Valid observations, for the 1st point their debt investments were redeeming in FY20 so I guess its just the redemption (they didn’t invest in debt mutual funds but in bonds of specific companies). For the second point, the quantum of payable decrease was also surprising for me whereas inventory and receivables increased marginally. As the management hasn’t yet announced a conference call, we might need to wait for their annual report or a virtual AGM.

2 Likes

Company came out with an explanation today, payables have been reduced to foreign creditors to avoid paying a larger sum of money due to rupee depreciation.

https://www.bseindia.com/xml-data/corpfiling/AttachLive/ab5e62da-a307-48b0-aa0c-2051d3943f24.pdf

2 Likes

PE Multiples will not be so low at the bottom. When earnings are low multiple will be high. PE at last trough was ~20.

1 Like

I have started to follow this company after hearing the concalls of steel companies for Q4FY20.

Overall commentary sounded positive on the steel sector as a whole and I was looking for players who could benefit due to this

Folks who have been following this company closely can someone confirm if this could be a direct beneficiary if the steel sector does turn up.

Any inputs/thoughts would be helpful

50% of their revenues are naturally hedged due to export, what was the need for them to pay off liabilities n do nothing about receivables? How well can we rely on management’s commentary?

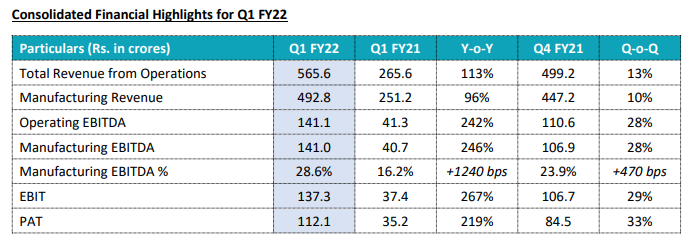

Interesting results today, they somehow were able to increase their manufacturing EBITDA margins to 16.2% from 13% in the last quarter. They are seeing greenshoots in the Indian steel market, driven by rural demand.

3 Likes

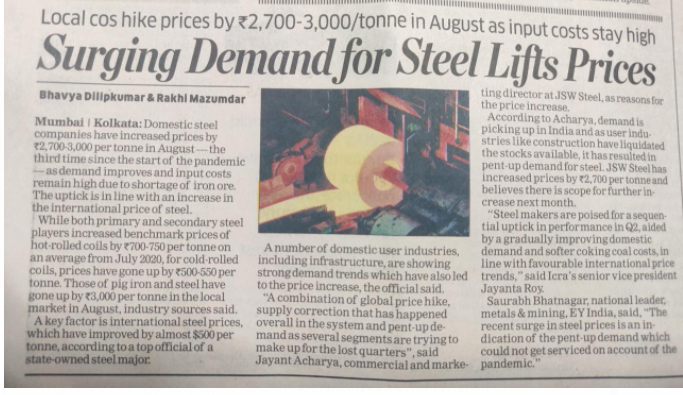

Can any one please provide insight on the impact on Maithan Alloys based on this article published in ET paper 21st Aug, 2020 edition.

1 Like

Very positive for maithani alloys…As it’s products are used for steel.plants

1 Like

If anyone attending the AGM tomorrow, could you please ask management what the impact would be if SAIL procures 2/3rd of their alloys requirement internally? As Maithan’s domestic revenues are dependent on SAIL.

This care rating report contains very useful informtion such as the raw material suppliers, credit terms given, etc. I found it much more useful than the CRISIL report.

2 Likes

So, As per H1FY21, company has cash equivalents of 820 cr and market cap of 1485 cr (CMP Rs 512.50) with yearly CFO of 200 crores. I am not sure what am I missing in the company. Usually people do stupid things with such high cash in hand and I hope Maithan doesn’t do it. I fail to understand what promoters want to achieve by not giving dividends. I think they can do 3 things with the cash

a) Go for Delisting (Pretty sure investors will not make much money)

b) Go for capacity expansion by adding new capacity or acquiring companies

c) Do diworsification

Let’s see what we get to see in future.

Disc. Invested and Biased

3 Likes

Sharing my two cents. Recently started looking at this company.

Maithan is a solid play on the long-term steel production/ infrastructure development in India. Maithan makes manganese based ferro alloys which go as inputs into steel manufacturing. Every 1 tonne of steel needs about 1-1.5% of manganese-based alloys. Maithan is not a commoditised business and operates with a ROCE of 25%+ consistently. The company is one of the most efficient alloy manufacturers in the world – as expected it is a bit of an outlier in the industry. This high ROCE is broadly the result of the fact that the company is obsessed with continuous efficiency improvements with investments in latest technology processes. Maithan also produces higher valued added products and alloy grades on which it can earn higher margins. Company’s capital allocation policy is very clear that it will focus on remaining a very efficient converter and not backward or forward integrate (into manganese ores or steel production). Maithan is the largest and the most profitable Mg alloy producers in India.

Competitive advantages:

- Lowest cost producer over the years and the most profitable alloy manufacturer (link)

- Long standing customer relationships with steel producers in both India and abroad

- Three facilities – two for domestic and one for exports. All equipped with the latest technology to aid in being the lowest cost producer.

