Brother request you to kindly read previous posts most of the answers have been satisfactorily answered by experts here, not possible to write in one message, Arv as assured by Dr Chava will continue fetching sale but there will be very modest growth, from this quarter there will be meaningful sales, as assured by other competetors also viz …Auropharma, even they see a recovery from Q42022 , but within 2 to 3 years Laurus will be in a very different league

Fdf, other api,Cdmo, bio will be substantially huge, massive capex going on i feel in the right direction, with very satisfactory corporate governance and best in classs leaders.

As paxlovid is not available worldwide there is now demand for Molnupiravir and Laurus will play it’s little role, also Laurus as per declaration is now supplying to a global life science, in just 20 days of notice if Laurus has declared it has to be significant we might get some colour in concall but high chances it can be for Paxlovid for Pfizer… Either Api or Fdf cause only this molecule is in deep deep shortage worldwide thus the rush , if not today tomorrow Laurus can play a significant role due to its expertice in Arv As (Paxlovid is a combination of Pfizer’s investigational antiviral PF-07321332 and a low dose of ritonavir, an antiretroviral medication traditionally used to treat HIV)

All in all exciting days ahead abhi to party shuru hui hai… . Also as it has huge inventory at end of Q3 which will be very handy in inflationary times. its finally your call if it’s giving headaches should sell and buy what gives you confidence and peace which is far more important

. Also as it has huge inventory at end of Q3 which will be very handy in inflationary times. its finally your call if it’s giving headaches should sell and buy what gives you confidence and peace which is far more important

Also please remove some time and go through The latest investor presentation given to Jefferies by Laurus labs it’s on BSE will get a glimpse of the future.

Just a request to all let’s also post a few posts on Thesis which we feel can pan out right with Laurus just to balance a bit of anti thesis, pointers are…Paxlovid,biosimilars,car-Tcell therapy,lab based meat, Cdmo growth,fdfs,other APIs…etc

Heavily invested and biased please DYOR no advise take care stay safe

I had attended Ami organics call post q3 result. And they manufacture intermediate used in manufacturing ARV API (Dolutegravir). This intermediate was among there top ten revenue contributor but not anymore now due to issue at the end market (destocking). However they did mentioned that the sales has again picked up in January qtr. Dr. Chaava also mentioned the same that in January qtr recovery will happen in arv api. Hopefully things are normalizing in ARV

