Contribution of ARV to total sales is 42% as mentioned by Dr. Chava in concall today.

ARV API’s: 379 crores

ARV FDF: 267 crores

Total: 646 crores.

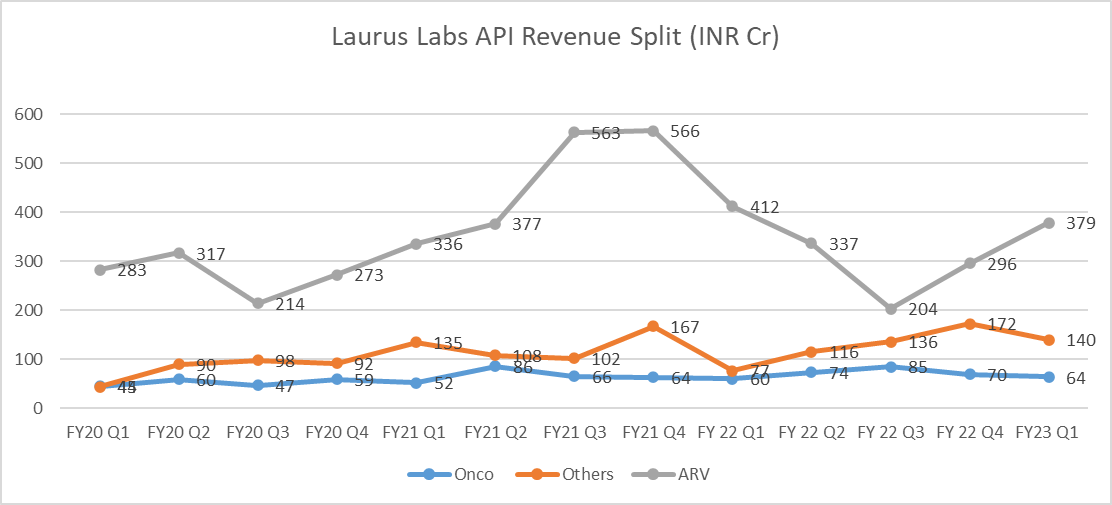

Looking at the break-up of API revenues for Laurus for the last 3 years, looks something like this

FY22 was not only a bad year for ARV APIs, it was pretty bad even for Onco and Other APIs. While CDMO is taking the bulk of the load in transitioning Laurus towards a less ARV dependent future, its critical to track revenue growth from Onco and Other APIs as well because they are also a key part of the diversification-away-from-ARV thesis.

Q1 FY23 numbers are encouraging for Other APIs (102% YOY growth) and flattish for Onco (7% YOY growth)

11 Likes

concall notes

2 Likes

3 Likes

one more concall note with key insights discussing why cdmo revenue will continue.

Disclosure: Invested.

2 Likes

FY23Q1 Conference Call Summary

P&L Statement

-

Rev 1.5KCr YUP 20%

-

Rev(Formulation): 0.35KCr YDN 33%

-

ARV Rev: 0.38KCr

- volume & prices will stabilize

- leading MS / will inc marginally

-

Onco API

- Rev: 63Cr YUP 5%

- has largest high potent capabilities

-

API (excl onco+ARV) : 0.14KCr YUP 80%

- incl diabetes, CV and asthma

- new contract supplies

- Ft: healthy growth FY23

-

GPM 57% YUP 1% ← better product mix

-

EBITDA: 0.45KCr / EBITDAm: 30%

-

RoCE: 29%

-

CAPEX: 209Cr / Ft: FY23 & FY24: 2KCr (1KCr - CDMO + 1KCr non-ARV)

-

Overall GPM stable

- lower ARV margin offset by higher CDMO margin

-

other expenses: 33Cr (higher)

- power sourced from pvt sources ← R: power shortage

- forex losses (restated loss, not real loss)

