MGL has to manage sourcing the natural gas through different medium and pass on the cost to consumers. will the demand be the same if the price is hiked?

As I assumed about Sourcing the Gas through other medium for the deallocation of 20% APM will be matched, confirmed by the MGL management during the Q2 FY25 Earnings Conference call.

Also, the volume growth is at 7% Year on Year, Half Yearly.

MGL has to manage sourcing the natural gas & absorb the cost impacts, which leads to reduction margin eventually. but does this change the demand for PNG & CNG over the long run?

Based on the earnings conference call notes, the MGL management is not going to hike the gas price in the near term. Instead, they will try to improve the operational efficiency & midterm contracts for gas sourcing.

Future Plans:

On October 7 this year, MGL has entered an indicative and nonbinding term sheet with

International Battery Company USA for setting up an EV battery cell manufacturing facility in

India under proposed joint venture company, which is called International Battery Company

Private Limited. The plant initial capacity is 1 GWh, which will be developed in 2 phases of 500

MWh each. The proposed equity investment by MGL in the range of INR385 crores in this joint

venture with the equity stake of approximately 40%.

Has anyone worked out the material cost price increase annual due to external sourcing , and it’s effect on the EPS, and does it warrant a drop of more than 20% from 52w high ?

I don’t see any drop in end users for CNG,and fundamentals are strong, except for the margin squeeze.

external Sourcing price depends on the midterm contract or spot price, as per the APM the source is done at $6.5 per SCM, may be external sourcing at $9 or so assumption.

MGL management said, “it is purely depending on the contract or if it purchased from the new wells or so”.

above info is fetched from the earnings notes. FYI.

Just some back of the envelope calculation, for 20% external sourcing of 165 cr ( Total annual material expenses of 827 cr) @ 9 USD ,instead of 6.5 USD, which works out 27% rise on 165 cr =210 cr

The annual material cost increases by only 5%

The market cap from 52w high 1988 to 1388 is a drop of 30%

My mistake I took figures from Screener. in for quarter Sept 2024 ( 1313x 0.63= 827 cr), still percentage wise the calculation should hold, Correct me if I am mistaken !

Thanks Vego for clarifying. 6.5 to 9 is 38% increase. So using your analogy there is rougly 63Cr increase in Purchase of Stock in Trade. Net Profit for Q2 was 283Cr. So there is possibility of 22% reduction in profit.

Very Detailed explanation on Reduction of qty under APM. In 2 years time, APM qty would be Zero.

Also allow competition to get better pricing. Interesting.

The central government’s recent decision to reduce gas allocation to city gas distribution companies under the administered price mechanism follows a decline in overall gas volumes, said Gajendra Singh, member of the Petroleum and Natural Gas Regulatory Board.

Over the weekend, the government had reduced APM gas allocation to the city gas distributors by another 20%, marking the second straight month of reduction in gas allocation.

Talking to NDTV Profit, Singh explained the reason, even though the Centre’s policy for gas distribution prioritises allocation of APM gas to CGD companies.

He said that the APM gas supplied to CGDs was being produced in the Mumbai High and its discovery was made in 1986 or 1987. And this asset has “already reached the phase where a decline has started”. When Mumbai High does not have enough volume, "reduction in allocation will need to be applied”.