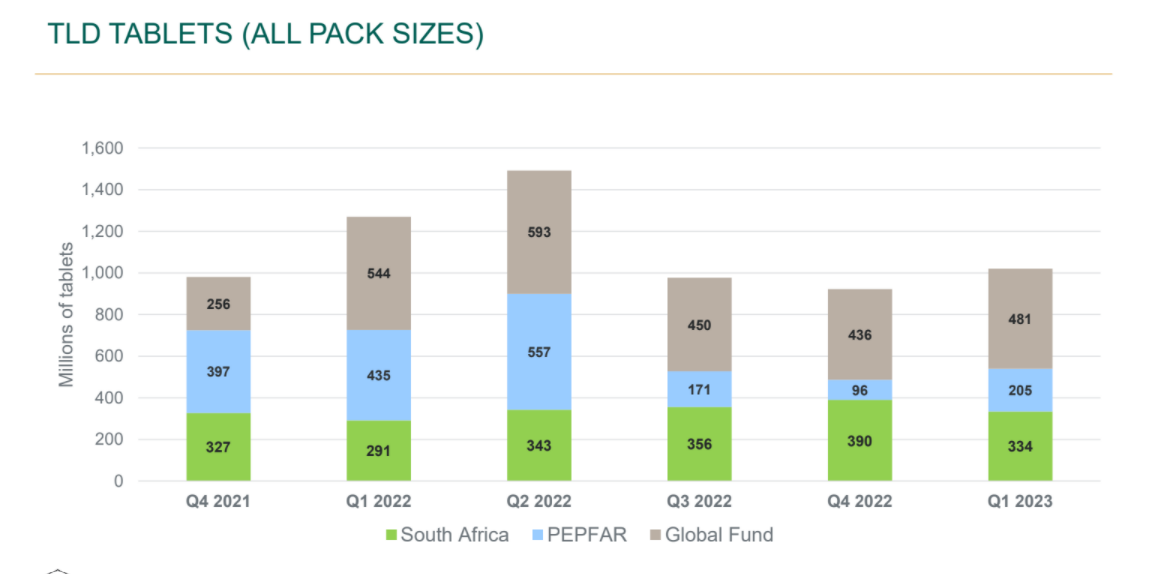

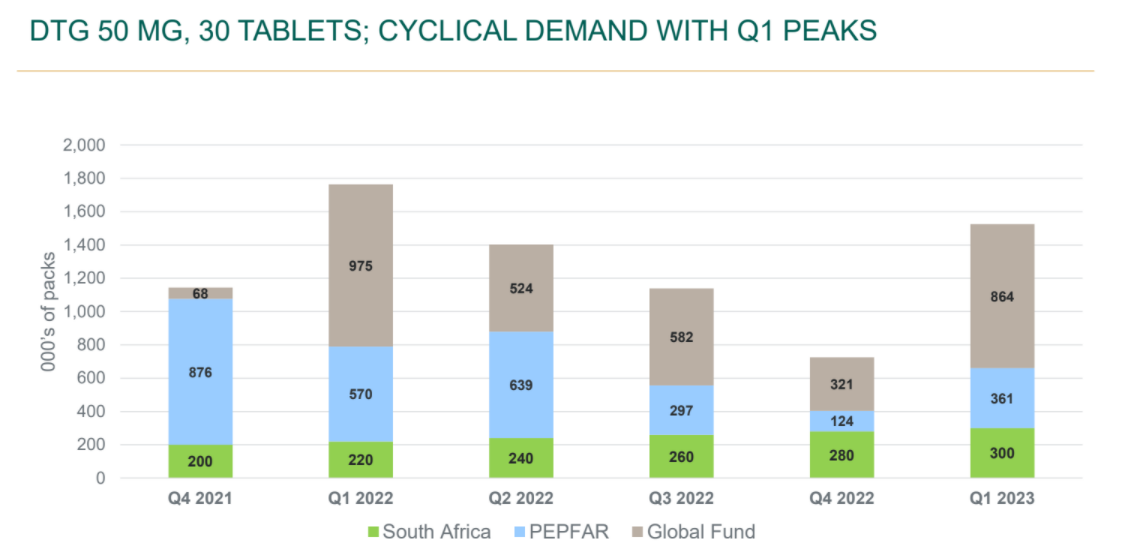

Sorry, but I think we need more details before one can equate Ami Organics’ Dolutegravir (DTG) API production and Laurus’ TLD, as there are some differences. While TLD contains Dolutegravir, it is available only in LMIC as dolutegravir alone is under patents in most countries.

I shared some data higher up in the thread, and one can see that Dolutegravir demand is not the same as TLD demand.

So I would first ask whether the DTG Ami Organics’ produces goes into the D in TLD, or DTG tablets. If it is the former, then we need to ask if Ami and Laurus cater to the same end markets. If it is the latter, data suggests that DTG demand from SA,PEPFAR and Global Fund alone is strong in Q4FY22 (Q12022 in the chart).

