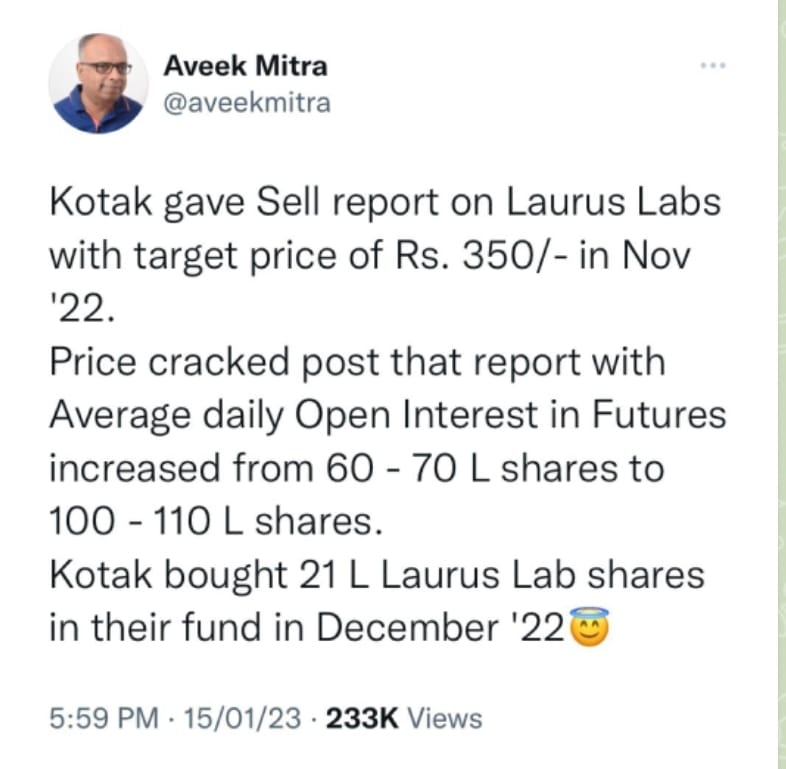

Kotak said target price of 350. In December LLhad reached only about low 400s. So clearly, stock was good enough to buy at that price. I understand LL antiviral biz is the Achilles heel, also CDMO may belumpy revenue. But LL ticker has been beaten down way too much.

But LL ticker has been beaten down way too much.

This conclusion will only be fair if you compare its current price with its all-time high of ₹707.

But that comparison isn’t fair. Because Laurus Labs even at its current market price is still a five-bagger compared to where it was less than three years back (split adjusted) and that is still a phenomenal return.

The fact that its share price scaled to those astronomical heights in the short span of 18 months (ending on August 2021) is a result of sheer euphoria when almost everyone wanted a piece of it no matter what the cost is.

What we are seeing now is sanity being restored with the stock being valued factoring in both the positives and the negatives of the underlying business. But that doesn’t necessarily imply that it won’t be a long-term wealth creator.

Thanks - Arnab Roy

Disclosure - Not Invested

LAURUS LABS: Q3 CONS NET PROFIT RUPEES 2.03B VS 1.54B (YOY); EST 1.85B

LAURUS LABS: Q3 EBITDA 4B RUPEES VS 2.85B (YOY)

