The results have been beyond my wildest expectation. The exciting part was - other than Forex - there does not seem to be much of a one off element and these numbers are sustainable.

2/3 things I found very interesting -

The gross margins moved from ~50% to 54%. Out of this, 2% was due to Forex gains. Other 2% was due to process efficiencies and efficiency in procuring raw materials. There was no element of price hikes and gross margin improvement was mainly led by API segment. This kind of hints at somewhat competitive advantage and capability to be most efficient. If this gross margin expansion continues for several quarters, we maybe onto something.

The supplementary thing to above one is that EFV demand is down by 60% but Laurus sales are not down by 60%. That kind of proves than Laurus might be last man standing due to its efficiencies.

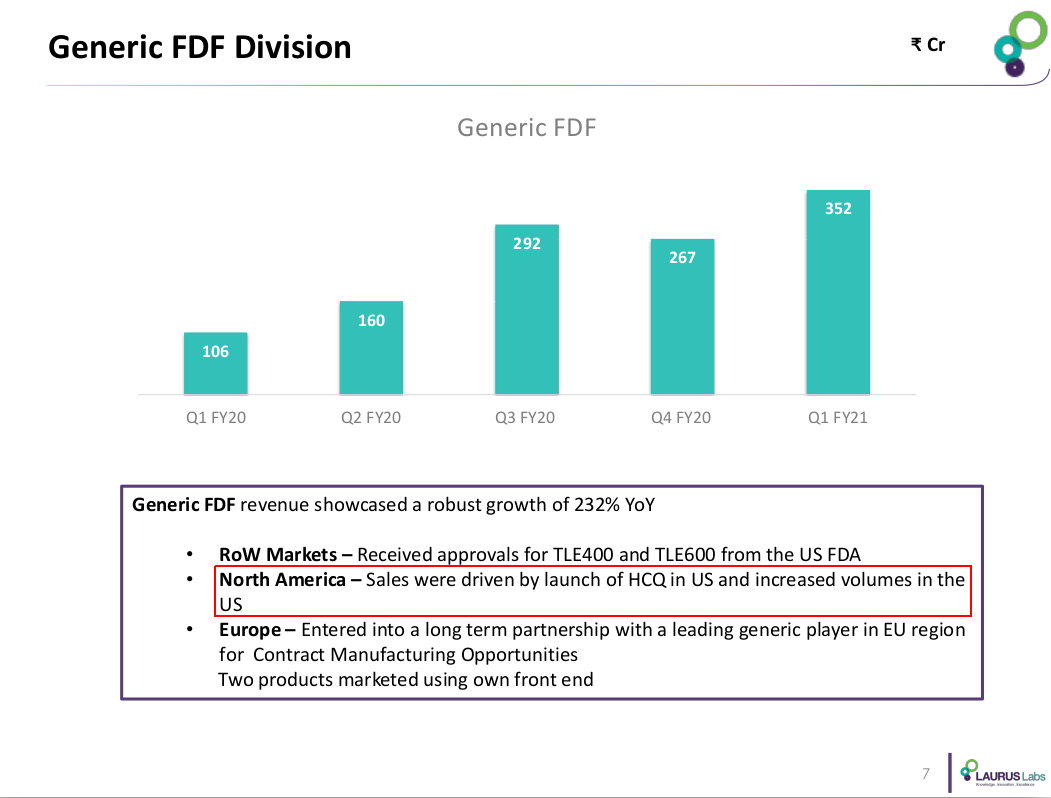

The FDF capacity is going from 5bn tablets to 9bn tablets. The most interesting part is all of this capacity is for non ARV FDF. We need to understand more about what are these non ARV FDFs. For one of the contract manufacturing client, business is expected to go from 1bn FDF tablets to 2bn FDF tablets over next 18 months in non ARV FDF. This (along with CDMO and Oncology API segments) has potential to change the complexion of the company from tender driven, ARV concentrated one to a more all round company.

Apart from this, I have always found Dr. Chava to be focused on growth (sometimes too focused ). If growth does not come at the expense of balance sheet and if balance sheet quality improves - then we are onto something. Balance sheet improvement needs to be tracked from hereon.

Listing few growth triggers -

TLE 400/600 sales will only start from Q2 FY21

20% capacity expansion on API side and 80% capacity expansion on FDF side.

Relationship going from 1bn FDF tablets to 2bn FDF tablets for one contract manufacturing customer.

Commercial API sales of first line therapies - DTG, Lamivudine and then some more from second line therapies.

