CONCALL SNIPPET Q4

Abhishek Maheshwari: Okay. So overall basis, you are seeing it was a 10% volume growth. Okay. And going ahead, do you see this to maintain similar levels in FY’24 also 10% to 15% volume, sir?

Ashwani Kumar Arora: Next year, as we are optimistic and the category is growing across the geography we are working. So we are positive to deliver double-digit growth

Abhishek Maheshwari: And I’ll get back to this maybe later on. Secondly, sir, do you see that at 11.5% EBITDA margins, you are at the peak of the operating leverage, or there is still some potential that operating leverage will kick-in with higher volumes and EBITDA margins quite improve?

Ashwani Arora: If there is a potential, we have given the guideline that by year 2025 our return on equity will be, we are targeting 20%, return on capital employed 23%. So there is still a room for the margin expansion.

Mohammed Patel: It is very difficult to hear you. Second question is, is the freight cost only reason of improvement in margins? And if yes, do we see that we shall pass on the benefits in correcting prices downwards in coming quarters?

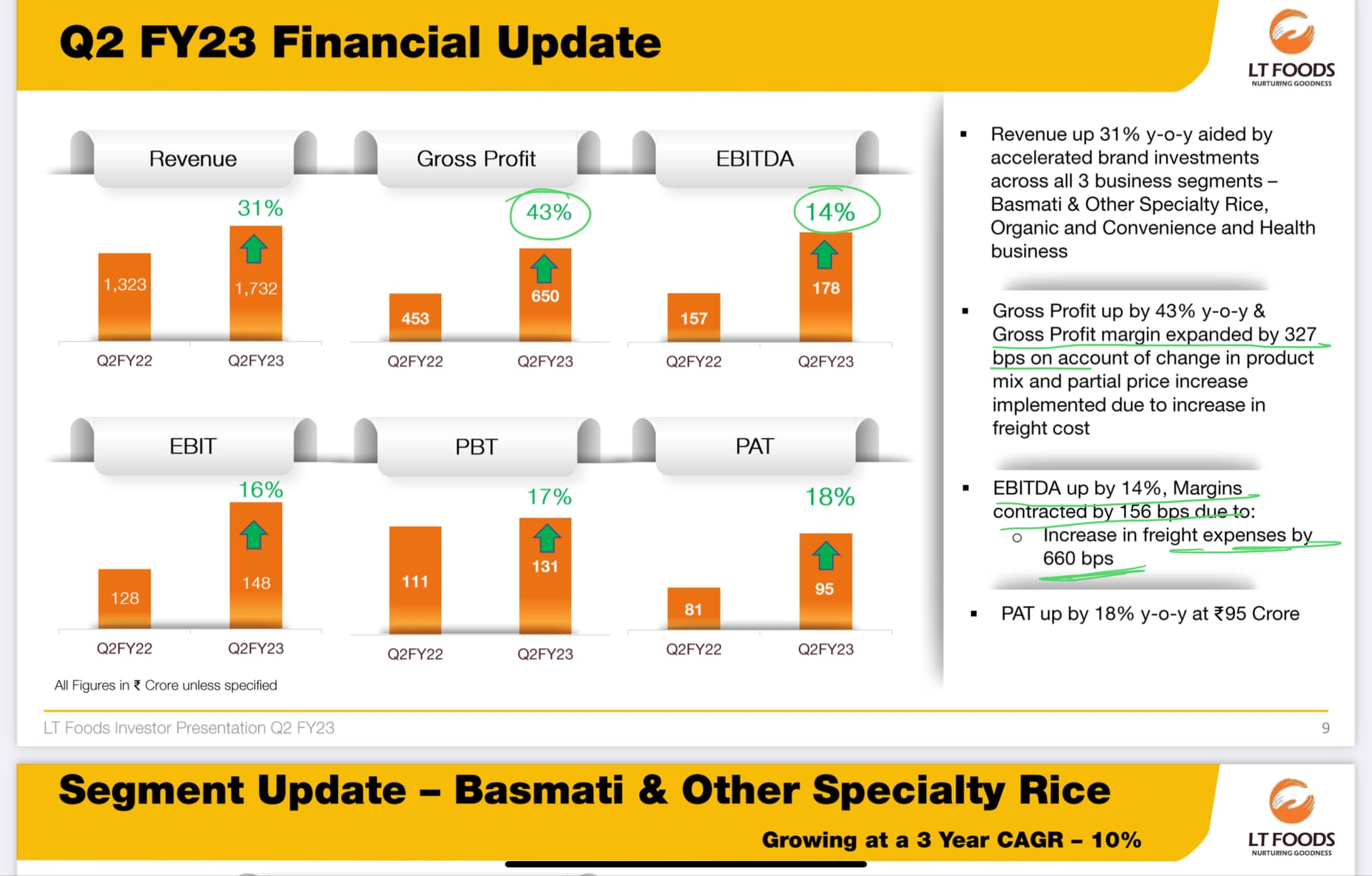

Sachin Gupta: Freight cost was one of the reasons for the growth in the margins in the quarter as well as year-on-year basis. So of course, certainly, certain part is to be passed on. But I think, the whole part will be passed on. So we are expecting a margin expansion in the going forward years as well. There was certainly the scale also kick in and I was able to have a 44% expansion in the profit on out of scale asset. And there was a GP also increased. So all these factors impacted to an increase in the overall EBITDA margin in this quarter.

Sunil Inani: Right, sir, and what are your capex plans going forward?

Ashwani Arora: So it will be similar in the range that we have done in the last year. So similar we will be increasing the production. Some will go in generation of power, and some will go in capex.