Ami organics don’t produce DTG. They manufacture intermediate used in making DTG. Laurus is there customer

Awesome…I really want to hang on with Laurus…But sometimes I feel…many things that you talked about is around “hope”…There is 50:50 chance of them happening or not happening…So in nutshell, its turning out to be a cyclical bet, more depended on future probabilistic events than the structural play. And the risk reward ratio is at the most balanced one…not skewed in my favour for a long term bet…Still waiting for atleast 2 more quarters before jumping the gun…Thanks a lot for your kind guidance…

Dear Mudit,Thanks feel its a wise decision to wait for 2 quarters so you can get a clear picture, might be i don’t agree this is a cyclical bet, or only 50 percent chance, I feel this will get better as years roll on surprising most in sunrise sectors of Cdmo and Bio, but that’s market and i respect your opinion what i see here in a nutshell is …

Just in a few years from pure Arv successfully transitioning to other api,Cdmo,Bio,FDF, i personally feel in Bio and Cdmo they will overshoot

Plus if from Arv they have diversified so well, can rationally expect they will surely invest in more exciting relevant things in future even they are getting better after every acquisition.

Very decent Ebita margins better than most and assurance of continuing, very good focus on research, my forte is not no crunching but am more sort of intuitive investor and see 2 things very strictly

- Business Model, and i love the one Laurus has , model with long term visibility for growth

- honest, adaptive, visionary , technocratic founder and other key management individuals… Who think on a massive scale , and having capabilities to conquer the vicissitudes which businesses at intervals always throw at you.

Having said that if fundamentals change will change my thesis so far am more than satisfied, my job is just to sit and let Dr Chava sweat it out for me😉 Invested so naturally biased DYOR take care

I cant agree more on what you just said about the thesis for investing in Laurus labs.

As you rightly pointed out, they have demonstrated and demonstrating their ability to invest in more exciting things, even though it is too early to say - investments in ImmunoACT , an advanced cell and gene therapy for cancer is an indication of what to expect from a visionary leaders like Dr.Chava.

Laurus approach of keeping facilities and infrastructure ready; even before having their customers signing in for the works speaks the level of confidence and aggressive risk taking abilities (That too in Pharma space). They have characteristics of an IT company in pharma space, which can help them grow at the pace of IT businesses.

I see a long runway ahead of Laurus,

Invested and position size here Businesses with 'MOAT'. Investment Strategy & Discussions

Laurus Labs is one among the 19 companies to receive licence to manufacture Plaxovid and supply worldwide as per this article specially Lmic countries where strength of Laurus lies as said earlier there is huge demand for Plaxovid thus market size is also huge

We have to be very cautious of this narrative of Molnupiravir, Plaxovid I have not seen anyone using any of these medicines prescribed by their GP. It is fair to say we are entering into the stage of endemic, this will be like any other flu. In the developed markets they take flu jabs every year, like this they will be taking covid jabs. People who are infected are not being admitted to hospitals, they are recovering quick and fast. If at all one has to bet on Covid related revenues then it is the vaccine that has the potential , oral medicine will not generate any kind of revenue as such as long as it remains as a prescription based medicine. (If it is available as a OTC then it is a different story )

Rafi Bhai Laurus has stated many times they are not dependent of Covid associated medicines, infact in their aspirational Target of 1 billion they have not counted income from this as far as i can recall, this IMHO is just extra income but beneficiary for both Patients and Companies, and validation of the capabilities of Laurus, having said that any Google search will tell us there is lots of shortage going on for this molecule and also in few places covid is still creating Havoc, and plaxovid is a very prefered medicine approved by all countries and having very good efficacy rate, specially Lmic countries who can now get access which they deserve.

So countries will prefer to keep enough stock for future, cause nobody can predit the future, pray no new variants come , and pendamic is over, but wisdom says have to prepare for the worst, so there can be good sales atleast for this molecule, but We will get idea only in the concall.

