Interesting data points in Navin’s concall today:-

Navin expects its KSM business for ARV Apis to pick up fully in H2FY23.

They have seen the commentary of one of the largest ARV player (presuming Laurus) about demand recovering.

If demand is recovering according to the large player, till now Navin hasn’t seen any pick up in supplies. However, this could also be due to the fact that inventory that has been built is being consumed currently.

Worst is behind, but given the commentary from Navin’s management. Full pick up of demand from their end for KSMs is expected by H2FY23.

Actually Navin warned us of the demand slackening before the results of Laurus were last announced. In their spechem business, supply of KSMs to ARV is a large portion. They saw growth challenges in Pharma division of spechem because of this.

Prima facie it looks like we have two contrasting data points? TLD data from ARV summit tell us that Q4FY22 and Q1FY23 should be stronger quarters than H2FY23. If we’re discussing APIs alone and not TLD tablets, I’m looking at the South Africa data, which looks flat throughout FY23. The questions then are whether Navin or Laurus is the leading indicator, how much of an overlap they have in end geographies for the ARV business, or if it’s a matter of inventory as you’ve suggested.

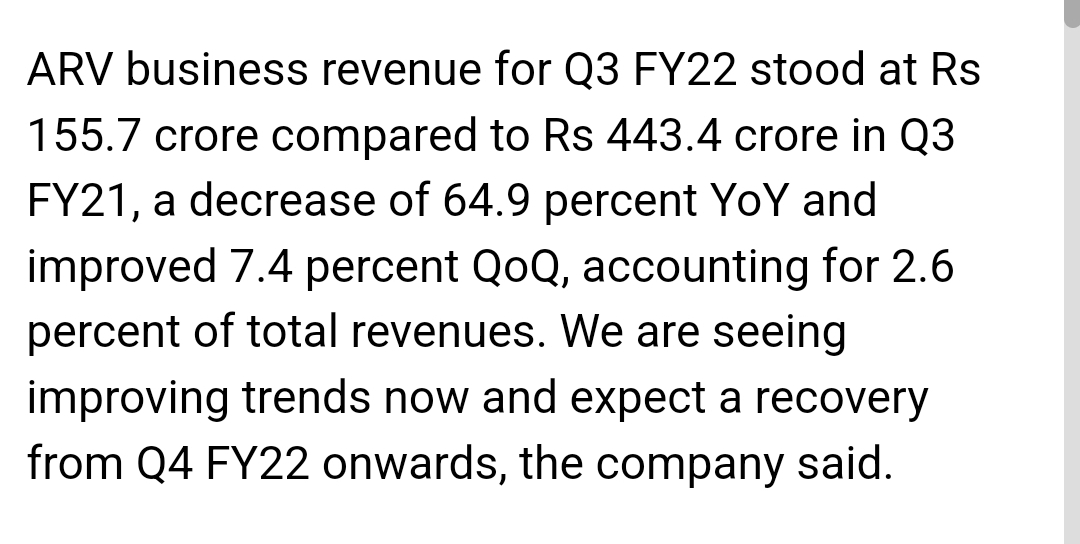

Overall, it looks like there’s consensus that the worst is behind for ARV: tender data, and both commentaries. Question is of how fast demand ramps back up. Now, or in H2.

Can be a little hopeful from this commentry after Q3FY22 results from Aurobindo Pharma that Arv sales can pick up from Q4 …source CNBC TV 18.

