Laurus saga is a good lesson on multiple fronts for all of us who have invested -

- Role of Luck in investing

- Most of us entered Laurus in mid to late 2020 because of anticipated operating leverage, lowest cost producer of ARV APIs etc etc kind of thesis. Now this is a normal thesis for anyone to enter a manufacturing company stock. But COVID led increased demand of ARV products led to inventory stocking. When supply is limited and demand is high, prices also go up. So we had more volumes + extra price led growth coming in Laurus business which went up from 2700 Cr to 4800 Cr in FY21. Now we are getting to know that since the inherent capability of Laurus’ business is to deliver around 2700 Cr of ARV revenues, which means they over-earnt around 800 Cr of revenues in FY21. The market cap went from around 4000 Cr pre-COVID to over 36000 Cr in FY21 August. This is perfect example of -

A great deal of investment success can result from just being in the right place at the right time

- Take managements at face value at your own peril

Here are some of the statements from Dr. Chava -

From Q4 onwards we do believe we will go back to the Q4 of FY’21, we’re very confident on that - Q2FY22 concall

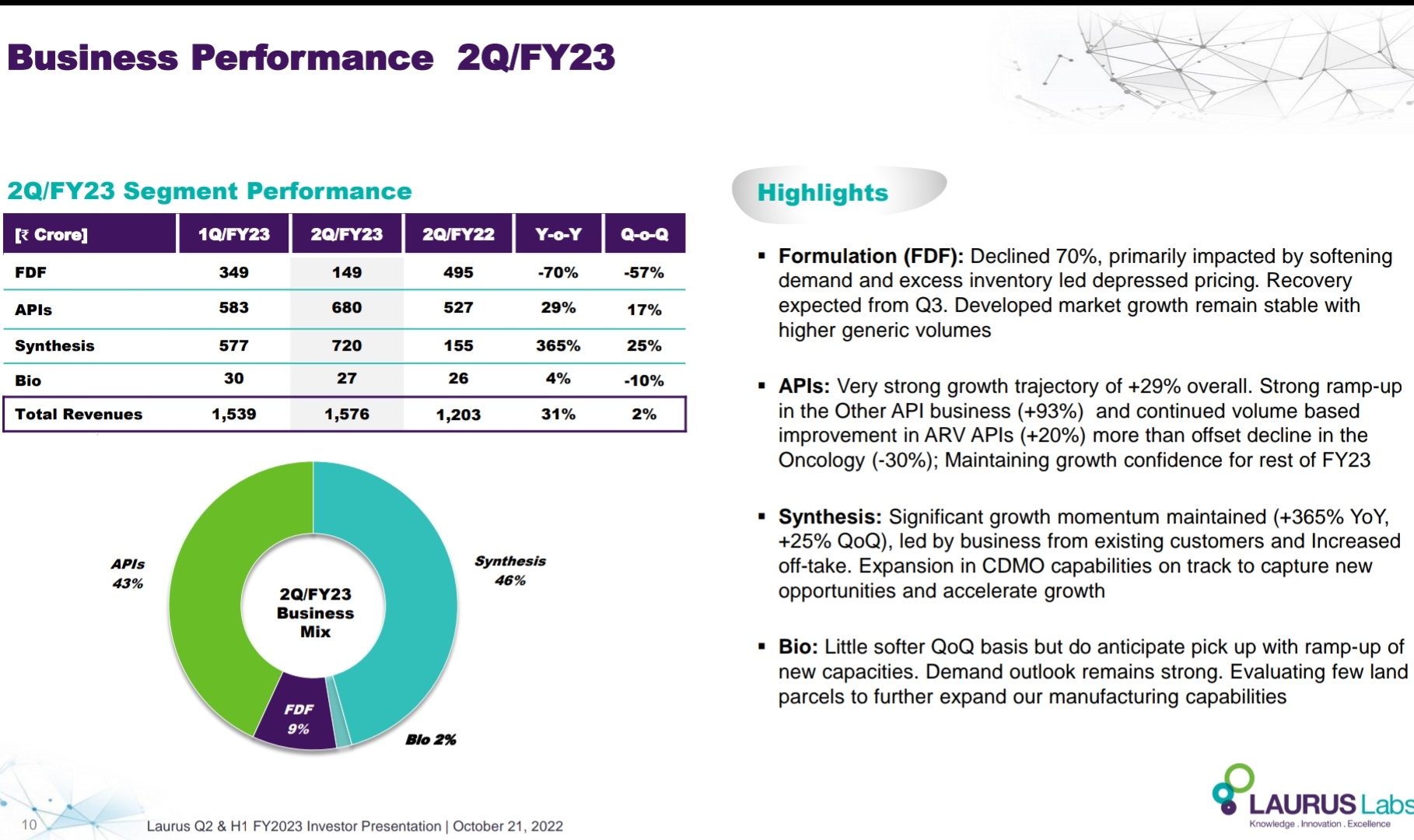

Reality - Q4FY21 was 565 Cr but Q4FY22 turned to be 296 Cr

ARV API business will normalize soon - Q1FY22 concall

Reality - It has still not crossed Q1FY22 level yet.

We continue to see good offtake in onco APIs. - Q1FY23 concall

Reality - Onco API number is down 25%+ sequentially

We have capacities, we have customers, we have visibility of orders and except one product approval in formulation all are in place, if we are scouting for customer, we are scouting for a capacity or a facility approval and all, it is a long goal. So, we are not at that, we are very close to our goal. We have all the actions required or abilities required to reach that number - Q1FY23 concall on $1B target

Reality - Target cut to 90% of original value in 2 months, when 1 month of quarter has already passed and one has good visibility of atleast 1 more month in such a business to give right idea to investors.

There are many more such statements with verbiage - “We expect good…”, “We anticipate good…”, “We continue to see…”. With such statements and our anchoring to $1B sales target in FY23, lot of us simply ignored the basic tenets of investing - Generics business is mostly brutal, supply demand led competitive challenges etc.

While management is doing its job of diversifying business from ARV to ARV + Non-ARV + CDMO by FY25, but the statements that they gave to depict that there is no risk to $1B target isn’t good at all.

Even now they are saying that CDMO has no one-offs, but given this track record, it is obvious that this can’t be trusted at all.

So right now as an investor we have two kinds of options -

- Believe in ambitious promoter and sit with the stock. Meanwhile, be ready for uncertain ride because this is Generic + CDMO business and markets give 3x-5x P/S to such businesses. Add to this, we don’t know what is their normalized sales number, given Paxlvoid numbers can be one-off. So market can act extremely on downside to such stocks.

- Given the uncertainty in revenue trajectory, simply sell the stock and re-look it later if you can understand the future and risk reward is favorable.

Disc. Sold some on Friday, will sell remaining next week.