The Quarterly results are out and its a loss in the income statement.

PBT Rs. -22 crore as compared to Rs. 29 crore last year and EPS (Diluted) Rs. -2.21 as compared to Rs. 2.60 last year.

Both consolidated and standalone results can be found in the below BSE link.

and in invetor presentation they have mentioned that quarter has positive free cash generation in Q1 F20.

link for that

Fellow VPs Please explain me Company has reported net loss for this quarter which we can see in the Income statement but if their cash flow are positive for this quarter where we can see that?

I tried going through the Annual reports from 18 to 20 of Mahindra Logistics in this video. This is my first ever video please forgive me if I made any mistake.

A 1000 cr deal(200cr/yr) for logistics transformation for Bajaj electrical, this could set a trend for similar such mega deals and position Mahindra Logistics a league apart. This leverages on group strength e.g. electric vehical stc.

These likely requires a mix of expertise around tech+warehousing + manufacturing ops + transportation ( EV usage being called out)+ Large Program management etc.

While it clearly gives revenue visibility, Would be interesting to understand margin profile

MLL through EDEL will enable Flipkart in its journey towards building a green supply chain by not only deploying a large fleet of EVs but also creating a conducive environment for EV deployment and operations across the country. This includes building supporting infrastructure and technology such as charging stations and parking lots, training workforce, route planning and even battery swapping stations in the near future. Another key focus area will be technology and control tower operations to enable greater efficiency and cost competitiveness

Flipkart has recently announced its partnership with leading electric vehicle manufacturers, including Hero Electric, Mahindra Electric and Piaggio, to deploy EVs in its logistics fleet across the country.

EDEL by Mahindra Logistics is a last-mile delivery cargo service on Electric Vehicles. EDEL provides multiple offerings, including package & trip-based services. These offerings provide customers with a scalable, sustainable and cost-efficient solution. With a load capacity and enhanced range that compares well with existing ICE options, EDEL gives customers in the E-commerce, FMCG, Pharmaceutical, Consumer Durables and Electronics industries a significant edge in efficient and responsible distribution and last-mile delivery solutions.

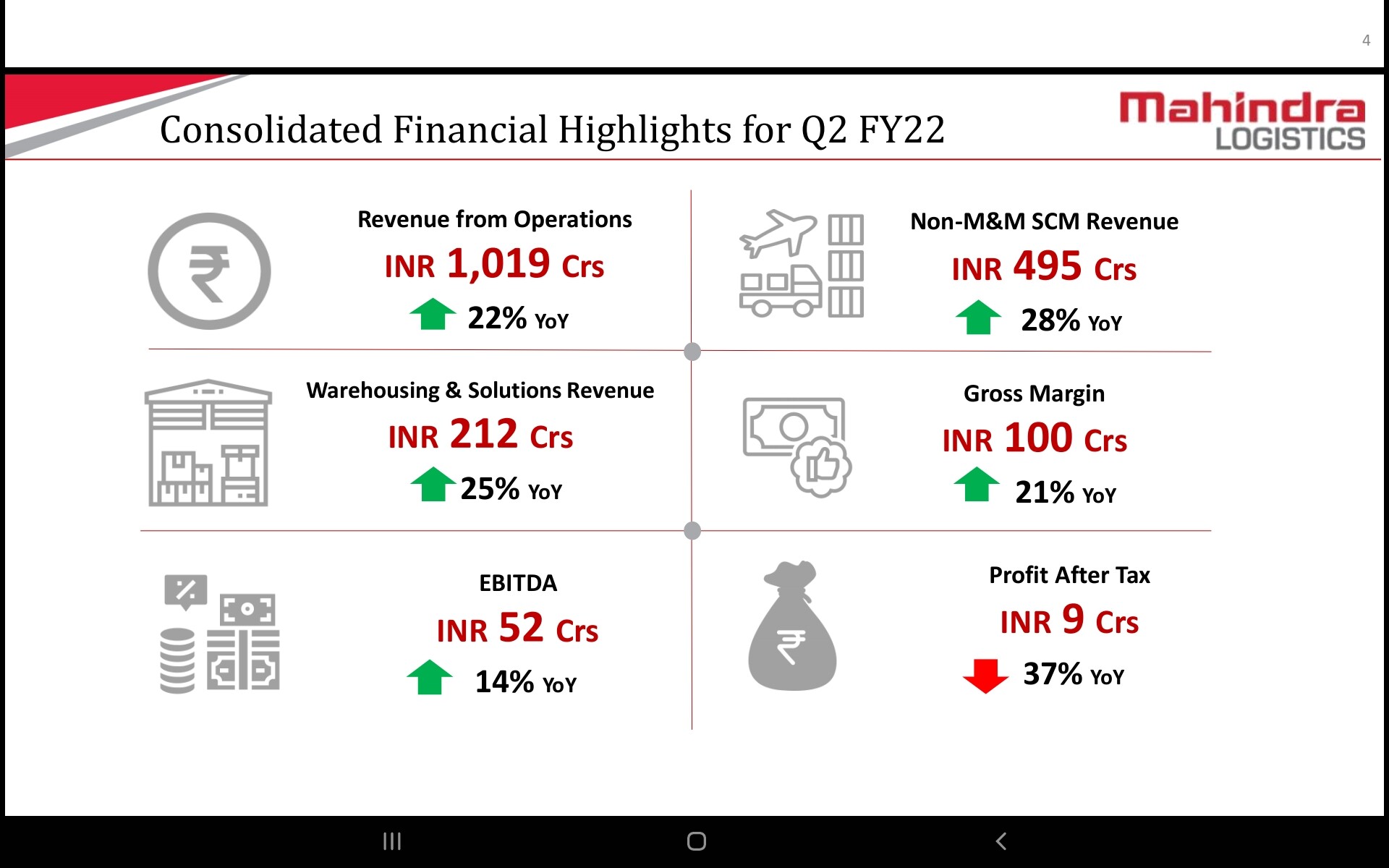

Overall a good result from the company.Good amount of Revenue & PBT growth,However there is a dip in the gross margin.Is it due to crude inflation??

