This looks like a very exciting initiative.

It covers 2 major pain points for gold loan industry:

- The opex in evaluation is a considerable expense for the lender

- The borrower has to spend considerable time physically at the branch for disbursement.

“With GoldPe | APM, they can get their gold loan instantly, safe and secured within less than 8min & 24x 7. Customers can deposit their gold in the machine, which then uses AI technology and Gold / Metal Analyzer to assess the Purity, Quality and Weight of the gold. The AI system will weigh the stone and gold weight separately, and based on this assessment; the machine instantly disburses the loan amount”

Pardon my naivety, wouldn’t performing KYC of customers require manual intervention? AFAIK the KYC docs have to be verified by a person. Just curious if/how the APM automates this aspect.

Not necessarily, in some cases KYC is done in an automated fashion and I reckon pretty soon its going to become the norm. Case in point Banks: How Banks are using RPA to Comply with KYC Guidelines

Big things ahead for Manappuram Fin My analysis suggests that it may report revenue of 2200 CR,profit of 550 cr . Asirvad is stepping up, With increasing demand, they’re set to spearhead the growth

“HDFC bank enabling 200-300 branches every quarter for gold loans. They have been pushing gold loans majorly”

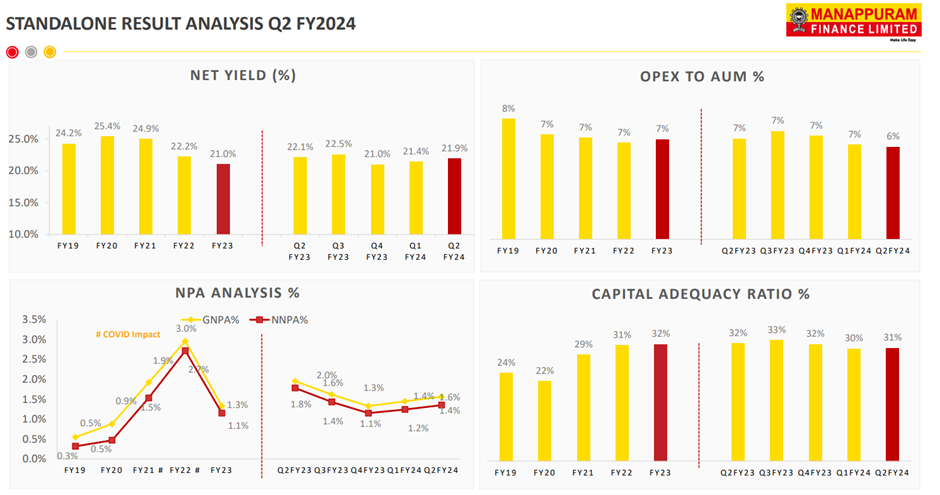

Superb Result by Mana for the quarter ended September 30,2023, posted highest revenue and net profit.

-Net Profit at ₹561 cr vs ₹409.5 cr (YoY)/₹498 cr (QoQ)

https://www.bseindia.com/xml-data/corpfiling/AttachLive/7feffcae-c195-4e9f-984b-ffc77dd5d21a.pdf

Non-compliance with certain provisions of the

“Non-Banking Financial Company -

insider trading

I feel there’s a big opportunity in the gold market and microfinance. Companies that perform well will succeed, increasing value for investors. We’ll see how this unfolds over time. Rising gold prices will be an additional advantage.

This is an exciting period for Manappuram Finance. Currently, the market is skeptical about its growth and sustainability, leading to throwaway valuations ,almost at book value ,means no value for brand ,business ,customer acquisition,long history,diversification ,everything free

Let’s see next few quarters

——————/

Some updates from vp nandkumar

https://www.financialexpress.com/business/banking-finance-evaluating-new-biz-opportunities-to-step-up-ops-in-vehicle-amp-home-finance-manappuram-finance-md-3313502/

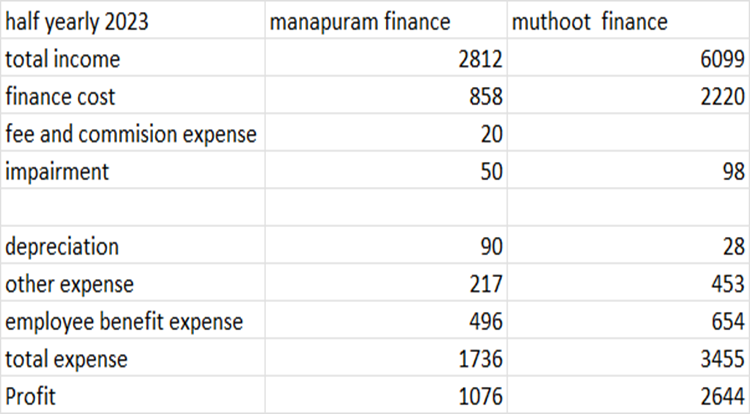

Why is the opex cost high compared to muthoot finance ?

