Some amazing results by the company, sales up 63 percent YOY, 7 percent QOQ.

PAT up 207 % YOY, 5.5% QOQ.

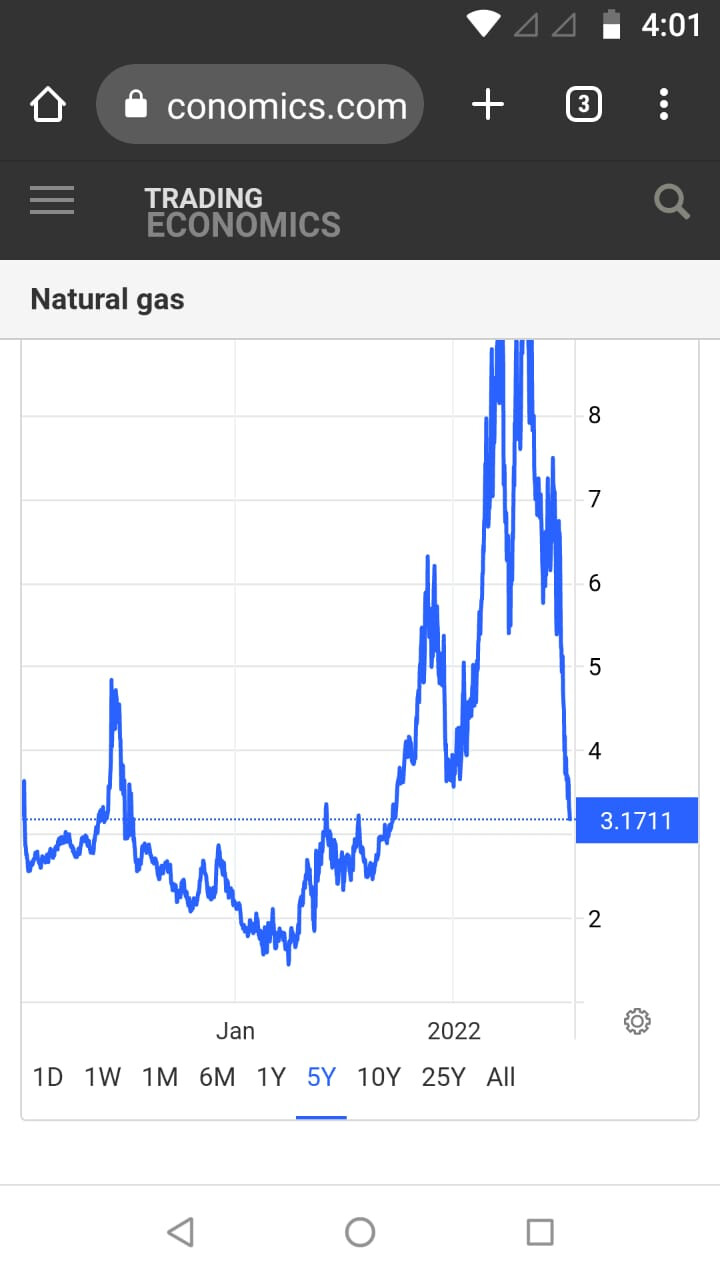

With natural gas prices deflating a lot and coming back to pre covid level. Benefits would be there from 2 quarters from now. Margins should expand in a couple of quarters from now.

Topline is up maybe due to cng prices being in the 80ies compared to 30 to 40 range .

CGD companies should get better margins this quarter, Cabinet approves Kirit Parikh reco

Natural gas now $ 2.05 but Mahanagar Gas still sells CNG at Rs 87 per kg. What’s happening?

What is your exact question can you tell me?

If global gas prices reduce CNG should be sold cheaper as well. That’s not happening. Who’s keeping the wide spread? When will CNG prices be reduced/normalised?

Probably it is happening not just with Gas prices, but fossil fuel prices as well.

I am not sure about Tax structure, but it seems that, prices will be kept at higher levels.

Now after OPEC production cut, the prices of fuel which are already high may go even further up.

In Maharashtra, electricity price per unit has been hiked by 5% to 25% across all slabs. It seems that, Inflation will remain stubborn for few more quarters.

I am not holding Mahanagar Gas but it was on my watchlist, but was unable to build conviction.