Acquisition of company in SA to improve contribution in SA tender market

Laurus has all the ingredients that I like Technocrat First gen Ethical entrepreneur with a growth mindset & execution track record. Tailwinds in sector leading to good cagr & ROCE. Moat in form of capex done over last many years & now op leverage helping out. Opp size large and increasing.

Listened to the recording of Laurus concall today. There seemed to be a lot of confidence to the tone of the management which is re assuring to see. Plus a lot of participation from HNIs, fund guys.

Results have been fantastic with sales improving with margin improvement. The latter two things are always a recipe for good returns.

The biggest plus has been the scale up in the FDF business which is a high margin business. API have performed in line with other api companies. Custom synthesis according to management seems to be showing good traction.

I think after the initial teething problems which most companies face after massive capex and fixed assets addition, the company now seems to be on a strong run way for growth. And from the tone and language of the management it seems there seems to be clear indications of good growth with similar or improving margins for next few quarters alteast.

Only concern for me remains too much continuing capex and its associated hazards.

Going by the numbers it seems company can do EPS of 65-70 per share for FY 21. (I am an investor in this company since my last write up on my thread about it and hence naturally inclined to be bullish. ) Question that remains to be answered is what kind of valuations it can go up to. With few companies offering good clear growth visiblity for the next few quarters irrespective of the Corona impact, my guess is there should be strong appetite for such stories.

I am adding this last line to this post as a PS to re iterate anout the state and importance of promoters pledge. As per a recent disclosure, it has reduced. Sometimes, to offer collateral against loans, promoters have to pledge their shares. If they are used to create assets and these assets result in good growth and profits, one has to learn to consider it as a minor deterrent and keep it in the back of the mind as a monitorable. But posting repeatedly about pledging without adding any value is useless and these one liner posts will be promptly deleted.

There are many participants in your thread in passive mode. I have been one of them for last 8-9 years. After going through your last 6-8 week discussions, I was going through concalls of Alembic, Aarti Drugs, Laurus in that sequence. However when I finished going through Annual reports, discussions, concalls, etc. priority was in opposite order. After 21% on Thursday, I took allocation to 30% on Friday morning considering it a High Undervaluation, reasonably high conviction bet, as discussed by Donald and yourself in Capital Allocation Framework Thread. Ben Graham also had a 20% limit, but hard limit was 40% (used for Geico). I decided against 40% since there were more opportunities in same sector - API as you discussed. Was thinking of adding another 5% allocation after management indicated that Q1 results could become baseline going forward, when above mentioned HNIs and fund guys namely from office of RaRe enterprises and Madhu asked questions, and immediately upped allocation to 35% (on cost basis) realising that there’s no point trying to time the remaining 5%. You guys have really provided us a lot of learning and support in understanding stock selection and portfolio allocation over the years. Hope I am able to do justice to the learnings.

My thesis is:

Sectoral Tailwinds:

Chinese bulk drugs/ API manufacturers had 3 advantages: externalizing cost of pollution control to environment, low cost financing, operating leverage due to huge size on account of previous points. Now, since 3 years Chinese govt. started becoming strict on pollution treatment, hence some plants were relocated, effluent treatment charges - costs incurred. Operating Leverage is working for some of the Indian manufacturers who weathered the 2016-20 period. So all 3 factors are nullified to some extent.

Formulations manufacturers worldwide seem to be looking for a robust supply chain and hence diversifying out of Chinese suppliers (may be only for a small fraction of inputs by now!!) and looking at Indian suppliers. To a lesser extent during above mentioned relocations and definitely after Jan, Feb this year.

General apathy towards Chinese suppliers by some major markets. This seems more of a geo-political construct then a business construct, but could play at the back of minds of lot of people, including investors. At the same time, goodwill for Indian pharma.

Generally the pharma cycle seems to be turning and many of the APIs are supplied by Chinese suppliers at 10-20% higher rater during last 6-8 months. So this does not seem to be a temporary covid phenomenon either.

Laurus:

Huge quantities in ARV - low cost production.

Dynamic management - ability to change product mix for higher gross margins reflects that. Also foray in CDMO reflects that.

Global market - Entering into long term JVs for CRAMS, marketing of FDF through partner, participating in tenders ala SA for ARV, global launches

Vertical Integration - Increasing FDF revenue as % of total sales.

Negligible US exposure - a) Less regulatory risks b) Have USFDA approvals, so huge market.

Growth minded management - could become a negative soon if overdone - need to keep a tab.