Disclosure : Invested

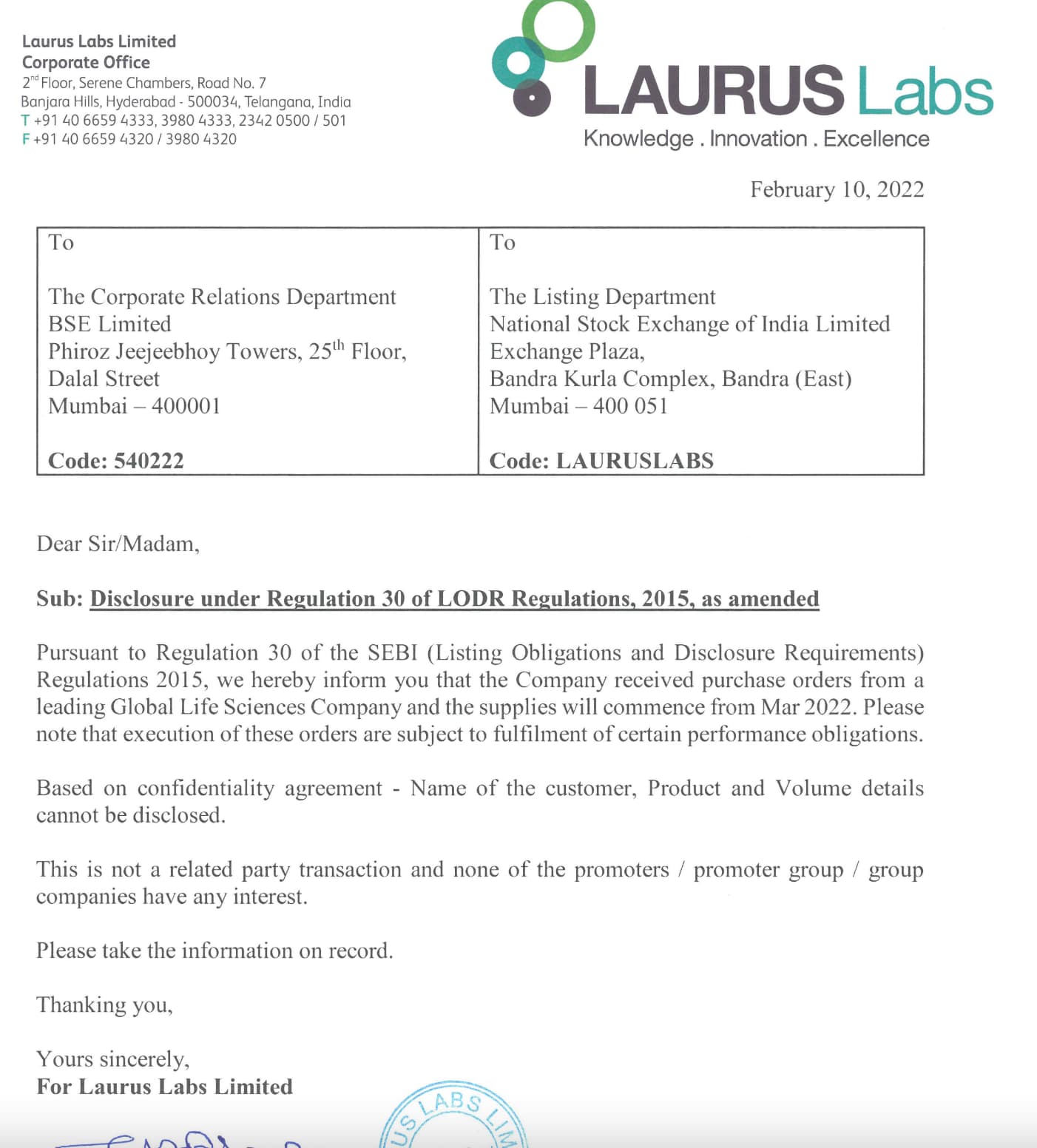

Laurus never gives such vague unusual declarations, on basis of tracking it since last few months they are pretty responsible.

Says a global life science company with whom Laurus does not have any prior relation before and wants to start supplies after say 20-30 days in such short period can’t be crams or a new molecule has to be something in which Laurus is a expert n can ramp up soon n fast , so as per rumours in market the needle points out towards paxlovid, as there is huge demand and lots and lots of shortage, so the hurry.

Laurus can be a ideal partner due to its huge expertiese in Arv and ability to scale up fast.

Also volume n price increasing abnormally in down markets but that can be due to rumours, or institution buying.

Relatively new to pharma so folks who are tracking Laurus since a long time can guide, just trying to read tea leaves here can be horribly wrong just my thoughts, heavily invested so biased no reco take care

For such short notice I think this could be related to covid-19 oral drug as its needs of an hour as they have mentioned. I am just trying to connect the dots… I may be wrong…