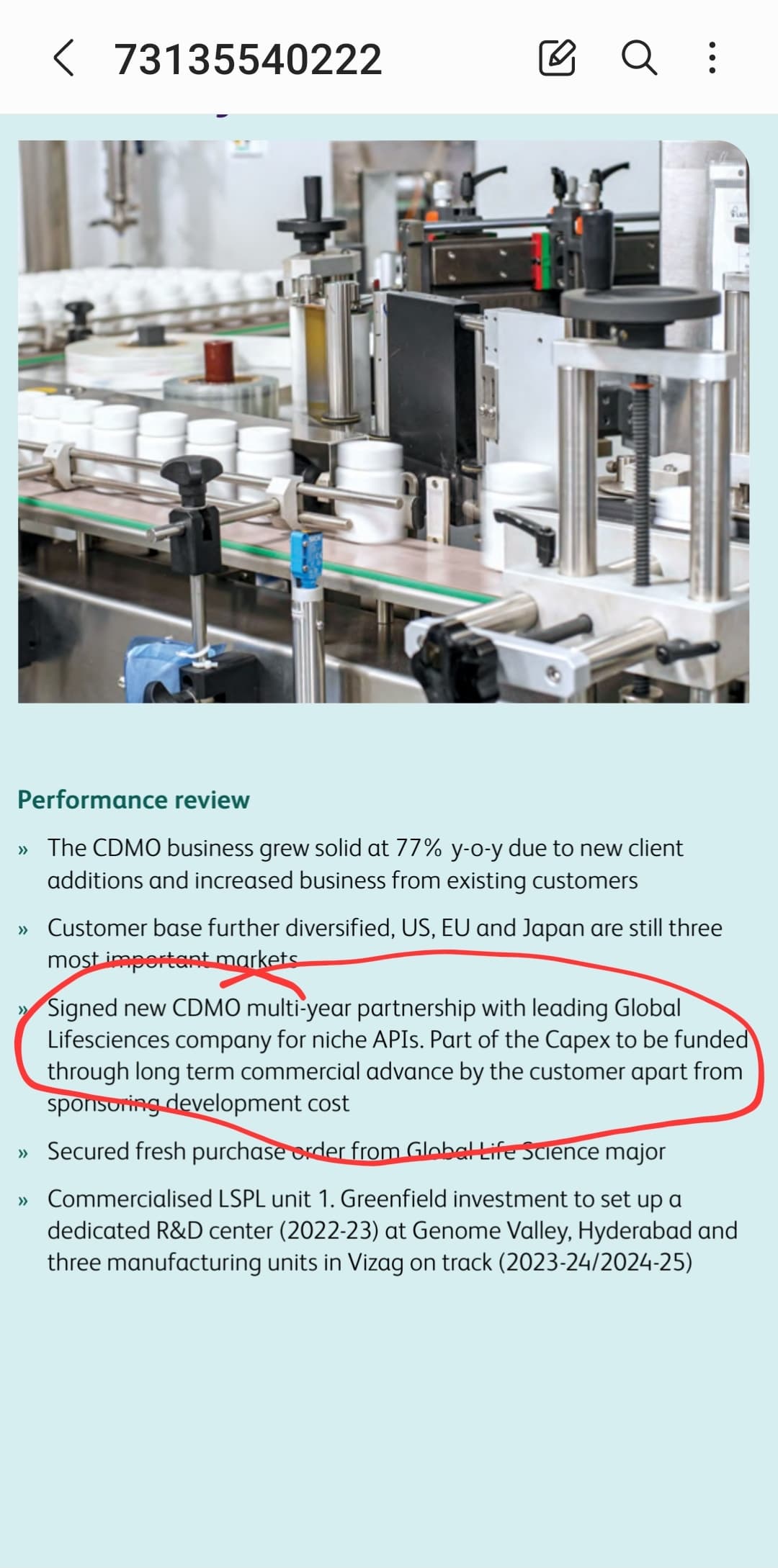

CDMO - Synthesis

-

Rev: 580Cr/Q YUP 190% [YUP - growth YoY]

-

contracts: 2

- multi CDMO contract with niche API

- global major life science

-

high demand → inv in 3 mnfg sites + R&D unit

- steroids, hormones, high potent molecules

- large volume products in animal health.

-

-: Mngt is not commital on future run rate

-

commercial products: 7 - intermediates: 4 / API: 3

- late-stage products: many

-

+: NCE - patented → long runway

-

+: pricing is predictable and stable / not much pricing pressure

-

Focus: commercial execution & pipeline expansion&execution

-

most rev coming from CMO

-

Ft: CAPEX asset turn: 1-1.5

-

Ft: Rev share: 33% ← 25%

-

differentiator - speed & flexibility

Laurus Bio

-

Rev: 30Cr

-

rev will pick-up with

- ramp-up of new capabilities

- debottlenecking for a large scale CDMO partner

-

alternate food industries

- scale, cost and functionality will remain the core drivers

-

fermentation - world is overdependent on China

-

capacity built for:

- synthetic biology

- alternate foods

- recombinant food proteins

-

Revenue forecast

- FY23Q1 30Cr

- FY23Q2 30Cr Same

- FY23Q3&Q4 inc in rev <–R: downstream debottlenecking

- FY24 ← flat

- FY25 Ramp-Up ← R: CAPEX

-

CAPEX 3-4M ltr capacity

- Plan: FY23Q2: land acq

- opportunity is there, lacks capacity

- facility ramp-up FY25

- start of CAPEX to peak commercial sale: 3-4Y

- competion of CAPEX to peak commerical sale: 2Y

(full capacity utilization)

