Any idea who the seller could be? 1.5% stock traded. Dont see SALIC, DSP, motilal selling. Could it be a FII seller?

Wait for day or two!!!

Check March 2024, shareholding !!!

What’s your observation on the same?

why market had not given high PE to it.historically it had traded at much low pe…

I think because Rice come under commodity category.

2 Likes

Whether a company is selling commodity is indicated by the ROE that the business is making. In case of LT foods it is consistently making 16 ROE and the operating margin has not gone below 10 in last 10 years. Market is cautious of Rice companies after KRBL fiasco, but if the business continues to deliver, I think it is a candidate for rerating

5 Likes

IF they focus more on value added products like Organic and ready to eat food segments, then high chance of rerating. One of the most recent commentary, they had better Income as compared to last year (9 months), due to realization of RICE. Then Cherry on the CAKE is Volume and Value-added products.

2 Likes

The sector is subject to whims of the regulators when it comes to exports. Also it’s a commodity, branding offers very little moat. One positive I see is that the company is foraying into packaged food, if that segment fires well then we can expect a PE re-rating.

3 Likes

I have a question, and if someone can please help me understand it, will be helpful.

LT Foods has consistently maintained 10-12% OPM over a long period, whereas the same for KRBL/Chamanlal Setia is not reflecting. Checking historical price trend of Basmati Rice (C Setia page 18/35) , I find it surprising how they have managed to maintain these margins. Their annual report mentions strong brand allows them to pass off these hikes to customers, but then India Gate is also a strong brand, however they can’t maintain it.

Can someone please throw some light on how this works? Is pricing for Finished goods different in US and EU? Logically, if RM and FG are both subjected to such fluctuations and there is a gap of 1-2 years in transactions, they should be impacted by this, correct?

As I close my research for this scrip, this is a big pt in my mind. (Risk being that actual OPM is quite large and they are skimming off in good years and putting something back in bad years)

I have no investment in this, and I am studying as of now

3 Likes

Pure Rice under control of Govt vis-a-vis Basmati Rice is exportable commodity. Generally, Basmati Rice is long age and 2-3 years is required for good exportable quality. Margin somehow to be maintain, If somebody in market leader, reverse control on SCM.

Sharing whatever little I understand considering last 5 years. India Gate is a strong brand of aged basmati rice which is reflected in their margin (14-21%) which fluctuates with RM cost and other factors. Chamanlal Setia does not age rice so OPM is lower but still fluctuates widely (8-14%). LT food appears to be following an approach to either invest profits back into strengthening business by innovations, efficiency etc. or passing on benefits to customers to maintain its 12% margin even in good years. Considering the risk scenario you mentioned, they should not need to put anything even in bad years as the margin in aged branded basmati rice from india gate is always northwards of 10%.

3 Likes

@yashchandak if you look into last 10 year data, LTFoods also has these fluctuations. When you look into quarterly data, you will find margin fluctuates between 9-13%, and by the same time KRBL fluctuates from 18-24% (except the quarters where they have deferred sales, stoppage in KSA sales, abnormal export of bulk rice). In Chamalal setia also, in FY21 you will find very high margin because of bulk exports, for other years you will find margins consistently increasing. FY21 is abnormal year for all 3 players.

Since LTFoods has less margin in absolute number basis, it may not look fluctuating, but if take median margin of both business, you will see margins fluctuates between +/-20% to median margin

2 Likes

LTFoods:

As per my understanding:

- Since their 80% of revenues are coming from exporting (US & Europe) & within india - premium brands of aging basmati rice business, which is cash cow.

- Organic & convenience segment - till now they are not contributing much.

- How LTFoods are ensuring consistent margins? Absorbing short term(1-2 Quarter) pricing shocks & also passing this to customers if they exists for long term(logistic costs).

- LTfoods is addressing the cyclicality - by establishing brands basmati business(cash cow) exporting to western countries. They are testing different high margin segments like snacks, organic, convenience, soyameal - if they are successful in anyone of the investments then re-rating will start (consistent earnings with high margins). Now all the big boys(MF, FII) are watching ltfoods from past 1 year, if they have consistent earnings for the next few quarters you can see huge rerating.

9 Likes

Hello Siddharth,

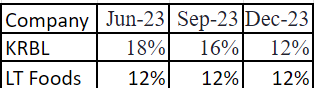

If I check last 3 quarters’ OPM for KRBL and LT Foods

The same can be seen in Mar’22 to Sep’22. I am not sure if they are reflecting the same trend in quarters like you suggested sir

@yashchandak KRBL last few years are very turbulent. In one Quarter they were able to export high broken rice and in other quarter, very high bulk export, in one quarter they have Saudi sales starting and in other quarter Saudi sales back to zero. In one quarter, a bulk shipment is not delivered to client and revenue got deferred to other quarter.

I would recommend you read concalls of LTFOODS and KRBL for last 5 years, You will neither find positive nor negative surprises from sales perspective for LTFoods except impact of soya sale due to US anti dumping duty. But in KRBL, you will find lot of these surprise both on positive and negative side, which makes their revenue to fluctuate lot higher even after factoring rice/paddy price fluctuation, this makes their Ebitda all over place

When it comes to LTFoods margin, In presentation you can find the Rice segments margin, you will find fluctuations, but offcourse not to the extent of KRBL which is due to their own problems

Q1 - 12.9%, Q2 - 13.9%, Q3 - 14.8%

8 Likes

Also KRBL has corporate governance issues and I am not sure if the promoters are honest. I found LT Foods management quite honest and clean.

2 Likes

Pls don’t think I’m questioning your statement but just curious as to how you assessed L&T foods management and found them clean. I like them too but wanted to get your opinion.

1 Like

Negative press about KRBL promoters depressed the share price several times. Look at KRBL’s shareholding pattern you’ll get your answer. About 6% held by Joint Director Of Enforcement, Central Region

3 Likes

I would not mind a bit even if you questioned my statement . Anybody can go wrong and there is no reason that I cannot. Infact identifying flaws in reasoning or beliefs can help us become better investors. Anyway, coming to the point I have never heard negative publicity of promoters unlike what I heard about KRBL promoters. This is partly the reason I chose LT foods over KRBL. Apart from this, I tend to observe what promoters said in the past and whether the results actually matched with their talk. Most of the time, I see they said something and they did it. They also acknowledge factors beyond their control and give a realistic view of the business.

A dishonest management would overcommit and always talk unrealistic things and miss out of what they committed last time. Having said that I would also love to hear if anybody has negative views about them.

5 Likes