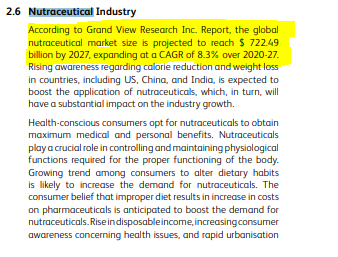

There is a very good runway for Indian Nutraceuticals for the coming few years as specified in the tweet above.

Laurus has mentioned about their capabilities in the segment multiple times in the AR, but has not quantified or put up numbers regarding it.

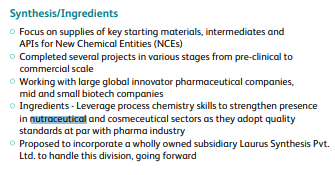

Snippets from Laurus AR 2020:-

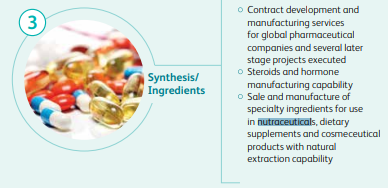

According to the AR, they manufacture “speciality ingredients” for nutraceutical companies.

This is part of their Synthesis division.

Nothing was spoken about this segment (nutraceuticals) in the concall.

Can we assume APIs being the major growth driver for the coming few years, this will be a dark horse or something that can produce a positive surprise?

The drugs losing patent exclusivity in 2020 and in which Laurus is present as mentioned in list provided by @Raj_A_A

Truvada… This contains a combination of emtricitabine and tenofovir. (combination used for HIV treatment and sometimes as pre exposure prophylaxis)

Atripla… This contains a combination of efavirenz, emtricitabine and tenofovir. Again used in HIV treatment.

Interesting thing in both these drug combinations is that Laurus is a very strong player in anti Hiv (anti retroviral) drugs and can act as one of the lowest cost producers because of the scale and experience it has in manufacturing these drugs.

We will have to see how it uses this opportunity and monetises it. ( it can go with a partnership model with some big player or market on their own… )

Wonderful explanation. Path of value migration from API to FDP was taken by Granules & similar problems of pledge, doubts about management was there leading to undervaluation. Now we can see the catch-up in valuation in Granules. Many road maps are there for Laurus management, let’s see what path they take. Gross undervaluation may not be there as pharma cycle is in uptick. Thanks Dr Hitesh

Truvda sales of 2018 for Gilead in US were 2.6Bn $. So, opportunity size is quite big even considering for 50-60% price erosion.

However, Gilead is planning to migrate from Truvada to Descovy and is expecting that around 2Bn $ revenue can be transferred. Any thoughts on this?

Atriva US sales are 500Mn$ + and worldwide sales are 3Bn $+ Again, huge opportunity size. Here, Teva has made a pact with Gilead for launch of generics. Let’s see if Laurus can become the API supplier/CDMO manufacturer?