- Competitive advantages are evident in gross margins and ROCEs which operate in a steady band and ROCEs which are surprisingly high for a metals alloy producer.

- Strong cash flow conversion except when setting up a new facility; visible in the cash build up and consistent dividend pay-outs across cycles.

Scalability :

- Steel demand globally grows at 2-3% CAGR; Asia ex China ex Japan grows at 5% and that in India has been growing at 7-8% CAGR. Indian steel demand should continue at this rate for a long time to come. Indian per capital steel consumption abysmally lower versus developed countries.

- Maithan has been growing volumes at 15% CAGR over the last 15 years which demonstrates share gains and scalability of the model. Revenues are a function of supply – capacities being set up by Maithan. The company is conservative and sets up a new capacity only after running for a while at peak utilisation. Prefers to use internal accruals (high ROCE helps) and does not like leverage. Except in downcycle years, demand is not a constraint – both due to secular demand trends in India and share gains for Maithan.

- Maithan has about 10% share of the Indian market and about 1% of the global market for Manganese alloys. It is the largest in India and has been gaining share.

- Maithan announced new capacity in WB in FY18 which should be fully ramped up by FY23-24; this will increase overall capacity by 50%. There is not upper limit on how much more capacity Maithan can set up.

Culture: - gleaned off after reading multiple years of annual reports and verifying with financials

- Mgmt. focussed on profitability and ROCE more than growth for its sake.

- Conservative approach in taking leverage and expanding capacities or making acquisitions.

- Understands that in a relatively commoditised business, the only way to survive is to strive to become the most efficient producer. They also focus on offering value added and a high degree of customised products to customers which helps realisations.

- Customer focus comes through clearly in their commentary. Prefer to not pass RM increases to customers and instead try to offset them through efficiency initiatives and value-added offerings. This may be helping them be the price leader as well as the cost leader helping continuous share gains.

- Company buys raw materials only in-line with orderbook and does not try to take a call on the commodity cycle by opportunistically purchasing more or less.

- Promoters own 75% of the company.

Price:

- As of Oct 2020, stock trades at about 6xTTM PE. Historically it has traded between 5x and 15x so current valuations offer a high margin of safety. From current levels, stock can substantially rerate over the next five years as a) cycle can only get better from here (5-6-year cycle typically) driving earnings growth b) once market cap cross Rs30bn (from current sub Rs15bn), institutional discovery of this company will start gradually.

- Versus the current market cap of Rs1400cr, company has cash on books of Rs650cr which means that adjusted for it, the stock trades at a very low multiple of 2.5x EV/EBIT. This is a very low multiple for a company which across a full cycle can grow earnings by 15% with 25%+ ROCEs. Multiple can easily double over the next five years.

- On a five-year basis, assuming a modest cyclical upturn (no major price increase but just the new capacity coming up) can drive a 25% IRR for the stock. If there is a stock upcycle, returns could be 30-35% CAGR. Downside risk (of a substantial derating or very weak earnings) is minimal from a five-year view given we are already in the weaker part of the cycle.

12 Likes

Maithan commentary post Sep-20 results is positive

3 Likes

Recently updated my research on Maithan since I’ve been owning it from 2018. I’ve attached the PDF here with my findings and personal judgements on the Company and industry and also done a rough back of the envelope calculation on valuation. Based on this I’ve added to my position in the Company.

Please feel free to add to this or correct it. Maithan Alloys.pdf (959.3 KB)

Edit: Sorry I forgot to update the Financial Snapshot. Updated now.

12 Likes

Maithan announced decent set of numbers for Q4,

Q4 sales of 499cr and profit of 85cr

Overall Cash stands around 800cr and moderate increase in Inventory and Receivables. Need to see how it moves in coming quarters.

do they have a call?

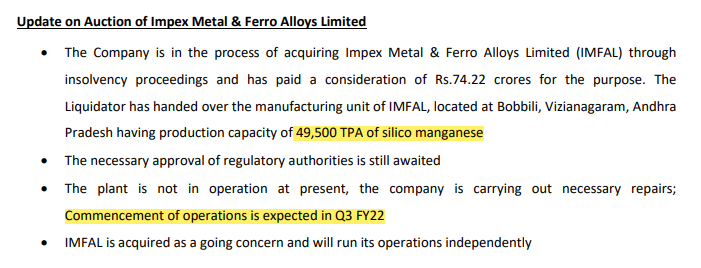

NCLAT approves the sale of lmpex Metal & Ferro Alloys (IMFAL) to Maithan at 74.22 cr. This should increase their capacity by 49’000 TPA of silico manganese (or 70’355 TPA of ferro manganese). For context, Maithan’s current capacity is 226’000 TPA, so this add 20%+ to their existing capacities.

IMFAL’s manufacturing unit is located in Bobbili, Vizianagram (Andhra Pradesh) and is 126 km from Vizag port. Manufacturing has been shut for >2 years.

Disclosure: Invested (position size here)

7 Likes

its possible that their FY22 EPS may be upwards of 200 given the upward trending prices !

Disc: Invested

3 Likes