1 Like

Thanks @Dinesh_476 for sharing the details.

Can someone please help me understand as to why Indraprastha Gas is richly valued compare to Mahanagar gas - both are PSU and into similar business. Is there any fundamental reason (because of size, profitability, growth potential, ROCE, corporate governance etc) or just a perception.

4 Likes

Market is always forward looking. Where is the future of MGL? They are only in 3 GAs.

Compare the same with IGL. As of now, Delhi contribute 65% of volume. Noida, Greater Noida & Ghaziabad contribute 21%. Rewari 3%, Gurgaon 2%, Karnal 1%, Meerut Muzaffarnagar 1% are other areas for growth. Kanpur, Kaithal is just the beginning. So is Ajmer. Bareilly, Unnao and Jhansi in UP are additional GAs (through collaboration). Then they have 50% share in Maharashtra Natural Gas Ltd (MNGL) - Pune & nearby areas.

7 Likes

Mahanagar Gas - Story slowly unfolding.

Future Prospects -

-

Entered i MOU with BMC to set up to set up CBG plant in Mumbai with a capacity of 1000 tons per day.(Reducing carbon footprints - Which EV sector has not achieved)

-

Entered MoU with Baidyanath LNG for setting up LNG stations in Maharashtra and outside also.

-

MGL also launched a mobile application MGL-TEZ in partnership with the BEST, the

transport company in Mumbai to facilitate convenient refueling for CNG commercial vehicle. -

As far as our Raigad GA is concerned, they have connected 69,106 domestic households and 29

CNG stations are currently operating there. -

The Savroli station, which is having LNG dispensing facility also was recently commissioned.

And they have started filling LNG into the vehicles from the Savroli station. -

MSRTC currently, they are running about 120-plus CNG buses. And they are expected to roll out 450 more buses to be inducted in 8 MSRTC depots in MGL geographical areas by November or December of this year. So about 50, 60 or so will add on every month.

(So those 450 buses will definitely contribute to volume addition over the next 2 quarters) -

They have recently commissioned online CNG filling facility for the vendor Vithalwadi Depot.

And are in the process of setting up CNG infrastructure in 6 more of their depots which are at:

Panvel, Karjat, Pen, Roha, Alibaug, Uran. -

MGL has signed a Share Purchase Agreement to acquire 100 per cent stake of Unison Enviro Private Limited (UEPL).

This acquisition will enable MGL to expand to newer geographical areas in Maharashtra (Ratnagiri, Latur & Osmanabad) and Karnataka (Chitradurga & Davanagere) thereby providing new avenues for long term growth.

