L t foods(DAAWAT)

LT Foods Ltd. (LTFL) is one of the leading basmati rice players in India having a strong foothold both in exports & domestic market .

=Key brands include Daawat (leading brand inIndia), Royal (#1 brand in USA) and ecoLife (organic food).

=It is moving up the Value Chain towards a branded foods company by increasing portfolio of organic food and new value added products.

=It is expanding its geographic presence by organic and inorganic growth.

=Its geographical segments include India, North America, Europe, Middle East and Rest of the World.

= Its operations include contract farming, procurement, storage, processing,packaging and distribution.

…

BUSINESS PROFILE

A…Domestic@35%

B…Export@65%

USA@37%

Europe@14%

Middle east@9%

54% market share of USA

26% market share of india

10% market share of middle east

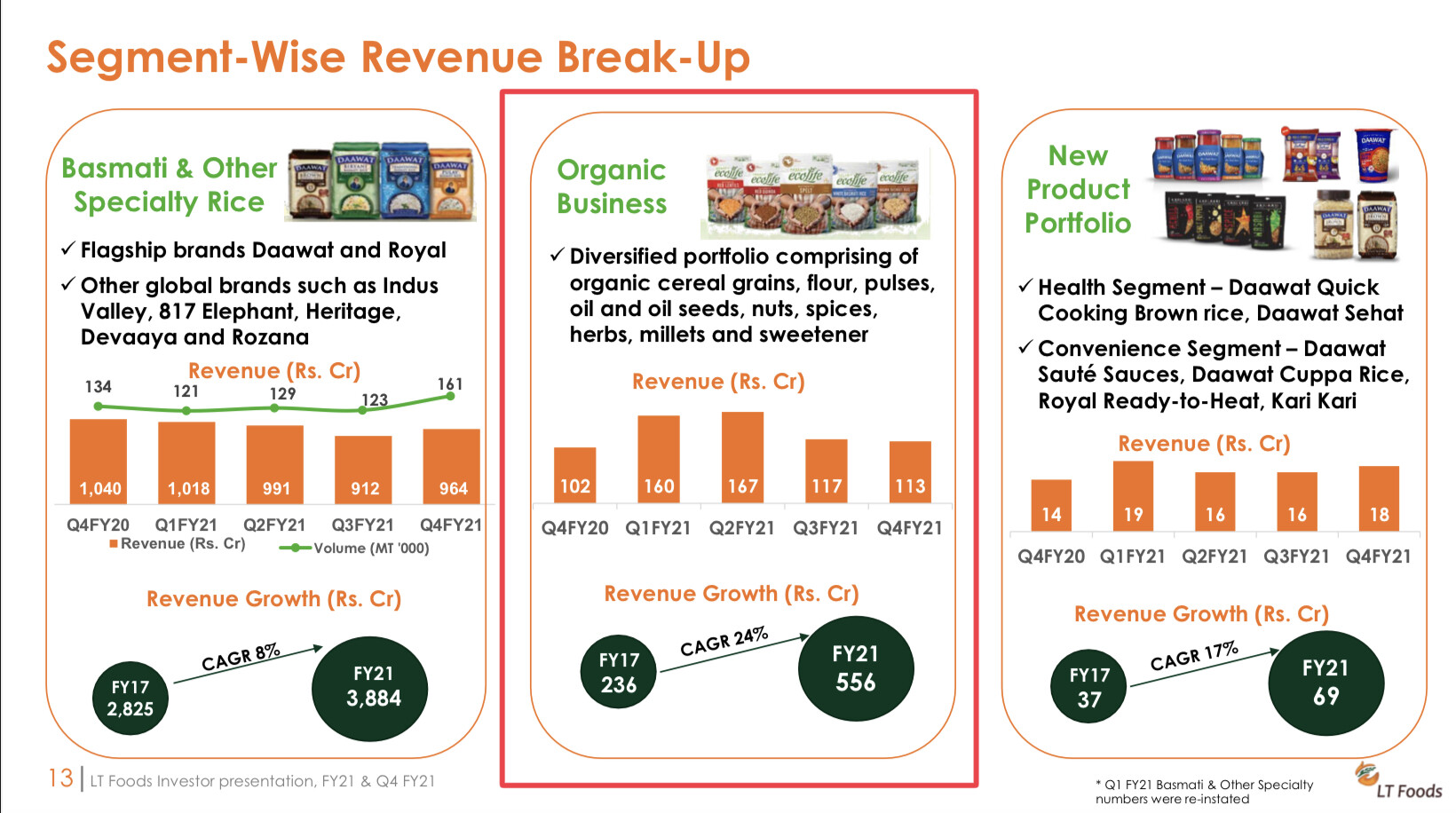

1…Rice@85% revenue@

8%cagr growth in last 5 yrs

2…Organic@9% revenue

@25%cagr

3…New products@1.1% revenue@

23% cagr in last 5 yrs

3.A=Health Segment –

=Daawat Quick

Cooking Brown rice,

=Daawat Sehat

3B=Convenience Segment –

=Daawat Sauté Sauces,

=Daawat Cuppa Rice,

=Royal Ready-to-Heat

=Kari Kari

…

MOAT

1…Strong Supply chain and Robust Global Distribution Network

2…Strong Brand creation

3…Basmati is commodity but not like sugar etc as area of cultivation is limited (g.i protected)

4…High entry barrier

5…Dull Industry does not attract much competitiors

=As basmati industry require huge inventory and thus it is huge working capital intensive business

…

FUYURE GROWTH

1…Strong Supply chain and Robust Global Distribution Network

=LT Foods transformation into an FMCG company requires a strong distribution network. The company

has over the years built an extensive network of distributors and retailers in the domestic as well as

global market. The company serves its customers through

=1,18,000 retail outlets in India,

= 7,200 modern trade channels including hypermarkets, supermarkets, Cash n Carry etc and

=all leading e-commerce platforms.

= 800 distributors across the globe out of which more than 700 distributors are in India and more than 100 distributors in the overseas market.

=The Company also aggressively scaled up its presence in the food service and HoReCa segment, with more than 2000 new accounts comprising restaurants, Biryani chains, Star Hotels and caterers

