Thanks for sharing the information

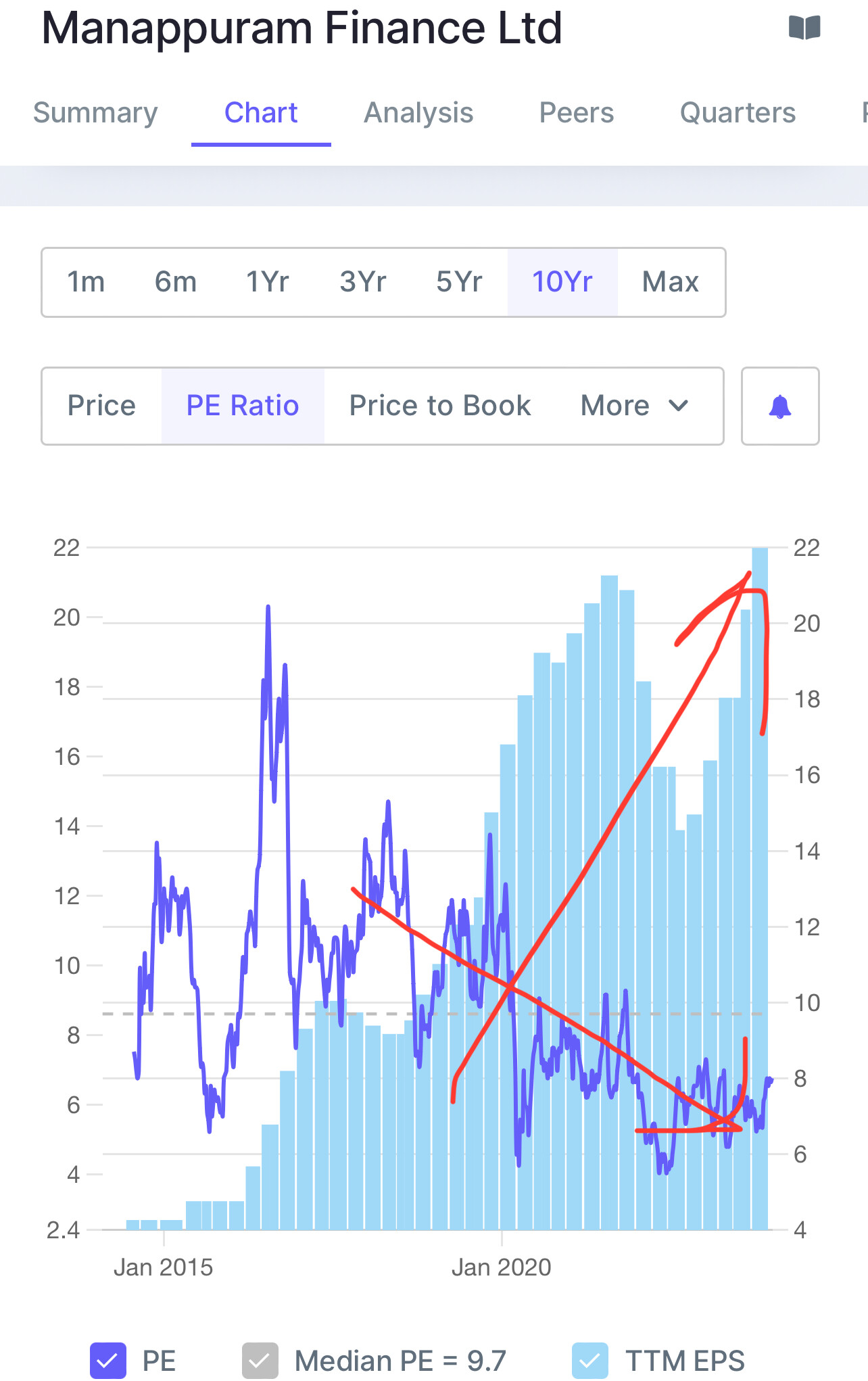

Fascinating chart: EPS is rising, yet the price-to-earnings is decreasing. Similarly, book value is increasing, but the price-to-book is declining. Unsure if I’m overlooking something or if it’s a market oversight.

It’s unexpected to find such a paradoxical chart during a bull run. Curious to see how long the graph will maintain this paradoxical trend.

2 Likes

Well, mostly market looks at Pure Price and there hes been a good increase. There should be a are rating now that promoter issues is behind and business continues to do well.

