@Himanshu_Nigam

Are you sure, this is exactly what happened with Rana Kapoor! I am afraid you are mixing this inappropriately. IMO, Rana kapoor saga is full of pre-planned scam and loot of depositors money in collusion with like minded corporates with full knowledge that money shall not be recovered and engaged in quid pro quo kind of transactions. His act was commissioned infront of independent directors, SEBI, RBI, FM et. al and when damage was done beyond repair the govt showed some action to sooth grieved depositors. I am doubtful about your inference in Laurus considering Rana kapoor deed.

Please enlighten some more details about your doubt and source of information in case of Laurus so that many of us can be benefited.

Sir, the reply on pledge creation was to the post by prashantrane2000 and vikky9995, and hence I had mentioned 2-3 times, that “if” this is the case Please do not take it otherwise. I am only aware of how details of corporate loans can be found out. The last charge creation date of 2019 is for the loan the company has taken from HSBC and does not mention anything about share pledge etc. and hence I have clarified that my observation holds “only if” loan amount has been increased by the promoters basis share price increase.

@Vijay_Kiran : I mentioned the example because Rana Kapoor’s shares got sold in the open market due to MTM issue. If someone takes a loan against shares, it is at a certain price, which is taken as the security value. If the security value reduces due to reduction in share price, the lender usually has conditions asking for repayment, because the value of security has diluted compared to the value of the loan.

Your message regarding loot, scam etc. are pertaining to an entirely different topic while I was only referring to the loans Rana Kapoor had taken against the pledge of his shares.

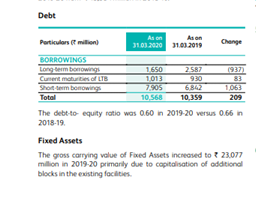

I will stand by what I mentioned about high debt. March 2020 has Borrowings of INR 1057 Cr on a turnover of INR 2832 Cr.(as per screener) Since the last charge creation date is for 2019 it shows no further debt has been taken and turnover will obviously increase. Assuming that turnover is 4000 Cr in Fy21 and debt is same at 1057 Cr it will be 25% of total turnover, which as per my limited understanding is high, and this becomes a problem if/when a firm faces a tough situation.

Please note again, I am not knowledgable about the domain and I don’t have anything against the company or the stock. My observation was only basis what I have personally seen what happens in companies with high debt. Laurus might well grow so much that they become debt free in the near future.

Great information for retail investors & thanks for helping us finding a way to get trusted info directly from MCA website.

I did a check for certain other companies (mainly because I own shares of them) & wanted to cross check with their Annual Reports / Management commentaries related to same topic. I did find big difference.

Now I am in doubt if I trust the management or find the reason behind this big gap.

I request your help in understanding it better as I don’t have any background of finance. Say if company A has taken a debt of X Cr on 01-01-2019 & paid back Y Cr on 01-04-2020, what does MCA webpage show…

i) it keeps showing X Cr as debt or it gets updated to (X-Y) Cr

ii) If it gets updated with (X-Y), what is the cycle of update… quarterly / annually etc

Hi, while this might not pertain to this thread, let me confirm since this has been asked here:

Management of listed companies will not mislead investors because anyone can pick up data from MCA. So there should never be a difference between data on MCA and the balance sheet. It can only be due to delay in updating MCA by one of the banks or a mistake in checking the data. In case a bank finds a mismatch, it is due to procedural issues and the company/other banks rectify it.