= Recently, LTF has digitized its supply chain network which led to further improvement in vehicle turn-around-time to 14 hours from 36 hours, while the loading time to trucks have improved to 2 hours from 6 hours earlier.

= The implementation of advanced automated systems and daily systematic operating procedures review has further streamlined the operations.

=The Company’s strong distribution network is a

testimony to the Company’s sustained fnancial performance, year after year.

=In India, we beneft from our strategically

Strong Supply Chain & Global Distribution Network

= In key International markets of the USA, Europe and Middle East, we have established our distribution centres to maintain adequate stocks to ensure

sustained business activity.

=We enjoy a reliable association with renowned and leading logistic companies to ensure effciency in

our distribution process

2…Strong Brand

=we lay constant emphasis on our brand building initiatives to sustain consumer loyalty and limit opportunities for competition.

=Relying on a solid reputation, excellent brand recall and a commitment to consistently deliver value, LT Foods today has securely cemented its position as a global leader par excellence.

3…USA BUSINESS

=Royal’ was worth $35 million when we acquired in 2007.

=Today, we have grown the brand at a 3-year CAGR of

20%, with Royal remaining the largest selling basmati rice brand in Americas.

=Company recently launched into the ready-to-heat (RTH) segment. Since launch, the business has achieved roughly 30%

= We have also widened our product portfolio, that now comprises of rice variants like Jasmine rice, Arborio rice, Wheat four and Ready-to-heat rice,dawaat

4…Middle east Business

=Middle East accounts for ~45% of the world’s total basmati rice consumption and around 9% of the

total revenue share of the company

=. To further strengthen its footprint in lucrative Middle East markets like Qutar, Oman, Bahrain,

UAE, Saudi Arabia and Kuwait, LTF acquired “Gold Seal Indus Valley” and “Rozana” brand from HUL in

FY17

=Post the acquisition of ‘Gold Seal Indus Valley’ and ‘Rozana’, we are now among the leading basmati rice player in several Middle East countries.

