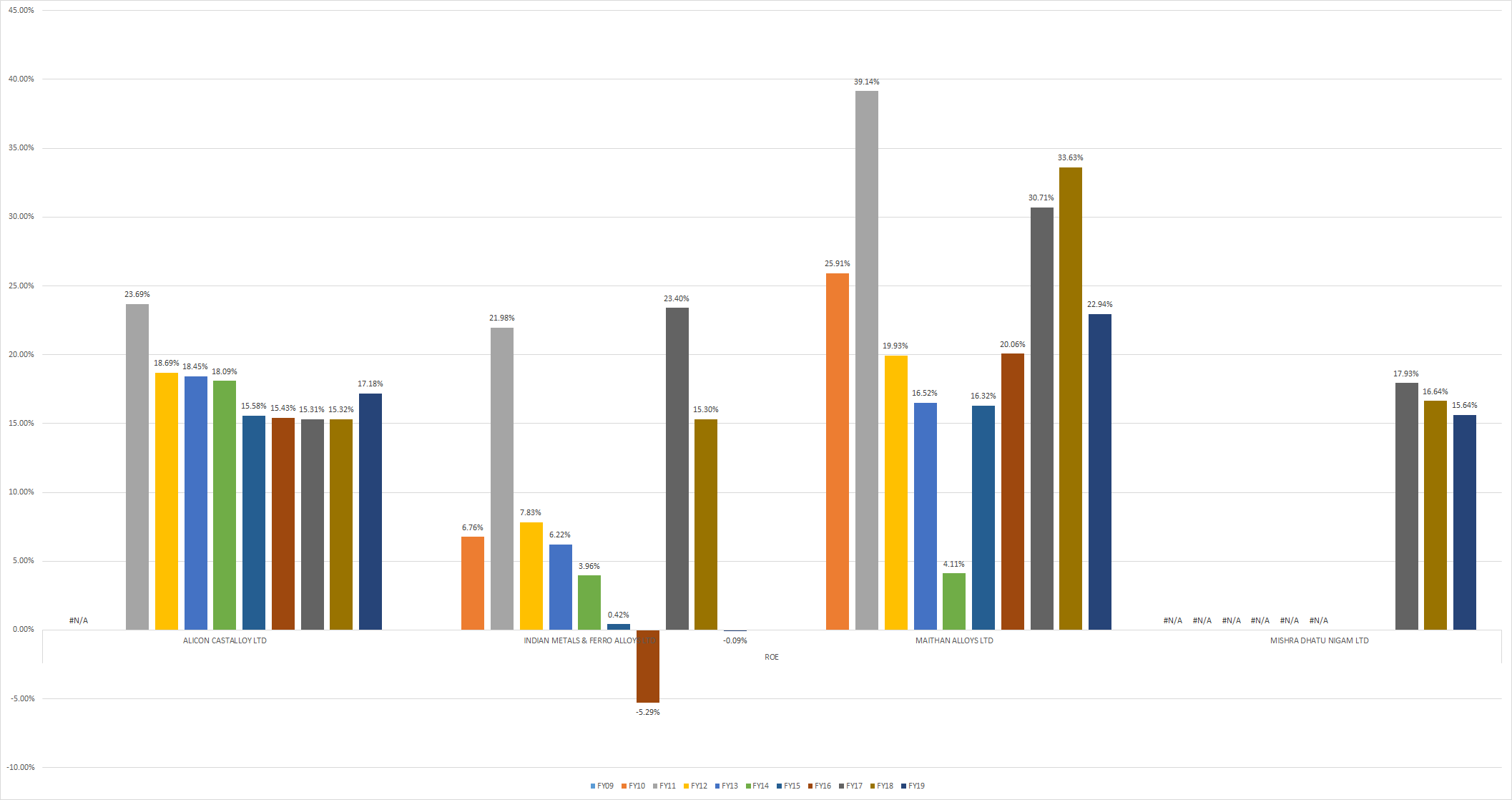

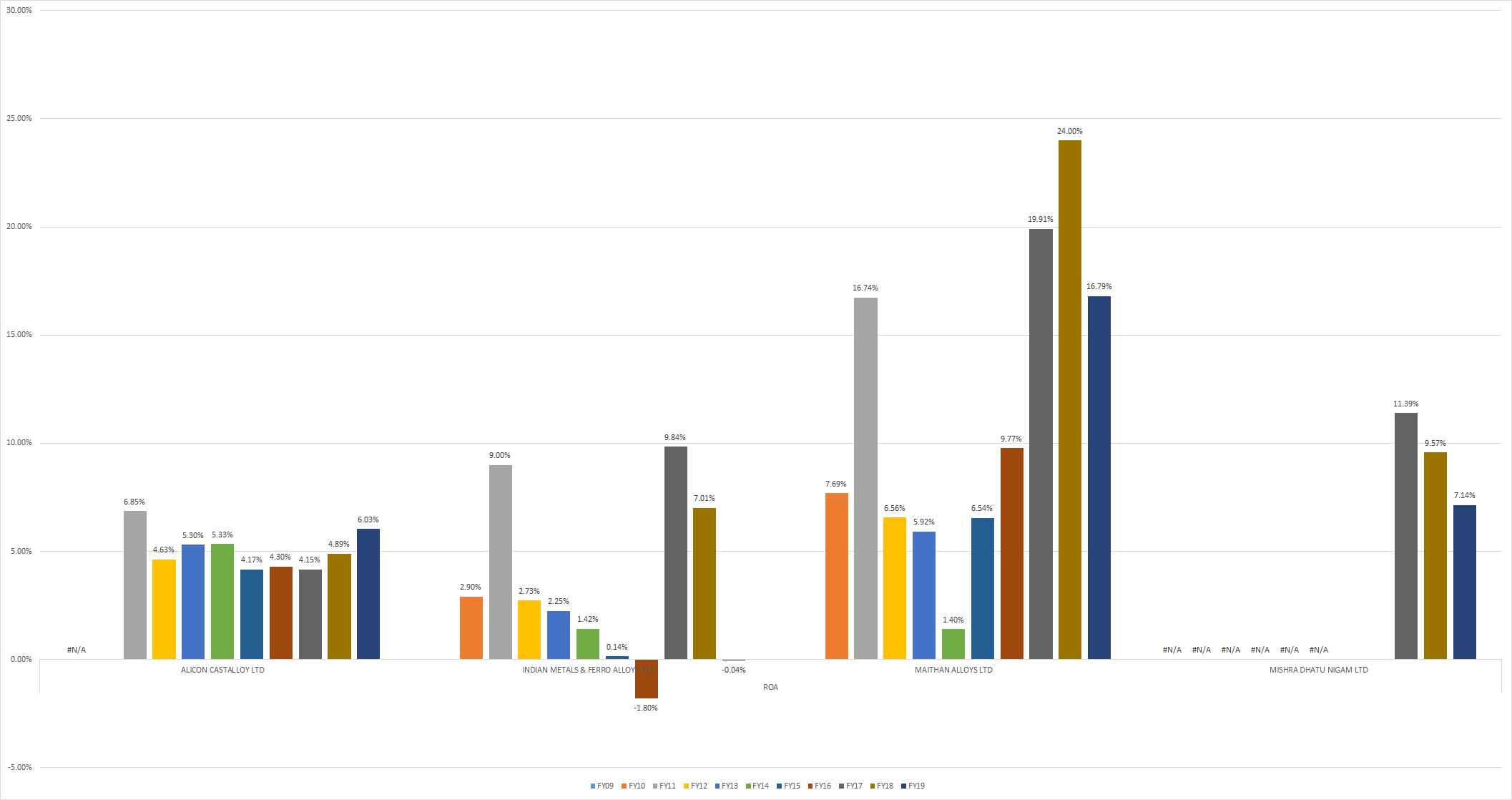

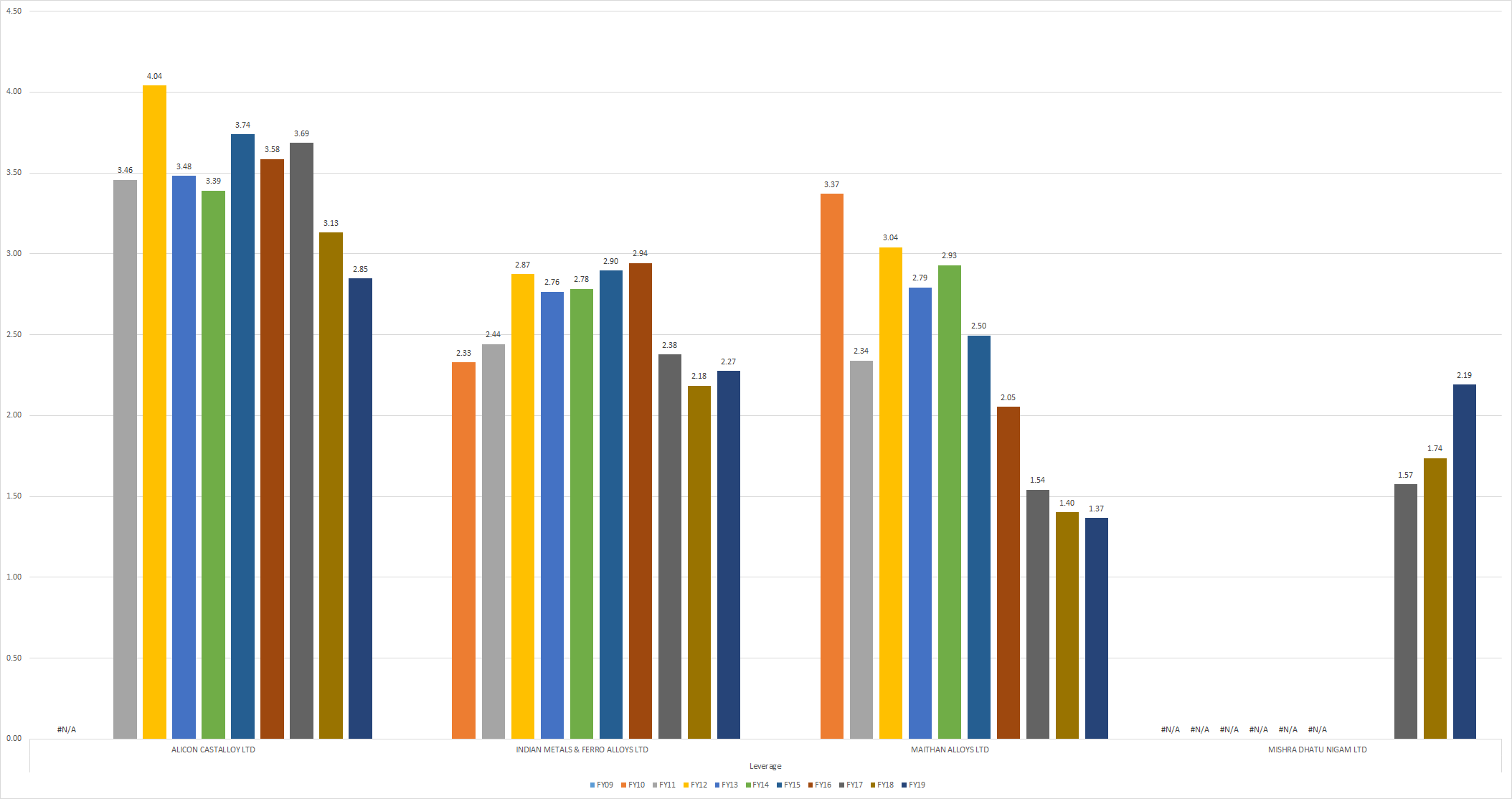

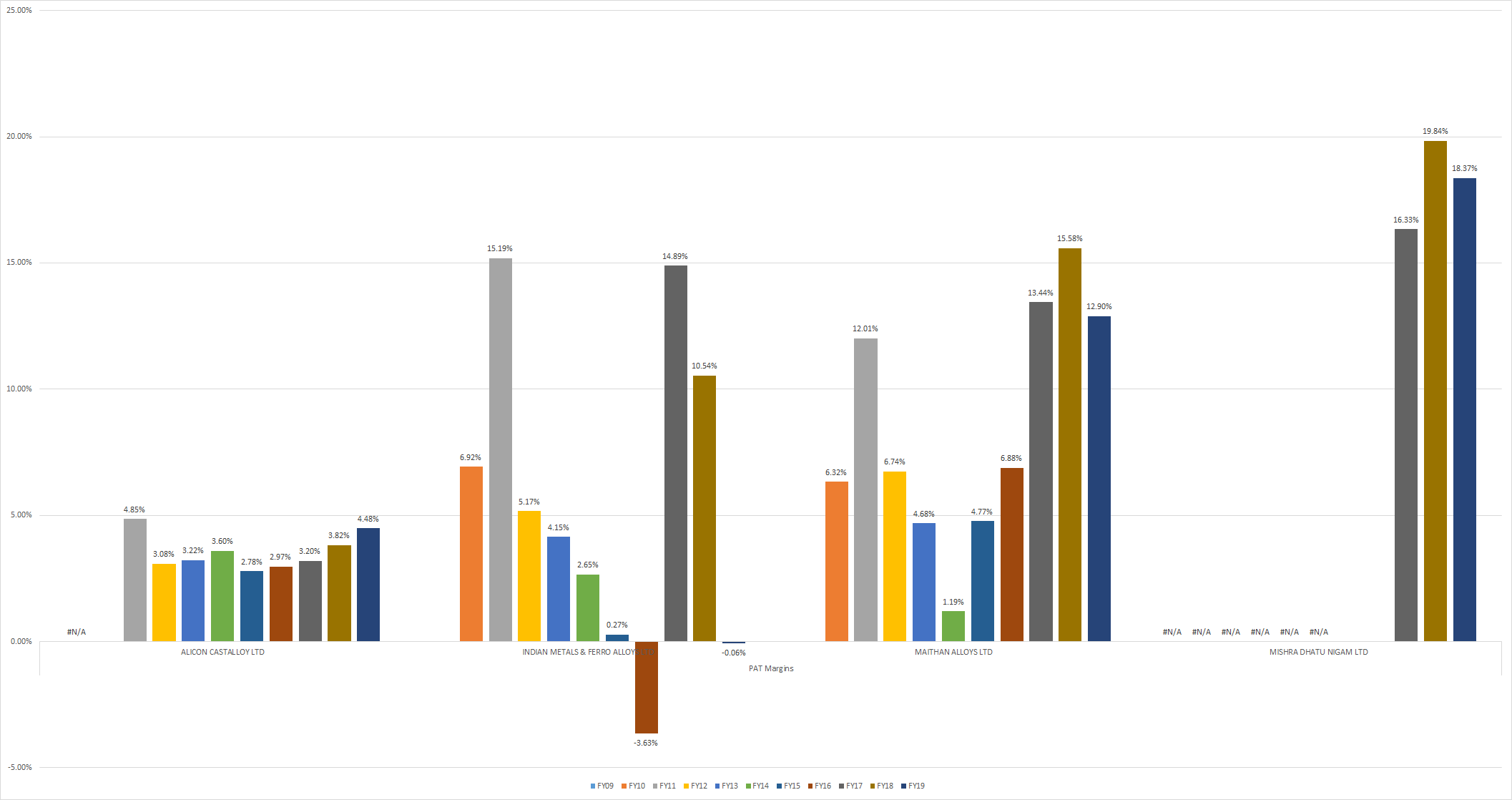