Disclosure - Not Invested

11 Likes

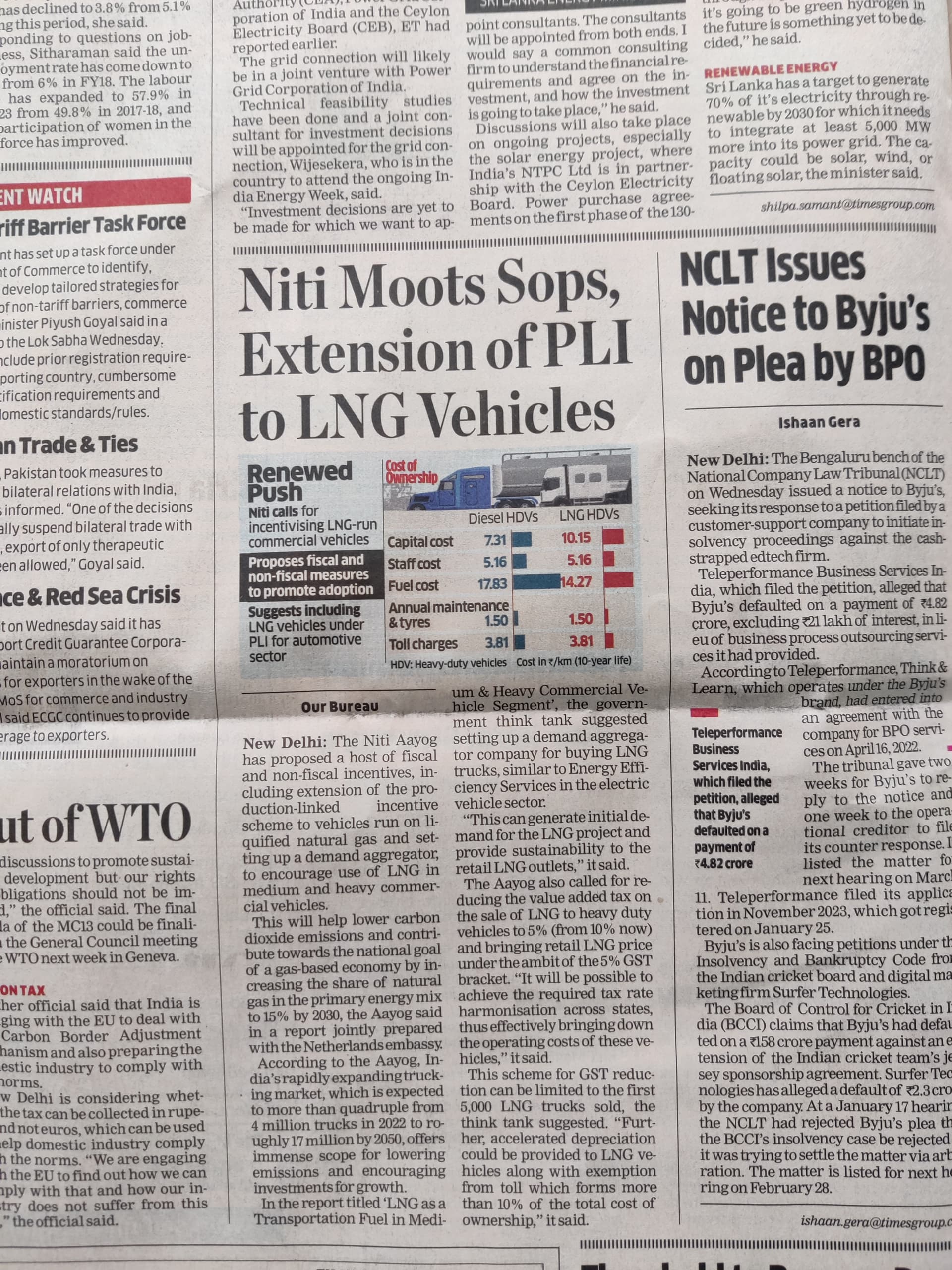

LNG trucks will be the next big thing as they can eliminate the need for refuelling for long haulage can go 1000 miles in one go, and popular abroad,although upfront cost is higher but, in reduced emissions and cost savings vis a vis diesel it is a winner , if the tie up of BLNG and green line picks up .

Disclosure: Invested and could be biased as working in Gas sector

5 Likes

@Vego Its really interesting to know that you work in Gas sector. Can you share your insights on being close to it, and your thesis behind your investment here. It will be much appreciated.

2 Likes

3 Likes

CNG vehicles would remain a preferred mode of transport in and around city area due to presence of CNG filling stations.

But for long haul trucks and buses , LNG would be preferred as LNG in liquid form can be stored in Cryogenic fuel tanks for long distance journey and no top up required up to 1000-1500 kms and even more .

But both CNG & LPG are non-renewable energy , though both are 8-16 times cleaner than petrol diesel vehicles in terms of carbon. Further , we have to meet our CNG/ LNG requirement partly through imports.

Therefore , CNG & LNG are approaching towards semi-final. and both would gradually & ultimately be replaced by renewable energy like CBG (compressed Bio gas) & LBG (Liquified Bio gas).

The beauty of the technology is such that the existing CNG network/ Infrastructure can handle CBG / LBG fuel dispensing and existing CNG/ LNG vehicles will be able to run with CBG & LBG fuel. After all all the four contain a simple molecule called Methane CH4 as source of energy.

The other alternatives would coexists together for quite some time - EV, Hybrids , Ethanol , Ethanol + petrol, Bio diesel , Hydrogen IC and Hydrogen fuel cell.

10 Likes

The Article does not mention about Li ion battery replacement cost, which could be one of the major cost factor even if recycling is adopted in a big way as replacing with a recycled battery will also cost money which would be of recurrent nature.

But the way in which EV adoption is taking place would over , hopefully some solution to high repair maintenance cost would be found out in the long run and the Govt subsidy will continue for quite some time.

