is Mahindra Logistics is good buy now, Price to book all time low and price to sales all time low and company continuously trying to expand the business

can anyone let me know what are the negative factors about their business model now

is Mahindra Logistics is good buy now, Price to book all time low and price to sales all time low and company continuously trying to expand the business

can anyone let me know what are the negative factors about their business model now

Last two quarters standalone EBITA margin jump to 8% from 5% .As per management this is because of the operational efficiency and can sustain going forward But the growth is not visible in the consolidated EBITA because of revigo acquisiton loss(-18cr).once the revigo EBITA break even happens (expected in q3fy24) Market may consider the growth and reward the stock

Hi,

Another bad set of results at the consolidation level. Seems like situation is getting worse instead of improving.

Q2 FY24 MLL Standalone compared with Q2 FY23

• Revenue Rs. 1,136 crores as compared to Rs. 1,195 crores

• EBITDA Rs. 74 crores as compared to Rs. 64 crores

• PBT Rs. 26 crores as compared to Rs. 15 crores

• PAT Rs. 19 crores as compared to Rs 11 crores.

• EPS (Diluted) Rs.2.59 as compared to Rs 1.5

Q2 FY24 (consolidated) performance compared with Q2FY23

• Revenue Rs. 1,365 crores as compared to Rs. 1,326 crores

• EBITDA Rs. 54 crores as compared to Rs. 68 crores

• PBT Rs. (8 crores) as compared to Rs. 17 crores

• PAT loss Rs 16 crores compared to profit of Rs. 11 crores

• EPS (Diluted) Rs. (2.21) as compared to Rs. 1.69

It is quite evident that the acquisitions made by the management is backfiring. They have not been able to streamline the processes yet. EBIDTA margins have deteriorated significantly due to higher operating expenses.

If we see standalone results it is improving, and they could have been better off instead of acquiring these loss-making cheap businesses. Even there is no revenue growth also.

Senior border please suggest your views!

Disclaimer: Invested, no buy/Sell recommendation.

Thanks,

Deb

Just checked that they are also participating in the ONDC program through their zipzap logistics service as a last mile delivery provider

does any one know about their Financial liabilities, that is increasing year by year and hitting hard on the cash flow (321 cr on FY24)

New CEO and MD - Hemant Sikka

Dividend 2.5 Rs per Share

Standalone business has done well in FY25

Still their cash generation poor

My calculation of open offer by Mahindra Logistics.

Right Entitlement 8 by 3.

If you buy 8 shares

Primary Purchase

Shares bought = 8

CMP = ₹404

Investment = 8 × ₹404 = ₹3,232

Rights Entitlement (RE)

RE Ratio = 3 for every 8 shares

So, you get 3 REs

Rights Investment = 3 × ₹277 = ₹831

Total Investment = ₹3,232 + ₹831 = ₹4,063

Exit Proceeds @ ₹404

Total shares = 8 + 3 = 11

Sale price = 11 × ₹404 = ₹4,444

Profit and Return

Profit = ₹4,444 – ₹4,063 = ₹381

Return = ₹381 / ₹4,063 ≈ 9.38%

Big assumptions: Price will remain Rs. 404, will it? In last month price moved 325 to 404.

Disc: Looking closely, may invest if gets attractive price. No investment as of now. Do your own research.

That’s a very big assumption One can apply some logic to it (thought that can be debated too).

Like for example…

The counter points to the logic could be, that company aims to pay off debt of 550 Cr. out of the proceeds and could save 50 odd cr. of interest payment as a result and become PAT positive in FY26 (?). Hence market will be able value more appropriately in terms of earnings multiple. But this is different topic than benefitting from the rights issue

But with the above assumption, only way, rights subscriber will make money, is if there is lukewarm response from market and there us huge over subscription.

@rajpanda Agree

I have calculated as below.

PE is not available so took CFO.

343 cr cfo

Current no of shares: 7,21,31,470

Price to cfo (PTC): 47.55

RE to be added: 27049301

Total share post RE: 99180771

Price to cfo post RE: 34.58

CMP: 412, PTC 47.55

With PTC 34.58 price will be 300

However such exact calculation won’t work exactly. Just mean to say there is possibility of price adjustment, hence can’t take CMP as fix price.

Lukewarm response hence more RE will get converted in acutal share, right?

How over subscription helps, please through some light. Thanks.

I think, even after the introduction of RE, there are still people who will neither sell their REs nor apply in the rights issue. Hence the under-subscribed rights will have to be distributed among people who apply for higher number of shares than their entitlement. But this is never a given. For people who buy RE from markets with the intention of applying for rights, very less chance of not applying.

How can one check the subscription status of a rights issue?