Amit Jeswani: A great set of number. My first question is, and my team has been asking you the same question multiple times, but sir your equity today is INR2,800 crores assuming you do a INR500 crores PAT next year, you’ll be at INR3,300 crores and broadly to achieve the 20% ROE okay, which you have guided, you’ll have to do INR660 crores of PAT that would be super. As of today, sir, we are – our market cap is INR4,000 crores. And you are now 40% bigger than the market leader, the old market is leader. If you reinvest this cash flow that you’re generating, I’m just seeing your last 4 year’s free cash flow is INR1,000 crores, right, your operating cash flow minus capex is INR1,000 crores. Sir, it makes no sense for you in our humble opinion, so why are we not doing buybacks at the INR4,000 crores market cap. You’re less than 9 PE, 10 PE your ROC will be north of 20%. If you can reduce your equity, you’ve been looking at a very large EPS. Our EPS today is INR12.5. You’re targeting closer to INR18 EPS and if you do a buyback of INR300 crores, INR400 crores, you’re looking at north of INR20. I’m just trying to understand, sir, you’re thinking about it. Because you’ve built a building business in the last 70 years. You’ve got one of the better auditors. Just trying to understand how you think about it.

Ashwani Arora: No, we have – as said in the last con call also, we are positive and because at that time, some deal was happening. And we are positive that in the next board meeting we may discuss about that.

Amit Jeswani: Got it. And Arora ji, typically, whatever you’re guiding, you’ve been able to achieve for last multiple years. How confident are you on the INR650 crores kind of PAT in FY’25 of the 20% ROE? That is the minimum PAT that you will have to achieve from INR420 crores PAT today.

Ashwani Arora: So we are very confident. That’s why we have given the guideline

Amit Jeswani: Sir, are you investing in power that KRBL doing. So now your margins will actually move higher from the 11% level closer to 14%, 15% in the next two years, is that the trade year? Ashwani Kumar Arora: That’s what the guideline is that we are targeting to have EBITDA margin, 13.5%. That’s what is one of the building blocks.

Ajay Rajguru: What is the size of distribution in India? And how many number of distributors and total outlet that you reach directly and indirectly?

Ashwani Kumar Arora: So in general trade, as you said, the retail outlet, we cover 171,000 outlets. And we are across all omnichannels and 110, distributors are at 1,200 distributors.