Hi Bharath

Will you please post the Q2FY24 presentation pdf here

The link on the Manappuram official website has stopped working

Hi Bharath

Will you please post the Q2FY24 presentation pdf here

The link on the Manappuram official website has stopped working

Concall Notes - Nov 2023

Financial Results:

Gold Loan Business:

Other Loan Businesses:

Dividends and Payouts:

Funding and Liquidity:

Future Outlook:

Other Financial Highlights:

you can access from here, the company has updated their website thats why the links are not working

@maheshkumar - Remember how the stock up from pessimism to optimism? Price changes perception! With the Aasirvad DHRP in place, I believe a lot of re-rating triggers in place.

Absolutely @Rupee_Millionaire

Rerating on board as visibility is visible to market now

Where else you can find near book value stock growing at 20% at PE of single digit…a clear cut recipe for rerating

Current rally in gold finance companies can be attributed to rally in Gold prices which is likely to sustain for some time given the global scenario and interest rate situation. Good read.

Manappuram has traded cheap for a reason. It used to be number 2 in gold finance and now has lost that spot to few competitors. The real rerating will happen (quickly) if the promoter changes. Next generation is not interested and the existing promoter may be looking to sell. Time is very good to get decent exit valuation. Cupid Ltd. stock nearly tripled in matter of few months once the promoter exited. Good business with growth oriented promoter gets rerated quickly. Will be interesting to see how this story plays out.

Technical experts will know beforehand that something is happening based on price volume.

Discl: Invested

Mr.Nandakumars current directors daughter is involved in the company promoter might not sell

exit of promotors wont result in rerating of company unless they are bad or the new promotors are very good

lets see

I feel rerating will happen due to

Derating will happen

It’s multi factorial ,so far cheap valuation offers the cushion from major downside

I am biased towards rerating

So far price movement is in strong favour

Management is forecasting growth, slowly some market participants are believing that growth can sustain at current yields

Once market gets full belief then real gain in price will take place

————————————————————————

Regarding valuation Manappuram is trading at half the PE and half the price to book than muthoot ( both trading at half the price to book of their historical best )

Current valuation:

Manappuram PE 7.4

Muthoot PE 15.5

Manappuram price to Book 1.3

Muthoot price ti book 2.6

**Historical best :

Manappuram max PE was 20 and price to book was 3.3

Muthoot max PE was 17.5 and max Price to book was 5.2

———————-

Post ANALYST MEET PRESENTATION (19/12/2023) all brokerages have upgraded their views and valuations for Manappuram

————————————-

Manappuram Finance’s potential for rerating is supported by

Signs of rerating as market start realising growth is possible at these yields with diverse products

All discussed here on this forum before ,is now coming in brokerage reports :

Overweight rs 210 Morgan Stanley

——————————————————

GOLD WORLD WIDE inclusion in portfolio

————————————-

Many tailwinds ahead

the prices are high, frauds will increase. We may just see banks retreat

Muthoot commentary suggests uptick in smaller size gold loans. This can be a huge positive for Manappuram whose main market is small ticket gold loans.

Disclosure: Invested in Manappuram (bought shares in last 30 days)

https://www.apnnews.com/dr-sumitha-nandan-ed-of-manappuram-finance-gets-jury-special-award/

not sure what her exact accomplishments are at the company though

rating rationale

Gold to enter 2024 with sights set on record highs By Reuters

Positives:

Negatives:

Not uncommon for this stock :

5-10% up /down in one day

10-25% in one month

And 50-100% in a year

If some one trades properly can easily get 10% return in this stock per month

Ideal trading stock

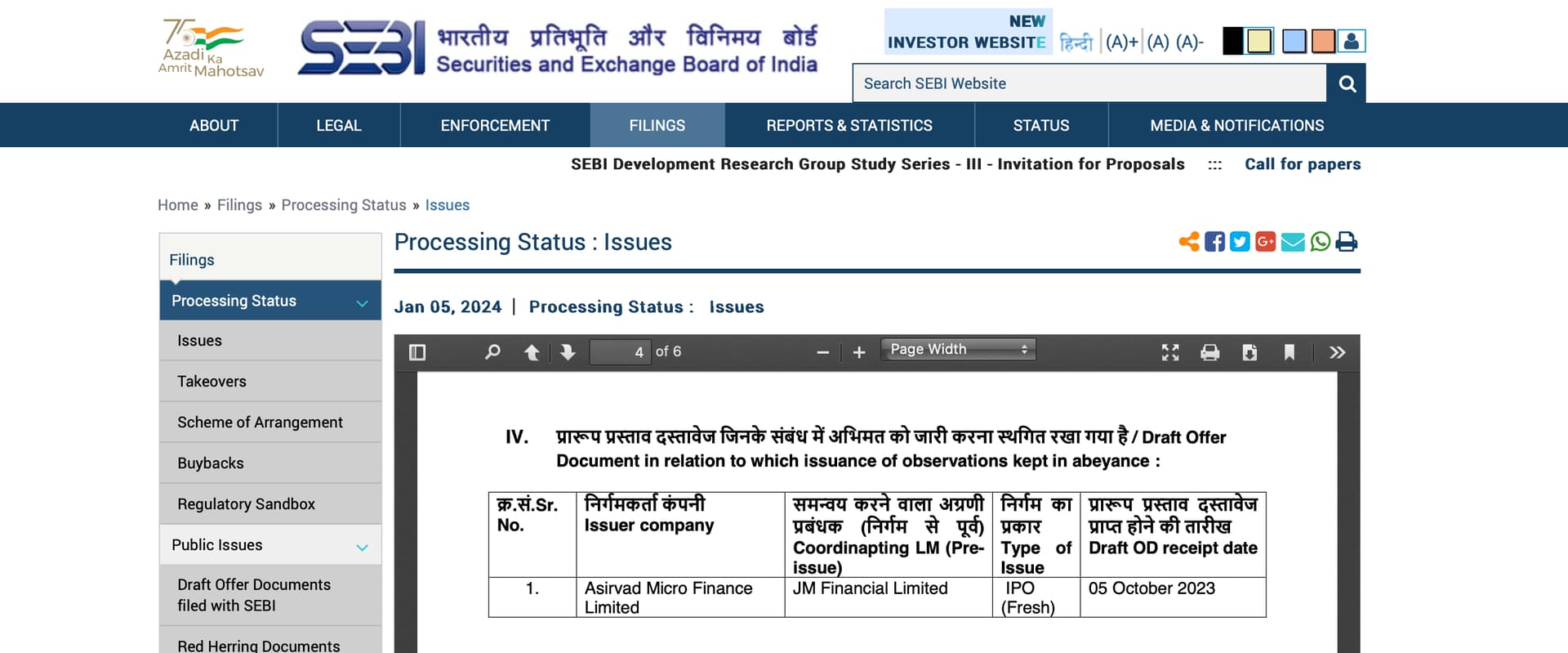

While there is no mention of the IPO being put on hold on the official SEBI website, this information is only available in news reports."

can you please share the link for where it mentions on sebi website

I couldn’t find it on SEBI website

But almost all news Channel has the same news so must be correct

Any how it’s just a delay /hold which is not unusual with IPO

Manappuram was due for rapid correction given one way upside move

Need a break before next move