=The acquisition of 29.91% equity stake by Saudi

Agricultural & Live Stock Investment Company(SALIC) marks a landmark moment for the Company’s

corporate journey in Middle East

5…Europe Business

=Lt foods has set up manufacturing facility in Rotterdam, Netherlands in 2017

= . The region has recorded more than 80% YoY growth in its revenue that stood at ₹468 crore in FY 19-20 which has been surpassed in

the 9MFY21 with record revenue of ₹590 crores and PAT of ₹15 crores. Despite macro-economic

challenges, the Company registered a healthy EBITDA margin of 3.6%.

= The company has a manufacturing facility in Rotterdam, Netherlands that will help them save on heavy import duty on white basmati rice.

=NBFL has recently acquired 30% stake in Leev, Netherlands through its subsidiary Nature Bio Foods BV.

= LTF has expanded its reach in new countries and also expanded to new customers such as Jumbo with more than 600 store supermarket chain in Europe.

=The stringent food, safety and quality norms in the

region, conventionally creates a strong entry barrier.

=However, with our strong Sustainable Rice Platform (SRP) program, quality standards and extensive distribution network, we continue to deepen our presence across many countries in Europe

6…Organic Food & Ingredient Business

=Company has launched various agro based products under the brand-EcoLife which is well accepted in the market

=With over two decades of existence

and experience, NBF/NBFL now

partners with 80,000+ farmer

families across India, to build

enduring relations with farmers

with over 118,000 hectares of

certifed organic land in India

=frst company in India to be

conferred with the coveted CII

Food Safety Award in FY 2019-20.

=NBFL

has recently acquired 30% stake in Leev, Netherlands through its subsidiary Nature Bio Foods BV.

=This acquisition will enable LTF to supply its organic ingredients to Leev and capitalize on

its strong consumer base of more than 2500 stores in Europe.

= The organic business has a high entry

barrier as it requires around 3 years of cultivation through organic methods to produce pure organic

harvest fit for consumption and distribution as an organic product.

7…New products

=LTF has recently launched its health and convenience product range which includes products such

as

A…health segment

=Daawat Quick Brown rice and

= Daawat Sehat under the

B…convenience segment.

.=Daawat Sauté Sauces,

=Daawat Cuppa Rice,

= Royal Ready-to-heat and

=Kari Kari under the Currently,

…the new product portfolio accounts for only 1% of the total revenue share, however, the company is planning to take this share to around 12%-15% in next five years.

= All the products have

performed extremely well in the initial launch stage and the company is in process to scale up the operations

A=Cuppa rice

Cuppa rice is also gaining a good traction in

the market and now the company is planning to expand this product to a full scale plant. Currently,

the cuppa rice is majorly servicing the railway demand, where they are receiving repeated order

B=RTH(Ready to heat)

Other product in this segment is the Ready-to heat (RTH) products which have established a good

presence in the US market. The ready to heat business under the brand Royal, which is about 70% of the

total RTH sales have almost doubled in the first half versus year ago. RTH continues to gain new listings

and new distribution in already listed chains and does well for LTF to maintain its business growth in the

future. The company is driving more trial and consumption with the launch of new flavors to continue

RTHs broad appeal across consumer ethnicities. Currently, almost 65% - 70% of the new products is made up by the US ready to heat product

C=Dawat quick brown rice

The Company’s Daawat Quick Cooking Brown Rice – has emerged as the fastest growing product in the new innovations segment.

D=Dawat sehat

The introduction of Daawat Sehat in 2019-20 marked another achievement in our legacy of innovations under health segment. Fortifed with iron, Vitamins and

Folic Acid, this product highlights the Company’s undeterred commitment to develop a need based product portfolio.

E=saute sauces

The Company’s range of saute sauces, available in

5 different variants, also captured a signifcant market share during the year under review.

F=Kari kari

After the successful launch of Kari Kari in the previous fnancial year, the Company has set-up a Kari Kari manufacturing unit in Haryana with a production

capacity of 3,000 units per day

8…QUALITY AUDIT

Sustainable Rice Platform is a UN Environment and International Rice Research Institute initiative.