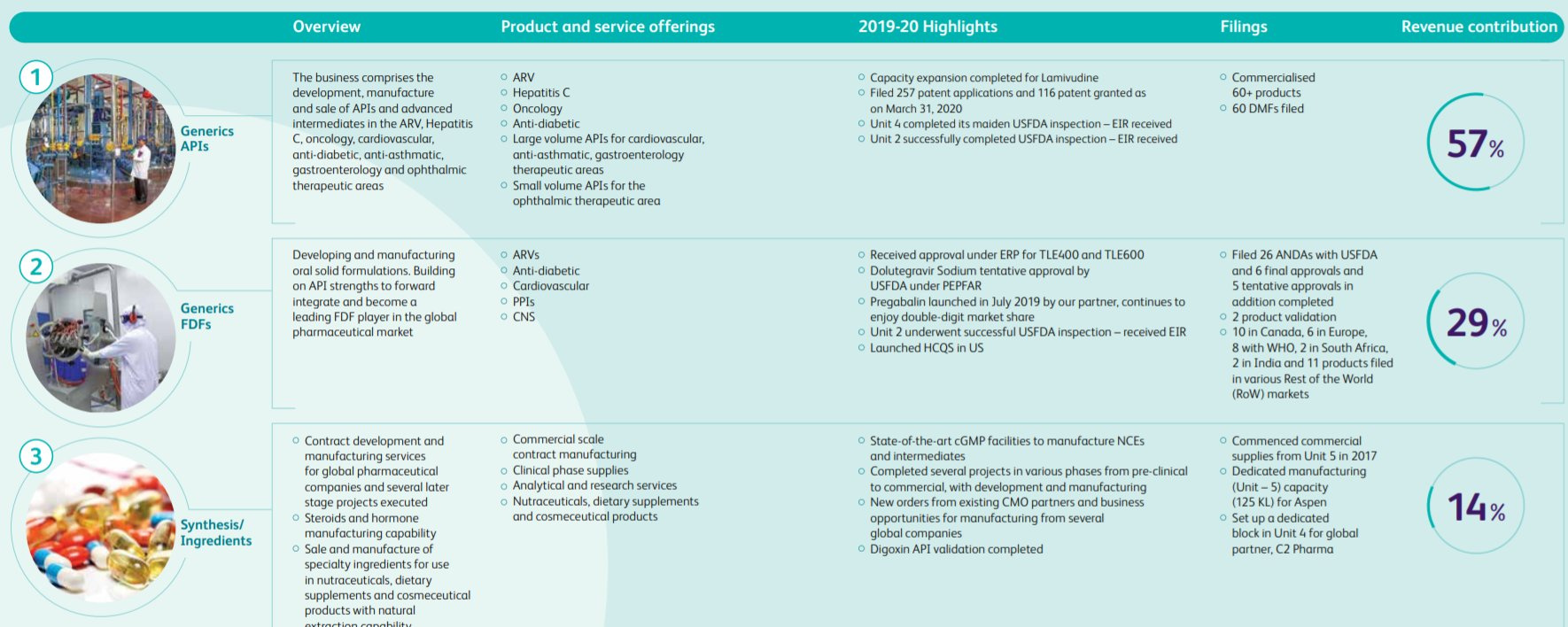

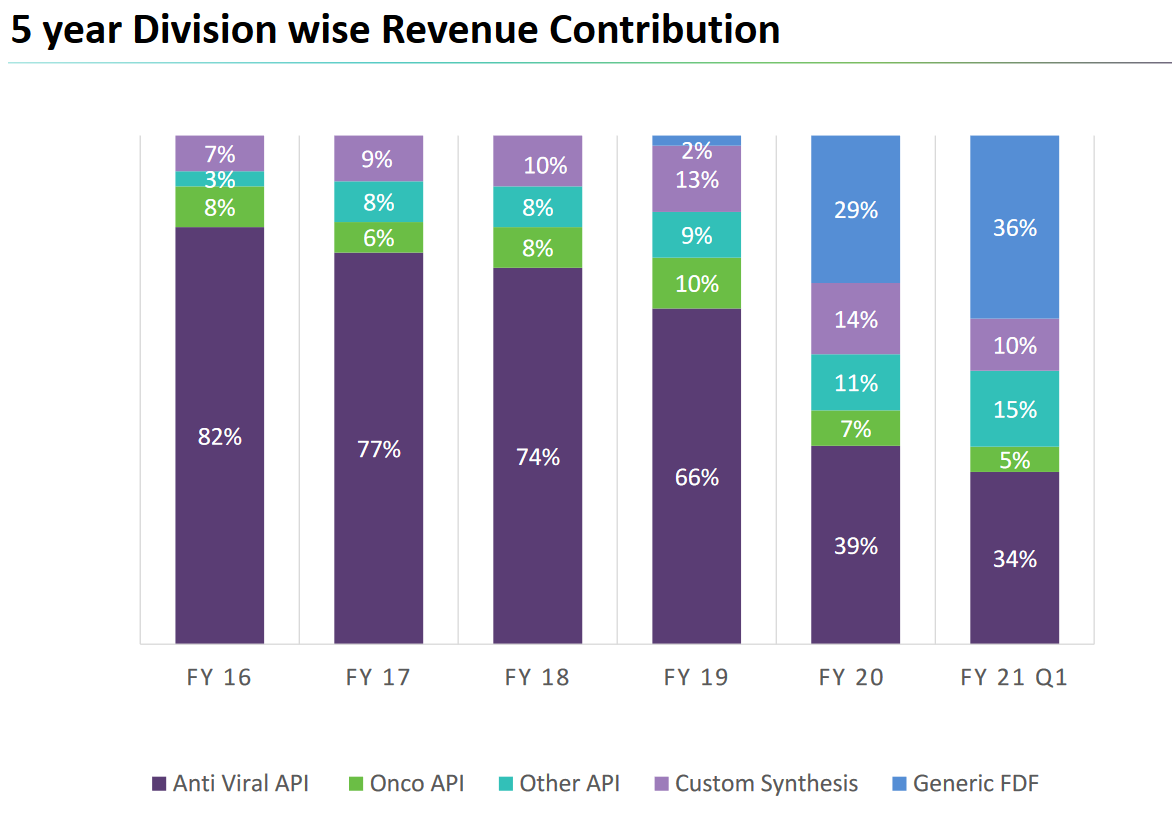

Laurus Labs:

It is a combination of API (57%), Formulation (29%) & CDMO (14%).

The basics of its business model is beautifully explained in a single page in its AR

As per my understanding the revenue of laurus labs is more tilted towards HIV related drugs. What will be its future when the HIV gradually diminishes or if a vaccine is invented?? isnt that a risk?

Disclosure: I’m invested in laurus since 700 levels

Only a risk if one has put his life savings in the company and sleeping quietly. Hardly anybody will do that, except maybe the promoters.

Further, with the kind of expertise Laurus have it won’t take longer for them to switch their focus to other kind of disease.

And HIV Vaccine is in development since 1984 and the work is still undergoing. If a vaccine is finally developed it will be a more than welcome thing than being considered as a ‘risk’ in the broader sense.

As of now the formulations are all anti viral. But Laurus is trying to diversify there as well, so ARV depandance is still 70% if I am not wrong. The formulations capacity expansion (abt 80% increase from current capacity) is all for non ARV. I believe over 5 yrs, Laurus will have very less dependence on ARV, by growing oncology, CRAMs, neutracuticals etc.

Few interesting observations from balance sheet / cash flow statements (relying on screener.com for break up)

For FY 14 to FY20:

Cash flow from operations ₹1557 cr

Fixed assets investment/ capex ₹ 1546 cr

So hardly any cash flow after capex. - first observation.

Debt plus equity raised ₹1500+ cr (from @Sivachander_Shivaji post). Associated cost ₹100 cr interest, plus repayments as and when due. Plus, Dividend, if any. - Second Observation.

Working capital changes are always negative I.e. business is using that much cash . This most probably linked to high growth phase, but we have to keep this in mind going forward.

Total cash used in wc ₹ 691 cr - third observation.

There’s hardly any cash left at the end of the year, I’ve personally seen very few balance sheets with such thin cash balance. And mind you, they hardly have any current investment.

So, what would they do if there’s any urgent need of cash? Most probably, they would use wc lines / od etc which will certainly cost them some interest. I’m not sure of reasons for such a strict cash management. Is this VC mentality ( Warburg Pincus?). Fourth observation.

You are right. Few weeks back I exclaimed by looking at their cash equivalent (80 lakh) comparing to the employee benefit expense (323 cr). Wont they have coming month salaries in thier books ?

Disc: Invested

The promoters released pledged share just before the release of q1 results and the results were excellent, but it seems promoters added additional euphoria to the share by releasing pledge. We may call it manipulative behaviour of promoters also. Better be some what cautious in this counter.

Releasing pledge and re-pledging with latest stock price means in absolute term loan amount has increased. As promoter is releasing pledge and another financial instituting is willing to give him another loan that means they find promotor credit worthy and they also find underlying is sound. So far I believe promotor is able to balance this well. This will be a concerning factor only if company stops growing and pledging keep going