EV will coexist for quite some some along with other renewable & non renewable form of energy.

2 Likes

Recent correction offers good buying opportunity:

3 Likes

For the cng stations currently dispensing CNG from MGL…is it possible that they stop their tie up with MGL and then tie up with the competitor? Is it out of the question or possible?

Just thinking that this might be the approach which few aggressive players (eg. adani) might adopt if they enter Maharashtra region.

Most of these CNG stations are owned by MGL. Also, they have exclusivity to 3 GAs (Mumbai, Thane, Raigad). So, no one else can sell in these GAs. I think exclusivity for Mumbai is about to expire, if not already expired. But they have already set up huge infrastructure so they have a big first-movers advantage. Also, these assets have been depreciated. New comer will have to set up all assets from scratch so there is depreciation impact. Also, there is impact of interest cost (as they will borrow). Another impact will be land cost. Mumbai land is very expensive.

All in all, it will be tough for someone else to setup CNG stations in Mumbai. Do not forget they have PNG business too.

However, business has limitations. Remember only 3 GAs. 4th one if you consider acquisition from Ashoka buildcon.

1 Like

I read in an above thread that only 30% stations are controlled by MGL …

so the query is in regards to threat of remaining 70%…

2 Likes

Mahanagar Gas Q1 FY25 Analysis: Key takeaways!!

Mahanagar Gas Limited (MGL) demonstrated robust performance in Q1 FY2025, with overall gas sales volume increasing by 13.1% year-over-year to 3.858 mmscmd. The company’s core CNG segment led growth, rising 11.7% YoY to 2.772 mmscmd. Domestic PNG and industrial/commercial segments also saw healthy increases of 10.4% and 23.8% respectively. This strong volume growth translated to improved financial performance, with EBITDA rising to Rs. 418 crores and net profit increasing 7.4% quarter-on-quarter to Rs. 285 crores.

Strategic Initiatives:

-

Accelerated CNG station expansion: MGL is targeting to add over 50 CNG stations in FY2025, more than doubling its historical annual additions. This aggressive expansion aims to capitalize on rising CNG vehicle adoption.

-

Diversification of gas sourcing: The company has signed multiple term contracts for gas supply, including Henry Hub-linked deals, to manage costs as APM gas allocation declines.

-

Entry into LNG retail: MGL has entered a joint venture to expand its LNG station network, complementing its existing CNG infrastructure.

-

Focus on Unison Enviro subsidiary: Management expects Unison to deliver 15%+ annual volume growth over the next few years as infrastructure expands in its newer geographical areas.

Trends and Themes:

- Accelerating CNG vehicle adoption, especially in commercial segments

- Shift towards larger CNG vehicles (medium & heavy commercial) from smaller ones

- Growing interest in CNG two-wheelers with recent launches by major OEMs

- Gradual reduction in APM gas allocation, necessitating diversification of gas sourcing

Industry Tailwinds:

- Government push for natural gas adoption in transportation sector

- Favorable economics of CNG vs. petrol/diesel, driving conversions

- Expansion of CNG infrastructure improving convenience for users

- Introduction of factory-fitted CNG models by major automakers

Industry Headwinds:

- Declining APM gas allocation, potentially pressuring margins

- Rising competition from electric vehicles, especially in public transportation

- Volatility in global LNG prices impacting sourcing costs

- Potential regulatory changes around marketing exclusivity in CGD areas

Analyst Concerns and Management Response:

-

Concern: Sustainability of high volume growth

Response: Management maintains 6-7% long-term volume growth guidance, viewing recent quarters as above-trend -

Concern: Margin pressure from lower APM allocation

Response: Diversifying gas sourcing through term contracts and optimizing gas cost through blending -

Concern: Competition from EVs in bus segment

Response: Highlighting lower total cost of ownership for CNG buses; noting supply constraints in EV buses

Competitive Landscape:

MGL enjoys a strong position in its core Mumbai market. However, the potential opening up of marketing exclusivity could introduce competition. The company is working to strengthen its position through aggressive infrastructure expansion and customer-focused initiatives.