Delivers with numbers

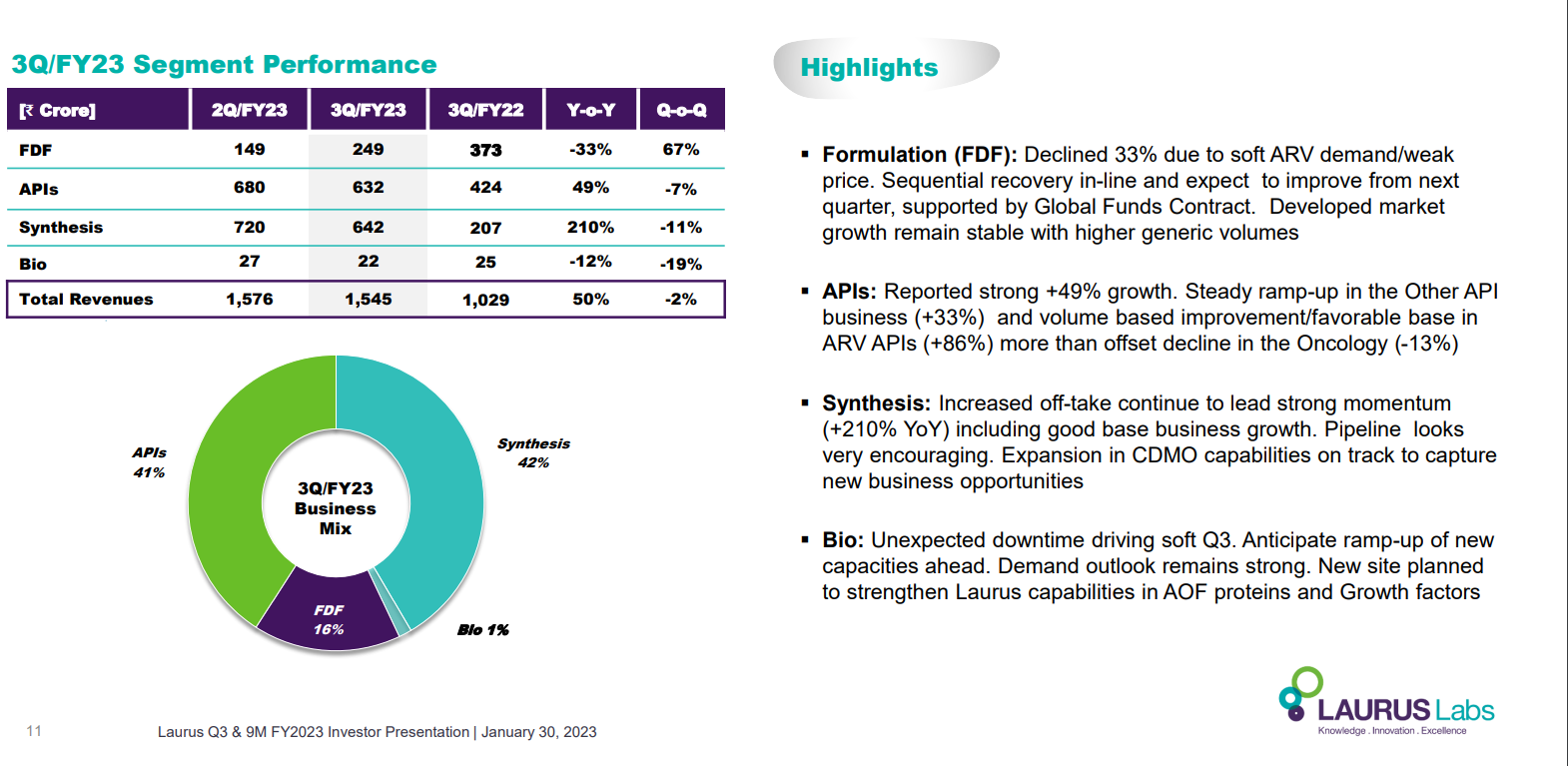

The recent quarter numbers don’t look great though or I am reading them wrong. Revenue dipped slightly (1577 Cr to 1546 Cr), Net profit dropped to 202 Cr from 233 Cr). Also, anyone has insights into what the CDMO revenue contribution was?

Laurus Labs Q3FY23 Concall

5 ANDAs filed in last 9M, filed first NDA for pediatric HIV delivery

We have a total of 64 products in R&D, TAM 40 billion

2000cr CAPEX in FY23-24

Power issues resolved and now we don’t have higher private power rates.

Gross-Margins decreased due to ARV API & Formulations. It will not go down further as non-ARV businesses that are growing have a higher margin than ARV

Hope to meet FY23 revised guidance.

ARV- API

In 9MFY23, ARV business in API and formulation together was 35%. By FY25 we hope to bring down that to 25% of overall business

Laurus has won a 3-year ARV business tender from a Global Fund. ARV pricing still depressed, will have a gradual uptick only

2Million capacity added in API will be used in non-ARV and CDMO business

ARV API & FORMULATION on a annual basis will have 2500cr revenues

FORMULATION

In 9M- 45% decline in business due to ARV business

No decline in non-ARV business

Current capacity utilization is 60% (6B of 10b tablet capacity) out of this, 25% of capacity is for CMO (1.5b tablets).

CDMO

60 active products in CDMO business, R&D center and two manufacturing division going on well. We will qualify one animal healthcare facility in the mid of FY24

One facility will be for Animal health and the other is for Agro-Chemicals pilot plant construction over and validation is going on in the pilot plant

Animal & Human health will have similar ratios , Agro will have lesser margins but higher asset turns

Human health growing well with many NCEs, Agro revenues will come in FY25-26

BIO

We are debottlenecking R2 unit and that lead to increased downtime

Initiated process for Land acquisition for bio business in Mysore, in animal origin proteins

Dr. Chava did his customary quarterly interview with BQ Quint today (Q3 Review | Laurus Labs' Growth Strategies For Coming Quarters | BQ Prime - YouTube). My brief notes from the interview:

-

Q4 revenues will be around the average of Q1-3, so expect to end the year between 6000-6200Cr revenue (7.5%-4.5% short of revised guidance of 6500Cr)

-

Laurus has reconciled itself to the fact that ARV API + Formulations revenues won’t grow beyond 2500Cr and growth for the company will have to come from elsewhere

-

As per Dr. Chava, Q3 FY23 saw the lowest pricing and margins in the ARV space and he is confident that pricing will only improve from here on (Personal opinion: Considering misleading guidance in the past wrt ARV sales and inventory stocking etc, I would not necessarily take this statement at face value)

-

Expects CDMO revenues in FY24 to remain below FY23 levels or at max be flat YoY. Did not explicitly concede the roll back of Paxlovid revenues in FY24 but his comment probably makes that eventuality clear.