Actually the above are all attempts at rationalization, but the only rational thing is Earnings growth.

Seems like a 2-4 year bet for now. But need to keep looking at earnings. If Earnings growth is less than half (or even two-thirds) of PE, I might want to remember how Chandrakant Sampat sold 10% every Wednesday at 12 noon till down to sound sleeping level.

@hitesh2710 What do you think are major risks to this story? May be it’s too premature to ask, but - What would you be looking out for to take any calls along that direction? (You did already mention capex)

One thing I am still grappling with is how easily Laurus is able to diversify to non-ARV streams.Back in 2016,they had an 80%+ exposure to ARVs which has come down steadily in just 4 years.Amazingly,even in formulations management is very confident of repeating this feat.So what is the company offering that diversifying into non-ARV segments seems like a walk in the park? It’s like they press a button and it’s there.ARVs seem to be their strongest point but why are competitors giving up their market so easily or the opportunity is just so huge that any efficient player can come in and tap it? I am not clear about this yet.

Coming to Q1,Laurus reported amazing earnings and the best part is that there is no “one-off”.In fact,employee expenses could come down in a few quarters as the incentives related to Covid subside,helping the margins a bit more.As Hitesh bhai pointed out,company could end the year with 600-50cr.+ kind of PAT and even after the sharp run up,the valuations have now fallen back to reasonable levels.On the other hand,debt continues to be fairly high at 1100 cr.Company is in hyper growth phase so these things don’t attract attention.The good part is that you keep making a lot of cash flows which you can plow back into the business to increase capacities and keep up the growth rate.However,high growth rates are seldom sustainable so I would like them to have a leaner balance sheet.As @rupeshtatiya noted,Dr. Chava does seem too focused on growth to the point that he’s more interested in tapping the growth opportunities rather than reducing leverage.I would breathe easier if the debt reduced in absolute terms,even if we have to sacrifice a few basis points off the growth rate.

Since there are a lot of bullish sentiments, I think we need to think about possible risks the company might face.

Continuous capex and its associated complications. As of now demand scenario is good but in future if demand slowdown happens due to whatever reason, there can be problems of maintaining expanded capacities and servicing the debt.

Debt as mentioned in point 1. As of now interest rate is very comfortable at 6.6% (according to concall) but if interest rates were to rise, or if company were to face demand slowdown, high debt can be an overhang.

Currency movements. Currently Rupee is very weak as compared to USD and even against Euro and hence exporters are having a good time. Things can change on this front in future.

Any mishap in the plants due to some sort of accidents etc.

I see a keyman risk also because after listening to dr Chhava, I think he is the key man and a lot depends upon him.

Regulatory risks. Problem of disqualification by USFDA, WHO, or any other regulatory body.

Re emergence of China in the API field. With the Chinese you never know.

Last would be pledging. Deliberately putting this last as I think all the above risks are more relevant than No. 8 at this point of time.

