LAURUS LAB ANNUAL REPORT 2020

https://www.bseindia.com/corporates/anndet_new.aspx?newsid=d7b965ee-e79b-4650-915b-37ebabc311c1

LAURUS LAB ANNUAL REPORT 2020

https://www.bseindia.com/corporates/anndet_new.aspx?newsid=d7b965ee-e79b-4650-915b-37ebabc311c1

Notes from AR 2020

Key business updates:

Business Segment:

API (57% of revenue):

Generic FDF (29% of revenue):

Synthesis/CDMO (14% of revenue):

Financial Performance:

Guidance:

Other Points:

Risks and Open Questions:

Promoters revoked pledge of 46.5 lakh shares on June 17. So, shares pledged by promoters came down to 31.64% from 45.22%.

I read Sajal Sir’s tweet about this a few weeks ago and kicking myself now for having missed what has been a secular up-move to near its 52 week high.

Here is a fundamental analysis.

Company has been investing a lot in net fixed assets, which have become 4 times in 6 years, during which time sales became only 2.7 times. So future growth can be higher from these fixed assets.

P/E ratio of 22.4 which is below its average P/E of close to 29. So there is room for another 30% upside from here as the pharma composition in sensex is going to increase. I think this could be a good buy

Disc: Following the stock and feel this is a buy. I generally like to buy these stocks when they fall. So will be looking for a fall of about 20% from the current price before buying as I believe in investing in a manner that gives me peaceful sleep

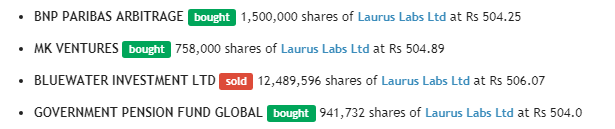

Bulk deal happened today (almost 10% of total shares) - Link

Would be interesting to know who bought and who sold.

Disclosure: Invested

This only accounts for approximately 32 lacs of selling & Buying.

Buyer details are not available for the balance 92 lacs shares sold by Blue water Investment

*Laurus Labs – Takeaways from the AGM *(Systematix Institutional Equities)

Regards. Nikhil Khandelwal. Systematix

Laurus Labs AGM:

My notes from Laurus AR 2020.Most of the statements are directly lifted from AR and this is my first attempt at taking notes from AR.Please excuse if there are quality issues.

Business Overview

What they do?

• They operate in 3 business lines

Laurus works with top 10 large global generic pharma companies in the following areas :

• Anti-retroviral (ARV) - Incremental HIV patients added to patient pool will support future revenue growth. Expanding in second line treatment will also add to growth

• Oncology - Leadership in select oncology APIs, new products added to support commercial launches on patent expiry. Backward integration completed for a key API

• Other APIs - Strong opportunity in other API space on account of diversified products on anti-diabetic, Central Nervous System (CNS) and Proton Pump Inhibitors (PPIs)

Generic FDF’s:

• In this segment they are targeting high growth market like US, Canada, Europe and LMIC

• Therapeutic focus areas remain on key segments of ARV, CVS, CNS, PPI and anti-diabetic

• Currently has 5 billion unit capacity

• Capacity expansion initiated in the existing Unit 2 building and will be operational by September 2020

• Proposed construction of second formulation block to enhance the capacity to 10 billion units per year expected to be completed by FY 2022

Synthesis/Ingredients:

• Focus on supplies of key starting materials, intermediates and APIs for New Chemical Entities (NCEs)

• Completed several projects in various stages from pre-clinical to commercial scale

• Proposed to incorporate a wholly owned subsidiary Laurus Synthesis Pvt. Ltd. to handle this division, going forward

Revenue Contribution from the above segment:

Generic API’s : 57%

Generic FDF’s : 29%

Synthesis Ingredients : 14%

CEO Message :

• We registered our highest ever revenue, EBITDA and profitability during the reporting year.

• Formulations business led by LMIC tender business continues to deliver robust growth, resulting in 30% revenue contribution for the year

• Along with the tender business we are also pursuing emerging opportunities in developed markets of North America and Europe

• We continue to file 8-10 ANDAs a year as we see many long-term opportunities in the US generics space. On the other hand, our Custom Synthesis business sustained its growth trajectory with higher volumes from the CDMO business.