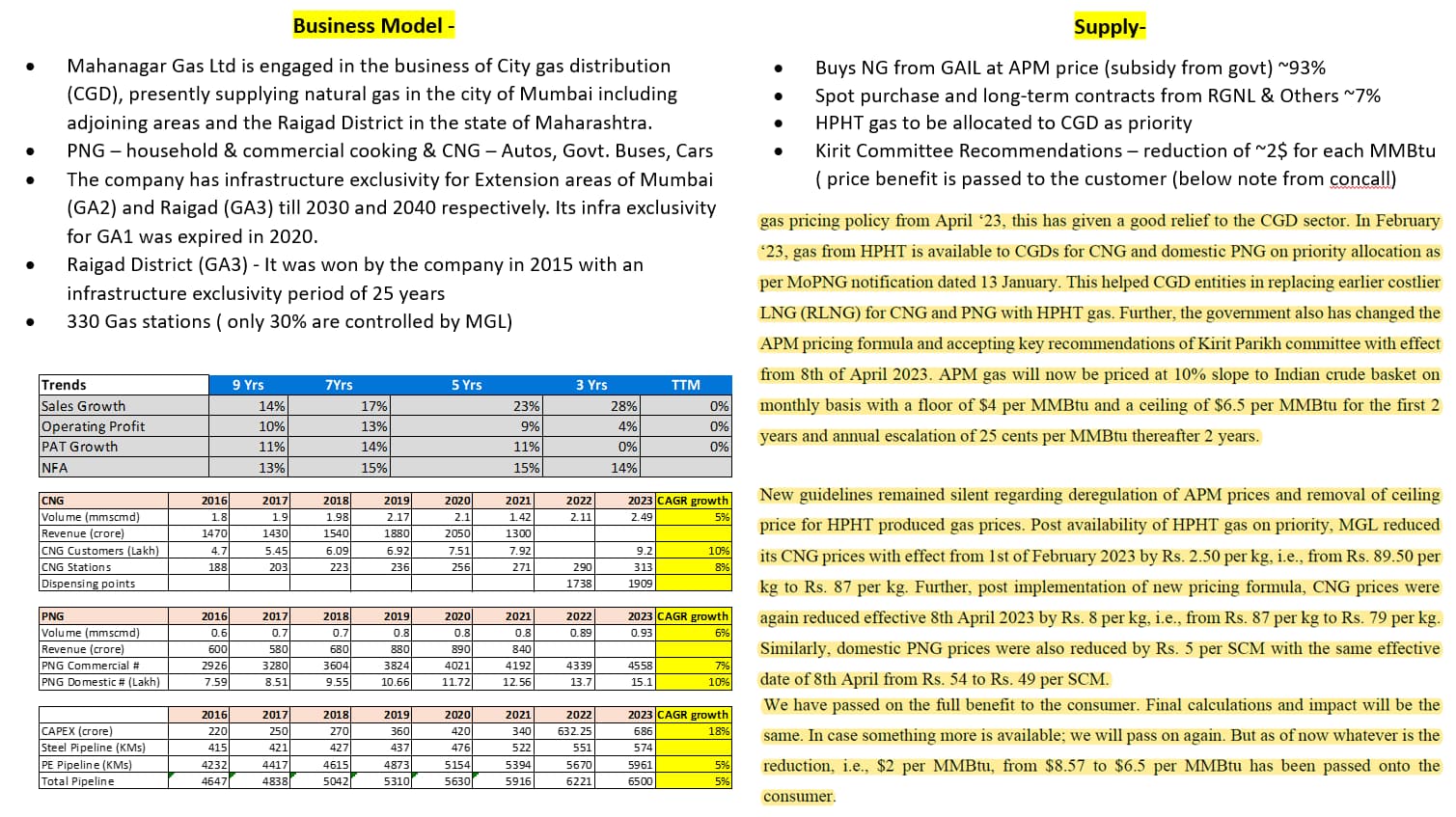

Cabinet approves revised domestic gas pricing mechanism recommended by Kirit parikh committe. This will help is improving margins for CGD companies like MGL, IGL, GUJGAS and also reduces cost for end customers(volumes will also increase). All the recommendation by KP committee seems to be accepted except annual hike of 0.5 USD per MMBTU comes only after 2 years( have to go through in detail to understand more)

https://pib.gov.in/PressReleseDetail.aspx?PRID=1914449

Dicl; invested in MGL and IGL.

@spartan - thanks. I have read several articles on this and all of them say it’s good for ONGC, Oil India and also for CGD companies.

However I don’t understand how can something be good for everyone? Who exactly pays for this? government?