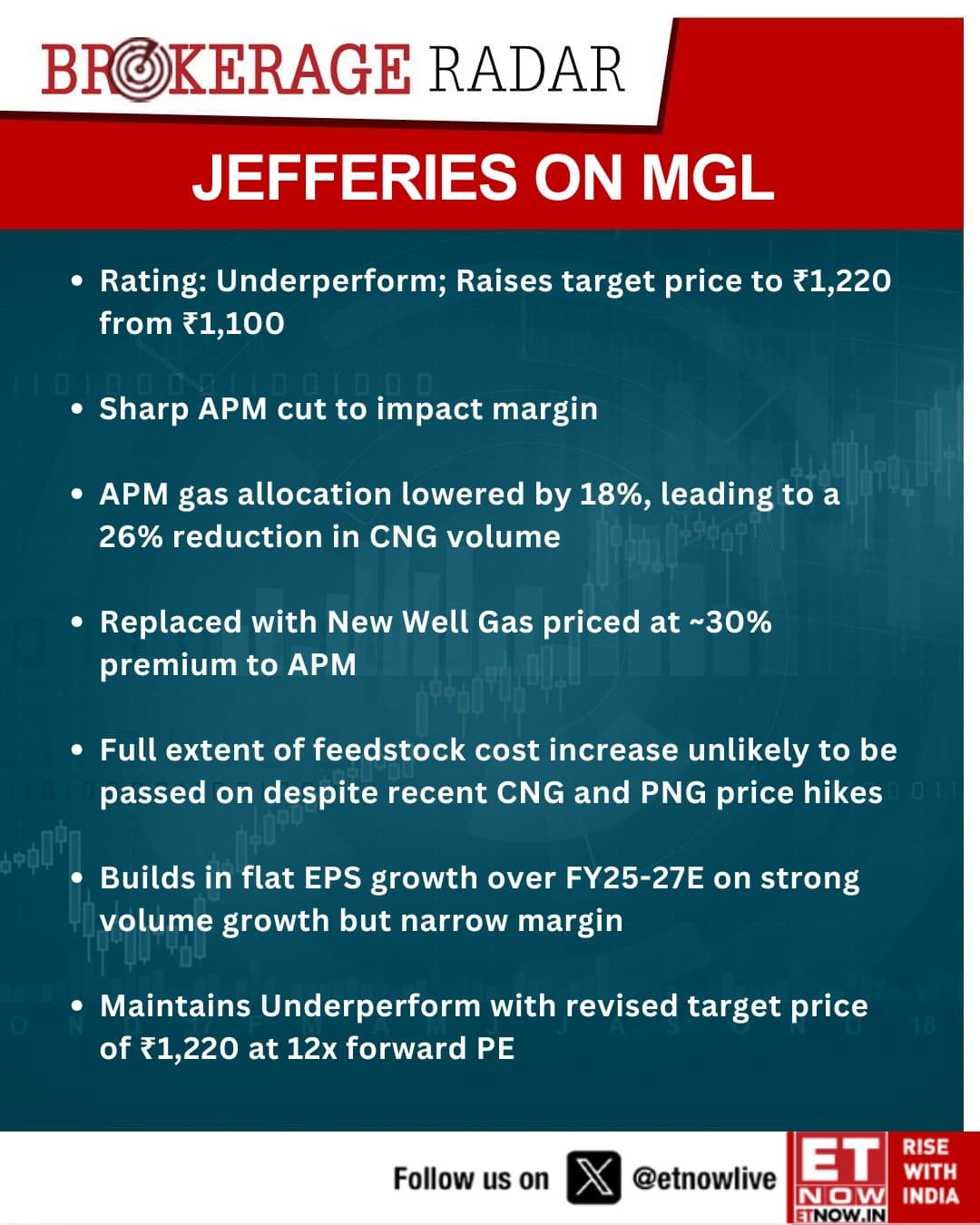

#BrokerageRadar Jefferies on MGL: Underperform, raises target price to ₹1,220 due to sharp APM cut impacting margin.

@Jefferies

CMP: 1312.40

The stock fell from 52 Weeks High of 1988 to the current levels of 1312.40, Thanks to Government APM Cut and not sure how long this uncertainty continues w.r.t these CGD companies.

A genuine query to all investors of CGD companies.

How do you deal with the volatility caused by govt changes in APM and Pricing.

Since this is a perennial problem, how does one put a target on rev growth and eps. Or do you assume the worst and then figure out right price to invest,

Asking because CGD obviously is the future. Question is determining entry price.

If they increase the gas price, the revenue will not be hit , conversely if they book long term gas contracts from spot markets, when the prices are low the impact on revenues would be minimal

Looks better than APM. CGD can do better now. Whether MGL will get a rerating?

"According to the ministry, the policy changes will allow CGD companies to better manage their demand forecasts and supply logistics, leading to greater operational efficiency. By aligning pricing to the Indian Crude Basket, the government also expects better affordability and transparency in gas procurement for CGD operators.