-

R1 facility expansion

- new R&D block

- downstream balancing equipment

R&D / Filing / Launches

-

US ANDA filed: 30 / Approved: 11 / Ten App: 14

-

CAN App: 11 / Launch: 5

-

EU: CMO opp: product validated: 2

-

DMF Filing: 74 (1 non-ARV in Q1)

-

launched lopi-rito combination in US

-

non-ARV formulation: lot of filing done, lot of approval anticipated

-

R&D/Sales: 3%

-

Products in R&D pipeline: 55 / Addressable Market Size: $40B

(review + dev)

ARV

-

ARV volume stable

-

ARV formulation will pick-up next quarter

-

Rev: ARV:non-ARV - 42%:58%

-

ARV API+FM prices down 10% FY22Q4

- down another 5% FY23Q1

- Ft: not expecting any further significant price drop

-

Ft: ARV revenue (API+Fm) 3KCr

- inc volume + dec price → GPM will go down

- maintain leadership position

- no more high margin business

- cash cow

Revenue Forecast

- Ft: FY23 Rev 7KCr

- we have capabilities, customers, orders, product approval in place to achieve the goal

- rev growth - not linear, but stepwise

Misellaneous

-

calibrated tendering approach

- R: focus on profitability

-

4 “C”: capacities, capabilities, credibility, clients

-

not a chemical company, but a chemistry company

- chemistry capabilities (large scale)

* chromatography

* biocatalysis

* fermentation

* hydrogenation

* continuous flow chemistry

* very low temperature chemistry

* spray drying - scale to offer value to our partners

- chemistry capabilities (large scale)

-

leadership in molecules: 8 / N2Y: 10 / aspiration: 15 [N2Y - in next 2 Years]

CAPEX

-

CAPEX N2Y 2KCr - mostly from internal accruals

- Asset turnover: 1-1.5

- CDMO: 1KCr

- non-ARV CAPEX (1KCr) : 2/3 API + 1/3 formulation

- ARV - no more CAPEX

-

sterile R&D lab - commissioned

- started working on a few priority projects

-

adding addl mnfg capacities in non-ARV & non-Onco API

- R: very high order book

-

formulation - new capacity caming-in

- full capUtil by CY22e

-

Added significant capabilities + reactor volume

- at scale capabilities:

* hydrogeneration, cryogenic

* biocatalysis, continuous flow

- at scale capabilities:

-

capacity fungible ??

- animal & human seperate

- some equipment technology specific - not fungible

- majority of the reactors are fungible

-

Unit #2 capacity: 10B (now)

- 5B - installed and qualified

- brownfield expansion: 5B (after 10B capacity is utilized)