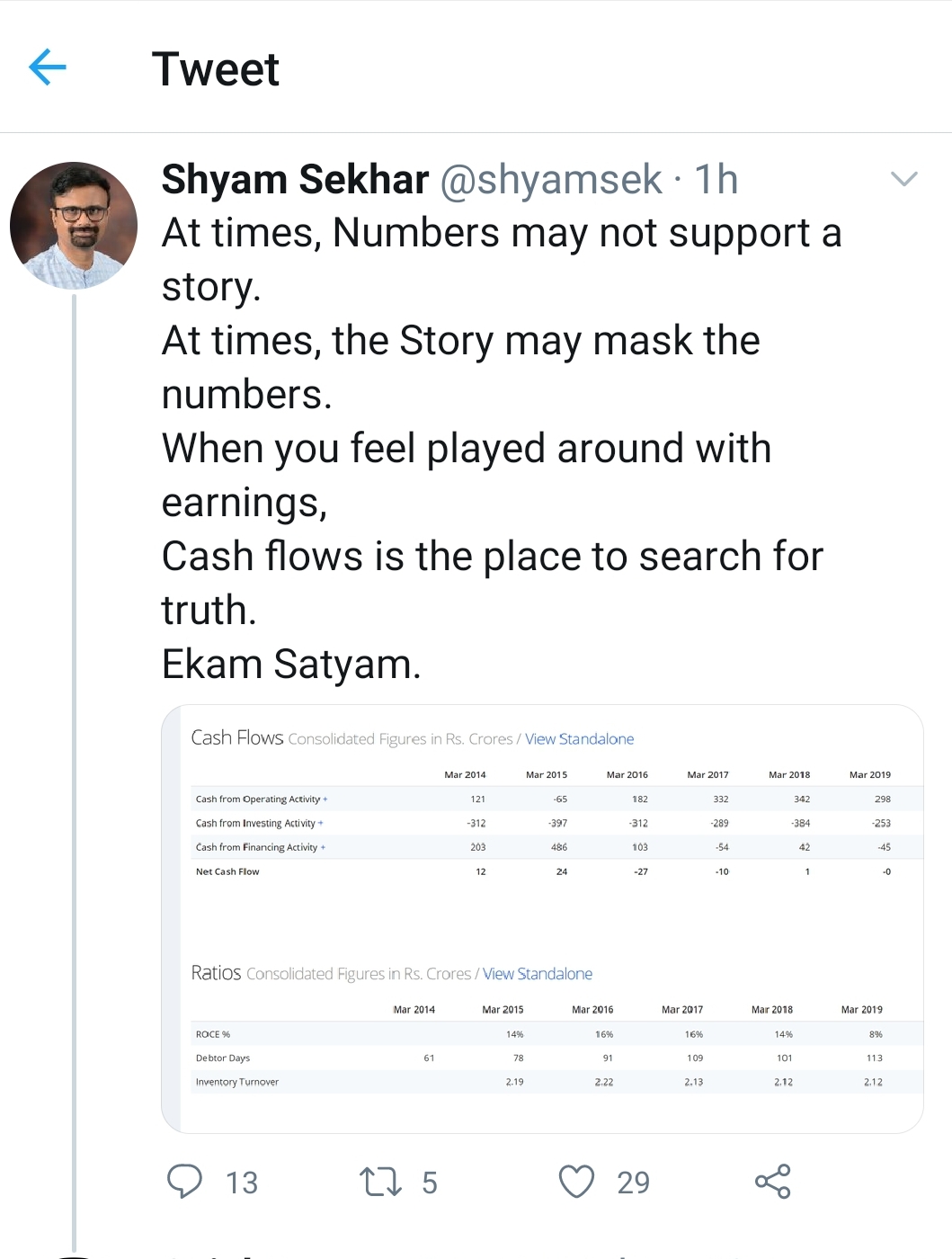

I cant understand his statement at first place.

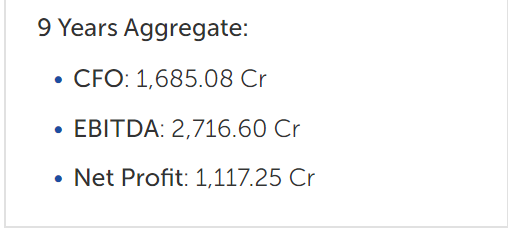

Cash flow from operations is 1685 which is more than the net profit in that period.

Company has invested this amount in addition to that they borrowed 1000+ crores and raised 500+ crore equity and invested (2155 cr invested in last 6 years).

So, where is the question of positive free cash flow ?

He can claim whatever they claims to have invested doesnt exists. That question makes sense.

Satyam scam is one where cashflow from operations was shown as positive( although no cashflow in first place) and they hided it by showing as related companies loans ( similar to wirecard 2 billion in recent times).

