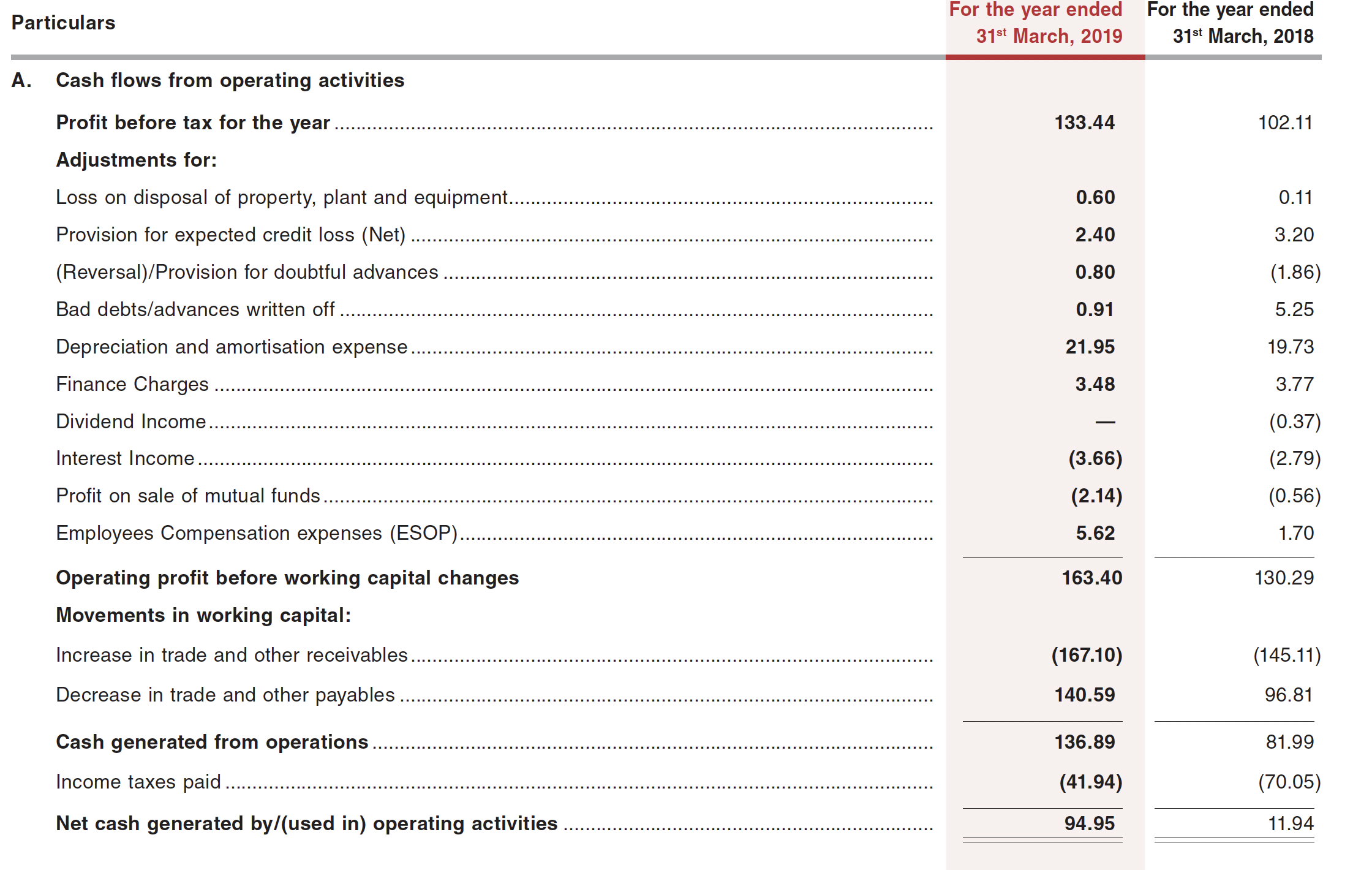

CFO only matches PAT in FY19, in all other years CFO has been negative or lower compared to reported PAT

This generally means money is getting stuck in working capital and the earnings are overstated. On closer inspection, I realized that cumulative accrual taxes from FY15-19 ~ 146 cr. whereas the company paid cash taxes ~ 218 cr. (~71 cr. extra tax paid). I did not find any tax asset of this amount in the annual reports. Does anyone know why company is paying extra taxes?