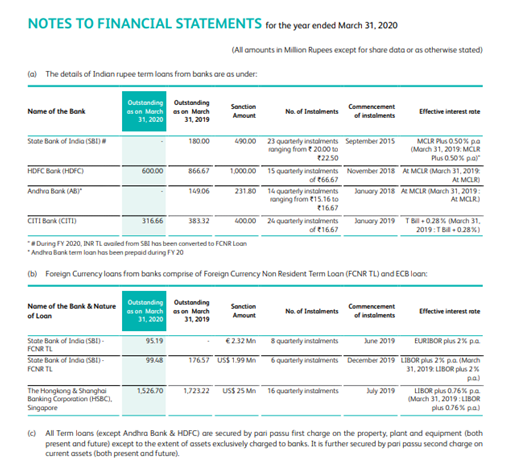

If a company has taken X loan from Bank1, there is a particular charge created against X loan from Bank1. That particular loan charge is individually closed when a company pays off the loan. This is why you will see multiple rows for the same bank sometimes. Eg: HSBC has a loan closed on 04-04-2019 while a new/separate loan was started on 14-02-2019. MCA website does not get updated with the total. You have to add that manually.

The only case for mismatch will happen if a loan has been taken from a bank after the date of publishing of balance sheet. Eg: If a company takes a fresh loan after March2020, this will only reflect in their next balance sheet, but the bank will update on MCA as soon as possible. This process is called ‘charge creation’. Banks create a charge on the asset of the company given as security - Current assets, fixed assets, future assets, propery given as collateral etc. So if a new bank is sanctioning a loan after March2020 they will cross check from MCA and not go only by the balance sheet. In case of laurus, there is no new loan charge created since Feb2019 on MCA, but SBI loan has been modified on Mar-2020. This modification can be an enhancement in loan amount also, which maybe explains the small rise in debt from FY19 to FY20.

For additional clarity: if 2-3 banks give loans to the company against the same securities(CA, MFA, properties), they give a Pari passu letter to each other so that they legally have the same security even through the property papers might be with one bank. This is called a multiple banking arrangement. In case of a consortium arrangement, all banks and company have a joint meeting to decide things, and there is a “Lead Bank” which takes care of most of the formalities on behalf of all banks and the banks dont have to carry out separate documentation, charge creation on MCA etc.

Current maturities are payment of long term loans due to be paid in current year

short term borrowing is for working capital.

The total shows INR 1056.8 Cr. for FY20

Screenshot from Page 62/109

So the balance sheet always gives the correct breakups. I was not able to find the breakup for short term loans, as due to lack of time was not able to go through all 100+ pages patiently. There is a need to go through MCA website only if you want to check if a fresh loan/modification has been done since the latest balance sheet. Re-iterating, no management/auditor of a listed firm will give false figures in a balance sheet about debt amounts. There can always be the rarest of exceptions.

Edit : Please also note, MCA shows sanctioned limits while the company might use only a part of those limits, also leading to a mismatch between MCA and Balance Sheet. Eg : If a bank has sanctioned 100 Cr to a company and their limit utilisation is only 50 Cr, then the March balance sheet will show only 50 Cr as Debt.

It does NOT get updated with partial repayment of loan

We can’t get current debt of particular company using this

In most of the scenarios, we will find the GAP as most of companies will payback the loan in multiple installments and we can’t get that amount on MCA webpage

Investor lawyer safir anand posted in Twitter that ambit capital in its research report said that "laurus labs is showing same traction like divis labs in its earlier days. And can be a big one. "

Where to read such research reports?? I have googled but didn’t find it . Could any one share the ambit capital research report??

Thanks.

