The peak valuation happened more than 1 year ago? The point is? Currently it was at lowest valuation, thank you!

Disc: Exited breakeven after 2.5 years, was 6% of portfolio.

The peak valuation happened more than 1 year ago? The point is? Currently it was at lowest valuation, thank you!

Disc: Exited breakeven after 2.5 years, was 6% of portfolio.

Some people have the ability to give random answers with no follow up. I feel the thesis of a company being b2c in this segment is not that strong, bulk sales will remain b2b

Bulk deal of 2.6L shares today at 158. That’s 3% equity. Holding on in a tight range in this bad market.

Seeing some Digital Marketing retargeting ads on campure, retail push is ON.

Promoter group increased stake by 3% from open market:

Promoter buybacks are assuring but seems all over price points, for now No participation in buy back and multiple buy from market seems like a good sign.

Promoters’ holding had increased from 47% to 52% over the last two years through acquisition and buyback. This week’s additional purchases take it to 55%. Current market capitalization is Rs 132 crore, Q3 pre-exceptional profit before tax was Rs. 10 crore. Cash flows are positive, being used to expand capacities. Looks like a positive risk/reward. (disclosure: small investment)

Mangalam started advertising its products on TV. I have recently seen one ad on Marathi news channel but I could not find it online. Some of the old youtube influencer videos are as attached below

Mangalam products like camphor tablets and cones continues to have 3.5- 4 star ratings on Amazon even after 300+ reviews. Although the retail sale would take long time to contribute to the overall sales and profits, I think company is moving in the right direction.

Hello,

Were you able to get some reason for drastic fall in quarterly sales and profit. Other than that, promoter buying is also positive.

Just unable to understand the fall in sales and profit.

Thanks

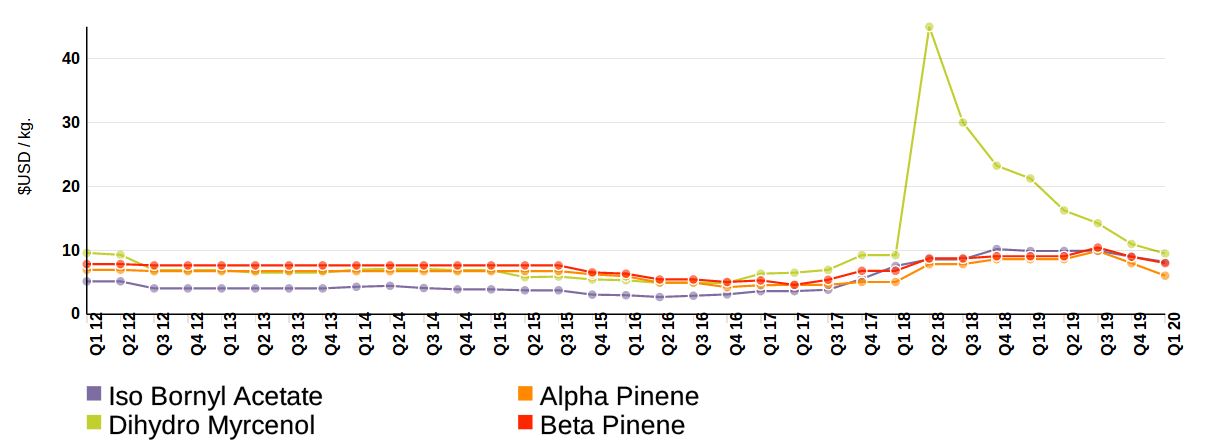

BerjeInc had posted on 21st Jan that prices of camphor in India were softening.

BerjeInc updated on 28th Feb that Gum Terpentine has seen 10-20% increase in prices due to lesser availability, courtesy Coronavirus.

Chart shows a decreasing trend QoQ for terpene compounds.

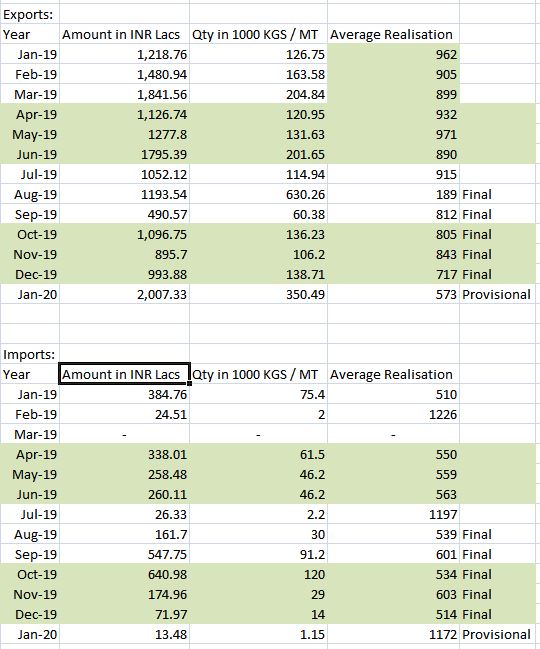

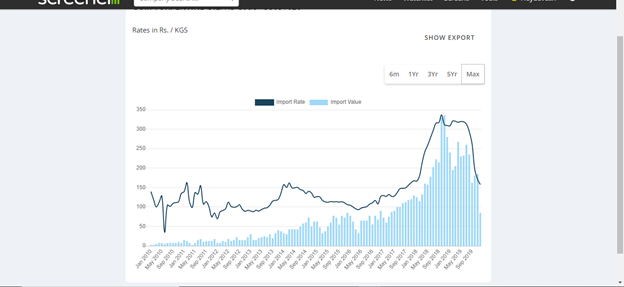

Jan exports have increased substantially YoY with fall in margins. Imports too have fallen substantially.