I suppose its due to their diversification in microfinance.

Operating margin for Muthoot is in mid 40s, Manappuram in mid 30s and IIFL in mid 20s

Muthoot Finance (FY23)

- Gold loans: 98.4%

- Non-gold loans: 1.6%

Manappuram Finance (FY23)

- Gold loans: 58.4%

- Non-gold loans: 41.6%

Any comparison available with IIFL?

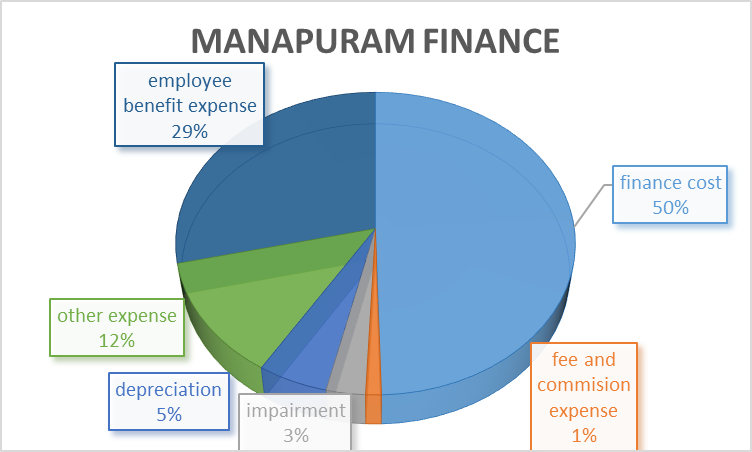

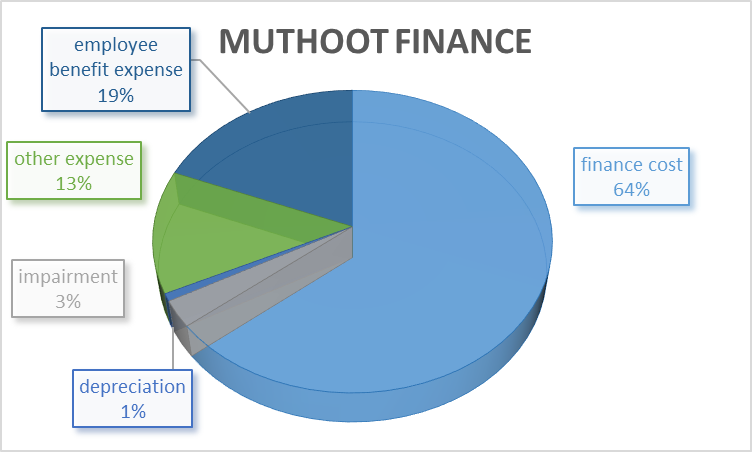

the percentages of expenses for half yearly of 2023 STANDALONE minor mistakes may be there

my thesis -

manappuram has higher employee cost due to lower AUM or operational inefficiencies

in the future this might get corrected so that it can effectively compete

Major reason for lower opex in Muthoot is their AUM per branch which is very high compared to any gold financier. Muthoot has a per branch AUM of 14.2 cr, whereas Manappuram has 5.6 cr, IIFL has 8.8 cr, FedFina has 7.1 cr. I don’t know how Muthoot is able to do that. Even if I assume they have bigger branches compared to other players, their employee expenditure is proportionally low compared to other players, which signifies they do better in all parameters.

Manappuram FY23 Total Employees: 63,760

Muthoot FY23 Total Employees: 27,273

That is a stark difference, even if we take out Microfinance Employees (close to 16,000)

I believe one reason for the same is the loan tenure which was 3 months for a very long time which required more employees to deal with customers and at the same time it kept the AUM low because employees were focused on renewing the loans rather than getting new loans. One big reason for IIFL’s growth I believe is that their loan tenure is 24 months which makes sure that the churn of loan book is low. Muthoot’s tenure is 12 months