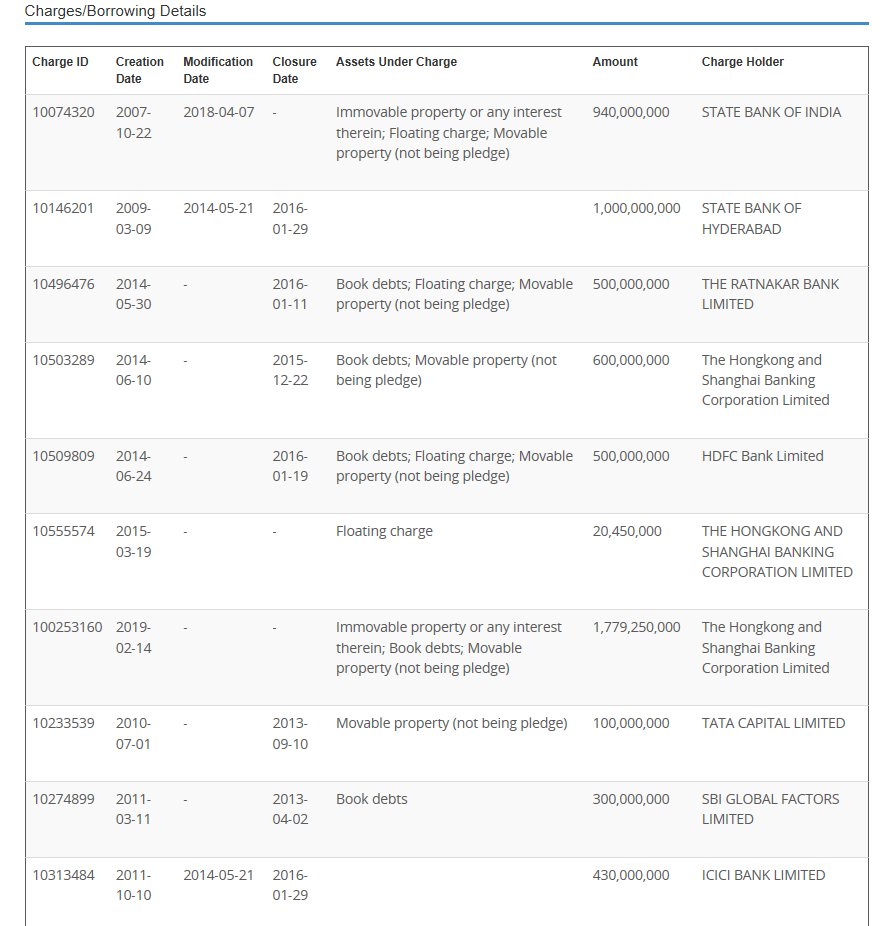

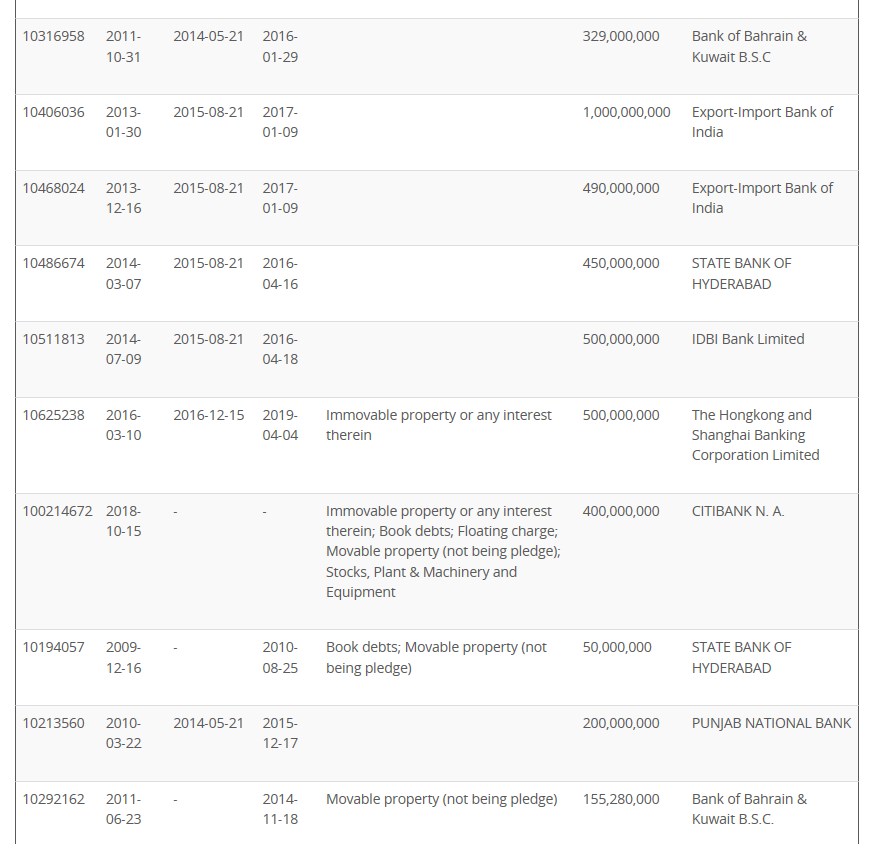

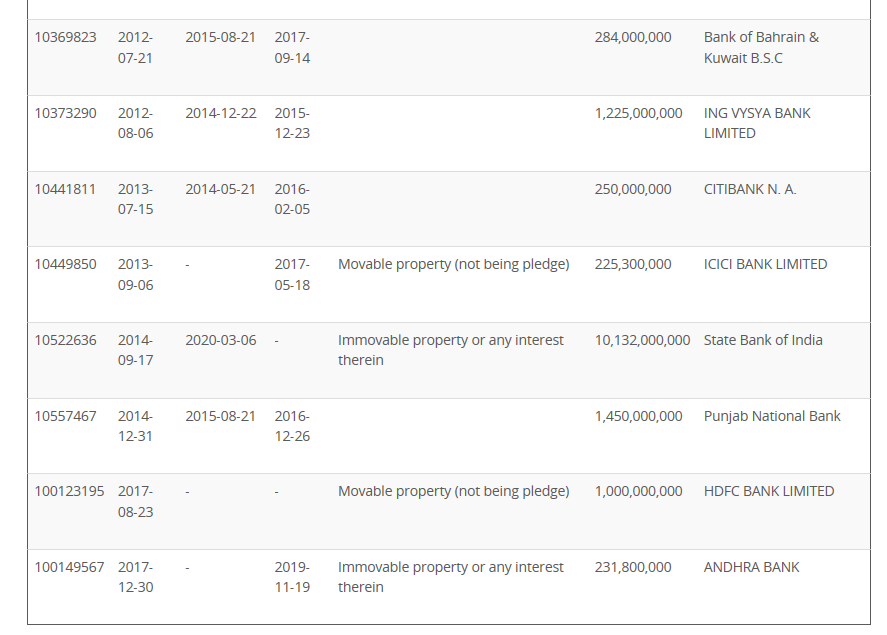

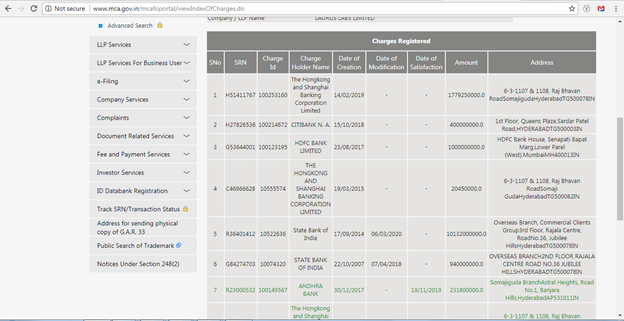

The various charges i.e loan taken by the company is found from below

Isn’t this taking loan from one bank than revalidated or refinance from other bank … I am not gone deep in detail but could someone help me to interpret this …