It says CGD companies benefits from low cost but again these costs are to be passed on to consumers as CNG and PNG prices may also have to fall. So how exactly does it benefit to CGD

And on other hand , there is a cap on prices for gas production from ONGC and Oil India (no doubt there is floor as well)… But cap is negative right?

Just trying to understand in case anyone knows it in more depth.

Disclosure: Not invested

Now MGL procures Gas from ONGC/Oil/RIL at a far lesser price, due to Cap. The Balance is procured from International Spot trades, which presently is at its lowest levels. The average will be lower, now instead of 6 months revision in basket price this will be revised every month.

These low gas costs will be passed on to consumers, with lesser time lag , dynamic pricing will help CGD companies to improve gas volumes, and better manage cash flow.

Just my line of thinking.

my understanding is Kirit committee’s recommendation is good for everyone as there is floor and ceiling defined and by 2027 it needs to move to open market pricing. However, at current moment, its not good for ONGC / OIL as they will get lower price for their gas from nominated fields (price for which is set under APM). For e.g. currently they were getting $8.57 per mmBtu. As per revised formulae of 10% of crude price, they should be getting $7.92 per mmBtu. But there is a ceiling of $6.5 per mmBtu. So, these companies will get $6.5 instead of $8.57 from 8th Apr.

my understanding is, companies will not pass on the entire benefit to customers. Last year when the cost escalated, they didn’t pass the entire increase, thereby taking hit on the profit. Similarly, when the price fall, they will reinstate their margins.