If we add the extra taxes back to CFO (52 + 71 ~ 123 cr.), this is still lower than cumulative profits of 270 cr. Cash flow statements from annual reports of FY18 and FY19 say that the main difference in CFO and PAT comes because of increase in working capital (receivables increased more than payables).

This is understandable as its a very low margin business and small changes in receivables will have a bigger impact on CFO. But why is the company paying higher cash taxes? Any feedback will be very useful. @1.5cr

ICICI Direct resonates with my personal view on this sector.

With introduction of newer norms (social distancing) and regulations shoved into the sector, it is becoming challenging to maintain turnaround times for customer for various companies, with increased labour costs. A 3PL company in such an environment can provide reduced logistics costs, better turnaround and also reverse logistics to each client company due to greater efficiency, lower capex and running the operations at better utilisation levels compared to each company internal logistics operations. MLL ended with ~400 clients in FY20 and expects 30-40 client additions each year.

If you compare MLL and TCI Express business model, TCI Express looks more promising. Did you do any comparison of MLL and TCI Express as investment case? Please share your view

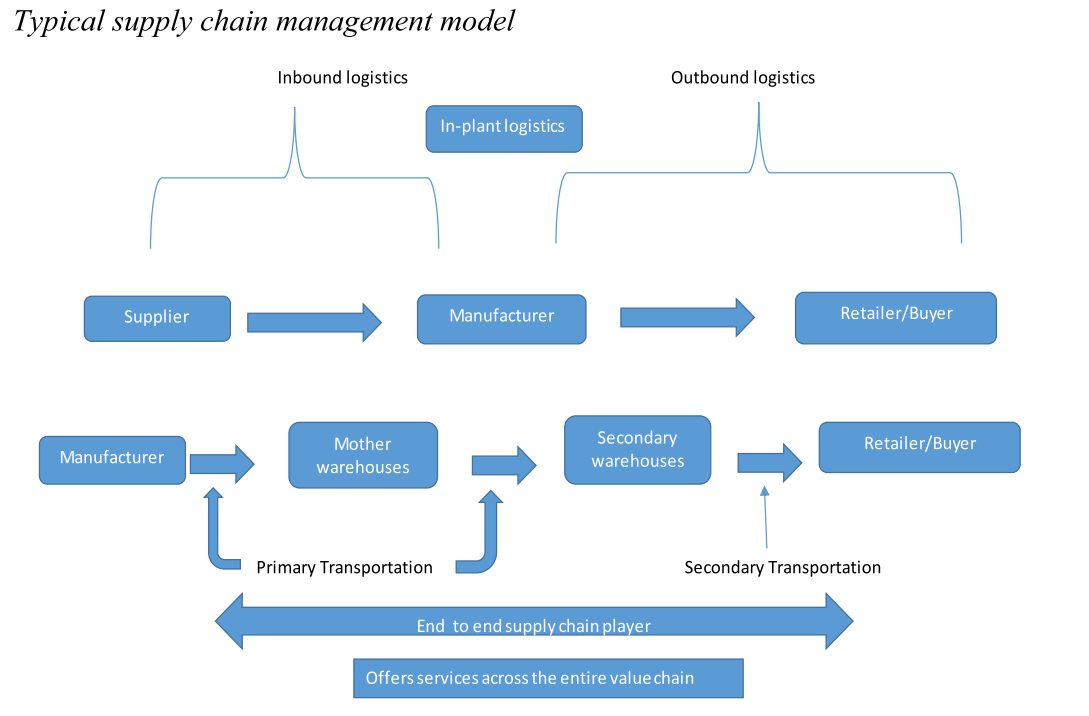

Difference between the domains of a 3PL logistics and Express Logistics is somewhat blurry to me. Following is my understanding. Feel free to correct me.

So, the functioning of a 3PL player stops after delivering finished goods to the retailers, distributors or wholesellers.

Express Logistics’ Domain

Scenario 1: Croma Retail needs to supply refrigerators to Mumbai warehouse from its Bangalore warehouse (where the 3PL logistics partner of Whirlpool supplied the goods). [B2B]

Scenario 2: If you place an order for a good from a non-Amazon seller, they first had to sent that item quickly to Amazon warehouse for checkup & packaging. Express logistics takes care of this transportation. [B2B]

Scenario 3: The e-Commerce site then sends the item to customers at express speed, or arrange a reverse pickup for item return or replacement. [B2C]

Scenario 4: An individual sends an item to another individual. [C2C]

For TCI Express contribution of Scenario 3 is around 5% and Scenario 4 is negligible.

