Think you might have missed some of the subsequent replies.

One of the entities pharmacare is laurus subsidiary.

Think you might have missed some of the subsequent replies.

One of the entities pharmacare is laurus subsidiary.

I think best way to look at this data is in terms of YoY annual growth. My sense is arv demand would be growing at low single digit YoY.

This is a lumpy biz. High demand in some quarters, low procurement in others.

A couple of critical questions for laurus investors:

Can the combined growth of non arv api & cdmo compensate for the lack of the growth in arv segment ?

Disc : invested, and definitely looking for some answers tomorrow concall. Will try to work on arv demand forecast annual YoY basis as well.

An important point to take note of is that ARV API sales are down from 570 crores in Q3 FY’21 to 203 crores in Q3 FY’22. You may choose to look at it from either the prism of overall API revenues going down significantly (negative) or the dependence on ARV’s as a portion of sales reducing(positive).

Next quarter, the ARV API sales should be back above current levels, but the important metric to look is the 60% growth in CDMO sales YOY. As we know, CDMO is margin accretive and if Laurus continues to scale this up, it can be a great lever for future growth. Not to forget, the recombinant protein space with Laurus Bio also presents a huge opportunity.

CDMO is margin accretive but is it predictable ? Is that not Lumpy business ?

How an innovator will look at Laurus when they want to offer a CRO / CDMO opportunity to Laurus where in the end product (therapeutic) market Laurus is also can become competitor ? (Not necessarily same like to like formulation )

FDF : What is that unique edge that Larus has in this space, these must be like any generics (few of them might be F2F or choosing complex molecules like Natco ). These drugs are sold in India or out of India? All the big Indian generic players are struggling to maintain margins in cut throat US market. More or less same is the situation with margins in other geographies.

API : Divis success is because of its “Pure API Play” , they never wanted to get into formulations at all. In Laurus case why a Formulator buy APIs from Laurus and then compete with them in the formulations market ?

Disc : Invested, looking for anti thesis pointers

Anyway you cut it, answer is clear:- Demerger of synthesis division once the size grows to a certain scale. Like what happened in the case of Syngene.

Difficult to serve the customers you end up competing with in one division.

Comparison with Divis isn’t apt for Laurus. Incrementally just looking at the capex spends, its going more towards being a vertically integrated formulations and Api business like :- Dr Reddys, Aurobindo Pharma or Alembic Pharma. An apt comparison of valuations should be and has to be done on a SOTP Basis,

Where you look at each segment and the look at the peers. Then check the relative valuations.

Is this investor narrative? How can Dr. Chava go to a US innovator and ask for outsourcing their patented drug molecule while undergoing a patent litigation at the same time? Currently, he is the face of the company.

In the case of biocon and syngene, Syngene used to be only a CRO (which is different from a CMO). Only now is Syngene trying to get into CMO and offer more integrated services. Whats their right to win there also remains to be seen. The question I would ask is Do we have any global example of a generic company that sells formulations, does Para IV while also manufacturing patented molecule for innovators? If yes, who?

There are examples of generic CMO manufacturing, but none of patented molecule manufacturing. Generic CMO manufacturing is nothing more than job work unless its some niche skill (like lyophilisation or sterile manufacturing). Even differentiated delivery methods (like delayed release capsules) which used to fetch better realisations in 2016 have started to lose their competitive positioning because now everyone does it.