2 Likes

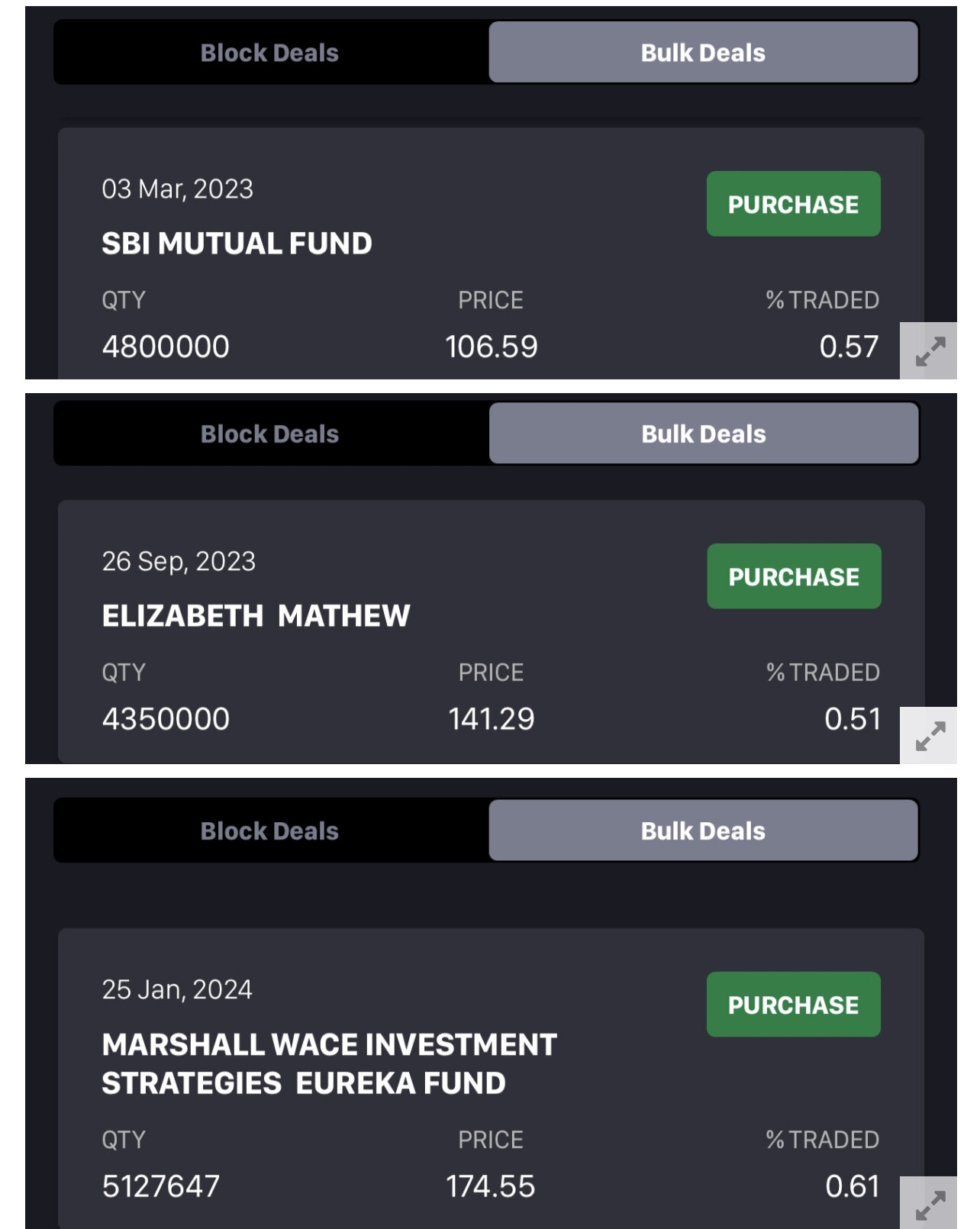

I think ,Few smart bulk deals which took place in last 12 months

first to catch the upside was SBI in March 23 at 105

Then in September 2023 Elizabeth Mathew entered at 141

And now

Marshall Wace picked up 51.27 lakh shares at Rs 174.55

Once Manappuram establishes that:

- Bank competition not affecting them too much , enabling over 10% growth in gold loans.

AND - are able to do non-gold business which is new to them with manageble NPAs with respectable growth

- gold prices don’t correct sharply

- no regulatory and political issues

- consolidated profit growth of 15-20%

Then it will be considered as a well balanced NBFC and will get better and sustained valuations

But usually market gets an idea well before the story unfolds and clarity appears

And stock makes upmove way before story is completely clear

retail investors participates when picture is clear but at that time valuations are super rich and gains are limited

5 Likes

I believe its just noise since they also picked up stake in multiple financial companies. What will matter more is the IPO Listing of Aasirvad and maintaining the growth momentum for the stock to get re-rerated.