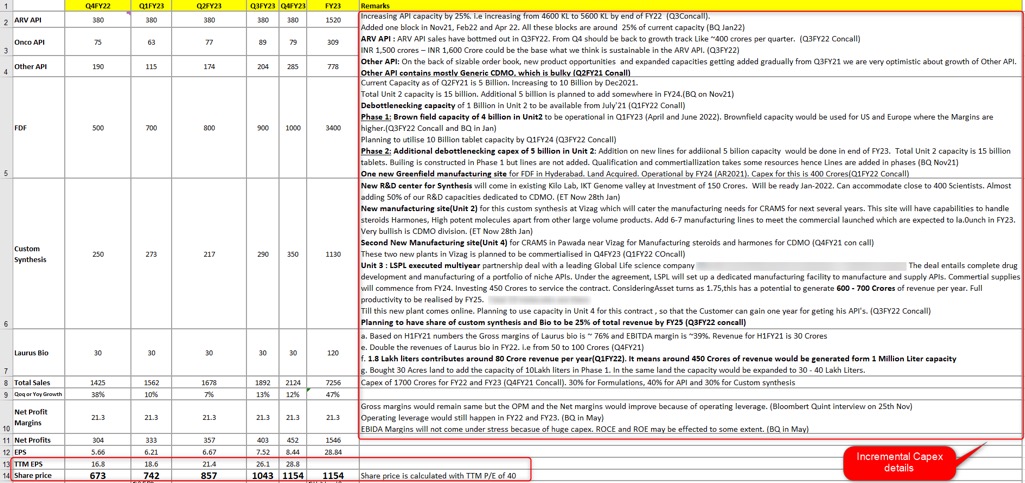

Attached are my projections for next 5 quarters…

Below are the future triggers

-

New FDF capacity of 5 Billion tables to be utilized in FY23. This new capacity has potential to generate ~ 1800 Crore Rev.

-

New Contract signed by LSPL for manufacturing Niche API for global life sciences company. Capex for new site is 450 Crore. (Source : Q2FY22 Concall). This has a revenue potential of ~800 Crores (Considering asset turns 1.75)

-

Add 1 million liter capacity every year for Bio for next 3 years. Purchased land of 30 acres to add capacity of 3 million. (Source: Q3FY22 concall). 3 million capacity could generate 1500 Crores of revenue

-

Add additional 5 billion capacity for formulation division in Unit-2 in Vizag in FY23 (BQ interview in Nov’21)

-

Two products will go commercial from Phase 3 in CDMO division in next 2 years (Source : Q2FY22 Concall)

-

Two para-4 and Seven first to file to start generating revenue in FY25 (Source: Q2FY22 Concall)

-

Shift from ARV to Non-ARV and from LMIC markets to Regulated markets Margins would improve going forward because of shift towards Non ARV / Regulated Markets / Bio. Significant diversification to non ARV and to regulated markets happens in FY23.

-

New Covid drug Paxlovid must be combined with Ritonavir to keep drug active in body for longer duration. Laurus is Leader is Manufacturing Ritonovir. Laurus also got approval to manufacture Molnupiravir (But this is highly crowded as many companies got approval for this drug)

-

Share holder value creation by listing Synthesis separately

Over all Laurus is Lethal combination of high growth and high ROCE business available at resonabke valuations

Regarding point number 4… Additional 5 billion tablets capacity would be added in FY24 (Not FY23)…

What is the revenue potential for this FDA nod?

Satyanarayana Chava - "We have very long term commitments with global pharma & WHO like agencies so we have challenges to pass it down to customers but because of our scale, we’re able to manage the impact much better than many other companies.

Challenge came especially in solvents where petro driven solvent’s prices went up significantly, coupled that with logistics challenges coming from China, we have some impact but managing very well"

Key guidance based take away - $1B by FY 23 , removed Aspirational as this is realistic now, despite headwinds - confident of 30% Margins. ARV off take and visibility good in current Qtr and next Qtrs( we are at end of Qtr).

Strength visible in charts. Insider buying also in recent days.

All fingers crossed

Constant hammering of the 1 billion target is a bit uncomfortable. If they are able to achieve it, markets will not be surprised as it is priced in, if on the other hand, they miss the target, markets will not like it, as it is a negative surprise and likely to hammer the stock, imho. disc. Invested, views maybe biased.