In many uses, especially cleaning, gum turpentine is substituted with mineral turpentine which is a crude derivative. The huge increase in crude availability coupled with the massive fall in crude prices is bound to exert pressure on GTO prices this month. If coronavirus recedes in China (looks possible) with crude remaining at these levels, we could see multi decadal lows for GTO prices - and subsequently camphor.

Today, Mangalam Organics published an advertisement on the front page of the Times of India for camphor cones available on Amazon. Currently, retail sales are a miniscule proportion of revenues and the business is susceptible to commodity cycles.

Looks like the 5Cr provisioned in last quarter PnL is for CESTAT settlement under sabka saath sabka vikas scheme. The intention to settle is perhaps good.

I found two facts that puzzled me somewhat about the December quarter.

First, while the amount of 5.12 crs was in final settlement of the dues amounting to 13.42 crs, the results perhaps indicated that the amount of Rs. 5.12 Crs was a provision made in Q3 out of a total liability of 13.42 Crs. Later on March 9, after making the payment the Co. clarified that this liability of 13.42 Crs was in fact settled at 5.12 Crs.

Secondly, where was the need to make a provision in Q3 when the payment itself was made in Q4. The Q3 results in any case were much below expectation. This provision further damaged the already poor Q3 numbers.

Meanwhile, the mgt. continues to accumulate & hike its holdings!

+Ve and +Ve - Intent and provision to settle was demonstrated in Q3, followed by sizable purchase from mkt in Q4 by promoters. (timing may be Q - another interesting aspect is that Govt bodies settling dispute with exact amount offered by company)

+Ve stock Price is relatively holding steady in current carnage (Q3 bashing has done damage already)

-Ve - GTO prices on downward spiral - seems to be in line with mean reversion - likely pressure on realization - is industry structural change theory under Q?

Invested from bit higher levels - current mkt chaos and mixed signals from company not helping on decision process of avg/sell

Would be helpful to hear what others are doing with their holdings here?

another interesting aspect is that Govt bodies settling dispute with exact amount offered by company)

These settlement schemes stipulate a specific sum to be paid. There is no discretion of the Govt body in calculating the liability. Same with the Income Tax Department’s Vivad se Vishwas scheme.

Poor quarterly result + no explanation from management + increase in stake

Seems to me that promoter wants lower prices to increase stake.

Also, I had been tracking number of ratings of their most popular product on Amazon (camphor cone). Number of ratings steadily increased to around 1800, then suddenly dropped to around 1200 and has since been hovering around that number. Does this mean Amazon found fake reviews and removed them. Could somebody knowledgeable about how this works educate me on this.

Thanks

i think we are being too much optimistic on this company. i have made same mistake many times before in commodity company.

manglam has not sizable sales in retail so we cant still say its in consumer business so PE should be of commodity only. also any online seller amazon etc or supermarket gets all thsi product at min 50 % discount to MRP. Then only they can survive and lure customer with min 20 % off or buy one get one free,etc etc . so how much they can turn in to profit is question mark . this is my opinion

disc not invested but tracking .

https://www.wsj.com/market-data/quotes/futures/OJ.1

Orange juice prices have increased 20% in the last week.Maybe people in USA have stockpiled in lockdown panic.If lockdown extends further,demand might still increase.

I have 1 observation and 1 question

1)This price rise might lure farmers to divert more agri land for oranges next sowing season => increased production of limonene from orange peels => reduced demand for dipentene => reduction in margins for mangalam next year.But orange production this season is expected to be stable in usa and reduce in brazil

2)fall in crude prices => reduction in prices of mineral turpentine.What effect might this have on gum turpentine and the margins of mangalam

Tagging those who were active in this thread,for any insights to improve my understanding @RajeevJ, @phreakv6, @vivek423

Edit 1:

more questions :

3)Other than camphor,the products like dipentene,sodium acetate,synthetic resins depend on growth of end industries like paints,textiles,leather tanning,tyres.With the world facing recession does the near term growth for these products look bleak?If so,fortunes of the company largely depend on camphor(which contributes about 70% of revenues) and raw material price fluctuations.

4)In the annual report it is mentioned that synthetic resins are unaffected by volatility of crude oil?I thought crude derivatives are substitues for synthetic resins.Or is this just the management being very positive about the company?

A quick look at the Cash FLow shows that the company has spent 27 Crores in Fixed Asset purchase, biggest in last ten years of the company.

Is it for production capacity expansion for manufacturing of Terpene? Or is the company started something new?

The alliance with French Co. “M/s. Les Derives Resinques & Terpeneques (DRT)” has recently been terminated.

https://www.bseindia.com/corporates/anndet_new.aspx?newsid=6d858214-ea63-4ae7-a18c-993ded20d2cb

I would have expected this to be a big negative , considering this alliance was touted as a game changer till an year back. No wonder we never heard much from the management all this while…

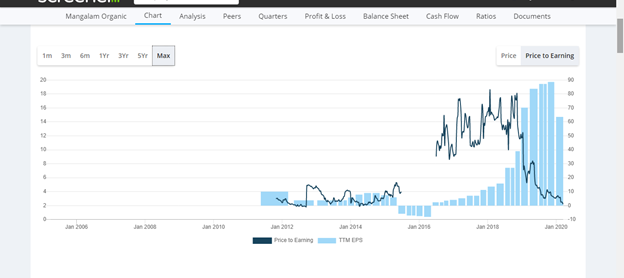

What puzzles me is the near doubling in share price from march lows of 130 Rs.

disclosure: Invested at around 450 levels, looking to cut losses on more price rise.