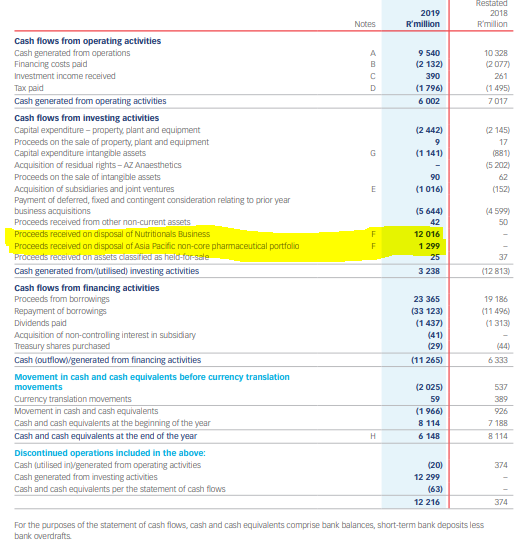

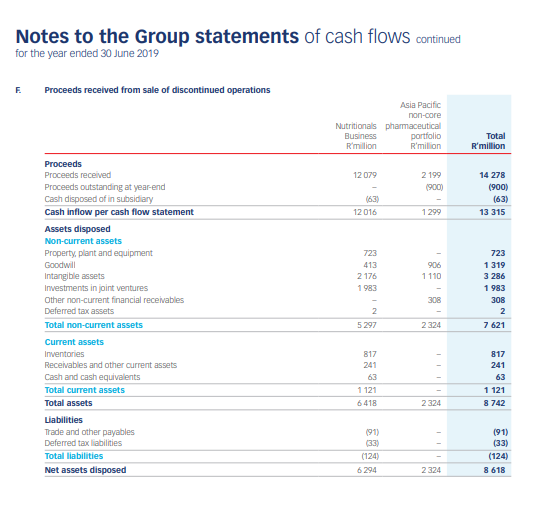

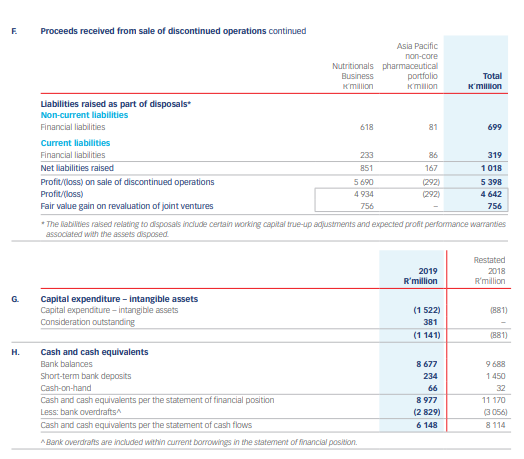

I might be wrong here : am ready to stand corrected - does this mean 50% revenue as it did receive as a beneficiary benefit of aspen selling/disposing of certain set of their business?

Was trying to understand how much key starting Raw material (as % of total raw material requirement) Laurus is importing from China for manufacturing it’s API’s?

This would indicate to what extent it is backward integrated and in case of a disruption in supplies of raw material from China , what would be the impact in its revenue?

Discl: Invested and wanted to add.This is not a buy or sell recommendations. Please apply due diligence before investments.

Being from the Corporate Banking domain, I can try to provide some clarity. MCA(Ministry of Corporate Affairs) site has a page called “index of charges” which shows charge created by banks on the assets of a company against the loans given. This(plus other reports) help a bank check and reconfirm exact loans taken by a company from other banks.

As per current MCA website, Laurus Labs has Loans from HSBC, Citibank and HDFC. Loans from Andhra Bank have been closed in 2019(along with one loan from HSBC), plus other banks’ loans clsoed earlier. This does not necessarily mean refinancing. The company might just be looking at lower interest rates which another bank sometimes offers, or better services.

There is a lot of debt on the balance sheet, and not a lot of cash. Any lender(bank) looks very minutely at this, while investors usually overlook this in a growing stock citing growth prospects coming from capex. Many firms eventually go down due to debt, and this figure is finally looked at by investors when things start going wrong. You can take any example - ADAG, Jet etc. This is also why debt free companies/MNCs command a higher PE ratio sometimes.

Releasing pledge and pledging with latest stock price(If I’m understanding correctly that this is what has happened) is not a good sign as per me because(if I understand correctly), there was a smaller loan amount due to a lower stock price and as soon as the stock price increased, the promoters took on more loan in accordance with the increased price(and increased security amount being provided). While the lender in this case might be gung ho, I doubt someone lilke Uday Kotak would have sanctioned such a loan. In case the stock market crashes and MTM hits, there is trouble. This is what happens with a lot of pledged loans and should be a red flag(If in case this is what has happened here) if a loan has been taken against a pedge of shares at a very high price. The lender will ask for the difference in money as soon as the share price drops and the promoters have to pay up. In fact, this is exactly what happened with Rana Kapoor.

I am nowhere close to having any great knowledge about this domain, but this viewpoint is only from a debt perspective on a balance sheet.

The latest date of pledge creation is feb 2019. Can you provide any recent details about pledge creation/release, since you seem to be privy to MCA data, and know more than most about the subject?

Would be interesting to see where things stand now.