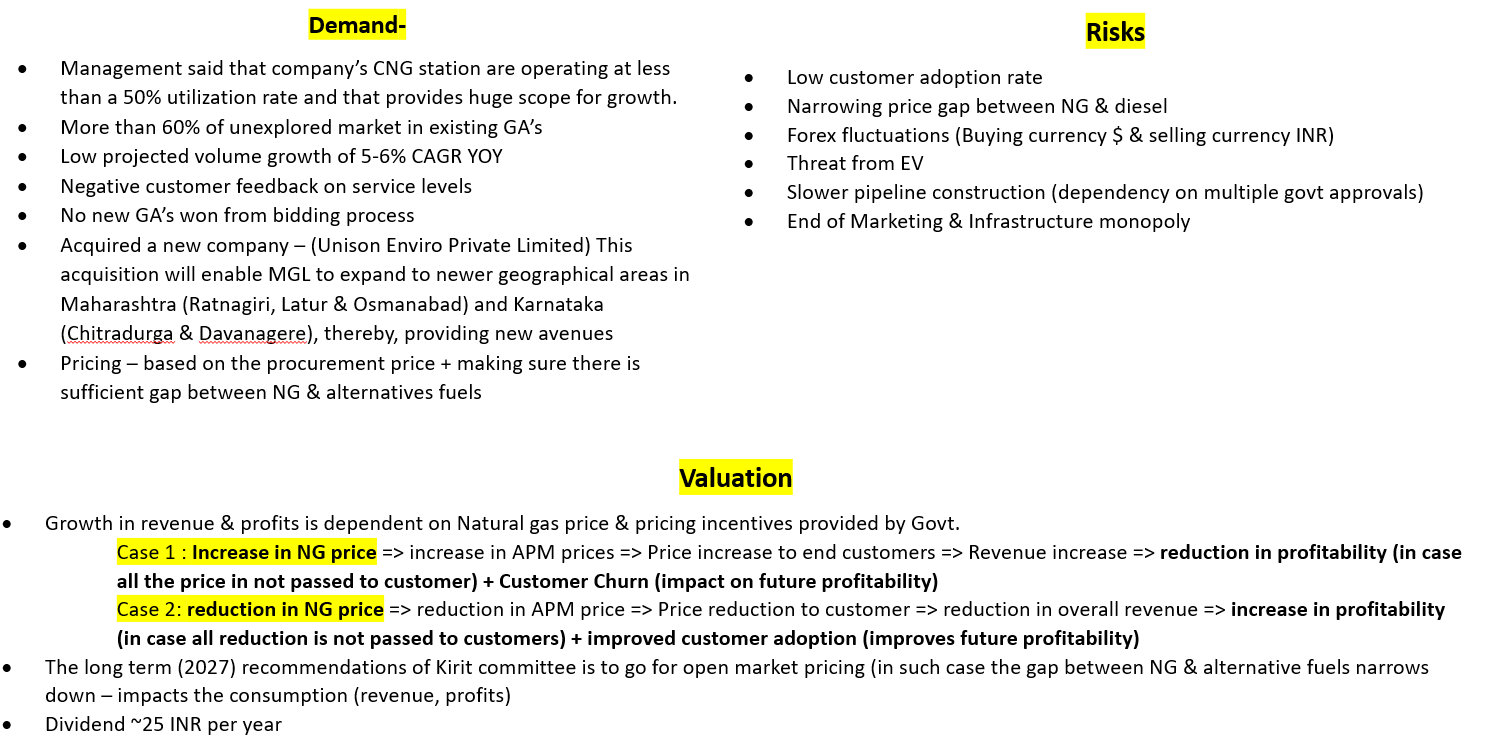

There is second angel to it. natural gas is in demand because of cost saving vs petrol (for CNG) and LPG (for PNG). Earlier difference between CNG & Petrol was 45-50% hence there was a demand for CNG powered cars. That difference reduced to ~20%. Now that difference will again increase to 45-50% which is good enough to keep CNG in demand. So companies will not be required to pass on additional saving on cost to customers, thereby helping improve margin.

This is a big issue. If I were to write on it, it will be an essay of more than 5000 words. In a nutshell, this natural gas (under Administered Price Mechanism) is only for priority / needy sector and hence price control. Although we have come a long way in last 8 yrs how the prices are controlled.

Open market cost is higher than APM cost. So, average will be higher. Please see costing for GGL.

You may want to study business model of MGL / IGL vs GGL. Former derive ~80-90% gas under APM vs later which derive ~25%.

In addition to points mentioned by @santoshj KP committee has kept a floor price of US$ 4MMBTU which will protect the downside for upstream companies like ONGC,OIL and Reliance. When gas prices were crashed during covid lockdown period these companies were unable to cover their cost of production which is around US$3 -3.5/MMBTU. Now with floor price fixed at 4mmbtu,these companies will have certainity that they will not faces loss in case gas prices were to crash again.

This price regulation applies for APM gas produced from old legacy fields only.

Gas produced from offshore, HTHP fields will continue to enjoy the premium price(?20% premium).

These factors will help exploration companies to invest and produce more gas domestically. Currently around 50% of consumed gas in India is imported. Govt wants to increase the contribution of gas in total energy consumption to 15% from current level of 6% for which country needs to produce more gas and incentivize the upstream companies.

Going by some of the research reports with the current recommendations the gas sourcing cost for IGL and MGL likely to reduce by Rs.6/scm which helps to improve margins. IGL and MGL margins were down to 15-17% during last few quarters when APM prices went more than US$8/MMBTU.

( I am unable to find complete report of KP committee. If anyone comes across kindly share. Reading the complete report will be helpfull)

| Q4FY23 | Q4FY22 | Q3FY23 | YOY | QOQ | |

|---|---|---|---|---|---|

| OP REVENUE | 1610 | 1086 | 1671 | 48 | -4 |

| EBITDA from op | 389 | 215 | 256 | 81 | 52 |

| % | 24 | 20 | 15 | 22 | 58 |

| NET profit | 268 | 131 | 172 | 105 | 56 |

| EPS | 27 | 13 | 17 | 105 | 56 |

| SALES VOLUME(SCM MILLION) | Q4FY23 | Q4FY22 | Q3FY23 | YOY | QOQ |

|---|---|---|---|---|---|

| CNG | 217 | 204 | 228 | 6 | -5 |

| PNG DOMESTIC | 45 | 42 | 45 | 7 | 0 |

| PNG INDUSTRY+COMMERCIAL | 40 | 37 | 40 | 8 | 0 |

Good set of results by MGL.

Operating margins which were below 20% during last few quarters due to high NG cost is improving (24% in Q4).

Margins should trend higher in next few quarters as NG cost is down substantially and gas sourced by APM route ( which forms more than 80% for MGL) has come under price regulation as per KP committee adopted by Govt. Even though CGD companies have passed on majority gas sourcing cost reduction to consumers , it will help in increasing the volumes sold and margins.

QOQ reduction in sales volume in CNG to some extent must be due to BEST taking off 400 CNG buses due to fire accident during Feb/March which seems to have restated again.

Mumbai: Most BEST buses withdrawn after fire are back on road.

Q4 concall notes:

Increase in EBITDA in Q4 is due to reduced gas cost.

Gas cost was low due low spot prices and priority allocation of HPHT gas to CGD companies from Feb helping in replacing costlier RLNG gas.