Guidance and Outlook:

- Maintaining 6-7% annual volume growth guidance for core MGL business

- Expecting 15%+ annual growth for Unison Enviro subsidiary

- Targeting EBITDA of Rs. 10-12 per SCM

Capital Allocation Strategy:

MGL is focusing on infrastructure expansion, particularly CNG stations. The company incurred Rs. 250 crores of CAPEX in Q1 FY2025 and plans to maintain an aggressive expansion pace.

Opportunities & Risks:

Opportunities:

- Expansion into new geographical areas through Unison Enviro

- Potential in CNG two-wheeler segment

- Growing adoption of CNG in medium and heavy commercial vehicles

Risks:

- Further reduction in APM gas allocation

- Increased competition if marketing exclusivity is removed

- Faster-than-expected EV adoption, especially in public transport

Regulatory Environment:

The regulatory landscape remains uncertain, with ongoing deliberations on marketing exclusivity and infrastructure exclusivity. MGL has sought extensions for infrastructure exclusivity and is awaiting regulatory decisions.

Customer Sentiment:

Customer sentiment towards CNG remains positive, driven by cost advantages and expanding infrastructure. The introduction of CNG two-wheelers could further improve sentiment among personal vehicle users.

Top 3 Takeaways:

- Strong volume growth of 13.1% YoY, led by CNG segment, driving financial performance

- Aggressive CNG station expansion plans to capitalize on rising adoption

- Focus on gas sourcing diversification to manage costs amid declining APM allocation

6 Likes

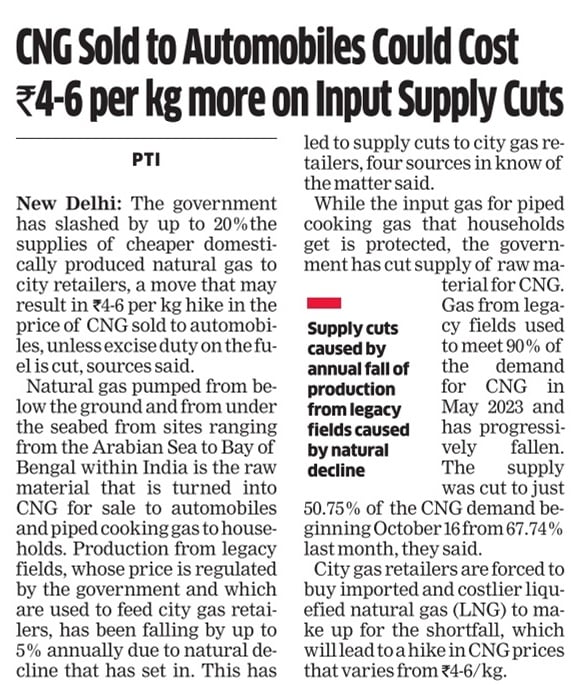

MGL_Allocation_Reduction.pdf (440.4 KB)

Allocation to the Company for CNG (Transport) has been reduced by ~20%, effective October 16, 2024,

compared to previous average quarterly APM allocation. This being major reduction in allocation, will have

an adverse impact on the profitability of the Company.

What possible outcomes shall be expected?

In my view,

- MGL has to manage sourcing the natural gas through different medium and pass on the cost to consumers. will the demand be the same if the price is hiked.

- MGL has to manage sourcing the natural gas & absorb the cost impacts, which leads to reduction margin eventually.

but does this change the demand for PNG & CNG over the long run?

4 Likes

As per the article, the CNG consumers are impacted by the supply cut. It’s not going to impact the house pipe connections.

Increase in price for CNG may impact the demand for CNG consumption in the short run, I guess. but still I feel it is good to accumulate for a long-term investment.

2 Likes

There are might be few private companies which might benefit by this cut in domestic CNG distribution by the revised policy.

Investors should probably look for those companies which might be importing CNG and Selling in India at higher cost / spot prices. Those companies might benefit by this policy change.

If some one can research on this area further, we might able to find some winners outside Mahanagar Gas and other CGD companies.

This is just a thought. I am not sure about this.

Disc: No Investment in MGL as of now. Edited the post to remove the reference to any company to avoid confusion.

5 Likes

Mahanagar gas is the subsidiary of GAIL, GAIL is valuation is comparatively higher than its long-term average over 5 years.

I see Mahanagar gas is fairly priced in my view. let’s see.

2 Likes