-

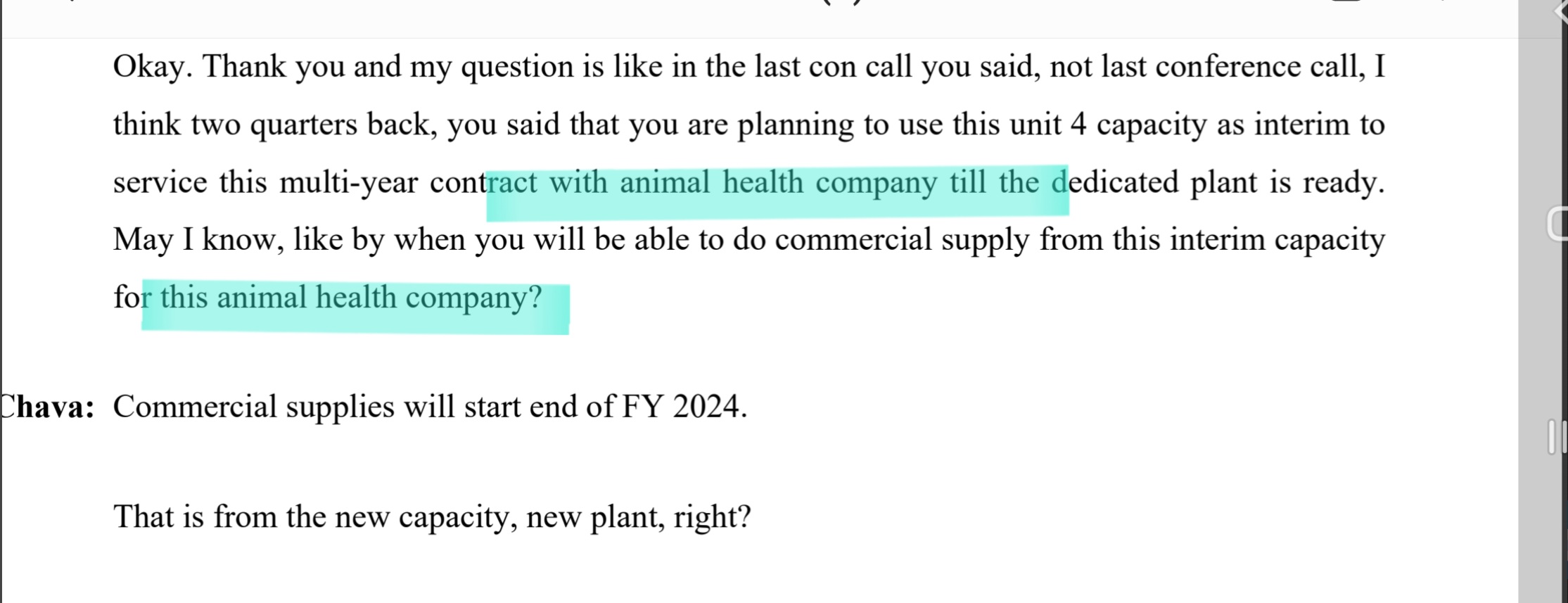

Multi-Year contract with animal health company

- commercial supply from dedicated plant: FY24

- till then: unit #4 (interim set-up)

15 Likes

Tendering process looks a bit disrupted now, happened before in 2014.

disc: invested

1 Like

I have few questions.

1.What is the current market share of ART in India?

2.Who supplies the most ART to govt?

3.Who will benefit the most? (Laurus or Cipla?)

1 Like

About 5% shares of Laurus have been acquired by New World Fund Inc USA on 16 Aug 22 through open market. This should be a bullish news for short term / mid term.

There is news of shortage of HIV medicine in India as per BBC. On the other hand the management was lukewarm about the immediate prospects of HIV medicine in Q1 23 concall.

1 Like

They were already holding 4.9%. They acquired around 0.1 % on 16 Aug. As such there is nothing substantial in this

8 Likes

Can anyone explain these ??

1.leadership molecules

2.animal company zoetis or not?

3.how can we know more about those technology or similar best COMPANIES in the world

2 Likes

in which category it will come for laurus. they didn’t mentioned any note on q1 23 concall

Good question. Considering the fragmented nature of pharma sector today, important to understand the niche.

Came across an article in simply wall street… mentioned in that laurus labs has too much debt exposure against earnings… can anyone throw some light on the whole seriousness?

The overall borrowing as on 31st Mar 2022 was 1777 crores. The Cash Flow from Operating Activities in 2022 was 911 crores. So assuming that Laurus would be able to grow earnings at around 25% CAGR, it would take 1.5 years of earnings to repay complete borrowings provided it would not take any new debt. The thing with fast growing capex intensive companies is that you need funds to grow topline, and that fund would either be equity or debt (rarely it would be completely from internal accruals).

Cheers,

Krishna

16 Likes

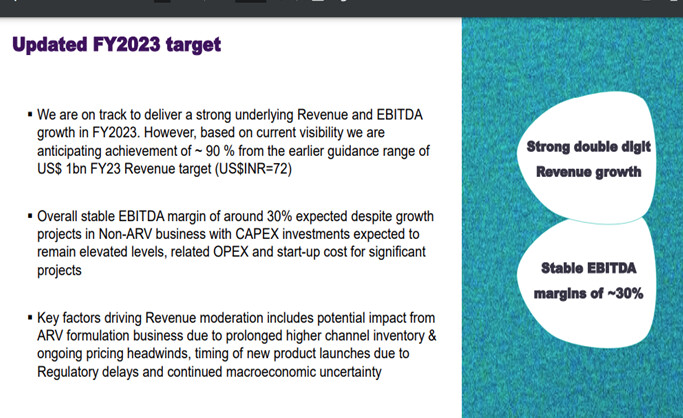

Results are below expectation led mainly by slump in FDF segment. Guidance is also reduced as per PPT.

Disclosure: Continue to Hold

2 Likes

Q2FY23 Concall Notes

ARV formulations was down , pricing pressure in that business had let down the revenue guidance.we lost 500crs in H1 in ARV formulations.

Will not have more downgrade of guidance. We didnt not revise the pricing in tenders and lost a lot of tenders. Client side destocking over , we have visibility going forward.

75% of our business will not be impacted by European situation.

EBITDA margins was low because of lower margins in ARV API and deleverage in ARV formulation sales.

Newly commissioned FDF unit already shipping products. We have area left for another 5billion brownfield capacity expansion will take a call on it next year we can do it in 12M

against 24M incase of a greenfield.By the end of this FY23 we will have 75% utilization of 10billion FDF capacity ,less than 20% of new capacity was allocated to ARV business

Dedicated R&D block for a large Lifescience client will be commercially available next year september-october

6 Likes

The hit for Formulations is just massive. The walk back on the billion dollar goal is embarrassing.

But, CDMO growth is just phenomenal. Tough times for Laurus,but I think it’s a good time to snack…

DISCLOSURE Opinion,NOT a Recommendation. I am a it of a dunce, to be honest.

3 Likes