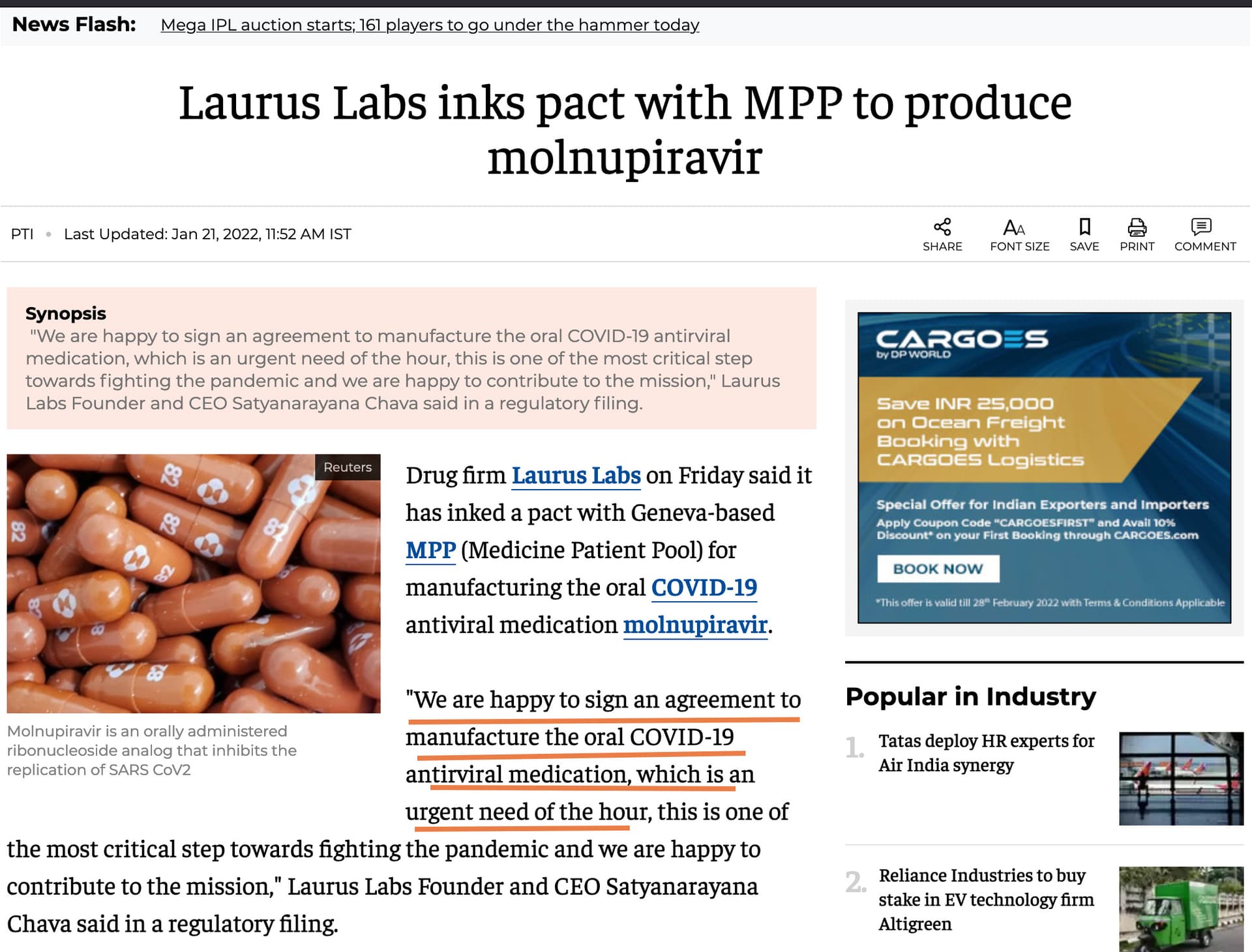

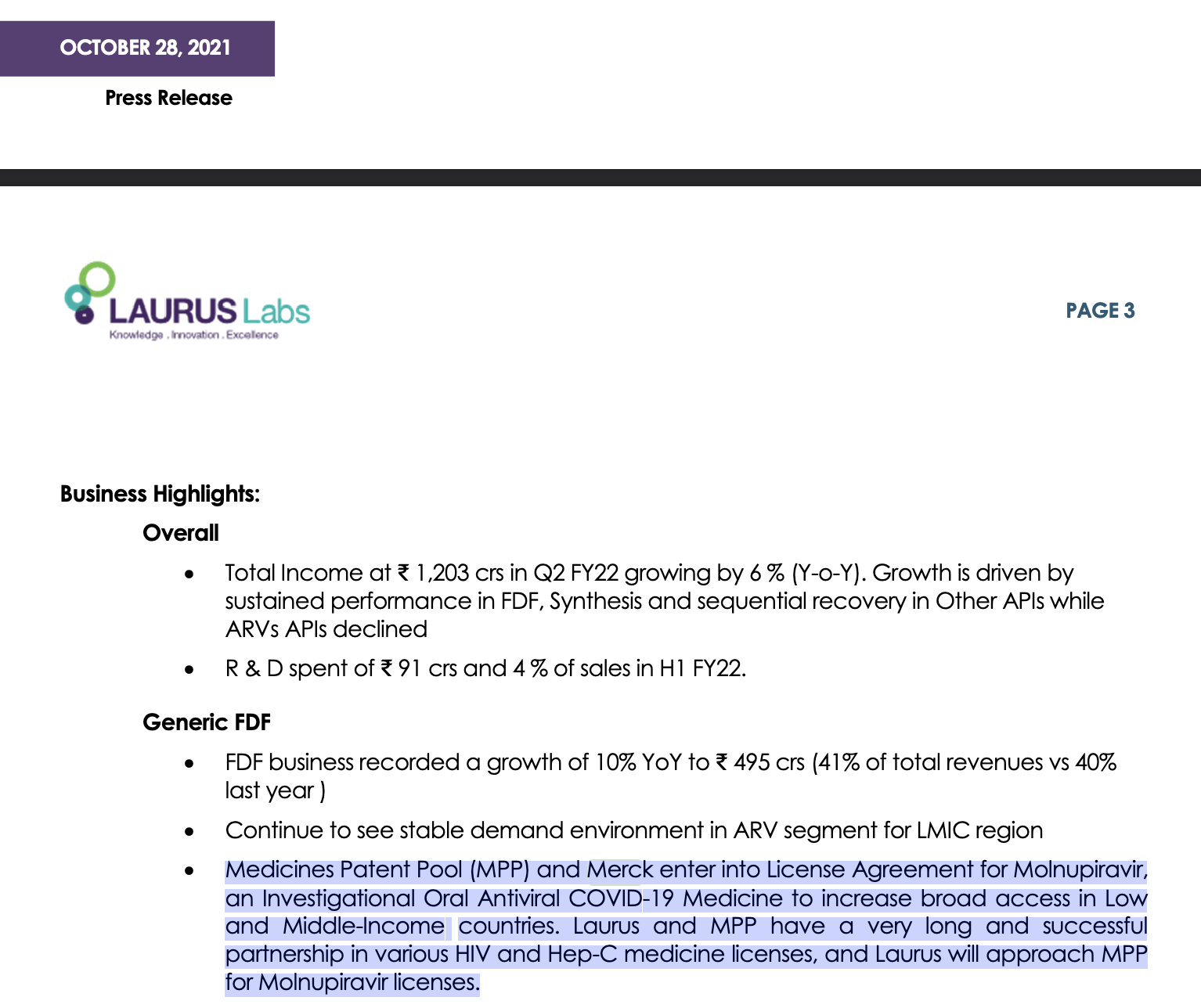

Twenty-seven drug makers have signed onto a deal to manufacture a generic version of molnupiravir, Merck’s oral antiviral for the treatment of COVID-19. The deal will allow affordable access to the drug in 105 low- and middle-income countries (LMICs) around the world.

Bhai …My finger is more towards Pfizer (Paxlovid) for API or Fdf which is in huge demand and great shortage had it been for Molnupiravir all companies making Molnupiravir would have seen push strangely it’s companies even after having bad quarters but having expertise in Arv n can scale up (Paxlovid is a combination of Pfizer’s investigational antiviral PF-07321332 and a low dose of ritonavir, an antiretroviral medication traditionally used to treat HIV) which are getting this push viz Aurobindo also, think now Arv is a boon rather than a curse just kidding😉

Laurus already has tie up for Molnupiravir through MPP and Dr Chava said the revenue as of Q32022 are not meaningfull (but can change as due to shortage of paxlovid customers are going for Molnupiravir as efficacy of Plaxovid is better) and the street knows this so signing up again with Merc directly won’t give that cheer IMHO, all these are just my wild guestimates market can easily prove me wrong, take care