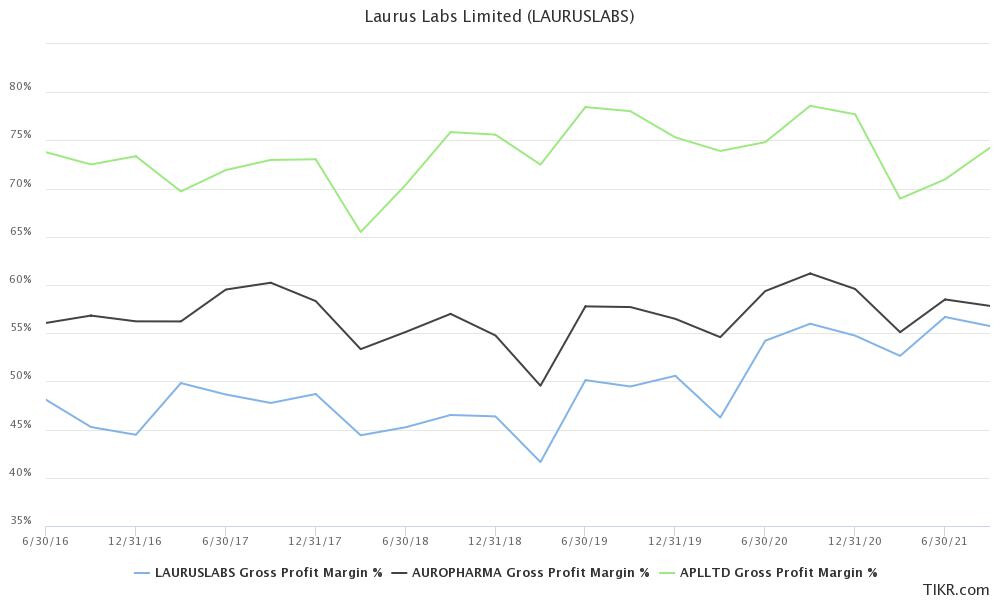

I don’t think Laurus should be benchmarked against Alembic Pharma as Alembic’s gross margins are north of 70%. Plus, Laurus doesn’t have any branded business. The correct benchmark for bulk of Laurus’ business is that of a low cost manufacturer like Aurobindo. The main difference b/w the two is that Auro’s strategy is to be lowest cost producer by building massive scale whereas Laurus tries to differentiate itself using process chemistry. Also, Auro was a very key customer of Laurus. This is also reflected in gross margins, Laurus’ gross margin profile is similar to that of aurobindo (55-60%), whereas Alembic does 70%+ gross margins (similar to a specialty company like Sun, Ajanta, Natco or Torrent). Alembic’s operating margin looks lower because of their very high R&D costs (14-15% of sales vs 5-6% for low cost producers like Auro and Laurus).

Also, we should differentiate b/w the product profile a company is selling from being an integrated manufacturer. We have companies like Ajanta that get 30% of sales from US and still do 70%+ gross margins because of product selection (without producing a single bit of API). An integrated company like Cadila or Lupin does 60-65% gross margins and 20-22% operating margins. I don’t know if Laurus’ operating margins are sustainable as I haven’t been able to find a single US generic formulator that has <60% gross margins and >25% EBITDA margins sustainably. I think Laurus did these kinds of EBITDA margins in last 6 quarters because of their tender business which doesn’t require a large frontend investment. If future growth is coming from US generic formulations, then EBITDA margins will come back to 20-22% kind of levels unless gross margins increase significantly.

This is not investor narrative. If you look carefully, they are already doing manufacturing for patented molecules under their CDMO Division…

Haven’t seen any other listed company atleast in India which has a similar business of selling generics and CDMO for patented molecules under one roof. Demerger plans aren’t investor narratives, already mentioned in BQ Quint interview.

Alembic follows a vertically integrated Formulations strategy, which is what Laurus seems to be doing in the ARV Api business atleast. Compared it from a strategy point of view (read again)

No peer is perfect, just rough comparisons.

Good point on margins though for US business

I didn’t mean to sound dismissive, I have also followed all their concalls. What I have struggled to grapple with is how and why are the only generic formulator that has a sizeable CMS business with innovators. They have previously mentioned that they are not into FTE services (see screenshot below), still somehow able to (potentially) crack commercial manufacturing. Have these relationships being established by someone who already had expertise in this?

About margins, it has to do with product profile, market share and not backward integration. Atleast, that’s what the data suggests.

Can be a good exercise to check Dr Reddy’s CDMO Scale before they sold off the business:-

https://twitter.com/i/broadcasts/1lDxLLepzOYxm?t=9yg03FZ7LX4Laze-vrz98Q&s=09

Niraj Shah interviewing Dr.Chava on Q3 results.

It has been a great investment for me and with 3.5x return I sold my shares today.

Revenue degrowth is the biggest issue for me. All others had also faced raw material, freight cost issue but laurus has been showing degrowth in revenue too. All other businesses CDMO, Bio, formulations these are far in the future. Moreover, with Pharma sector out of flavour and with these kind of result, it will be difficult in the near future for Laurus Labs whereas other sectors like IT has corrected after posting very good result.