Hi Tushar, you can track the status in following link :

Cheers

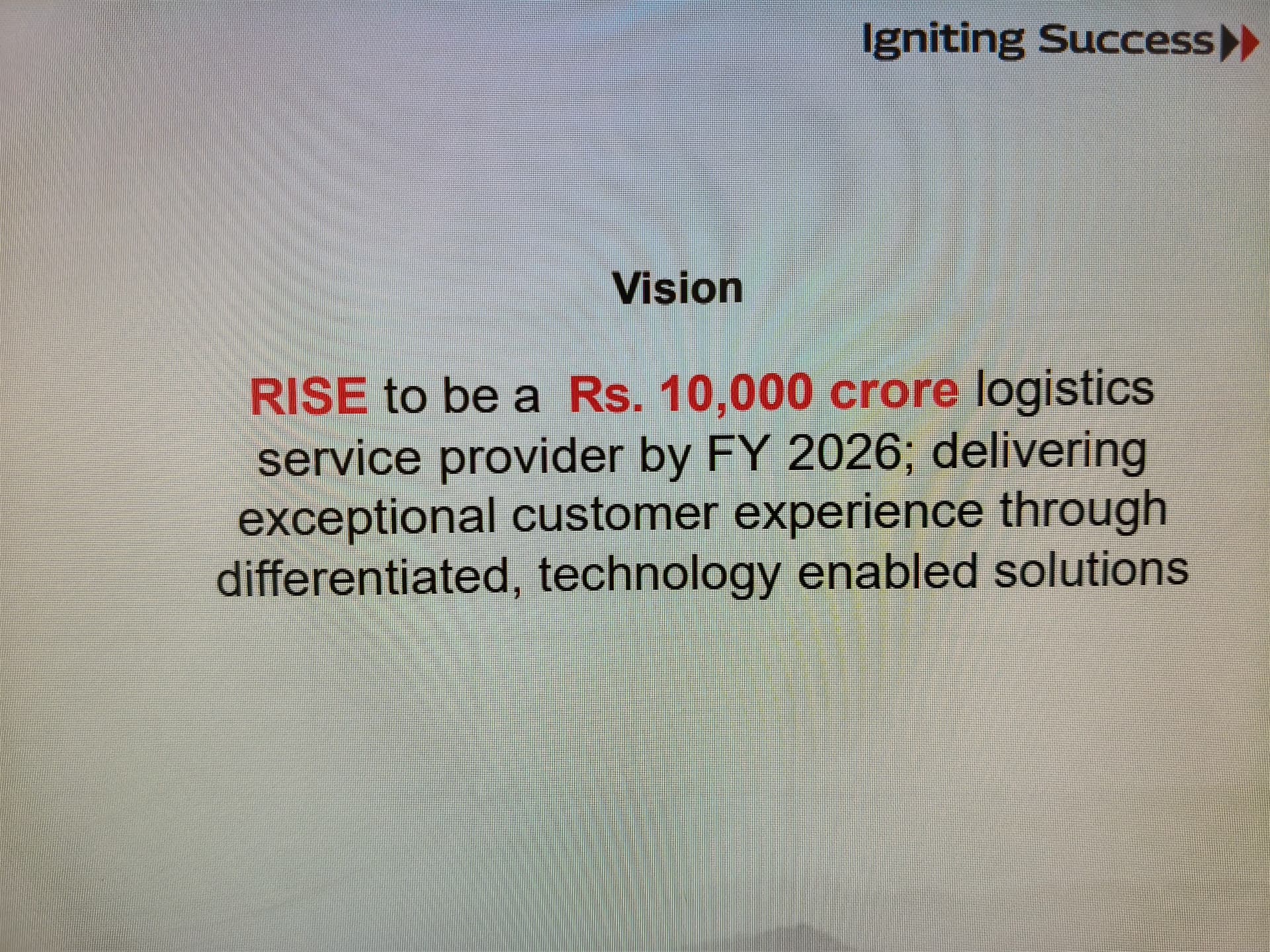

TWhat about this target..they are not even closure to that. This is their vision in Apr2024. They are mentioning this thing now.

Price ₹ 443 M.Cap ₹ 4,407 Cr PE 1749.0

| YOY | Mar 2026 | Dec 2025 | Mar 2025 | |

|---|---|---|---|---|

| Sales | ⇡ 14% | 1,791 | 1,898 | 1,570 |

| EBIDT | ⇡ 45% | 112 | 103 | 77.7 |

| Net profit | ⇡ 399% | 22.4 | 6.01 | -5.29 |

| EPS | ⇡ 399% | ₹ 2.03 | ₹ 0.33 | ₹ -0.68 |