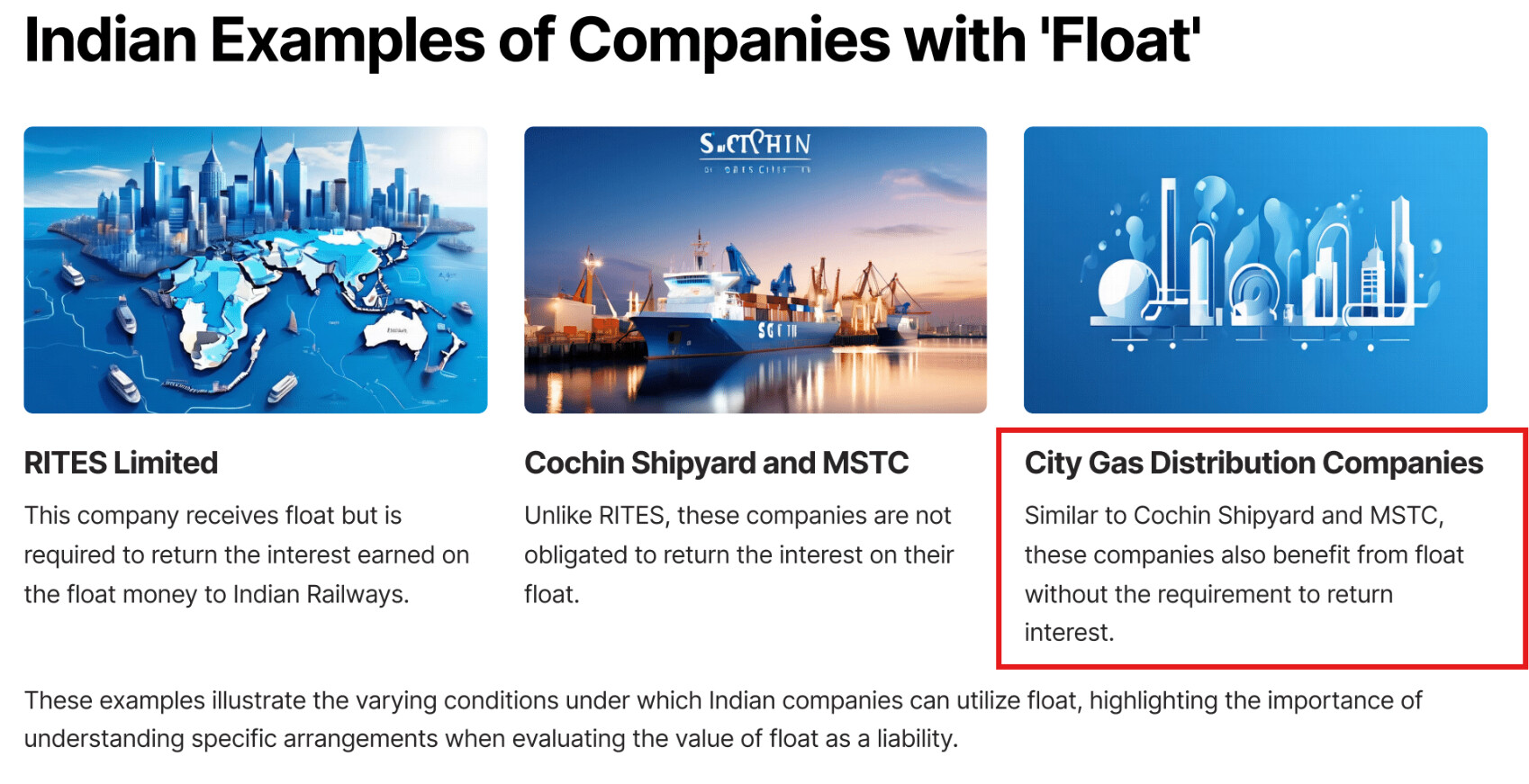

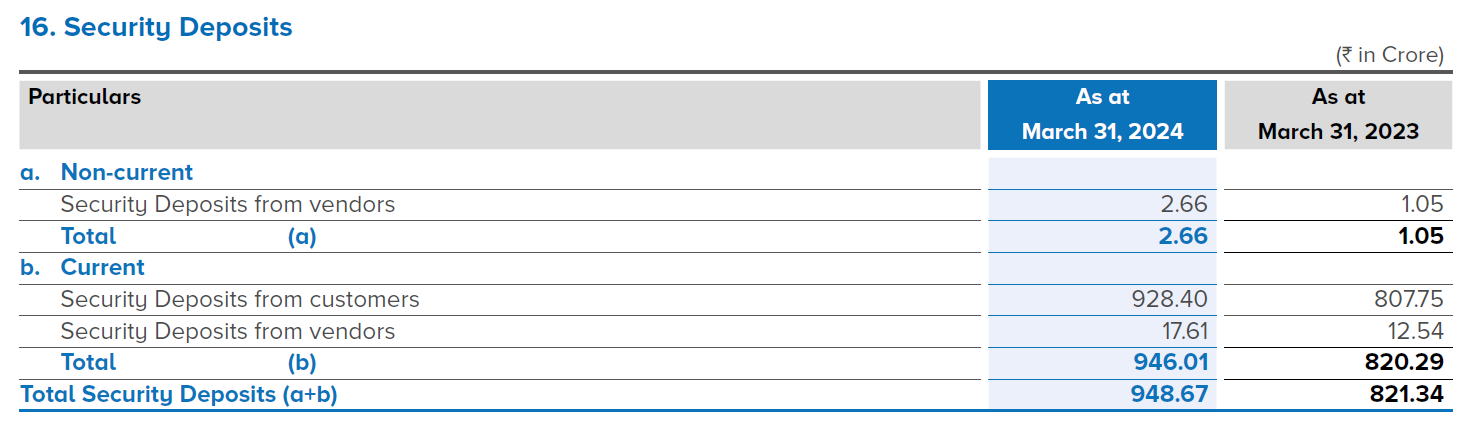

I believe it could be the Initial Deposit which we pay for getting the Mahanagar Gas connection which was Rs 5K in old days but now might be much higher. This money remains with the company for a very long period, Say 20-30 years or even more as mostly connections are never disconnected by most of the customers. To me, this looks similar to a premium which Insurance companies get in advance and they invest it in various financial instruments and earn interest on your money. It is called as “Float” in case of insurance company, and Deposit looks similar to this “Float” for a CGD company. They can use for 30+ years without paying interest to customers as per my knowledge.

I might be wrong as well but I am trying to understand it by using similar analogy from insurance sector.

Thank you @gsapte. You’re absolutely correct. This security deposit line does NOT show up in the Balance Sheet in either Moneycontrol nor Screener as this information is present only in the Notes to Accounts section in Annual Report. Screener has any entry “Advance from Customers”, but the amount is 33Cr & 27Cr for FY24 & FY23 respectively.