Edit: I feel that Express Logistics players may also carry out outbound logistics in case no 3PL player is involved with the Manufacturer.

While this will definitely challenge those who are already in the business and are asset-heavy (having their own transport and all that), on the reverse side, MLL will attract new competitors as MLL have showed them a way on how to get into logistics with significantly less startup costs.

If that happens how will MLL handle those new entrants ? If I am right, some has already started to follow their footsteps…

Very true! M&M Group as the anchor client,Tech Mahindra as the technology partner and the reputation of the group gives Mahindra Logistics a right to win.

I think it means, Anchor Client for Mahindra Logistics is M&M itself being a large conglomerate, by providing transportation for vehicles manufactured by M&M itself and commutation for its employees, for ex.

And yes, Tech Mahindra may be giving Tech and M&M Finance doing it’s bit. But, at the end of the day they can thrive in this difficult sector, which hasn’t had any impressive performer in decades, if they are able to generate the efficiencies, and the industry indeed has that kind of juice.

I think you are talking about logistics in general as 3PL is a sunrise sector.

Logistics sector in general has seen the boom only after the emergence of eCommerce and GST implementation, which also brought with it cutthroat competition fueled by PE money.

Regardless, Bluedart had been a darling of investors from 2003 to 2015 during which its mcap went up 136x with CAGR of 48%! And during the last 20 years it went up 20x with a decent CAGR of 16%.

You see it as a sunrise sector, is it because of GST implementation and emergence of eCommerce? That would make sense.

An 18% CAGR growth is expected in this sunrise sector. What different does 3PL do that FTL or LTL wasn’t doing all these years. I know a few transporters, they have warehousing ability and trucks, either by owning them or renting them out making them asset light models, they have been around for decades now. How different is 3PL?

The research report quotes:

“We see two key growth drivers: (i) a mindset shift among large clients to outsource

logistics to 3PL players and focus on core business; and …”

They site this as the main reason for growth in 3PL. The same thing FTL and LTL service providers can do? Is the question in my mind. This sounds silly, right off the bat, because I do not see what essential service 3PL might be providing.

I feel as our country’s GDP picks-up transportation will have an important role. I am just not sure where I should invest. VRL is an efficient business, but old school. So is TCI.