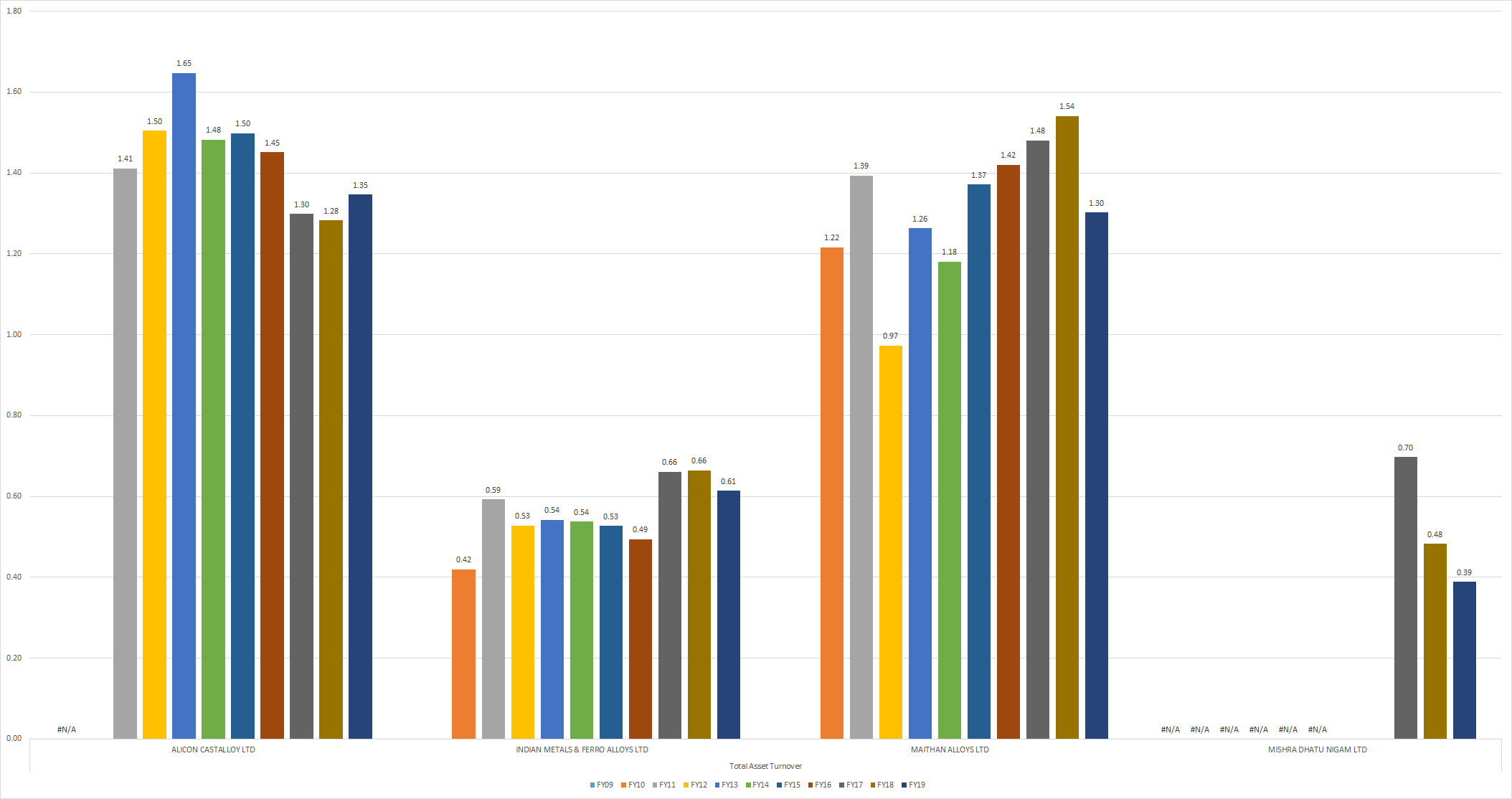

The company has consistently outperformed its peers in terms of ROE. Dissecting the ROE we see outperformance in ROA as well while the multiplier effect of Leverage is lower than peers. So focusing on the two components of ROA, we see some dominance in PAT margins relative to peers, while the real outperformance comes from Asset Turnover.