4 Likes

anticipating robust performance from Manappuram in the upcoming earnings report, especially with the NBFC sector demonstrating a consistent 7-11% quarter-on-quarter growth trend. Expecting revenues to surpass 2300 crores and profits to exceed 600 crores. If all factors align, there is a possibility of witnessing a reevaluation of the share price.

The festive and marriage season is anticipated to further bolster the company’s growth trajectory. Positive results in line with the aforementioned projections would yield an earnings per share (EPS) of 7 for the current quarter. Assuming a sustained growth pattern, the EPS for the next fiscal year is projected to surpass 26 on an annual basis.

Manappuram appears undervalued in comparison to its peers such as IIFL Finance and Muthoot, considering various parameters including market capitalization to sales ratio, price-to-earnings ratio, and others.

11 Likes

127 cr profit

7% qoq up

80% yoy up

3 Likes

Margins have slightly decreased for asirvad, and based on my projection, the revenue is expected to surpass 2350 crores. If Gold Home and Vehicle perform exceptionally, it could potentially exceed 2400 crores. In the absence of a negative impact on gold, and considering that the future OI is lower compared to the previous period during result announcements, there is no restriction on upward potential even after the results are declared.

1 Like

The performance is unsatisfactory, as gold isn’t contributing to growth in AUM or revenue, possibly due to intense competition from banking entities.

1 Like

The potential reclassification of the company as a microfinance institution rather than a gold financier could be perceived favorably by the market, particularly considering the typically higher valuations accorded to microfinance entities. Investors may find reassurance in acknowledging the company’s diversified operations beyond gold lending, potentially mitigating concerns associated with gold loan growth.

4 Likes

They should not do it since they will violate one of the immutable laws of branding. Rather, they should spin off Aasirvad Microfinance which will accord higher valuation. As a result, the parent company will also get re-rated.

Why are they unable to grow their gold loan book needs to be seen closely. If they are purely a microfinance institution as a group, why not take our bets elsewhere?

2 Likes

Key takeaways:

Financial Performance:

The net profit increased by 46% year-on-year, reaching 575 crores.

