demand research report will be very helpful if anyone having it.

10 Likes

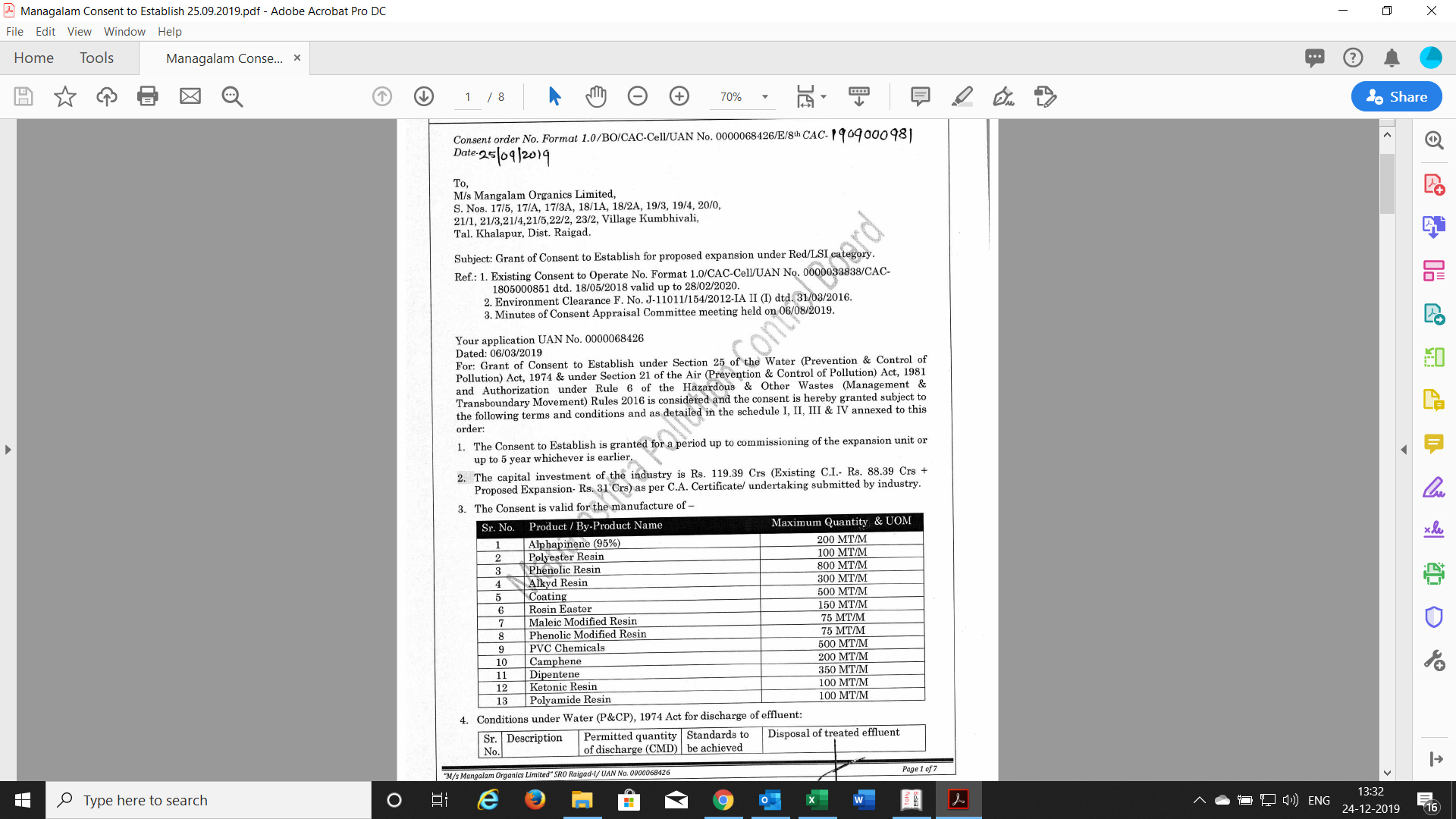

As per Annual Report 2019, Pinene and Campene derivatives will give healthier margins.Managalam Consent to Establish 25.09.2019.pdf (1.9 MB) dated 25.09.2019

It seems that above expansion will increase the margins of the company.

Disclaimer : Invested,

8 Likes

Some updates from Berje. They created a seperated post about Camphor USP in India this month but they did not share much details.

I have noticed prices of camphor on amazon are pretty much the same. Are they talking about the festive season coming to an end?

This is the update on Gum Turpentine:

https://www.berjeinc.com/2020/01/10/gum-turpentine/

There seems to be a small increase in supply but overall output is apprently still low given the weak demand of gum rosin.

I can’t find any numbers for the above information though.

6 Likes

5Cr Rent deposit to “Dujodwala Resins & Terpenes Ltd” from 2014 onwards, anyone have any clue what this deposit is about?

AR 19 says it was 3.20Cr in FY 17-18 but AR 18 says it was 5CR

Disclosure : Invested

Crisil rating maintained.

Regards,

Abhijit.

Disclosure : invested.

4 Likes

I could download rating rationale from CRISIL. Please see attached

Rating Rationale CRISIL.pdf (147.6 KB)

As per the report, most of the raw material is imported from Indonesia, Brazil, Russia and Europe. Under weaknesses, the report mentions revival of import from China could have adverse impact on the entire industry. Hence it seems domestic camphor industry could be beneficiary of the current issues in China since its input cost would not be impacted but competition could be reduced in short to medium term.

Disclosure - invested and hence biased.

15 Likes

If the volume is not increasing then why add more capacity? This is interesting, as it appears that the ride MOL had was purely based on the camphor price and nothing more? Am I missing something here?

Yes you are missing lot of other thing.

Mangalam was going to produce camphor for Pharma companies and that’s the reason quality of camphor and demand was going to be more starting this year

2 Likes

What is the reason then for Kanchi to go 3x? As far as I know they are not going to produce Pharma grade Camphor

Is there any report that justifies the demand of pharma grade camphor that MOL is focusing on?

1 Like

Could you kindly go through the entire thread so that you can get the info. you seek and more?

Every domestic producer is thinking that Chines factory shut down is permanent event & demand will be always be high. Nobody knows exactly how the story will unfold.

IMO Camphor will always be a commodity, Chines may shift their capacities to other countries.

Disclosure : Invested (Small position)

1 Like