Q1FY21 Results.pdf (646.3 KB)

Not sure. But you are seeing decent valuation for Laurus as it is growing much faster than the three names you mentioned and so PE gets reset after each quarterly results.

Q1FY21 Results.pdf (646.3 KB)

Not sure. But you are seeing decent valuation for Laurus as it is growing much faster than the three names you mentioned and so PE gets reset after each quarterly results.

Does anybody know whether Laurus has the capabilities to manufacture Metformin Extended release tablets? If yes, are they already selling them? Google search says Laurus sells normal Metformin tablets.

Discl: Invested

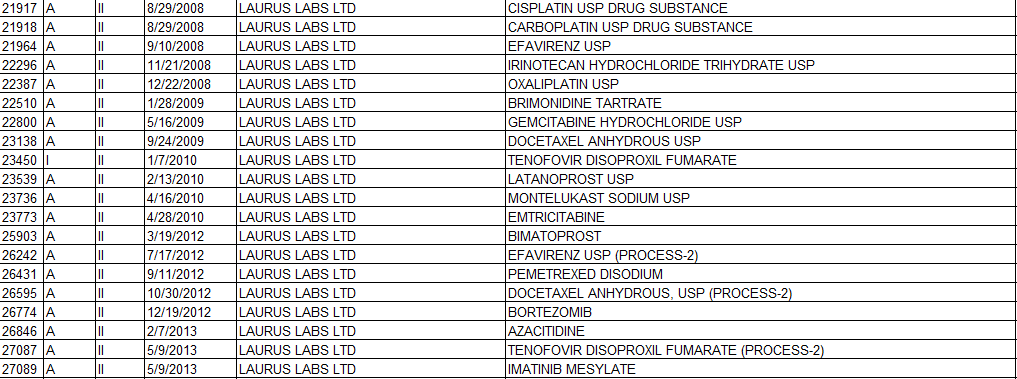

The link points to Drug Master Files (DMF). DMFs can be active or inactive. What is DMF? According to FDA, this is the answer.

I didn’t get any impression there is something like active drug.

More on keyman risk.

Con call transcript Q1 FY21:

Hello boarders, in the call, the management said that they have acquired stake in the South African company Aspen for 70,000 Rands (which comes to about 3 lac INR).

Can anyone confirm the nature of this deal? The amount seems too less (while acquiring a company).

As per reports last year, they have agreed to acquire 100 % stake in Phekolong pharma, a subsidiary of Aspen.

Does anyone find any flags with the value of acquisition?