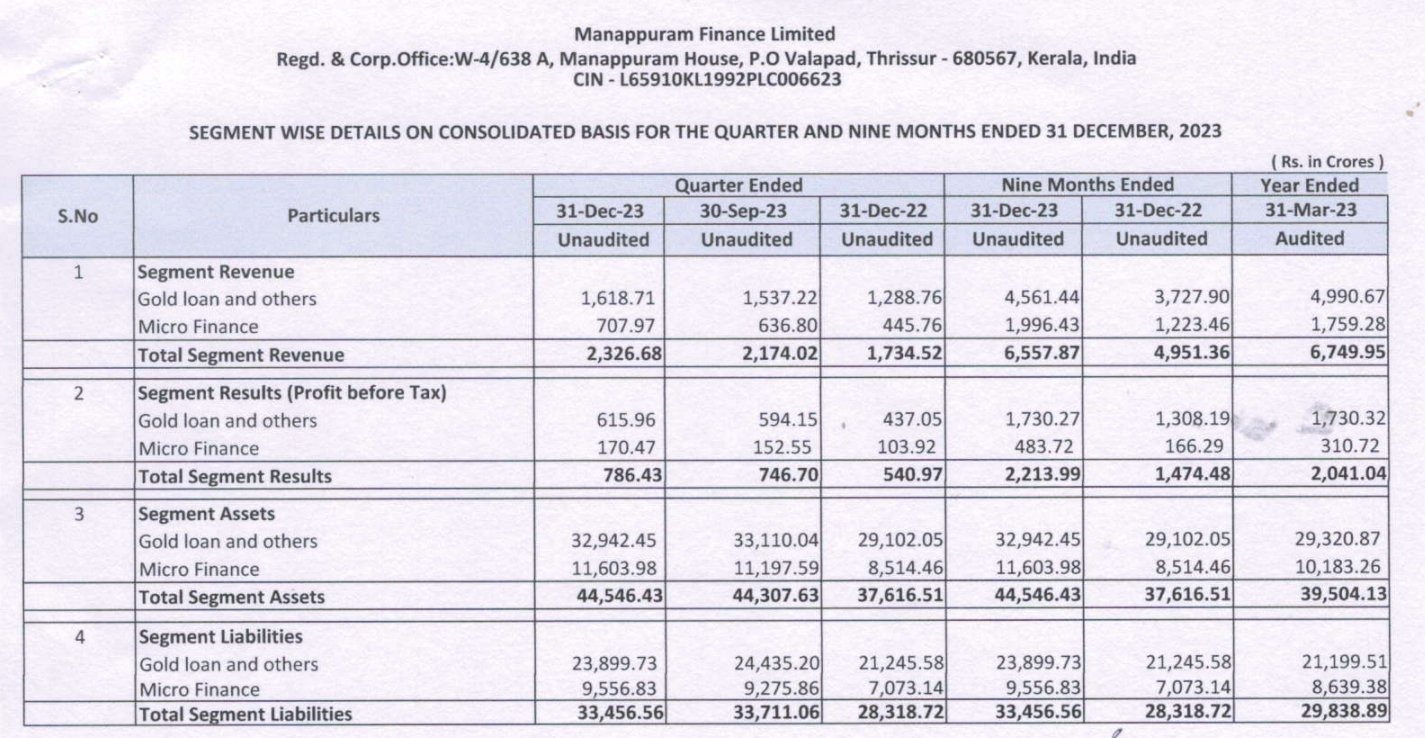

Gold Loan saw an 11.5% year-on-year improvement, totaling 20,758 crores.

Standalone AUM for NGT grew by 23% to 27,407 crores.

Consolidated AUM reached 40,385 crores, a 27% increase over the previous year’s quarter.

The recorded ROA for the quarter was approximately 5.2%, significantly surpassing the industry average.

Ashirwad, the microfinance subsidiary, achieved an AUM of 11,563 crores, representing a 34% year-on-year growth and a Q3 profit of 127 crores, an 80% increase year-on-year.

The vehicle finance business experienced a 70% year-on-year increase, reaching an AUM of 3,597 crores.

Home loans showed a 41% increase over the previous quarter in FY23, with an AUM of 1,415 crores.

profit of 28 crores was reported from the fee-based business.

Current Operational Performance:

Standalone GNPA increased to 1.99% from 1.56% in the previous quarter.

Cash and cash equivalents on a consolidated basis totaled Rs. 3,076 crores, with an undrawn bank line of Rs. 7,138 crores.

Collection efficiency for the quarter was 98%, with GNPA at 2.6% for vehicle finance.

For home loans, collection efficiency was at 96%, with GNPA at 2.67%.

Collection efficiency was at 102%, with GNPA at 1.5% for MSME and allied businesses.

On-lending AUM amounted to Rs. 1,022 crores, with a 5% ROA for the quarter.

The consolidated net worth was Rs. 11,063 crores, with a book value of Rs. 130.70.

Future Outlook:

Anticipates a similar increase in the cost of borrowing in Q4 due to the circular that raised the risk rate on consumer credit exposure of NBFC lending.

Confident in achieving top-line and bottom-line growth while maintaining adequate liquidity.

Foresees a reduction in the surplus in auction, allowing for branch expansion.

Concerns:

Elevated credit costs in the microfinance business due to delays in collections in certain states.

Increase in the cost of borrowing due to the circular that raised risk rate on consumer credit exposure of NBFC lending.

Other Points:

The company has applied for 300 branches and is hopeful of getting permission for expansion.

7 Likes

To take other bets ,We need to find company growing at 15- 20% at PE of 8 with high dividend yield with good ROE ,excellent positive cash flow

Overall in last 5 years growth is around 20%

if we find any better valuations elsewhere then such bet can be taken

Here we are getting a chance of rerating to PE15(8-20) with ongoing 10-20% growth

Now moving towards diversified NBFC

Post covid Gold loan growth affected by huge competition from everyone

Not sure this conpetetiob is permanent or temporary

Market May not give better valuations to this script ,unless consistent gold loan comes

Management :

Ashirwad ipo hoping for positive news

New branches Hoping for positive outcome

Gold loan hoping for 8-10% annual growth

Gold loan some quarters will be flat while some will show growth

Non gold growing well

Still majority of gold loan is with unorganised sector so all players have enough pie

7 Likes

Valuation point well-taken. An NBFC cannot replace a bank. A bank is a bank for a reason. The value will get unlocked once the micro-finance entity gets demerged. MFL is still undervalued and with price changes perception.

5 Likes

VP NANDKUMAR

Expecting reasonable gold growth in quarter 4

Ashirwad Microfinance IPO expectation march /april

Overall 18-20% growth expectations

Non gold 30% growth expectations

Gold 8-10% annual expectation

—————

I feel if such growth continues 10% gold and 30% non gold then in 6-7 years non gold profit will be more than gold loan profit

6 Likes

Asirvad IPO may come in Mid-March to early April

1 Like

2 Likes

2 Likes