On his call with Bloomberg-Quint, Mr. Chava said that Molnupiravir is unlikely to be big opportunity for Laurus Labs; reason given was too many approvals & other factors. But still, it’s good to know the company is making inroads. Thanks for sharing. Also, if you or anyone has any views on any surprises in this regard please do share.

This has been discussed here multiple times but sharing a research report on impact of mRNA on ARV business and impact on Laurus. Free to access report from BOB capital( hopefully no issue in sharing) Pharmaceuticals-SectorReport15Feb22-Research.pdf (2.0 MB)

I am a layman as far as pharma is concerned as well as most other subjects. Luckily there are quite a few excellent and very informative postings by brilliant minds on this thread.

It would be a very happy day for humanity when HIV drugs are no longer required. However in my opinion it is premature at this moment, to think that ARVs are going away or even starting to reduce any time soon. Every year the number of patients is rising by 5% due to new infections and we are losing 2% to death with the result 3% annual increase in patients. Even when Vaccinations start hopefully in say 3 to 5 years down the line, it would be targeted at uninfected population surrounding present 4.5 crore patients in the current geographies and current demographics. So are we looking at 100 crore vaccinations ? Could be more. Very expensive and time consuming task requiring additional funds and additional sponsors. And it would not be an easy job as the jab would carry a latent suggestion that the recipient is a possible candidate to indulge in unsafe social conduct.