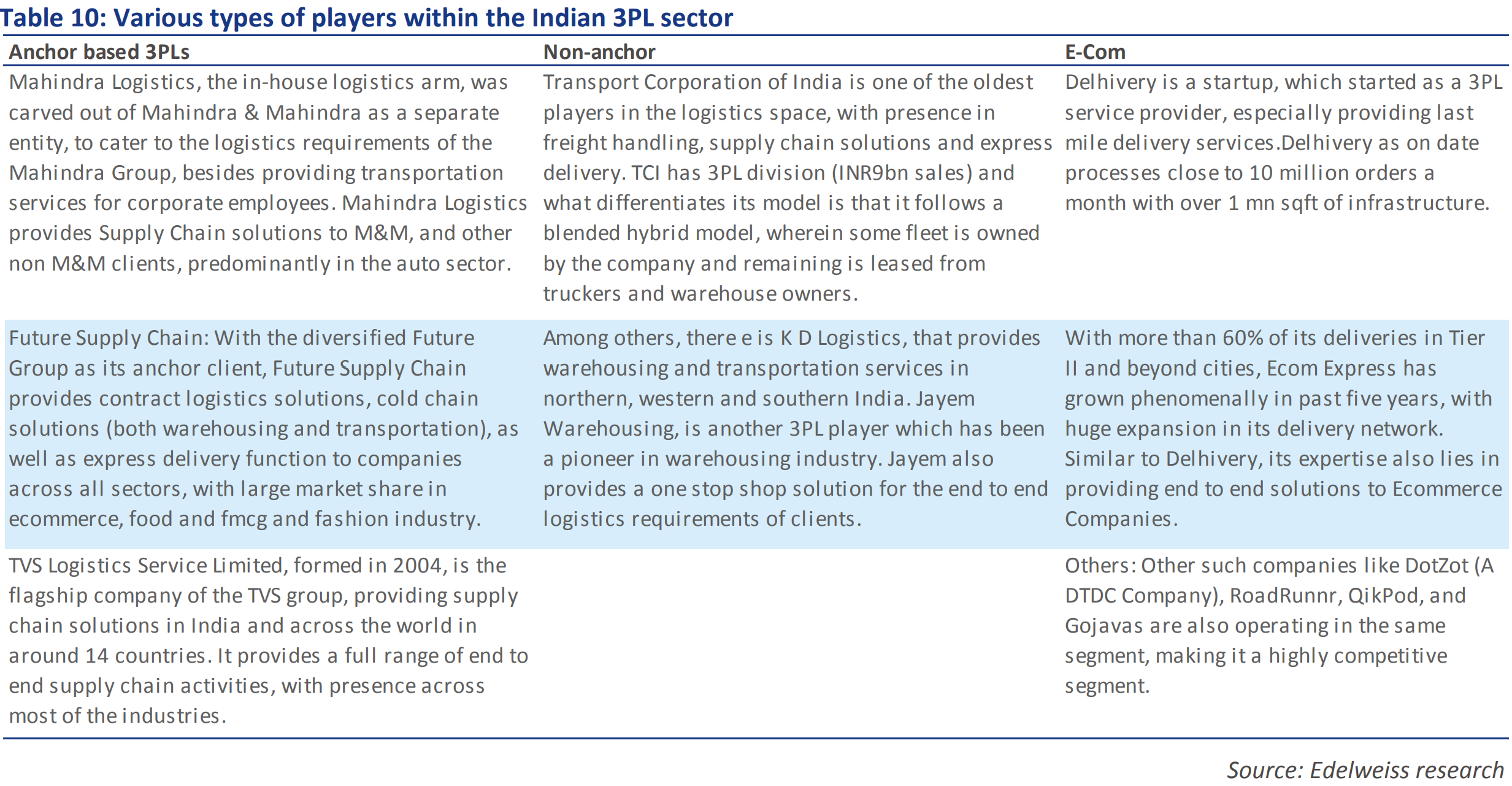

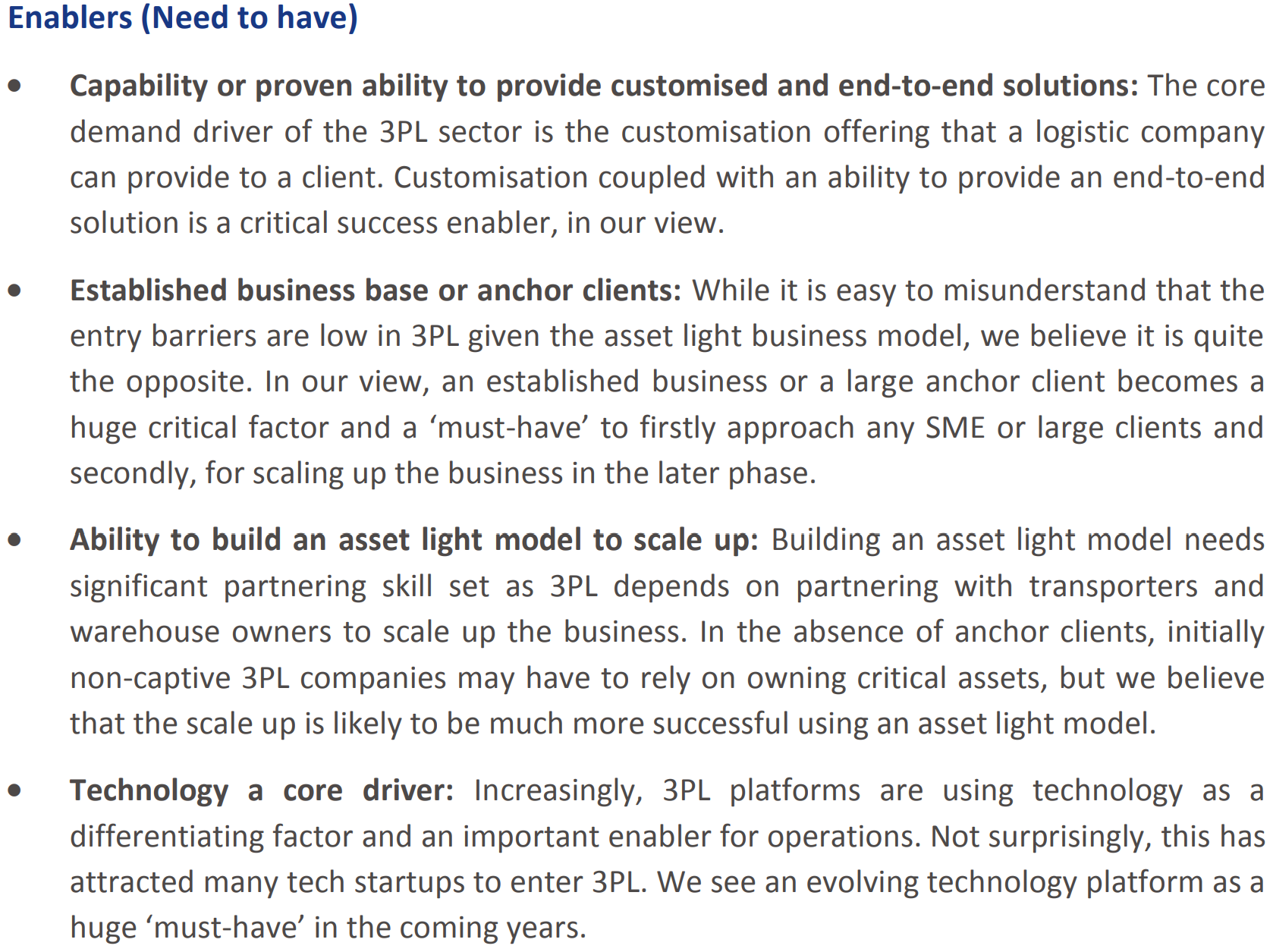

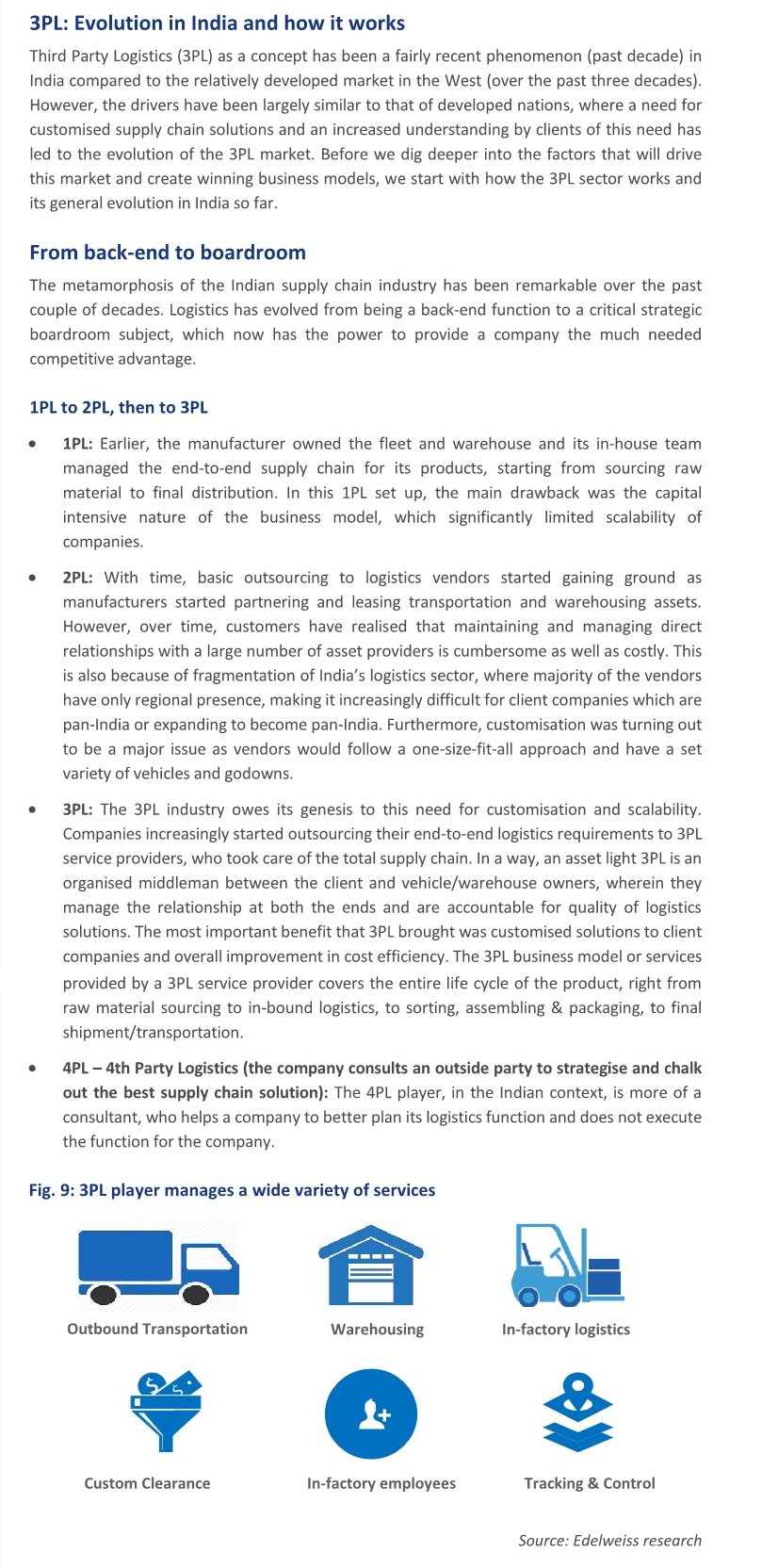

No GST implementation has only added fuel to logistics in general. And eCommerce has added another distribution channel for various products. And eCommerce has become another big industry in itself. But none of that led to the emergence of 3PL. 3PL emerged from the need for more coherent logistics operations and the need to outsource more non-core operations. FTL and LTL service providers does only part of the job and 3PL offers more integrated operations. Following screen-grab from the Edelweiss report (page 19-20) drives home this point better.

I am wondering if someone has looked at cash flow statements of Mahindra and why they have paid taxes in excess of what they have provided for. Even accounting for that, their money is getting stuck in working capital. I can understand this as its a new business, any further insights will be very valuable.

@ashwinidamani have you tracked this company and look at their cash flow statements?

I did some work on this last year. My assessment of this B2B business is that it is a low margin business (esp transportation) and while there may be some shift to higher margin warehousing business, the number of players in the space and low business activity will put