Hi All,

Here is a newly listed company from a great corporate house. They are into the logistics space.

Mahindra Logistics Limited is one of India’s largest Third Party Logistics (3PL) solutions provider in the Indian logistics industry which was estimated at 6,40,000 crores in Fiscal 2017, according to a report titled “Report of supply chain and 3PL potential in India, freight forwarding and corporate people transportation services” dated 31 July 2017, prepared by CRISIL Research. The competitive advantage is their “asset-light” business model pursuant to which assets necessary for operations such as vehicles and warehouses are owned or provided by a large network of business partners. Their technology enabled, “asset-light” business model allows for scalability of services as well as the flexibility to develop and offer customized logistics solutions across a diverse set of industries. They operate in two distinct business segments, Supply Chain Management (“SCM”) and People Transport Solutions (“PTS”).

SCM

They offer customized and end-to-end logistics solutions and services including transportation and distribution, warehousing, in-factory logistics and value-added services to clients. They operate through a pan-India network comprising 25 city offices and over 350 client and operating locations. Mahindra Logistics have a large network of over 1,000 business partners providing vehicles, warehouses and other assets and services. They manage over 13.0 million square feet of warehousing space spread across our pan-India network of multi-user warehouses, built-to-suit warehouses, stockyards, network hubs and cross-docks and operate in-factory stores and line-feed at over 35 manufacturing locations. The “asset-light” business model along with solutions design capabilities enables to serve over 200 domestic and multinational companies operating in several industry verticals in India, including automotive, engineering, consumer goods, pharmaceuticals, e-commerce and bulk. They have sourced or developed customized technology systems to provide innovative and cost-efficient solutions to improve transparency and visibility for their clients.

PTS

Mahindra Logistics provides technology-enabled people transportation solutions and services across India to over 100 domestic and multinational companies operating in the information technology (“IT”), information technology-enabled services (“ITeS”), business process outsourcing, financial services, consulting and manufacturing industries. Services are through a fleet of vehicles provided by a large network of over 500 business partners.

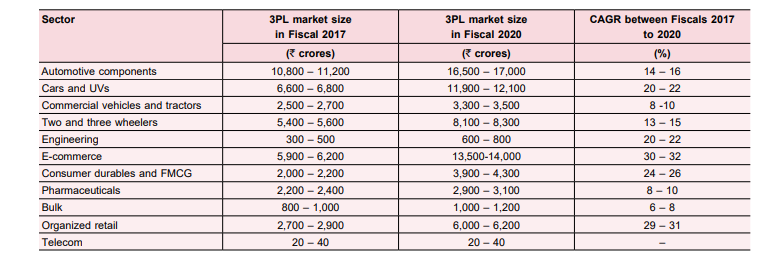

As per CRISIL, Logistics as a percentage of GDP is 13-14%. The Indian logistics industry comprising segments such as road freight, rail freight, coastal freight, warehousing, cold chain and container freight stations and inland container depots (“CFS/ICD”) is estimated at

6,40,000 crores in Fiscal 2017. This is expected to grow at a CAGR of approximately 13.0% to 9,20,000 crores by Fiscal 2020.

Further the report has estimated the 3PL market in India at 32,500-33,500 crores in Fiscal 2017, which is expected to grow at a CAGR of 19-21% to reach ` 57,000-58,000 crores

by Fiscal 2020. It is to be noted that Mahindra Logistics does ~4,000cr in revenues so they are a significant player in the 3PL market.

2 Noteworthy subsidiaries of theirs:

Lords Freight (India) Private Limited,provides international freight forwarding services for exports and imports, customs brokerage operations, project cargo services and charters.

2X2 Logistics Private Limited, provides logistics and transportation services to OEMs to carry finished automobiles from the manufacturing locations to stockyards or directly to the distributors through specially designed vehicles.

Now one of the highlights is of course that the majority of the company’s revenue comes from the Mahindra group itself. In 16-17 it was ~54% and in 17-18 ~54.5%. And the bulk of the revenues come from the automotive sector in 16-17 it was ~61% & in 17-18 it was ~62%.