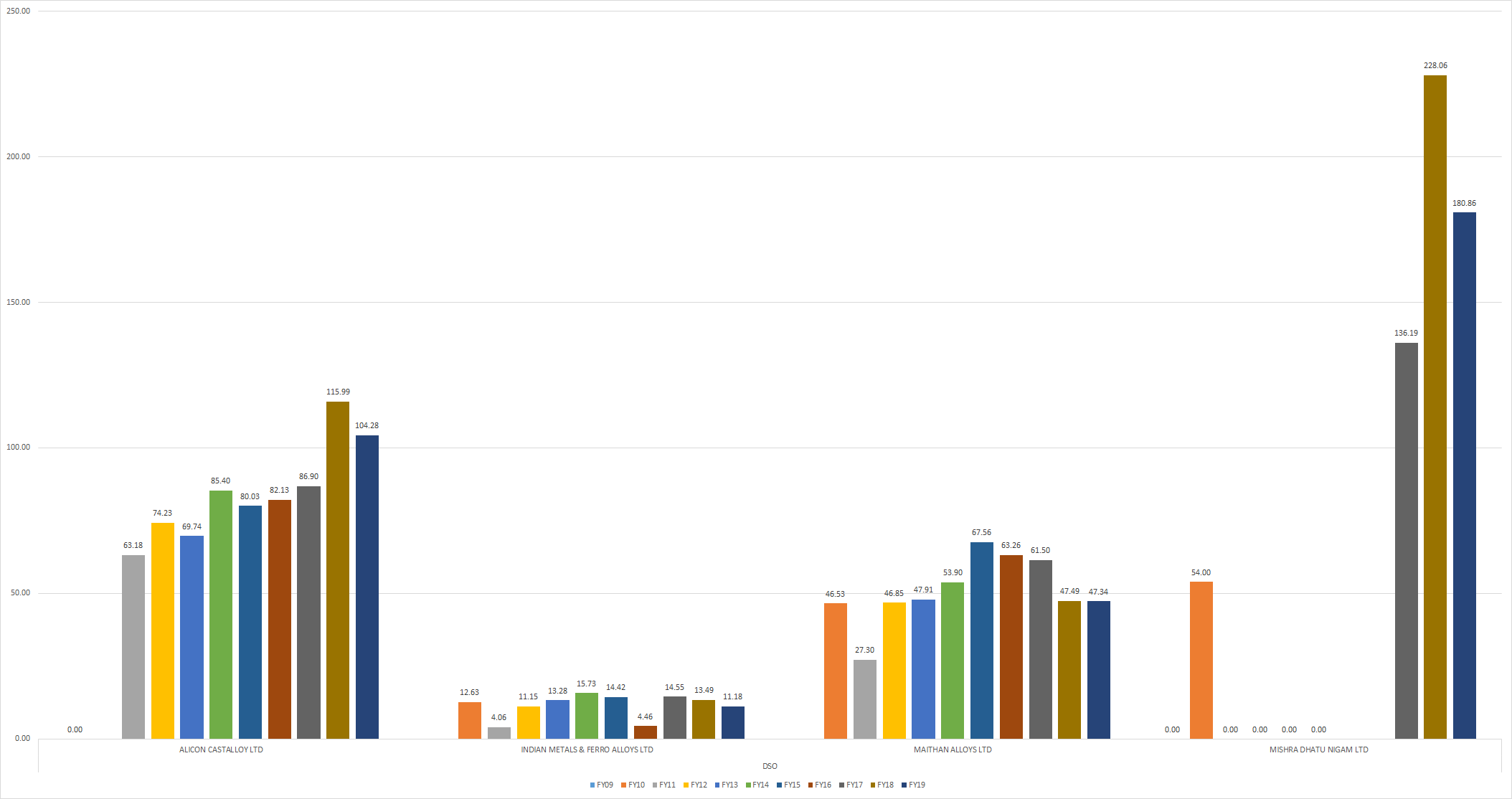

Further dwelling into the asset turnover we see almost 2x outperformance in terms of inventory turnover against IMFA. In terms of DSO (Day of Sales O/S) IMFA’s numbers are unbelievable, while MA’s seem more standard. I do not have the data for the payables comparison.

Coming to margins, MA’s lower tax % hints at an SEZ connection. Would be good to check how much time remains in the tax holiday for their EOU.