pressure. Its a business where pricing power is less but once you get a large customer, stickiness is high. Even in Q2FY20, there was stretch in receivables due to weak economy and tight liqidity. Company gave an update few days back that there may be further stretch in receivables which is not surprising given the impact that auto industry saw prior to Covid and post Covid.

PTS business is likely to be impacted in the current environment and probably in the post Covid-19 world. There are many small players operating but limited pan India organized players. PTS business is not a business which seems very exciting.

Mahlog considers TCI and TVS Logistics as its main competitors as they offer integrated solutions and are strong in auto sector. In the transportation side, there are many competitors.

One also needs to bear in mind if M&M would lose market share in auto segment in the BS-6 world and the impact that it may have on Mahlog. My understanding is that Mahlog gets more business from M&M’s non-tractor auto than it gets from M&M’s tractor business.

A positive that I see is that Mahlog has been able to get customers in other industries including consumer, pharma, ecommerce.

I think just the opposite. MLL is well-positioned to cope with challenges in the post-covid era but I doubt its small peers remain able to maintain their pre-covid market share.

Tacitly, this thread is comparing MLL with TCI Express.

TCI Express is a competetive business, with a strong parentage. It appears well poised for capturing market share. It is commissioning two more high tech centers (in Pune and Kolhapur, I think).

MLL is largely dependant on the work from MM, but there is no such dependency issue with TCIx.

So, yes, this thread would benefit if it compared the two entitites.

Why the EBIDTA margin of MLL is so low(4.13) compared to EBIDTA margin of TCI is 11.93(2019)?I think the gap also will widen further for 2020 as MLL impact will be substantial as parent M&M business to it will take a significant hit.

If you check their market-share, its pretty low. There are a lot of unorganized players in both express and logistics industry. So it is highly unlikely that one will hinder other’s growth.

Company is expecting significant impact of Covid-19 in its business.

Quoting below statement regarding revenues

“revenue in Q1FY21 could be lower by as much as 50% to 60% as compared to a normal quarter”

AS per my understanding the PTS business will be almost zero for this quarter and also in the SCM part auto revenue will be very less.only silver-lining will be essentails part.

Will the asset light model help them atleast not to report any losses in this quarter??