Therefore in my opinion I do not see ARVs experiencing a start of declining trend before 10 years. The pharma companies to opt out first would be those who have marginal market share, making them uneconomic earlier, thus vacating space for companies like Laurus and Hetero.

In another 5 years max, Laurus should itself be diversified enough to comfortably absorb any decline in ARVs. So the future of the company is certainly not under a cloud. On the other hand these possibilities have clearly triggered Laurus onto a much better path leading to a much wider canvas where better sustainability, higher profitability and newer moats can be created.

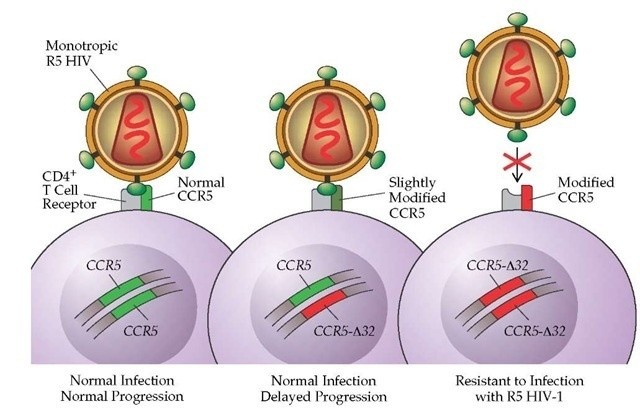

HIV causes AIDS by infecting the white blood cells of the patient, specifically CD4+ T helper lymphocytes. HIV enters into these lymphocytes by attaching with some receptors (proteins) found in the membrane of the lymphocytes. One such receptor is CCR5 receptor, which is like a door for HIV to enter into lymphocytes.

In very few people, the gene coding for CCR5 receptor is defective and they will be having abnormal CCR5 receptor. (We all have 2 genes which codes for a single protein and both these 2 genes which codes for CCR5 receptor have to be defective, called as homozygous condition)

Therefore in people with this very rare condition where CCR5 receptor is altered, that means ‘the door’ for HIV to enter into lymphocytes is altered and virus can’t infect that person! This is a very rare inborn natural resistance to HIV infection.

In this particular case, the lady(patient) had both leukemia and AIDS. For the treatment of leukemia, lady had recieved blood stem cells from a particular donar who by chance was resistant to HIV infection. Thus the stem cells the lady received had produced lymphocytes which are normally resistant to HIV infection. (due to altered CCR5 receptor). This is a very rare incident and only 3 incidents like this have happened in the past with a cure to HIV infection.

Giving this very rare stem cells to all HIV patients is not a viable option now. However studies are going on to alter the CCR5 receptor in lymphocytes by gene editing. IMHO this gene editing option may take significant time as further consequences and off target effects of gene editing has to be studied.

It is worth mentioning that in 2018 one chinese scientist named He Jiankui, had announced the births of twin girls named Lulu and Nana from embryos that had been genetically altered (CRISPR based genome editing) to resemble those with the CCR5 delta 32 mutation which had created a great controversy among medical community regarding it’s ethical aspects.

If more companies are opted out of ARV and at end if Laurus be last very few player in it will be good for the company as competition and margin will go towards South and North respectively, It will have boring, predictive but good margins.

A good article on Dr Chava …

Key Highlights…We want to become a leader in the products we make, that’s our philosophy,” says Chava. Laurus Labs puts a lot of products for development, but also kills many if it realises it cannot become the leader in the segment. “We don’t want to be a fifth player or 10th player, we want to be first, second or third in the market share for that product,” says Chava.

“Dr Satya loves to call himself the founder and first employee of the organisation rather than a promoter. As a founder and the first employee, he never held 50 per cent stock. He believes that after a certain [point], there is no value [of] money. His passion is the subject of Chemistry. Applying knowledge on a commercial scale is what makes him a successful leader,” sums up Kumar

with ARV business in API as well as Formulations is undergoing pain and in forseeable future, it may not come back to earlier levels, due to global tendering process mthodology…also foray into formulations, which is very competitive and new area for Laurus Labs, where it may be competing with its own API clients…I am losing the confidence in overall thesis. Disclaimer : I am invested into it and its my second largest holding in my portfolio …can you elaborate, am I missing something? is this a secular story going forward, for next 7-10 years?