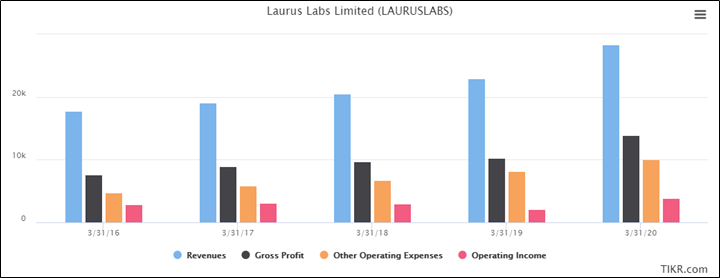

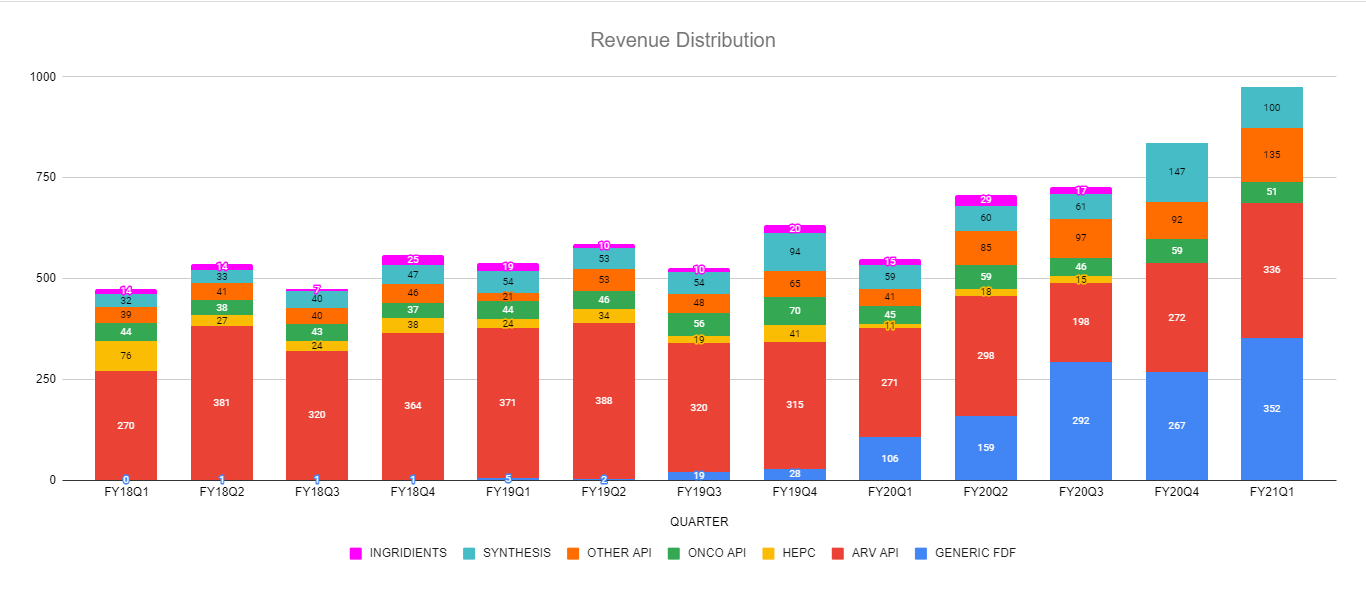

Yes that is indeed true. From the latest investor presentation (FY21Q1) it is evident that since 2019-20, the contribution from Generic FDF division has increased by manifolds. That has subsequently increased the net revenue steadily as can be seen in the Figure - 2 below.

What I also noticed is that the management has clearly written in the presentation that as part of their future outlook, they are focusing quite heavily on the Generic FDF division (more on that later) – stating that they are doubling their FDF capacity by FY22.

However, as can be seen in Figure – 2 that constantly increasing operating expense meant that the operating income from this increased revenue is yet to play out.

Now quickly focusing on their Outlook For FY21 and Beyond :

Partnership with Global Fund offers higher volume contracts with reasonable predictability in FDF Tender business – which is a good news considering the Generic FDF business has now became a major contributor to the company revenue

Have a healthy order book for FY 21 & beyond in FDF CMO business

Robust growth in Other API segment to continue on the back of higher order book visibility

Changing business mix to drive growth - Generic FDF segment contributed 36% in FY21Q1 total revenue as opposed to a mere 2% in FY19

Non-ARV API business (HepC, Oncology & Others) to contribute significantly showcasing the speed of diversification of revenues.