Investor presentation attached. MLL Investor Presentation (mahindralogistics.com)

Hi,

Mahindra Logistics has fallen from 500 to 390 levels in a span of 1 month. I am wondering if I missed any news or are there any specific triggers for this fall.

Just started reading about this company and seems lucrative given the market size, and the company size and the Mahindra group. They even bought tech (and existing clients for express) from rivigo at steal prices.

I will go through its last few con calls but trying my luck here on this thread if I can get my answers?

Why is depreciation so high? Does it include rentals or does the money stays with company and can be used to repay debt? And the entry is just an accounting standard?

If yes, it’s great else servicing such a huge debt seems difficult in near term. Anybody has any insights on the debt serviceability?

No, tthat doesn’t seem to be true. The interest component has increased along with it. As per screener Sep22 debt is 538cr, and quarterly payout is 11cr which makes 44cr annually and is very near to 8% mark.

under IND AS 116, all leases are required to be recognized on the balance sheet as a right-of-use asset and a lease liability. This means that companies will now recognize interest expense on all leases, including operating leases, over the lease term. So, companies may see an increase in their interest expense.

Under IND AS 116, the right-of-use asset related to a lease will be depreciated over the lease term. This means that the asset will be gradually written off over the period of the lease, which may result in a higher depreciation expense in the earlier years of the lease.

In summary, under IND AS 116, companies will recognize interest expense on all leases and will have to depreciate the right-of-use asset related to the lease over the lease term. This could result in higher interest expense and depreciation expense in the earlier years of the lease.

I did not understand this from the quarterly call. Can someone explain what is India’s impact mentioned here? Also for acquisition, do we consider it as intagible asset or tangible asset ? How do we depreciate them over time ?

Sure, thanks for the elaborative answer. And also, this depreciation has increased to

nearly INR55 crores at the consolidated level. So what's the normalized run rate we

can look forward to for depreciation?

Rampraveen Swaminathan: So I think depreciation has gone up. I think there are multiple components to that,

Alok. And obviously, a part of that has essentially been around INR10 crores of the

increase in depreciation because of the Meru consolidated effect on a full year basis

because of the mobility business which you acquired from Meru. So around INR8

crores of it have been the run rate impact of the MESPL business. So that's

approximately been around 20%, if you may, of the increase in the overall

depreciation, prior 22%.

The rest of it has been India's impact on it. In the remaining INR35 crores, INR36

crores, India's impact is around INR27 crores. And I can give a more specific number,

but I think it is around INR27 crores. The remaining INR10 crores is split between

electric vehicle, fleet addition, some other capital items, software depreciation and so

on.

From a run rate basis, I think MESPL and the Meru depreciation should be capped

roughly in this range. So we don't expect any significant addition there. And as far as

the MLL, the core 3PL business is concerned, I think we will see some normative

increase in terms of capital, which is in the same range as this year. This year we spent

a capital of around INR75 crores.. We expect it to be in the INR80 crores, INR85

crores range, at least for 2023-2024.

So we expect that to roughly be in that range. The warehousing will have a 116 impact,

but there's also a tail-off impact on 116 as some of the older leases come off. So net-

net we expect that we will be a little bit up, marginally up on the MLL side of the

business, probably 7% to 8% up on depreciation. The Meru and the MLL mobility and

the MESPL number should roughly be capped

Some more clarity on debt from recent quarterly call. I saw some messages along that line.

Okay, Saras. So let me take both those questions in some form. So I think on the debt

side, we do have around INR400 crores of debt on the books. It's spread across

multiple parts of the business. The largest part of it, of course, has been debt taken by

MESPL for the acquisition of the Rivigo business, which is a little bit around, roughly

around INR220 crores. That's long-term in nature and has a structured repayment plan

around it. I won't get into a lot of details, but it's a structured repayment plan on a

fairly, attractive coupon. But that is the largest part of it.

Apart from that, we have around INR150 crores, which is spread across within the

MLL side of the business, which has largely been investments we made, borrowings

we made to support acquisition of the Meru business from M&M in FY '21-FY '22

and for the investment in Whizzard. Those are the two larger parts of that, along with

some amount of working capital there. There are, of course, working capital lines in

the 2x2 business. There are working capital lines in the forwarding business as well,

and those are purely working capital lines.

Its not india impact

IND AS 116 (Indian Accounting Standard 116) is a financial reporting standard introduced by the Institute of Chartered Accountants of India (ICAI) that governs lease accounting. The standard was issued in 2019 and came into effect from April 1, 2019.

In the past, when companies leased assets, they only had to show the cost of the lease payments they made in their financial statements, and not the full value of the leased asset itself. But now, with IND AS 116, companies have to show the full value of the asset on their financial statements

#mahindra #logistics #analysis")