Disc: Invested

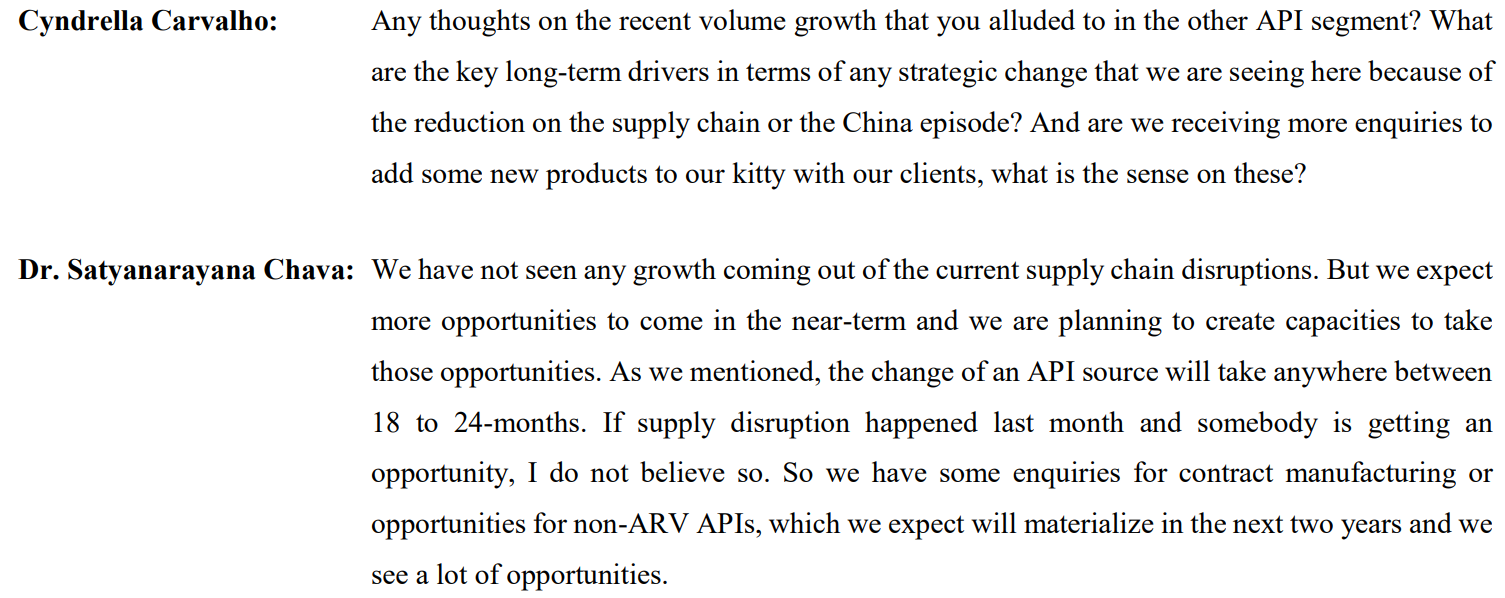

The jump in pharma sector (API esp.) as a whole is a bit difficult to understand, Dr Chava below is saying it is not related to China factor at all, and that is not possible as per him in general.

So the other possibilities remain:

At least companies are not doing panic buys as per Laurus CFO!

So, the only possibility remains some (temporary) element of demand growth led by end users, else this is long term structural, helped in a bit by rupee depreciation.

The explanation for the API structural is (in part) China substitution which has been likely planned for in the capacities added by the Indian manufacturers.

Note - for pharma in general this is perhaps not the best place to discuss. Though there are remarks of a fresh batch of off-patent drugs expected, from views of an analyst I read somewhere, together with the maturing of Indian investments in developing markets, now paying off.

This is in complete contrast to what Divi’s said in the concall I quote from Divi’s thread. @YachnaBhatia

Yes, Divi’s is likely correct, Laurus guys are I think only answering about “China episode” (border conflict) and the customs delays surrounding that! (they mention 1 month time-line too).

The overall China substitution play is structural and will take much more time to play out.

Some players are in better position to ride the tailwinds having shown steady growth trend anyway for past year or so and growth plans already in the works. (mainly APIs)

Even neuland lab management suggested along similar lines of what Dr Chava suggested. It takes 1.5yrs to 2 yrs for the process of change of API supplier by formulation company (part of it could be need for reapproval of FDA). So, Dr Chava says there will be opportunities 1-2 yrs down the line and they are planning capacities for capturing some of those.

Discl: invsted in Laurus (very basic knowledge in Pharma)

Are international pharma major sourcing API’s from India, if available and avoiding Chinese API? Do you know for sure this is happening?

Are Indian pharma majors sourcing API’s from India, if available and avoiding Chinese API?

Can Indian API manufacturers compete with Chinese counter part either in quality or price?

I don’t have have credible news items saying API shifting from China to India. I am really surprised looking at the results of API manufacturers because nobody had a slightest clue about it before hand.

I just have results and Divi’s and Laurus answers to base my (qualified) opinion.

Yes, it was a surprise, likely no body expected a big backlash against China.

China substitution or China+1 supply chains are to be expected though.

It takes time for such huge volumes to shift is understandable hence the Long term.

Divi’s is also not saying anything definite, gives us options about what the reason might be, I would think it is the lower demand at play here and not the lack of manufacturing ability. (after all Q1 period was much better for China than Q4)

Laurus says they getting inquiries (non ARV API) and will expect materialization in medium term. (about 2 years)