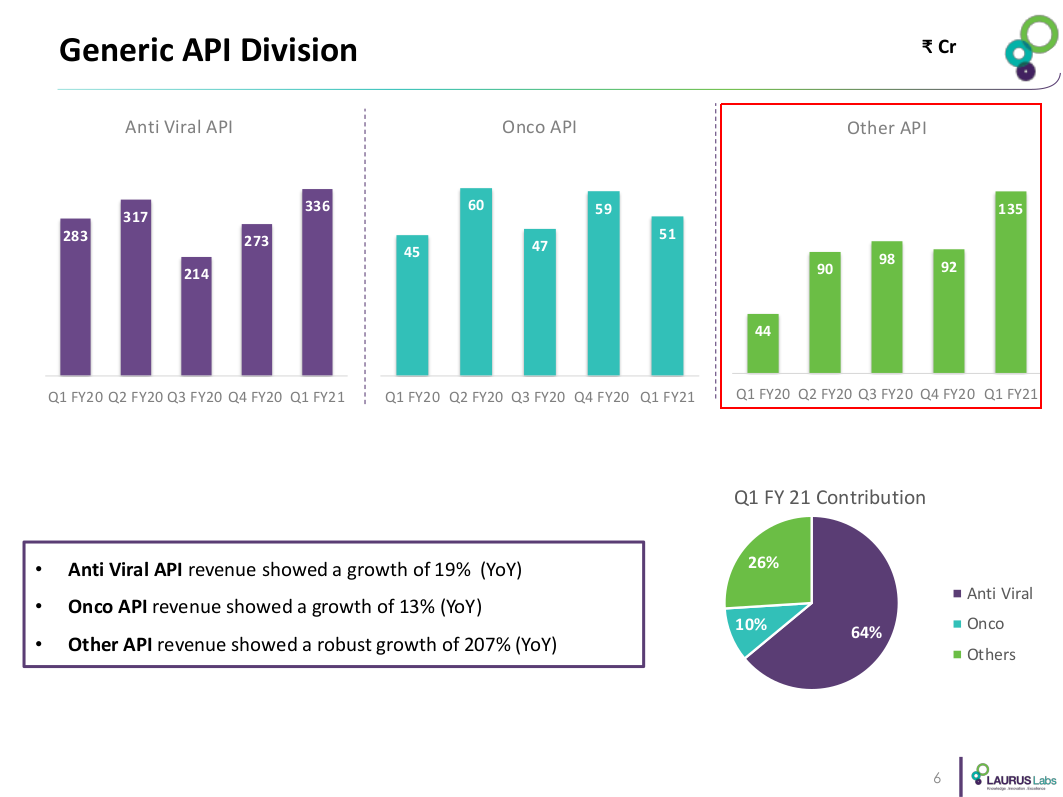

Other API showed a growth of 207%, also company mentions Efavirenz, Tenofovir & Gemcitabine API and their FDF as their main products in their fy20 annual report. Efavirenz is a AIDS drug, Tenofovir is HepB drug & Gemcitabine is a cancer drug.

I generally have no idea, how many API’s a company can manufacture? What kind of capabilities are required to have API’s in so many different areas of medicine?

Highest increase in FII holding during The Quarter Ended June 2020

Jub Food

Laurus Lab

FIIs seem to have lapped up large holdings in Laurus Labs. Good long term investors seem to be getting into it. The results also seem to match the exuberance.

At 1Q21 conf call, Mr Chava said they see a HUGE opportunity in the CDMO segment. But how can they have FDF and CDMO both given CDMO customers might have IP issues with that. If that’s easy, why has Divi’s labs not entered high margin FDF segment?

Also, looks like CDMO division has very high margins. I did some back of the envelope calc. for Divis labs’s/Suven/Dishman segment-wise margins and found that CDMO segment margins are highest (CDMO - ~40-50% vs API 20-30%) while FDF margins could be ~5-10% higher vs APIs.

Laurus also incorporated a subsidiary Laurus Synthesis Private Limited to give an increased focus and then eventually assign a dedicated R&D and manufacturing site for its operations (maybe to comfort CDMO clients ).

FYI, Dr. Reddy also is into CDMO, and many others (including Biocon). So, IP issues are not a concern if the company is trustworthy.

So, that was solely Divi’s strategy to remain in no competition mode. Neuland also seems to have the same strategy.

No competition strategy is the best way to gain confidence of innovators. And being an early starter in this domain made Divi’s to adopt this strategy as then this outsourcing wave were not very much prevalent.

@sujay85 thanks for this explanation.

I am seeing mostly all pure play CDMO businesses (Syngene/Neuland/Divis) valued much higher on PE/EV-EBITDA basis vs. those in diversified API/CDMO/FDF.

Does that imply limited valuation re-rating opportunity for Laurus?

My rough analysis basis notes collected from concall. There could be misinterpretations , help me in correcting those. I have tried to quantify what could be expected in future if management delivers as promised. Notes are only for study purpose.

Disc: Invested

). If growth does not come at the expense of balance sheet and if balance sheet quality improves - then we are onto something. Balance sheet improvement needs to be tracked from hereon.

). If growth does not come at the expense of balance sheet and if balance sheet quality improves - then we are onto something. Balance sheet improvement needs to be tracked from hereon. ) Question that remains to be answered is what kind of valuations it can go up to. With few companies offering good clear growth visiblity for the next few quarters irrespective of the Corona impact, my guess is there should be strong appetite for such stories.

) Question that remains to be answered is what kind of valuations it can go up to. With few companies offering good clear growth visiblity for the next few quarters irrespective of the Corona impact, my guess is there should be strong appetite for such stories.