• Expecting other API business to grow in coming quarters due to introduction of new products

• We have reached maximum utilization levels of our formulation unit and with healthy outlook and order book, we continue to invest further in our FDF infrastructure and also in the development

• ARV segment has degrown due to lack of clarity on tender being awarded in South Africa where key customers of Laurus are not stocking up the inventory. Once the tenders are cleared business is expected to grow.

• We have completed filing of our second line ARV APIs of Lopinavir and Ritonavir and we expect to do formulation development of second line API as well. In the other API segment, we performed well, the growth was primarily driven by contract manufacturing of APIs to other generic companies. Synthesis business continued to show gains in line with scale up in engagement with Aspen.

• Execute large size opportunity from tenders

• Scale up business in association with ASPEN

• API business to deliver volume growth in key ARV segments

• Other therapeutic areas, including oncology to offer consistent opportunities to broaden scope

• Being the cost leader in ARV APIs, Laurus is best placed to garner attractive market share (in 3 products) of the US$ 2 billion ARV tender market. Lower cost and patented processes have been the key factors in making Laurus the preferred API supplier in the ARV segment.

• Laurus currently supplies APIs to 9 of the 10 largest generic pharmaceutical companies and has an advantage in backward integration

• Laurus has filed 26 ANDAs with USFDA and 6 final approvals and 5 tentative approvals. In addition, it has completed 2 product validations. It is likely to file 8-10 ANDAs every year with a focus on various therapeutic areas of ARV, CVS, CNS, and PPIs along with few Para IV opportunities. Laurus also participates in LMIC tender market via partnership with Global Fund, the ARV - LMIC market size is ~$ 2 billion.

Strategy:

• Capitalise on leadership position in APIs in select, high-growth therapeutic areas. Deeper foray into regulated markets

• Expand API portfolio in key therapeutic areas, such as ARV, Oncology, CVS, Anti-diabetic and PPIs

• Leverage API cost advantage for forward integration into Generic FDF

• Develop synthesis business through various global innovators including Aspen

• Expanding from synthetic process to natural extraction

Others:

• Promoters increased stake by 0.09%

• FII’s have reduced their stake by 20%. Earlier it was 36.6%(March Quarter) and now its 16.06%(Whats cooking here?)

• DII’s have increased by nearly 2%

• Public have increased their stake by 18%

500000 shares pledge released

https://www.bseindia.com/stock-share-price/laurus-labs-ltd/LAURUSLABS/540222/disclosures-insider-trading-2015/

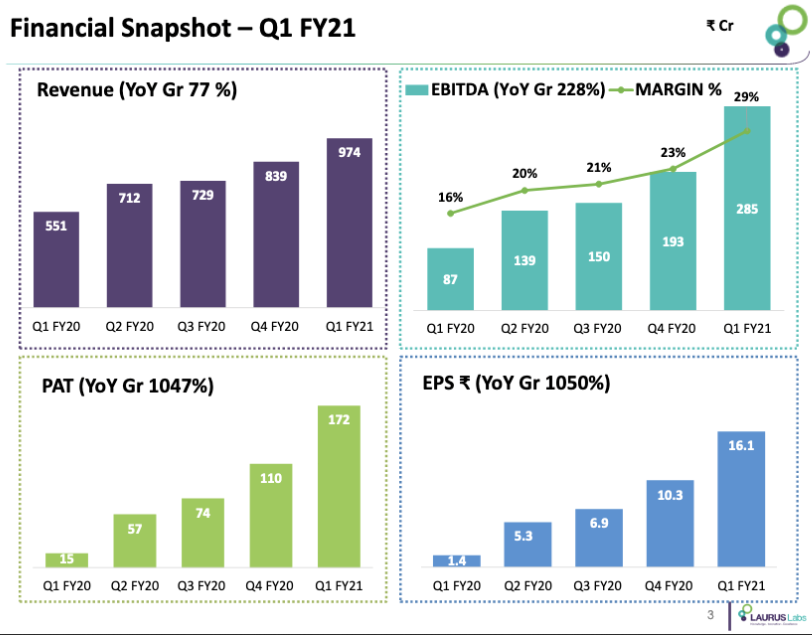

Operating leverage playing out in a big way in this company.