-

On being pressed about margins, Dr. Chava said he does not expect the margins to slide from FY23 levels in FY24 due to rollback of Paxlovid as he expects other CMO/CDMO projects to compensate (I am personally skeptical about this, I think FY24 may see some margin impact)

-

Animal Health CDMO revenues to start in FY24 and meaningfully ramp up in FY25 and agro CDMO revenues to start in FY25 and meaningfully ramp up in FY26

-

Expects FY24 to be muted (Calls it a year of consolidation) and expects FY25 to be a step up year

By the looks of it, the business as well as the stock will go through a period of consolidation for the next year or year and a half. This period will probably solidify the post ARV avatar of Laurus. I think Dr. Chava’s thesis was built on ARV revenues remaining strong for a few more years so that there was a smooth transition from being an ARV led company to being a CDMO led company. But that thesis has been disrupted now with Laurus conceding ARV growth will be capped. Remains to be seen whether the Laurus 2.0 that emerges in FY25 will be more like Syngene or more like a generic pharma API/FDF supplier.

Disclaimer: Exited most of my holdings in last Q. Continue holding a small position.

Excellent summary, Nirvana. Having heard Dr. Chava in all interviews and concalls for the better part of last two years, my sense is that he was very restrained on giving any number/guidance/forecast given how badly the $1bn revenue guidance has panned out. My sense is that the FDF division may spring in a positive surprise in the next quarter or the subsequent one, given that entire 10bn units capacity is on stream now and bulk of the revenues come from the non-ARV space. Everyone is focused on how CDMO and ARV revenues progress moving ahead, but FDF could clock in close to FY’22 revenues of circa 1800 crores in FY’24.

D:Invested.

Things turned from 1 billion dollars to year of consolidation pretty fast. I have lost my conviction on this stock.

Will exit my remaining position.

Added at 330 levels. One things laurus has teach me to never run for cake pie.Wait and watch till time comes. Price correction, time correction, volatility, uncertainty and headwinds are all price which one have to pay to create long term wealth.

Lots of negativity around failed promise of 1B. Now Dr.Chava said even FY24 will be muted due to CDMO consolidation and for FY25 there is no visibility of margins. Doesn’t look good.

A very good video of the Unit 2 in Vizag.

Dear All,

I have few questions as follows:

- Can we assume there was no paxlovid sale during the quarter ending Dec’23? Or safe to assume quarterly run rate of 640 cr for CS going forward?

My aim is to know safe assumption on CS base ex-paxlovid going forward.

-

Less margin contraction compared to Divis, is it right interpretation that some other CS projects are supporting the margin?

-

Since CS will have FY24 year of consolidation, should we expect decent growth from FDF and API business exc ARV as pricing pressure eases?

Disc: Invested

Laurus labs has lost its charm, next year will also be time correction… will be around 250-300 unless some big institutional investors exit around… otherwise it could be going around 160 in terms of technical trends… let’s check out in FY 25 as chava mentioned in one of the interview

We have tried to analyse the wave structure.

if we just assume no growth in sales and no improvement in margins for next FY, it’s trading at 11x FY24 EV/EBIDTA and 2.8x Price/Sales. Valuation multiples look cheap. If there are any positive surprises in earnings, it will make it even more cheaper.

As per Dr Chava, music will start from FY25 but market might factor it in the price even before that. So, we can’t wait to time the entry. We can’t trust Dr Chava’s commentary based on the past track record but execution has been great and mostly it will do well down the line. Is it a good time to accumulate if we are prepared for short term pain? Any views will be helpful.

Also, how do we calculate depreciation? Any rule of thumb?

Hi, I am new to doing in-depth analysis of financial statements. Please bear with my question.

I saw many annual reports where they mention how an acquisition or investment will help the company and how much they paid and how much revenues or profit will be added because of the acquisition. But in case of Laurus they just mention we did acquisition for X amount. Thats it no mention of how it will help the company. It was odd no one asked about these acquisitions in con calls also. I searched the transcripts for last 2 yeas. Am I missing something or company want to hide something. You are answer will help me to gain knowledge, Please help.

What’s the capex going into dedicated CDMO block that’s coming up in FY25 ? And what’s the peak revenue potential from it ? I assume the gross margins would be in par with the consolidated margins of around 30

Follow up from earlier post:

Laurus and Divi’s both saw covid related products fall off a cliff and go to 0 in Q3FY23. Now, Laurus has resumed shipping Paxlovid in Q4FY23. It currently forms 50% of Laurus’ export revenue in Q4.

Despite this resumption, the market hasn’t reacted. One expects sequential improvement in Laurus’ numbers due to this, but ex-covid related molecules (like TLD) are still very much in the doldrums compared to volumes seen a year ago.