=It has instituted a third-party audit to certify cultivation in sustainable ways

=. LT Foods is among the best growing

companies as per Sustainable Rice Platform standards

=Our srp scre increased from 80 to 96.1 in 3 yrs

=We conduct audits by certified institutions to ensure compliance to globally defined quality and

safety standards.

= We comply with all leading import standards, as

specified by FDA, CFIA, EU, GCC and SASO.

=Our facilities are also regularly audited by global retail

consumers to ensure compliance to international country specific standards

9…Cost efciencies Having control on the complete

value chain gives LT Foods an edge over its competitors. Staying cost conscious at every

step of the value chain has helped the organization to stay competitive in its space

10…Basmati is commodity but not like sugar etc as area of cultivation is limited (g.i protected)

…

RISKS

1…Susceptibility to volatile raw material prices and regulatory changes

=LTF starts the paddy purchase in third quarter and stores it for the rest of the year.

=Being a commodity,

the prices of rice and paddy are susceptible to factors like supply, demand, rain and availability

of healthy land.

=The company usually enters into an understanding with customers for supply of

rice, though this is not binding. Hence, exposure to risks related to any steep decline in paddy

prices, subsequent to procurement, remains high.

= Additionally, exports of agricultural commodities,

including rice, are highly regulated. However, having strong brands, wide geographical reach and

sourcing capabilities have helped the group maintain profitability.

2…Foreign Exchange Rate Risk

=LTF derives 65% of its revenue from the global market making it susceptible to exchange rate

fluctuations. However, the company has put in place a well-framed hedging policy that mitigates

any potential risk due to currency volatility and cause a financial impact.

.3…Competitiors

=In India, there are few major branded players in the Basmati rice business which dominate the local

as well as the export markets. The major peers of LTF in the organized sector include KRBL , Kohinoor

foods, Amir Chand Jagdish Kumar (Export) Ltd, Sarveshwar Food, Misthann Foods Limited, Adani

Wilmar Limited, Amira Pure Foods Limited, Dunar Foods.

=The leading packed rice brands are India Gate, Dawaat, Kohinoor, Golden Harvest and Aeroplane.

=Private label brands like Big Basket, Amazon, Flipkart, and Grofers are trying their hands in this sector plus the edible oil sector like Fortune brand have started penetrating in this sector.

4…Iran sanction

Recent US sanction on Iran has created a rift between the Iranian and Indian government with the

end of oil imports from Iran to India. Iran expected India to be more resilient to US pressure and has

expressed disappointment over India for taking up US orders so easily. As a result of this displeasure,

Iran is planning to stop import of basmati rice and other food products from India (however, there are

exports still going to Iran). Iran advised India to take actions that meet the interests of both countries.

On the other hand, Iran is set to improve trade relations with Pakistan (second largest basmati rice

producer in the world). The Indian exporters and farmers will have to bear the consequences of the

trade relations between the nations

5…contingent liabilities…65 cr

6…Geopolitical Risks

LTF is a global rice company having exports in more than 60 countries. Any geo

political tensions

between major economies can cause supply & demand glut in turn affecting the prices of raw

material and final products

7…Multiple subsideries and few acqusitions.

However all acqusitions are in same business line.

…

FINANCIALS

1…AVERAGE ROE

5yrs@12.8

10yrs@13.8

= Roe of last 5 yrs was low due to QIP and huge capex done

=ROE will improve in coming yrs as there is only maintenence capex in near future

2…D/E ratio

Continuously decreasing since last 5 yrs

2021@0.86

3…CAPEX

=520 cr capex in last 5 yrs

=No future major capex except maintenence capex of around 70-80 cr

4…Operating margin @10-12% since last 9yrs(relatively stable)

5…fcf% …capex

2020…9.3%…89 cr

2019…(-)…120cr

2018…(-)…239cr

2017…4.5%…80cr

2016…8.1%…54cr

2015…(.-)…55cr

2014…1.9%…54cr

6…Growth rate(average)

SALES GROWTH

5yrs@9.39%

10yrs@14.28%

PAT GROWTH

5yrs@21.30%

10yrs@21.97%

Disc…invested