Core Business: Operates as an e-commerce platform specializing in electronic and robotic parts, including components for drones, E-bikes, IoT devices, DIY kits, and more.

Key Stats:

Over 30,000 SKUs.

Partnerships with 210+ vendors domestically and internationally.

A dedicated 35,000 sq. ft. warehouse with a staff of 200+ (both in-house and contractual).

Growth: Consistent growth in turnover, EBITDA, and PAT with a CAGR of 67%, 77%, and 88%, respectively, over the last three years.

2. Financial Highlights (H1 FY25)

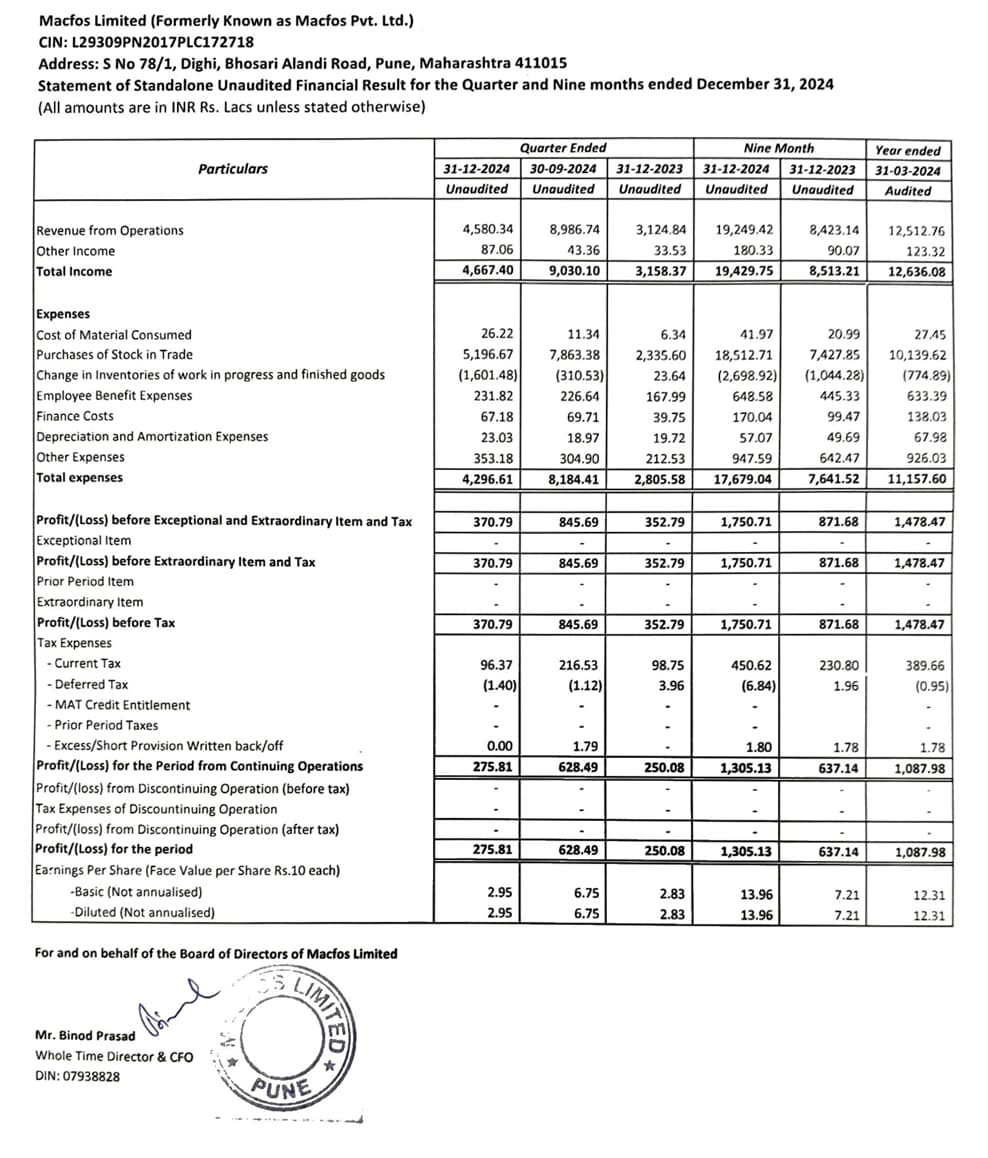

Revenue: ₹147.62 crore (+176% YoY).

EBITDA: ₹15.11 crore (+150% YoY).

PAT: ₹10.29 crore (+166% YoY).

Revenue includes a contribution from one-time corporate orders, which are non-recurring. Excluding these, core business revenue grew by 43% YoY.

Profit Margins:

EBITDA Margin: 10.23% (compared to 11.28% in H1 FY24).

PAT Margin: 6.97% (compared to 7.23% in H1 FY24).

3. Key Operational Metrics

Customer Engagement:

Total customers served: 80,838 (H1 FY25).

Average monthly website and app visitors increased from 4.57 lakh (H1 FY24) to 5.27 lakh (H1 FY25).

Category Revenue Contribution:

Key categories: Development boards (19.59%), Drone parts (14.85%), 3D printers & parts (13.11%), and batteries & chargers (9.37%).

Inventory Efficiency:

Only 3.08% of inventory is very slow-moving (compared to 3.68% as of March 2024).

4. Strategic Priorities

Robu 1.0 (Core Distribution Business):

Focus on delivering tech products at affordable prices with minimal lead times.

Expand SKU offerings (added 6,000 new SKUs in H1 FY25).

Enhance IT infrastructure and optimize supply chain cycles.

Robu 2.0 (Proprietary Products Development):

Long-term focus on building proprietary brands, particularly in drones, mechanical products, and other electronics.

Recent developments:

53 new SKUs for sensors and modules.

46 new SKUs across four new product categories.

Expanded offerings in tools and drone components.

5. Future Outlook

Growth Drivers:

Increased adoption of electronics in daily life and supportive government policies (e.g., Make in India).

Expanding the customer base, particularly among corporates.

IT and Operational Enhancements:

Leveraging ERP systems for operational efficiency.

Scalable in-house IT infrastructure to support growth.

Commitment to balancing regular business growth with new opportunities while maintaining sustainable profitability.

Well, the company is not about China or Taiwan. Of course, as China and Taiwan is major low cost manufacturer of electronic goods, the e-commerce operator do import those items from there and sell. Even if say tomorrow, China or Taiwan cease to exist or Government prohibit any import from those countries… still the e-commerce operator will procure the goods from somewhere and sell it. Thus, China or Taiwan is not very relevant.

What is relevant is electronics and drones. Recent middle east crisis has shown the power of electronics and drones in warfare. I think that now drones are not merely hobby items, it is serious business. Macfos has some edge in those areas as e-commerece operator and if they are lucky, they can maintain the lead.

Our govt won’t ban imports but sanctions on China will make difficult to import such things. And I don’t think there are many options beyond China, it will heavily hit revenue for many quarters as getting alternatives and having agreements with them will take lot of time (if they get alternative). Plus, the supply chain will put much strain on those alternatives making it difficult to procure.

Hi @Divyanshu_Parganiha Robu has penetrated to the higher education sector in India. I did a random sampling and most of the students with whom I had interacted, know about the brand and they purchase from Robu. Along with this, the National Education Policy is pushing for more projects and student lead startups in which they use Robu for sourcing and prototyping. The spending can be from a few thousand up to a lakh rupee in value. The post on Holmarc has a great discussion on NEP for reference and applies here. Like Holmarc Opto Robu is also active on GEM ( Eg: https://www.iiserpune.ac.in/storage/media-library/43d3815a-2003-406c-8e30-6143efcffe62.pdf). As I understand it, a strong customer base and brand building is happening during this process.

I consider Robu as the Indian equivalent of McMaster Car or Grainger. The growth can be compared for study purposes.

I can see valuable discussions on other aspects in the forum and thank you for the perspectives.

Could you clarify how we compare growth of Grainger to Macfos, Macfos is electronic/embedded tech seller. I want to estimate TAM SAM SOM so that we can estimate revenue at saturation, this will also give us insight how much max PE ratio is acceptable.

I appreciate your perspective on this topic. I want to share my thoughts, which might differ slightly. Many of these companies have a significant customer base in the startup sector, sitting at an intersection between B2B and B2C. Typically, the purchases made are geared toward prototyping, which accelerates their development processes.

It’s worth noting that many startups unfortunately do fail, making way for new ones to emerge. U.S., reached a level of maturity in this ecosystem, but in India, the startup scene is still in its infancy and shows immense potential for growth. I genuinely believe that Macfos could thrive alongside this evolving landscape.

I hope my insights add some value to the discussion!

Number of shareholders are growing at healthy rate. Including increased holding of DII. DII are buying from public rather than promoter which is another good thing.

The company has shared Investor Presentation. Macfos-Investor Presentation.pdf (2.0 MB)

Totak number of SKUs has exceeded 50K. Now they are serving around 1 lakh order per quarter, with average value of Rs. 4600/-. On various parameters, the companies performance is improving.

There has been dip in the margins in Q3- 2024-25; which management has explained. Overall good performance of the company continues.

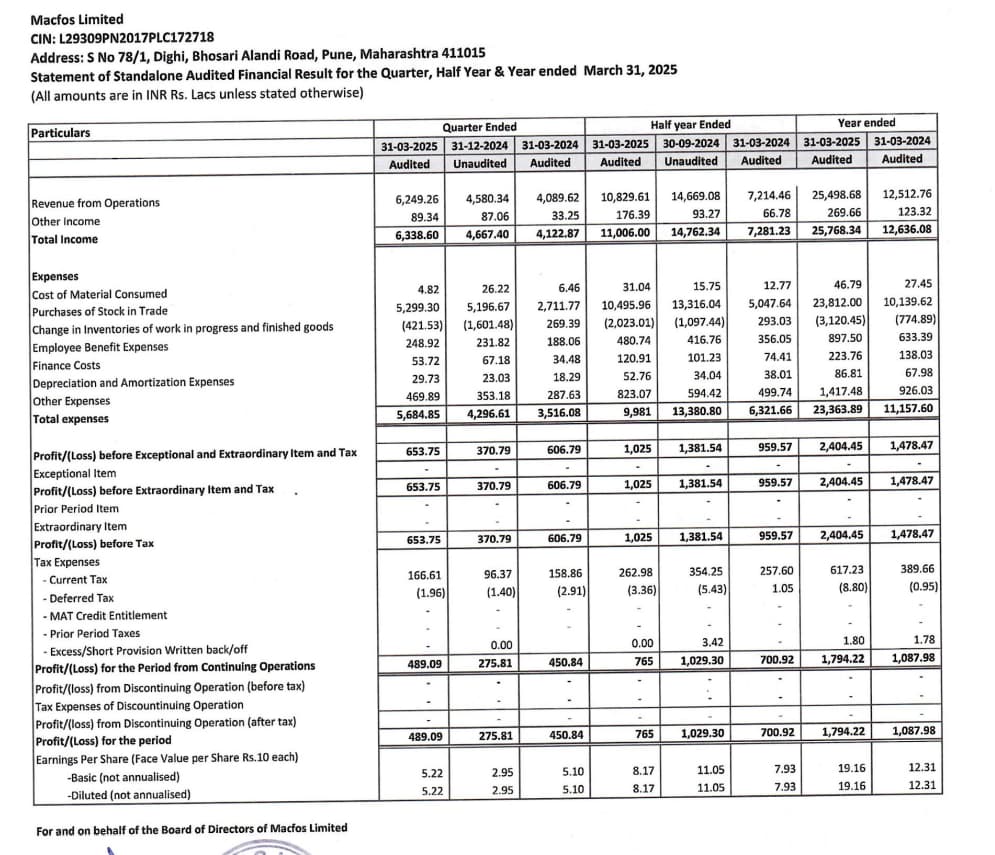

The result has been pretty robust. Excluding the one time sale of around 50 crores in Q2-2024-25; the company is growing at the rate of 50%. Margins appear to be improved in Q4. If the momentum continues in current financial year, we can expect a topline of more than 300 crores, with net profit of Rs. 30 crore plus.

Hopefully the good story continues.

The latest results have been decent, although I guess existing investors were hoping for a higher annual PAT number. The company is trading at roughly 45x past earnings and 30x one-year-forward earnings assuming a 50% revenue growth with intact margins (though we’re yet to hear from management regarding their guidance). Given the current macro-environment, with urban consumption being sluggish, I find it quite a bit pricey on the forward PE front to invest at current levels. In my limited experience, generally it is hard to make money on stocks with a 1-yr forward PE of more than 20. Hopefully, I’m wrong here.

Though it is easier to buy low p/e stocks, a company growing at 50 percent is a different phenomenon. In such companies we should focus primarily on sustainability of growth and margins.

This year they have added more than 50K SKUs… When the company got listed one and half years ago, it had 12K SKUs, now they have 72K. Number of customers, number or orders and value of orders are increasing at a decent pace. With such a growth rate, the company will become almost a monopoly in electronics e-commerce market.

On a trailing earning basis, the company is trading at around 45 times. If the company can grow at the rate of 50 percent merely in current financial year, 45 times look justified. It 50 percent growth rate can be maintained in 2-3 years, the company may command pretty high p/e than 45. If it can grow at this pace for 5-10 years, no body knows the value.

The company’s current P/E ratio of around 40 is actually below the average P/E seen in similarly high-growth small-cap e-commerce companies. For context, leading e-commerce players are trading at significantly higher valuations — Zomato’s P/E exceeds 400, while Nykaa’s is above 1000.

Evaluating a high-growth small-cap solely based on its P/E ratio does not present a fair or complete picture, especially when compared to its peers in the e-commerce space.

Regarding the broader economic environment, it’s important to recognize that a sluggish economy impacts all companies across sectors. Excluding this company from consideration on that basis alone would be inconsistent.

It is true that small-cap companies are generally more sensitive to economic downturns, particularly due to elevated borrowing costs. However, if one’s investment approach is to avoid all small-caps for this reason, then that strategy should be applied for all small-caps rather than selectively picking few smallcaps.

Finally, from a management perspective, I appreciate their efforts to build a strong internal culture, evidenced by initiatives such as the “Robu IPL” and other employee engagement events. This suggests the leadership is committed not only to driving financial performance but also to fostering a positive, sustainable work environment, signalling their intent to remain and grow in the long term.

Well, you’re free to bet with your money if you have a strong conviction

The only thing I would say is that it is downright illogical to compare Zomato to Robu. Zomato has an OPM of 1%, which can easily jump to 10% if they stop chasing growth-at-all-costs and start raising prices / cutting staff. That effectively would cut down the PE to ~40, which is far more digestable for a pan-India food-platform business. Nykaa seems to be in another universe altogether, and I don’t understand women’s fashion, so I’d rather not comment. These business have turnovers in tens of thousands of crores and are still growing 20% minimum (60% for Zomato).

Robu is nowhere near and doesn’t have the privilege of even doubling its OPM; these businesses are 30-70x larger.

There is merit in both sides of the argument. Personally, I wouldn’t be loath to taking a bet on 750 cr m.cap company if it can become 5000 cr in 5 years. To get to 5k crore, assuming an exit PE of 20, the company needs to do 250 cr in PAT or about 3500 cr in topline. That is 14x current scale. B2B niche mey this kind of scale ka plausibility needs to be understood. Mathematically that is 70% CAGR for next 5 years, and ~60% of the demonstrated CAGR in the last 5. But maintaining such CAGR on a higher base each year is a different hurdle altogether.

Would love to reach out and connect with management here for some visibility and confidence.

Why does everyone view Macfos as an e-commerce firm?

It’s a Redington-style trader that sells stuff through a website. I am sure they have a small sales force as well.

So, it should be valued at the same level. Sure, margins are slightly higher, but that would not sustain. Players like Ofbusiness, Inframart, and other traditional electronics and equipment trading companies will target this niche.

Revenue I have no idea but margins would be in mid-high single digits at best.