It is not a bad thing that bulk of the revenues come from the automotive industry. There is always an opportunity in the auto space whether it is ICE, EV, Bikes, Cars etc:. The company however is looking to diversify its sector dependence.

Their asset-light model provides them with lots of flexibility in the case of a lull in a certain industry/scaling down/scaling up operations. Due the asset-light nature the impact on the company should such a scenario occur can be decreased in my view.

The business however does operate on slim margins.

Mahindra logistics comes across as more of a logistics technology company. An aggregator on the supply side and a tech company on the operations side.

They intend to continue to develop technology systems to increase transparency, improve operating efficiencies, and strengthen the competitive position. IGoing forward, the plan is to focus on the areas set out below:

• Enhancements to transportation management systems

including last mile route and load optimization capabilities

• Digitization of internal processes (e.g. implementation

of an advanced human resources management system,

accounts receivable/payable management systems)

• Implementation of advanced warehouse management

systems (e.g. Oracle Log Fire) at our warehouses

• Implementation of “internet of things (IoT)” projects in

certain operations

• Work with startups to develop a cloud based platform for

handling end to end transport desk outsourcing operations

for the PTS business

• Analytics to improve operating efficiencies

They may develop these technologies themselves or outsource development to third party vendors. They are actively assessing opportunities to work with logistics technology start-ups, either by incubating them, or partnering with them. They will consider acquiring technologies to help achieve their digitization objectives.

Here are a few articles:

Mahindra Logistics picks up stake in transport management startup ShipX

Kedaara Capital-backed third-party logistics (3PL) solution provider Mahindra Logistics Ltd has invested Rs 7 crore (about $1

Mahindra Logistics awaits nod to use drones in warehouses

Move to improve accuracy of stock, lower labour cost

Coming to the valuations there are a few questions I would like consider:

- Is the business growing fast? can we get 20% cagr for sometime (3-5 years)?

- Can the business sustain its high ROCE for a long time (5 years plus) ?

- Is the business in an innovator and a leader in its sector?

- Can the business scale?

- What is the reason for clients to choose them?/ competitive advantage?

- Valuations?

A1) By the looks of things the business is growing fast and should be able to continue doing so for the next few years.

A2) It seems like the business can maintain a high ROCE going forward. They have decent working capital and debtor days as per screener data.

A3) It definately does look like it. They seem to be focussed on innovation and applying technology. Further they do have a certain know-how and scale to lead the sector.

A4) Yes. They can scale faster than a traditional logistics player can. They can also do so more cost effectively.

A5) The space and the business is not at all an easy business to operate. Let alone doing so cost effectively, all while operating on a slim margin. Doing it at scale is not something that just anybody can do. Further being asset light and aggregating hundreds of suppliers is a challenge for a new entrant. Many providers will be rather comfortable working with the Mahindra group as opposed to another 3PL player or even approaching a client directly as they may only fullfill a small portion of the clients logistics requirements. Such clients will also prefer to deal with a single experienced vendor for an end-end service. This leads to some stickiness as well. Further Mahindra Logistics offers customised solutions which could be a mix of various forms of logistics services/supply chain solutions that may involve multiple partners and co-ordinating the same. It is much easier for a corporation to outsource end-to-end work to one reputed company. It saves them operational costs and inefficiencies as well.

A6) Two ways to look at it

- The business can grow fast and scale quickly. The industry is growing fast as well. You are getting a leader in a fast growing industry with the potential to scale & a high quality corporate house backing it. The company generates a high ROCE as well. The 40x multiple seems expensive but the growth is there.

- You are getting a high quality Mahindra group company that is growing at 3500cr market cap.

I would love to have the views of our members on the same.

Financial data can be found here: Mahindra Logistics Ltd share price | About Mahindra Logis. | Key Insights - Screener

Sources: Screener & Company AR.

Disclosure: Thinking about taking a small tracking position.