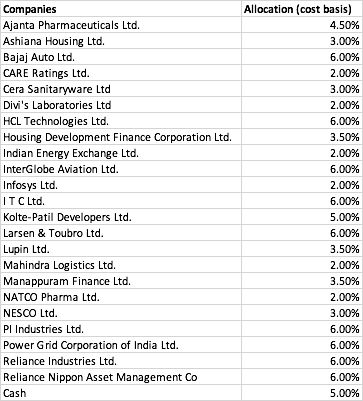

As of today, I reduced weightage of Lupin by 1% (from 4.5% to 3.5%) and increased weightage of Ajanta Pharma by 1% (from 3.5% to 4.5%). This is because Ajanta has near term earnings visibility (~20% upto FY22 due to expansion in US generic markets). Apart from this, I am closely tracking the following companies which are close to my buy range:

- Maithan alloys - Detailed thesis can be seen at this link Maithan Alloys Ltd - #232 by harsh.beria93

- Avanti feeds

- HDFC AMC

- INOX Leisure

- Vinati Organics

I will post the detailed thesis after creating a position in the specific company. The updated portfolio looks like this: