Hi Sidharth,

Thanks for the business model analysis.

Yes, you are correct. KRBL Margins > LTFoods Margins, due to transport cost. Now, LTFoods are planning to expand in Middle east. Isn’t a threat to KRBL business?

Hi Sidharth,

Thanks for the business model analysis.

Yes, you are correct. KRBL Margins > LTFoods Margins, due to transport cost. Now, LTFoods are planning to expand in Middle east. Isn’t a threat to KRBL business?

I think, indiagate is superior brand and it is available at premium price than Daawat across all basmati segments.That is the real reason for higher opm of krbl(Indiagate rice is more aged and so have better quality and premium rate).That is real moat of krbl

However, i am betting on new products, organic products, good advertising, and good financials of Daawat available at cheap pe ratio.

Disc…invested in lt foods

Middle East business is very tough to crack and very big market. Daawat is trying to grow it’s business here, but it is not necessarily mean they taking the business from KRBL. It is indeed the nature of the business. Every company tries to enter new territory. Daawat tries to grow in Middle east, KRBL tries to grow in US. This threat always exists and we have to wait and see how things evolves.

Brand perspective and Brand Quality are two different thing. India gate is indeed a brand with better perspective. That does not mean Daawat is inferior to Indiagate in quality. They both buy from same set of farmers, both are equally aged. I am not sure from where you figured out that daawat is less aged compared to India gate.

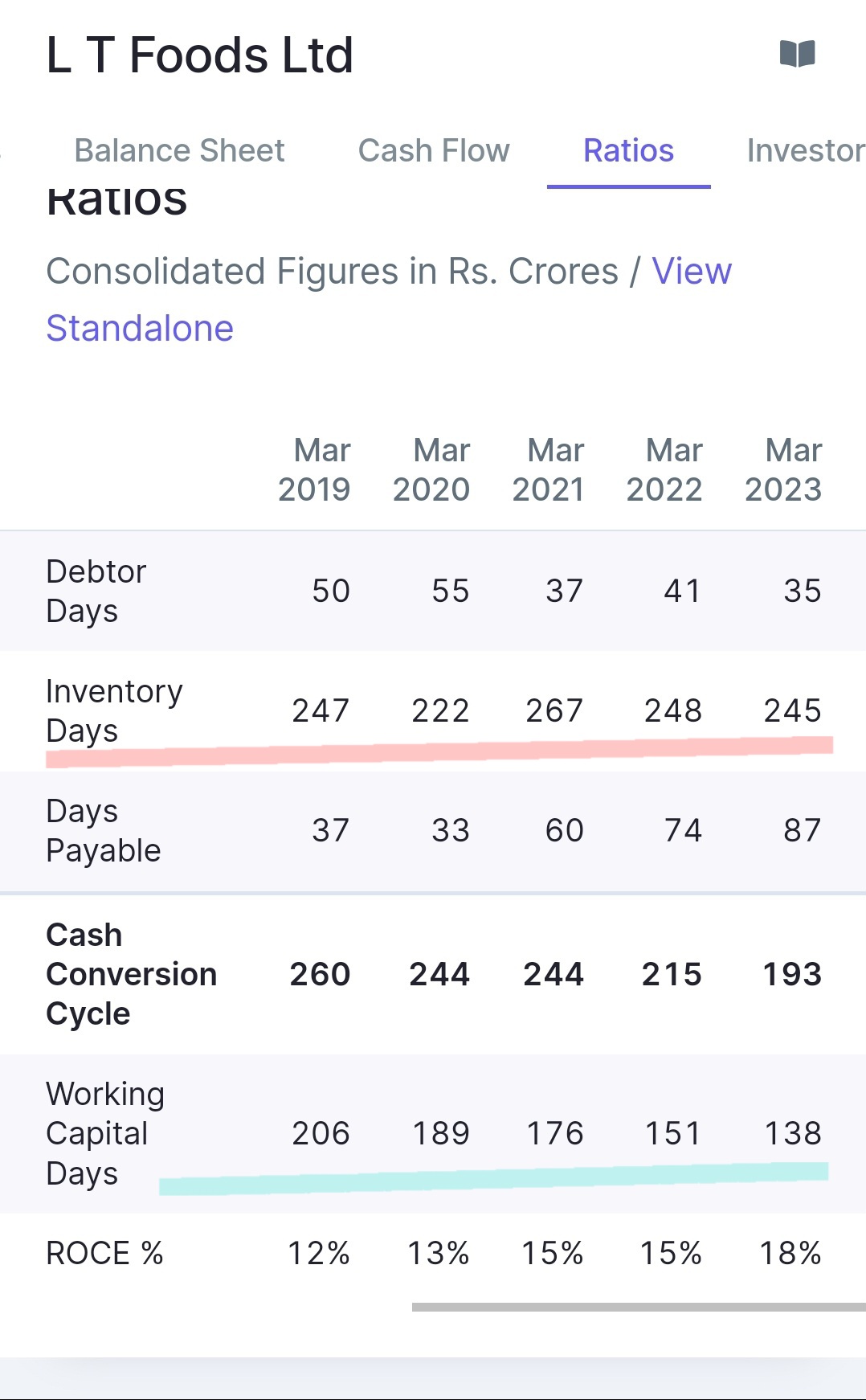

When I look this number in past, I thought so. But again when you look into the product range LT Foods offers, You will find the difference.