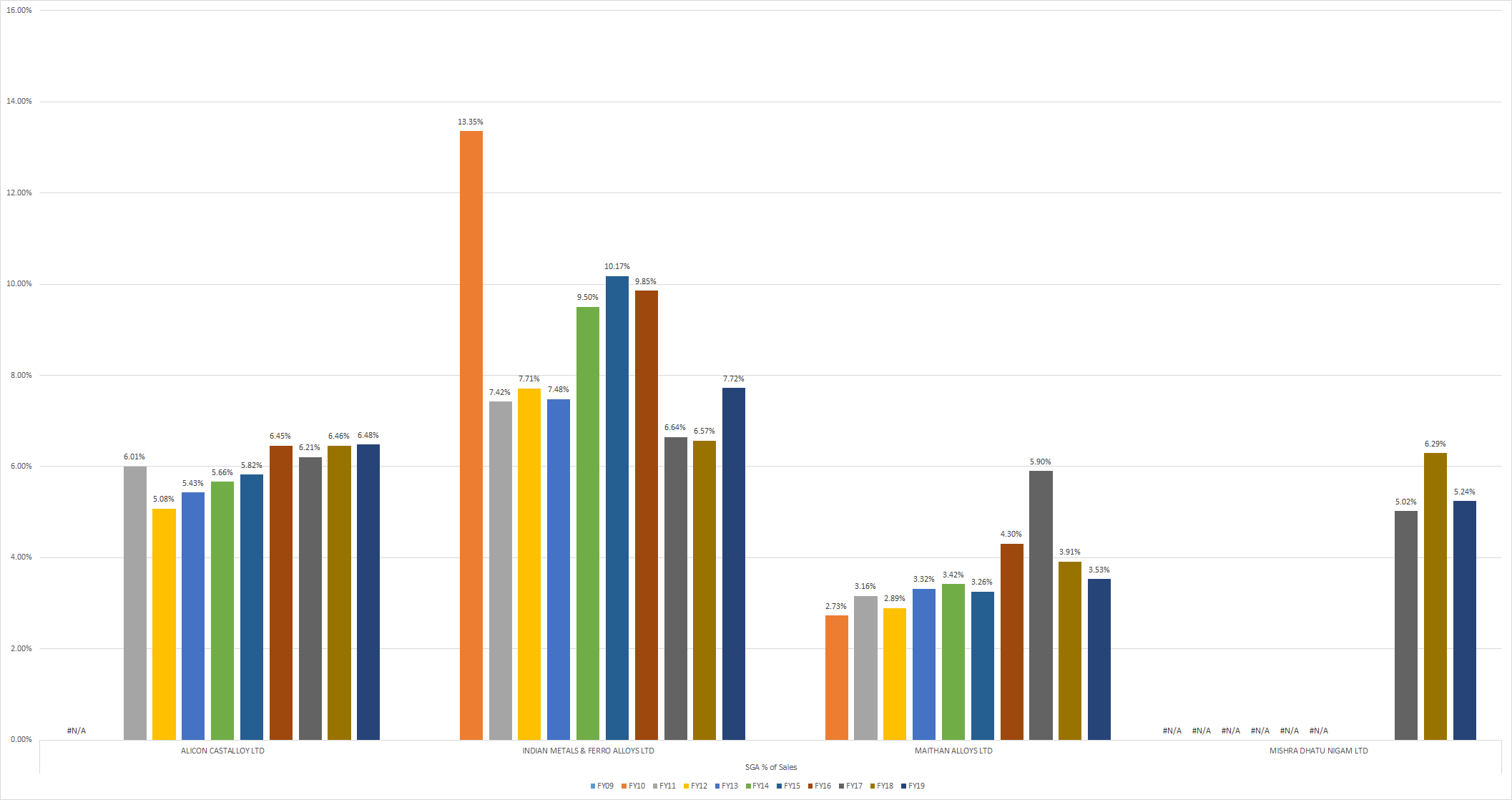

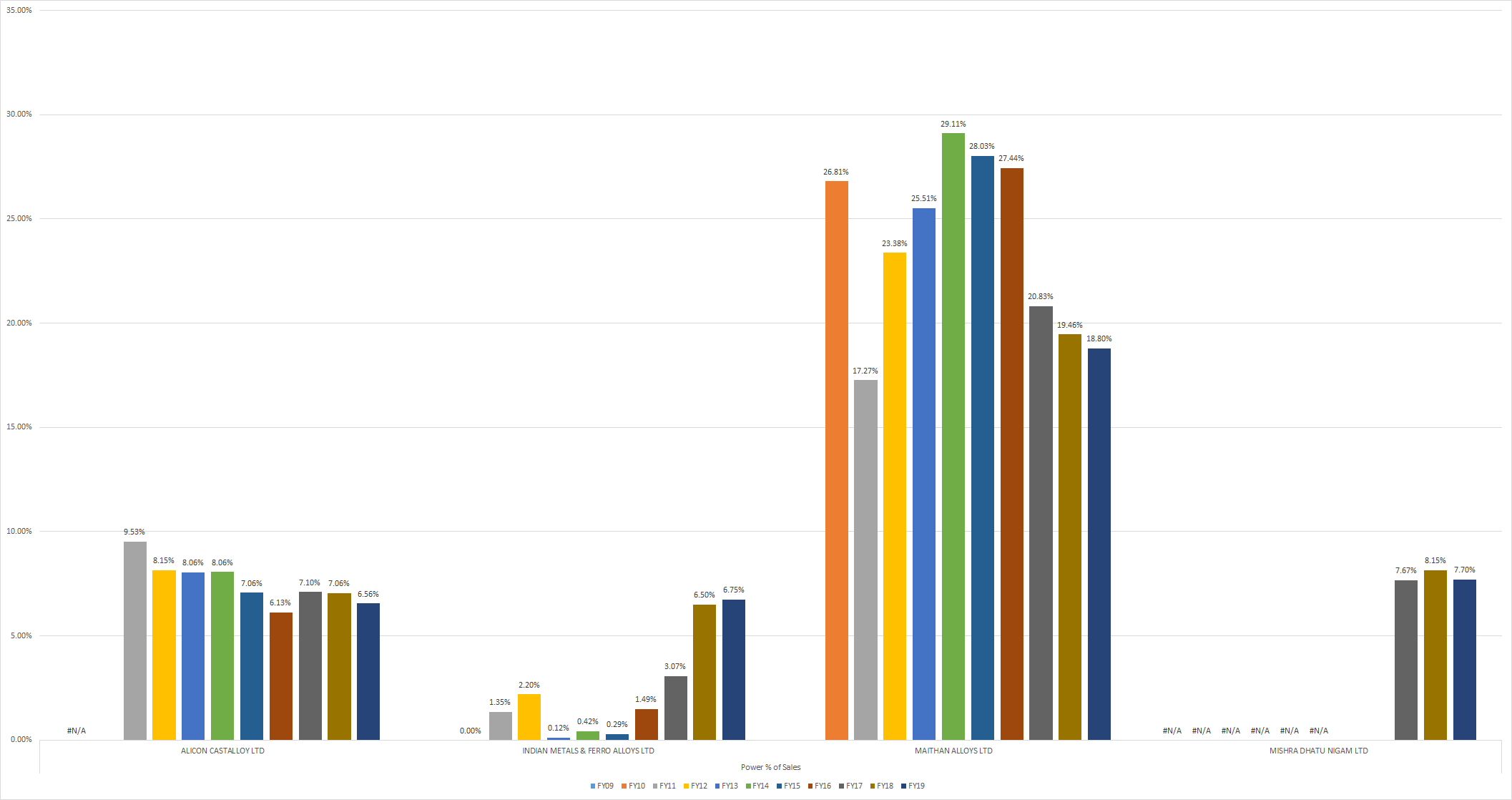

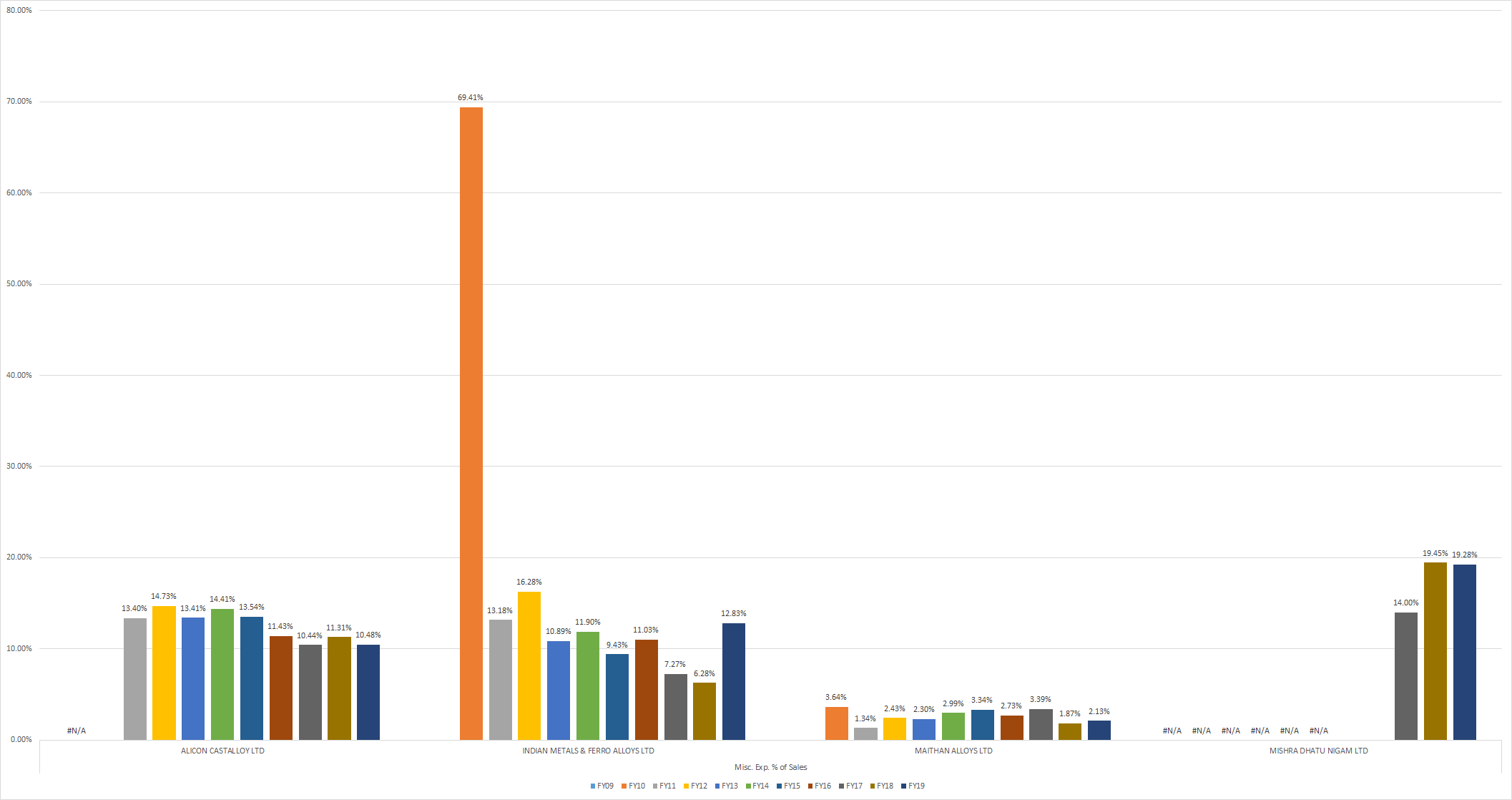

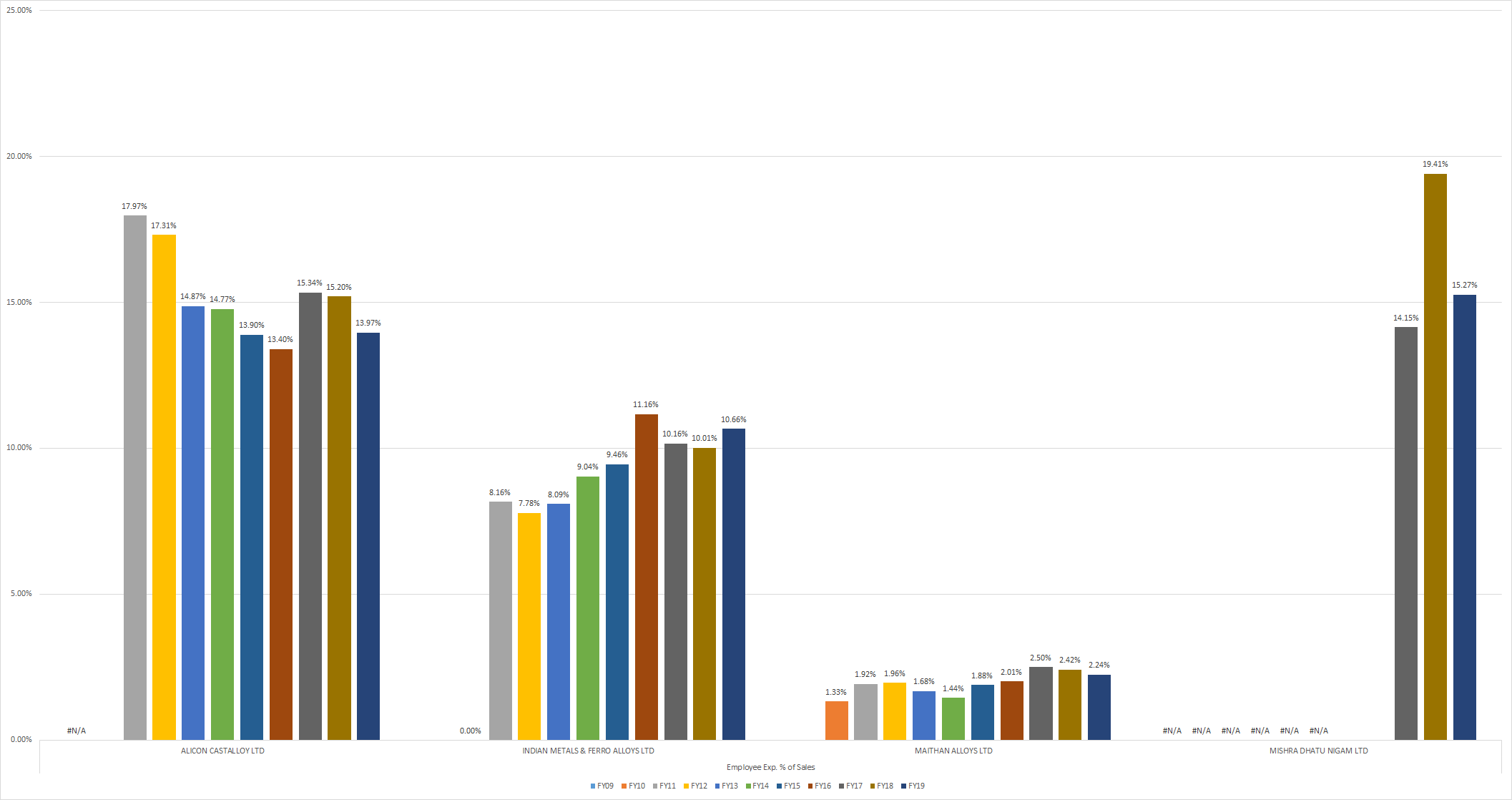

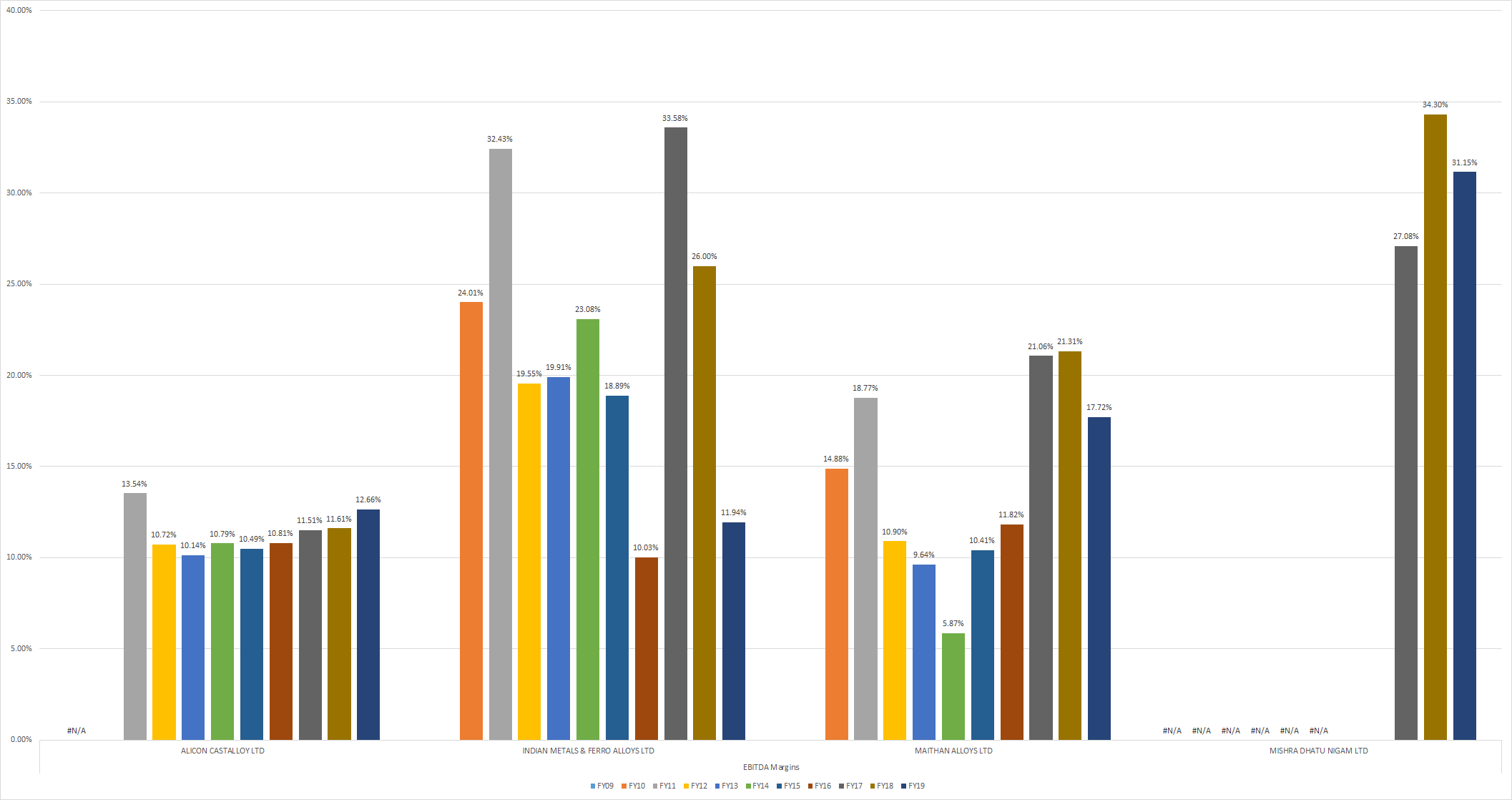

We see some positive outliers in terms of SGA/Revenue, Employee Exp./Revenue, and Misc. Exp./Revenue but a big negative outlier in Power Exp./Revenue which results in a very closely comparable OPM between IMFA and MA.

While these businesses are not completely like for like, the differences in the above parameters are somewhat too different to ignore for businesses which are somewhat similar. We need to find the underlying reasons for such outperformance in productivity/efficiency in utilizing inputs such as employees and assets and such underperformance in power expenses.

Sharing this in case you or others can share some more insights into why such differences are there.

Frankly, i don’t try to read too much into every action n give more weightage to bigger impact items where they ve more control under them to from mgmt n execution perspective to create significant positive or negative impact . Company submitted presentation for Q3.

SAIL forms 80% of the domestic sales. This raises the question as to why is Maithan not dividing its business among the private players. SAIL is talking about producing Ferro alloys in-house to mitigate raw material risk. One would think that since Maithan is the lowest cost producer, he will find another customer without any problem. But why doesn’t he have JSW and Tata as its customers? The only reason that I can think of is that they manufacture it in-house since they already have access to manganese ore mines.

Free Cash Flow : 307.53 crs

Therefore, its available at 2.53x

Capital Employed from 2010 to 2019 : 331.25 crs

Cumulative Earnings for the same period : 1315.48 crs

Net Income generated between 2010 and 2019 : 282.94 crs

So,

Out of the cumulative earnings of 1315.48 crs , only 331.35 crs were deployed back in the business, 48.94 crs were given as dividends. Other major capital deployed in investments though only 82% of net earnings have been converted to cash flow from operations.