APM gas price fixed as per KP committee recommendation from April.

CNG prices are reduced twice to current price of Rs.79 from Rs.89

Domestic PNG price reduced from Rs. 54/scm to Rs.49/SCM from April.

Covid impact and high CNG prices have impacted growth last year. One time impact on CNG in Q4 due to BEST taking off CNG buses for a month.

Volume growth guidance of 5 to 6% on a long term basis. With reduction in prices CNG volumes will increase, Raigad area industrial/ commercial customers and increase in domestic connections in the last 2 yrs will support growth.

Normal domestic PNG growth is 5-6%.

Management is open to reduce the gas price further depending on sourcing cost and alternate fuel prices.

Currently CNG price is 16% discount to diesel.

Present Spot gas at ~12$/mmbtu …HPHT at 12$/mmbtu. ( Was at average of 17$ in Q4?) … for next few month cost of gas looks good for us.

Domestic household new connections in Q4: 92k

Total conections 2.17 millions.

12 new CNG stations added in Q4 and 25 for FY 23. 41 CNG stations were upgraded.

FY24 target is to add 40 new stations in GA 2 & 3 and 40 will be upgraded.

Total no of CNG stations:313

Raigad GA:68K household connections. 28 CNG stations.

New Industrial and commercial customers added;115. total customers no: 4558

CNG vehicle addition during Q4 is low at 14k…with CNG price reduction from April volumes have grown at 7% week on week.

Among CNG volumes buses:8%, auto 3w:35% pvt car/tax:45% cv/trucks:10%.

CNG penetration is low in cv segment. OEMs are are coming out with factory fitted CNG variants in light commercial vehicles

Cng ecosystem is becoming pan india. All the highways from mumbai have CNG stations to distant places.

% of APM gas sourcing 93% in FY 23…likely to be 90% for FY24.

Rs/SCM is the right matrix to track for CGD companies than EBITDA% to revenue.

Op cost Rs.5.4 /scm in FY23.

EBITDA of Rs 12.8 /SCM IN Q4 for the whole year is Rs.9.5/scm.

Discussing with Mumbai municipal to set up a CBG plant.

One of the key risk factor for CGD companies is EV adoption which is increasing every year.This can have significant impact as the majority of revenue for CGD companies comes from CNG vehicles.

In the past the majority of conversion to CNG use to happen by retrofitting CNG kits to vehicles. Now the majority of OEMs come with factory fitted CNG variants.( we can see this when we go to Maruthi/Toyota showrooms where there will be hoarding mentioning availability of factory fitted CNG cars). As the CNG ecosystem is developing across the country with Govt focus on gas based economy by allocating geographical areas and new CNG stations it’s probable that both CNG and EV vehicles may coexist in future.

Below is the data from https://vahan.parivahan.gov.in/vahan4dashboard/ which shows the no of CNG and CNG/Petrol vehicles sold across the country by OEMs. Overall sales seems to be uptrending particularly for the CNG only variants( 2020 and 2021 covid affected yrs)

( I am not sure why no for the year 2019 is low. May be some data issue or automobile sales were low due to economic slowdown and NBFC/ILFC crisis)

| ALL India | 2019 | 2020 | 2021 | 2022 | YTD2023 |

|---|---|---|---|---|---|

| CNG only | 33,337 | 43,192 | 1,66,253 | 2,96,795 | 1,37,764 |

| Petrol/CNG | 4,04,900 | 2,16,899 | 2,49,739 | 4,05,604 | 1,50,270 |

We can track data using state wise and RTO wise. Below is the data for the state of Maharashtra which is relevant for MGL.

| Maharastra | 2019 | 2020 | 2021 | 2022 | YTD2023 |

|---|---|---|---|---|---|

| CNG only | 575 | 8,128 | 31,587 | 48,888 | 20,741 |

| Petrol/CNG | 1,06,098 | 63,981 | 71,640 | 1,09,422 | 37,585 |

Any thoughts on why the market is assigning such a low PE to MGL compared to its peers? Logically the business has a long runway ahead of it…

Revenue & Profitability is dependent on below factors (difficult to predict)

- Natural Gas pricing & its gap with alternative fuels.

- Govt. subsidies on procurement price (APM, Kirit Committee etc.)

- Govt. push for Natural Gas adoption

- Expansion to new regions + Penetration of existing regions

Kirit Committe Recommendations -

Supply from GAIL -