Scale up in engagement with Aspen

Acquired Aspen’s South African Subsidiary, in order to get a foothold in worlds’ largest Generic Accessible ARV market – shows a lot of positive intent

Acquired assets of an API Unit in Vizag to be used for backward integration and pre-clinical chemistry – once again shows that they are not going to sit pretty any time soon

All the green field expansion have now turned Cash positive in FY20 with near maximum utilization

Continue to undertake Brown Field Capex programs for Capacity addition in line with strong order book visibility and business outlook

Some other critical points which I have noted from the FY21Q1 investor presentation are below :

Generic API division showcased a healthy growth of 40% YoY

Anti Viral segment recorded growth of 19% YoY

Onco API revenue showed a growth of 13% (YoY)

Other API revenue showed a robust growth of 207% (YoY)

Generic FDF Revenue Showcased a robust growth of 232% YoY

The growth was led by higher LMIC Market volumes and increased volumes from North America and EU

RoW (Rest of the World) Markets – Received approvals for TLE400 and TLE600 from the US FDA

Entered into a long term partnership with a leading generic player in EU region for Contract Manufacturing Opportunities

Custom Synthesis division recorded a strong growth of 37%

Total Number of Active Projects in the CDMO division stood at 47 as on Q1 FY21

Incorporated Wholly Owned Subsidiary to give increased focus and eventually dedicated R&D and Manufacturing

Commercial supplies started for 4 products

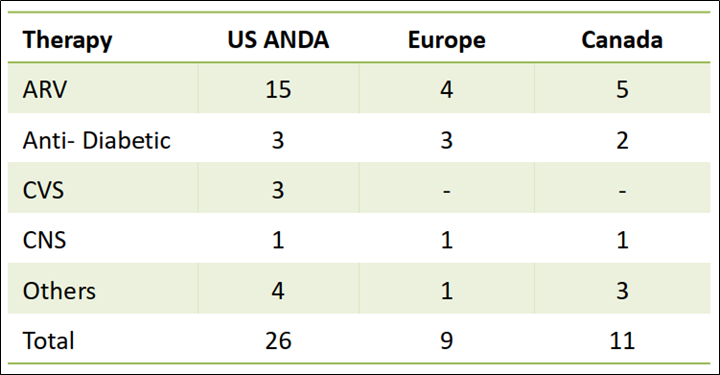

Finally let us focus on the number of fillings they currently have in their portfolio.

I have been able to assort the revenue distribution by segment from all the investor presentations available in the website of Laurus Labs.

I present the numbers in the chart below. I thought it was much easier for me to comprehend the prevailing investment thesis with this data. Hence sharing.

Bayshore Pharmaceuticals, LLC Issues Voluntary Nationwide Recall of Metformin Hydrochloride Extended-Release Tablets USP, 500 mg and 750 mg Due to the Detection of N-Nitrosodimethylamine (NDMA) Impurity

There are other competitors inline : Aarti Drugs, IOLCP, Alkem, Auro Labs, Lupin, IPCA

Am not being totally negative here - just to know, does Laurus/Granules fill in the missing gaps or is some other competitive companies has good strategy to deliver in terms of low pricing and market share?

Wanted to know in terms of Laurus pricing - definitely a rocket got a extra boost here.

The above link shows, Laurus can supply Lenalidomide, which seems to be generic name for Revlimid as per below article.

If Laurus supplies API to Natco for this, it will be a good growth driver for Laurus along with Natco. If somebody has knowledge on this part, please throw some light.

Edit: Laurus has profit sharing partnership with Natco only for Hep C. I got it wrong when I said Oncology. Apologies for misleading statements.

Please do not take it otherwise. I am only aware of how details of corporate loans can be found out. The last charge creation date of 2019 is for the loan the company has taken from HSBC and does not mention anything about share pledge etc. and hence I have clarified that my observation holds “only if” loan amount has been increased by the promoters basis share price increase.

Please do not take it otherwise. I am only aware of how details of corporate loans can be found out. The last charge creation date of 2019 is for the loan the company has taken from HSBC and does not mention anything about share pledge etc. and hence I have clarified that my observation holds “only if” loan amount has been increased by the promoters basis share price increase.