Revenue up 77 %

EBITDA UP 228%

PAT up 1047%

EPS up 1050%

The other interesting thing is that Standalone Profit is 159 Cr. and Consolidated profit is 172 Cr. For Q4 the numbers were 112 S/A v/s 110 Cons. So FDF (Finished Dosage Form) business, which had broken even last quarter now seems to be contributing positively to the bottom line after 5-6 years of capex.

Generics FDF contributed 36% to revenue this quarter at 352 cr. v/s 267 cr. in Q4’20 and 106 cr. in Q1’20.

Excerpts:

Acquired Aspen’s South African Subsidiary, in order to get a foothold in South Africa’s large ARV market

• RoW Markets – Received approvals for TLE400 and TLE600 from the US FDA

• North America – Sales were driven by launch of HCQ in US and increased volumes in the

US

• Europe – Entered into a long term partnership with a leading generic player in EU region

for Contract Manufacturing Opportunities

• All the green field expansion have turned Cash positive in FY20 with near maximum utilization

• Continue to undertake Brown Field Capex programs for Capacity addition in line with strong order book visibility and business outlook

• Brown Field capex in existing sites to have shorter payback period and ROCE accretive

• Doubling our FDF capacity by FY22

• Acquired assets of an API Unit in Vizag to be used for backward integration and pre-clinical chemistry

• With higher utilizations ROCE (annualized) improved to 32% Q1 FY21

Results conference call on Friday July 31, 2020 at 11:00 AM IST

Universal Dial-In +91 22 6280 1214

India Local access Number +91 7045671221 Available all over India

Singapore + 6531575746

Hong Kong + 85230186877

USA + 13233868721

UK + 442034785524

Q4 concall link

An interesting discussion on pharma sector opportunities with Madhu Kela and some other experts

I invested 21% of my (currently 1 stock) portfolio in this company after results. Was thinking of investing 10 or 15% of portfolio as valuations seemed to have run up. Now, even if we take Q4’20 and Q1’21 results and extrapolate for next 6 months, at 292*2 = 580 cr. of extrapolated PAT and 8400 cr. of market cap the PE multiple is 14.5 on a 6 month forward basis.

Thanks to Rupesh Tatiya, Hitesh bhai, Madhusudan Kela for bringing this stock on the radar.

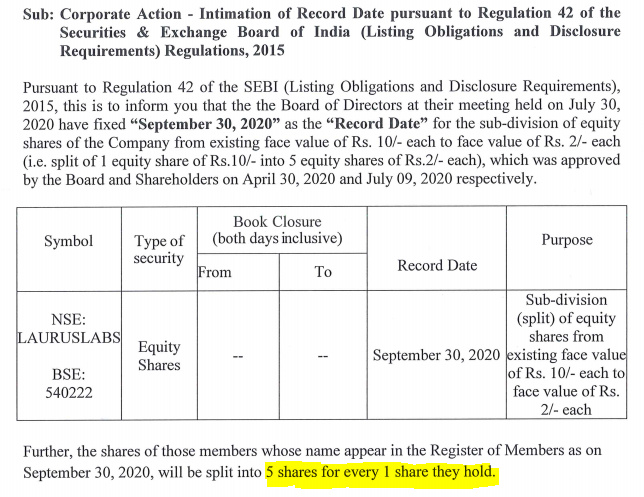

Stock Split :

https://www.bseindia.com/xml-data/corpfiling/AttachLive/c3fe3529-33ca-4df0-a691-1dccfcd7a43b.pdf

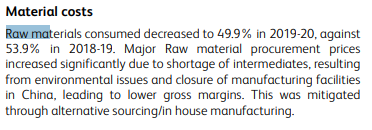

I have skimmed through the whole annual report for FY20 buy could not find information on what key raw material company use and how they are sourced?

On page 45, we have very brief mention of increase in raw material prices due to environmental issues in China. How much is company dependent on raw material imports from China and what are the key raw materials?

Below is from the concall dated 30-Apr-20, so they are definitely sourcing raw material from China. But what are these raw materials need to be explored?

If anyone has copy of RHP and can upload it will be great help.

I am not sure what are the key raw materials. But, I remember Dr Chavva mentioning earlier that Laurus uses 500-600 tonnes of IPA per month:

We have Deepak Nitrite in addition to Deepak fertilizer who can supply IPA locally.

Concall notes

Note : I may have overheard certain discussion. Please don’t consider it as sale/ buy recommendation and don’t let your actions influenced by above post