Incase of KRBL, It is pure play basmati rice[as of one year ago]. They buy basmati paddy age it, sell it. Even for KRBL, not all rice are aged for 2 years. That’s why you will see inventory days near to 1 year and not 2 years. Be their local sales or export their, rice remains same, process remains same.

Whereas when it comes to LT Foods, The business model of brand Daawat alone is comparable with IndiaGate. Which is equally aged, equal quality

And sub brands like Tibar, Dubar, Rozana, Devaaya are either rice length is short which you will not get premium anyway and these are not necessarily aged less. Some of these brands are sorted out rice which are less in length from 2 year aged rice.

Now when it comes to why LT foods inventory days are less, The Brand Royal does not deal only in basmati but also other rices like Jasmine rice, for which they import from the sellers in thailand. So ageing is done by millers in thailand and not by LT foods, so there is no inventory days, other business like organic and convenience also needs much less inventory days.

In short, Other segments of LT foods except brand Daawat pulls down the Inventory days. I agree to the point IndiaGate commands a premium but that is because brand perception not because of quality/ageing [To validate this, I am from Tier 3 town in tamilnadu, till 2 years back i have no idea that a brand called Daawat exists, on other hand we buy indiagate regularly] In comparison done by you, compare indiagate rozana with Daawat Rozana Gold, you will find MRP matching

Disc: Bullish on both KRBL and Daawat, Invested in Daawat

Does anyone know what quantum of other rice (ex-Basmati) like Sona masoori sold in North america by LT Foods

Almost Nil as I know

What effect on this stock for baned rice export by government???

Despite the decline, non-basmati rice remains an important part of LT Foods’ international business.

| Year | Non-basmati rice revenue contribution (%) |

|---|---|

| FY2020-21 | 25 |

| FY2021-22 | 22 |

| FY2022-23 | 18 |

L t foods update(from credit rating 2023 and one research report)

1…Performance 2022-2023

27% revenue growth

36% net profit growth

2…FUTURE FROWTH

…Segment wise Growth

a…Robust growth in basmati rice segment (+30%YoY, contributes ~83% of total revenue), supported by both volume and price growth.

b…Organic foods segment (~9% of total revenue) grew by 25%YoY and

c…Convenience & Health segment (~2.1% of total revenue) grew by 3% YoY.

A…Branding and distribution network

=LTF’s consistent efforts on strengthening the brands, widening distribution, and region

& product diversification through organic & inorganic routes have been the strategy for growth.

=LTF targets a 5Yr revenue CAGR of 10-12%, aided by continuous focus on

a…Expanding its product portfolio,

b…making investments in branding

c…and strengthening its distribution network.

=Retail outlets have increased by 9%YoY to 1.77 lakhs, which will strongly support future growth.

B…Organic food segment

= Organic business is continuing on the path of strong growth and registered a CAGR of 18% over last 4 years. Further, growth in organic business should lead to higher consolidated revenue over medium term and remains key monitorable factor.

C…LTF has recently acquired Golden Star Trading Inc. to strengthen market share in US (Jasmine rice segment, the brand has ~10% share in US

market)

D… The strategic transaction with SALIC (PIF, Saudi SovereignFund) currently holds ~9.2% stake in LT Foods (Rs.455.5cr) is expected to provide future growth plans in the MEA and Saudi Arabia regions.

E…Capex

=LTF is doing a capex of

Rs.140cr/Rs.120cr in FY24/FY25 in power generation, warehouse, and the capacity enhancement (by ~1 lakh tons)

F…Improving financial risk profile:

=LT’s group dependency on debt levels has reduced y-o-y. Group’s 80-85% of debt primarily comprises of short-term debt (working capital borrowings) required for stocking-up of paddy and seasonality in nature of business.

Disc…invested

Q2 FY24 Concall Notes:

Company Gaining Market Share in both India (30.2% with 160 bps improvement) and USA (gained 1.6% Market Share compared to previous Quarter). USA contributes 41% of the sales and with the acquisition of Jasmine Brand company is doing very well.

Company entered 5 new countries making the total presence to 78 countries.

Gross Margin has reduced to 31% due to increase in Input cost and reduction in Price in USA by the company due to competition. Company expects Margin to be in the range of 32-33%.

EBITDA Margin has improved 248 bps due to decrease in freight costs and economies of scale.

Revenue has grown 15% y-o-y. Historically H1: H2 sales ratio is 45:55. Management expects the same to continue this year also. Company expects H2 to be positive.

Organic soya business has de-grown because of this anti-dumping duty on India, So, company has put organic plant in Uganda.

Health and Convenience Segment: Company just launched Briyani kit and other products in India. In USA its growing at 8%.

Double digit revenue guidance given by the management.

Debt levels will not increase from here as per Management.

Working capital days improved, long term debts has been brought to negligible levels all these have led to significant improvement in Financial Ratios like Debt- Equity, ROE and ROCE.