So if we simply think , we have have business which have generated 282.94 crs in earnings on capital deployed of 331.25 crs and which is available at 2.5x of free cash flow.

More dividends could have flowed to shareholders but being in the cyclical industry, its better to always have cash.

The business in FY 20 will generate around approx 260 crs of EBIT and the whole company can be bought at an EV of 783 crs (EBIT / EV = 33%)

They kept 600 crores in hand to bid on distressed assets/companies. They even won the auction for Impex Metals but for some strange reasons, Impex was sold to someone else. I have written about it somewhere above.

Yeah I remember that in the past they told they will be on a look out for an acquisition.

But this is one company that

Is a better investment than a 10y corporate bond since current corporate bond is available at a PE of 15 with no earnings getting reinvested for 10 years.

The valuations are hitting hard on head with a cricket bat.

Earning growth is dependent on High Reinvestment Rate (which in case of Maithan is around 95%) and Return on Capital (which vary from 30-40%). Thus giving us the earning growth of 28% over a long term period. In 2018, Maithan retained 97% of their earnings but had a degrowth of 15% in 2019 earnings (keeping the ROE as 22% , earning growth should have been atleast 20%)

Q1. What are the existing assets that Maithan have and new assets that Maithan will create to keep that return on capital sustained ?

Q2. What reinvestment opportunities do Maithan will tap on to keep that high reinvestment rate ?

Its interesting to think in a way how management of Maithan will be thinking.

I have been reading up on MA and based on past bull and bear steel cycles, here are two hypothetical scenarios of how the company should look like at the bottom of the current bear cycle, and at the top of the next bull cycle.

Bottom of bear cycle

Expected year ~ FY21 or FY22 (generally its 3-4 years after the last peak)

Topline ~ 2000 cr. (similar to what we have today)

EBITDA margins ~9% (at worse point, margins can go down to 5% as well, but that situation doesn’t last long as most players go into red below 8% margins)

Depreciation ~ 20 cr.

EBIT ~ 2000 * 9% – 20 ~ 160 cr.

Other income ~ 7% * 500 cr. (cash and investments) ~ 35 cr.

Interest charges ~ 0 (no debt now)

PBT ~ 160 + 35 – 15 (miscellaneous expenses) ~ 180 cr.

Tax ~ 25% * 180 ~ 45cr. (SEZ tax benefit is until FY2021)

PAT ~ 130 cr. (peak PAT during last bull cycle was ~292 cr.)

P/E ratio ~ 2

Cash & equivalents ~ 500 cr.

Market cap ~ 2*130 + 500 ~ 760 cr.

Top of next bull cycle

Expected year -> FY21 + 3 years ~ FY24-FY25

Topline ~ 3500 cr. (Current greenfield investment of 275 cr will generate incremental sales of 3 * 275 + nominal growth due to brown field expansion)

EBITDA margins ~ 18%

Depreciation ~ 50 cr. (putting a higher than expected number)

EBIT ~ 35000.18 – 50 ~ 580 cr.

PBT ~ 550 cr. (Miscellaneous expenses of 30 cr.)

Tax ~ 25% * 550 ~ 140 cr. (SEZ tax benefit is until FY2021)

PAT ~ 410cr.

P/E ratio ~ 10

Market cap ~ 41010 ~ 4100 cr. (I am assuming that cash of 500 cr. was spent in growing topline)

Current market cap ~ 1400 cr.

If the cycle plays out according to projects, we can have a 3-bagger in the next 6-7 years, with a potential downside of 50%. I am not looking to buy at current market prices, but will like to hear thoughts from others who have been tracking MA. @jitenp - do you track this company?

Key Risk: SAIL accounts for 80% of domestic procurement (i.e. 40% of overall topline) and they are planning to manufacture their own ferro-chrome.

They got the cash in the last up cycle (2017-18). They are now setting up a greenfield capacity in Bankura (~275 cr. CAPEX, currently awaiting regulatory approvals, Pg27AR2019). This will increase their overall capacity by 48% (from 235’000 MTA to 355’000 MTA). This is the first time where they don’t have to take debt to increase capacity, which makes them more resilient and also the lowest cost producer. Company has maintained a consistent dividend payout where they paid dividends in the worse of times. It makes sense for the company to hold cash if they can deploy it at incrementally higher ROCEs.

Well the sept 2019 balance sheet shows 600 crore worth cash,surely they can increase dividend payout if the expected capex is 275 crore.In the meantime they can expect accruals from their operations too.

What other way is there to know if the management is willing to pass on the additional profits to the shareholder?I am not criticizing the management here and indeed it is admirable to not let go of the minority shareholder’s hand in troubled times,but the shareholders expect more than a constant dividend.Even this year the company has paid a interim dividend of 6 rs on an eps of 87 rs,which comes to a dividend payout of 7 percent.But i am guessing they may still pay another dividend for FY 20.

You can take it up with the management. I am simply looking at their past track record over the last 3 cycles, I understand the cyclicality of this business. There are lots of companies that have gone bankrupt because of leverage in this business as downcycles can last for 3-4 years. The management has also stated that they are looking for acquisition candidates out of NCLT. They haven’t found anything yet. I do understand that cash make people do stupid things, but a lot of managements are rightfully conservative about their cash positions (NESCO, Wonderla comes to mind). Its a matter of incremental ROCEs on whether cash should be reinvested or given back to shareholders.

Seems like most of the company’s competitors are under bankruptcy or having financial issues .Due to the covid related economic slowdown,a lot of them may face additional pressures.

1)Indian metals is under losses without much cash in hand

2)navbharat is heavily indebted with a roce of 8.8 percent,though the financial condition seems ok.

3)Ferro alloys is undergoing insolvency

4)Balasore is undergoing financial troubles and has had losses from the past 2 years.

5)Rohit ferro is also under insolvency.

They have been holding that cash to bid for some distressed mine assets under IBC. They successfully bid for Impex Alloys at one such auction but after they won the bid, their bid got cancelled for some strange reasons. I have written about it somewhere above in the same thread.

Company came out with their results, FY20 revenues came at 1830 cr. vs 1979 cr. in FY19. EBITDA margins for the full year is 12.7% which shows that the sector is probably not in red yet i.e. we probably haven’t reached the bottom of the cycle. No more dividends for the year, all their debt investments have been redeemed which leaves them with a hefty bank balance of 638 cr. I will update the post once they come out with their presentation and annual report.