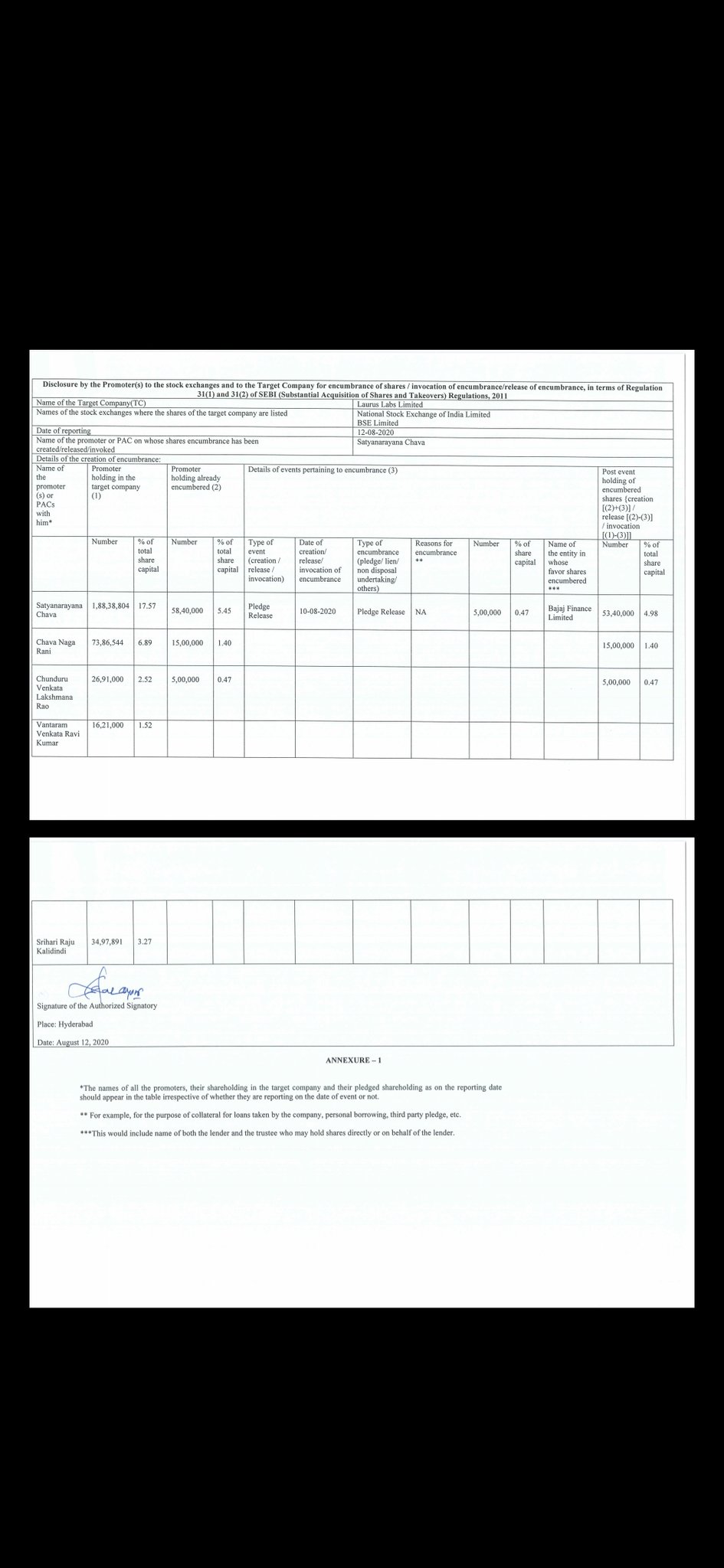

They have released the pledge from Bajaj Finance and repledged the shares with Tata Capital

Could you kindly list the salient points as some of us do not have the subscription of ET

I think one has to think about laurus labs journey as a continuous process, a part of Dr Chhava’s life. He used to work for Matrix labs and is a specialist in the pharmaceutical field.

Now if you want to start a pharma company, and don’t have enough capital, you have to partner for investors who are ready to fund the company and its growth. So he has had to dilute his personal stake in the company in order to start his company and see it grow.

He might have had a choice of sitting content with a company with turnover of 500 crores and profits of 50-60 crores and enjoying a comfortable life. But someone obsessed with growth will not be satisfied and would want to grow the company into a much bigger entity. There were live examples in front of him in the form of divis etc in the same geographical location. This would always serve as an encouraging example for anyone wanting to see a dream and pursue it.

API business is the basic building block in pharma field. Once a certain scale is achieved in api, there are two choices. One is to take the path less travelled as in case of divis where you stick to the api space, build long term relationships, build huge scale in such a manner that very few people can compete with you even on a global scale. The other frequently travelled path is to move forward into finished dosages, and enter into contract manufacturing services and partner with innovators and take the molecule from its infancy to clinical launch and continue supplying that molecule to innovator till patent expires. Post patent expiry, one can launch the molecule in US market itself after having got ANDA approval (or in case of API, DMF approval and be a big supplier to the new incumbents).

In case of Laurus, the move from API to finished dosages was littered with problems for a few quarters and that came to the fore post its listing. Once these initial teething problems resolved and things got on track, as we can see since past two quarters, there has been no stopping the company.

How far the journey can go is a question investors need to figure out. One way forward is to continue to grow FDF business which is a high margin business for the company. An additional way could be to launch directly or with partner in US markets by filing and getting approvals for ANDA. Here the product selection matters a lot. Company ideally should be fully backward integrated to be able to suceed from modest backgrounds in the US markets. Plus the molecule itself should have a long runway and preferably low competition.

Laurus seems to be somewhere halfway on the journey and how things go ahead needs to be seen. The company still remains in the growth phase with continuous capex and hence will continue to need funds to grow. How prudently it grows will determine its fate. There are examples of companies that have suceeded and made it big and others who have blown it and gone bust. I would keenly monitor the growth plans and how they fructify and how profitable they are and take an appropriate call.

The matters like slight increase and decrease in pledge (often people jump the gun without fully understanding whether pledge has increased or decreased  ), intraday movements or short term movements etc should at best be relegated to less important things to monitor. If one is a trend follower, better look at the pattern of higher tops and higher bottoms on daily or weekly time frames to see how trend is shaping up.

), intraday movements or short term movements etc should at best be relegated to less important things to monitor. If one is a trend follower, better look at the pattern of higher tops and higher bottoms on daily or weekly time frames to see how trend is shaping up.

For those who want to go into detals, Donald is not getting into the deep end of the business dynamics, so part of the job is getting done.