For inclusion of SALIC we have diluted our equity which is more of a strategic nature so as enter the big Middle East Market. Management said they have no plans of further diluting the equity.

Invested and Biased

Finally company received order in its favour. https://www.bseindia.com/xml-data/corpfiling/AttachLive/0d5ab9bb-1741-42ad-ba31-fdd6a8da97ed.pdf

Resignation of M/s Grant Thornton Bharat LLP as the Internal Auditor of the Company w.e.f.

January 17, 2024.

They have resigned because of their preoccupancy and inability to continue as the

Internal Auditor of the Company

Hello All,

As per the data from LT foods:

This has been a general trend for dawaat

Their Sept Dec results are always at par from last 3 years.

Although this time they are able to keep their margins same and overall it has increased.

Their ROCE has also increased over the years.

Disc: Invested, my views may be biased.

Health and convinience segment contributes 3% revenue and growing at very fast pace @23% cagr.

If these products are clicked in future, lt foods will definately become FMCG company.

Disc…invested

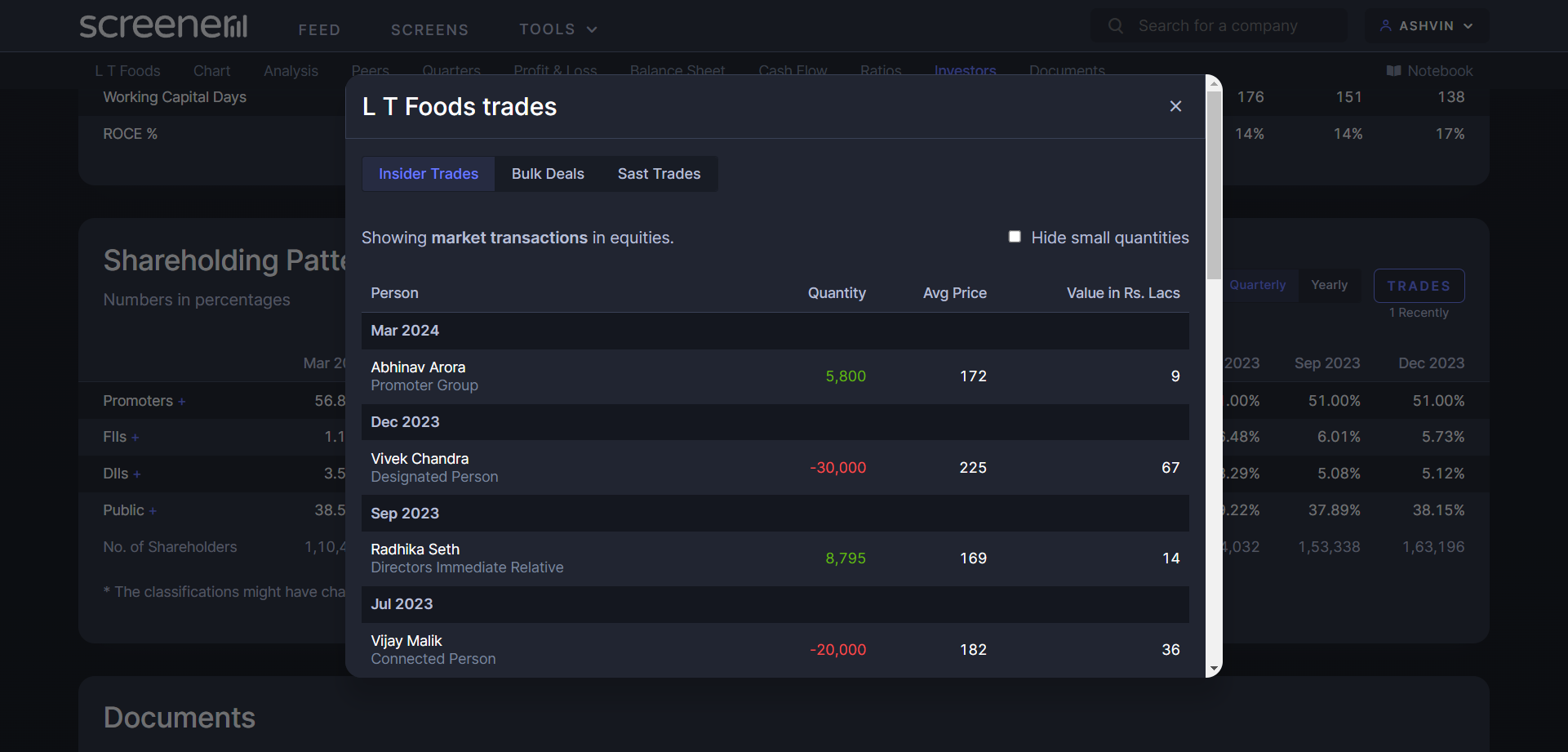

ABAKKUS ASSET MANAGER LLP has bought 33,93,543 Lacs @ 162.04/- before that Motilal Oswal Growth Opportunities Fund Series II has hold 34,81,504 shares and almost 700,000 shares added by DSP in Feb 2024.

So good fund manager is showing interest on business!!!