Expecting demand comeback in q4fy22. Maintain guidance of 1B$ in fy23. Only contingency is approval for new ANDAs. Arv demand decreased due to inventory stocking until now. Normalization seen in q4. Dolutegravir remains standard therapeutic, expected to grow, including in pediatrics. Market share of other therapies won’t go up significantly in fy25. 50% of revenue coming from arv rest non arv now. (My notes : this has been 70% in recent past). Tender for next 3 years will come in near future. Haven’t gotten it yet. Some part of arv inventory will get liquidated in Q4. Arv Formulation declined 20% arv api 45% in this Q. Can sustain 1500-1600 arv api annual revenue base in next 2-3 years. 1-2 new players might get into formulation space but don’t see any new arv api player coming in next 12-24 months.

3 ANDAs files in 9M. Will file 3-4 more in Q4. 30 andas filed, 10 approved. 8 tentative approved until now. Oher api we have added only 1 molecule this year. There has been delay in approval for non arv api approvals (my notes : probably due to COVIDbppstponing regulatory actions). Diabetic cardio are two areas we are expecting approvals.

Capex: Capex execution is on track. 25% of our gross block is not yielding any revenue right now. Formulation capacity will almost double from current capacity to what it will be early in next year.

Multi product multi year contract is funding part of the cdmo capex. Commercial advance. Completing valuation of NCE in our own unit 4 block. Will transfer it to partner funded capex block when it’s finished. Have all qualities to become very large player in cdmo. 200cr runrate is not large at all. Look at global cdmos. By fy25 we want cdmo to be 25% of revenues including biologics & chemical cdmo. Total synthesis can be 3-4x larger in 3 years (25% of 3 year forward revenues). 2 products can go to commercial in next 2-3 years. One of them we are single source.

Many for licences from MPP for molnupiravir. Icmr didn’t approve. Biz won’t be meaningful for us.

We will get back to normal growth trajectory in q4 even if arv is a little below q4fy21 500 cr runrate because of all other biz divisions firing. 1B$ sales target for fy23 is in tact.

we got several enzyme orders. Richcore investment Thesis is playing out. Wil be 40cr quarterly runrate. Planning for 2 million fermentation capacity in 2023. Already taken land. Talking to customers. Phased manner we will create it. In fact land can accomodate up to 3M fermantation capacity.

invested in r&d and capacity much ahead of actual biz. Our r&d investment has been constant in absolute. But % of sales it has gone down. Same for manpower costs. That is the operational leverage which has led to ebitda margin expansion. Gross margin improvment is because of expansion of non arv sales. Yoy gross margin is up 5% operating margin down 4%. There is aspect of operational deleverage (lower sales). Gross margin improvement is because of product mix. Arv api is low gross margin.

I wanted to ask a few questions that i did not get to ask in concall. Does anyone know email id of laurus investment relation or someone in laurus management i can email to get questions answered?

Disclaimer: invested, biased, adding.

Laurus conf call Q3 jan 22

3 ANDAs in 9 months

11 product approvals in canada

2 product validations in cdmo

capacity on high potent areas, unit4

CDMO- we had strong growth. Dedicated facility, multiproduct, multiyear contract with large life sciences company. Part of the capex from advance payments.

creating dedicated r&d, dedicated manufacturing facility. Sales are not big now. But we have all qualities to become a bigger player. Have abilities to grow. biz is at an infancy stage. 200 crores this quarter- very small for our capacities & aspirations. By FY25 cdmo revenue is expected to be 25% of total revenue. We are building dedicated facilities. 2 products may go commercial in next 2-3 years, where we are the only supplier. Not all projects yeilds significant revenue.

Can’t give margins of cdmo. Margins are higher than corporate average.

BIO - total capacity of 180KL.

We are making several enzymes for chemical synthesis. Working on classical manufacturing of steroids. 2 million capacity by FY23.(We have the land; phased manner by 1million+ 1 million+ 1million)

1 BILLION SALE BY END OF FY23

In API space, november to april this year, we are adding 25% more capacities than what we already had. Formulations capacity has doubled. Regarding the factors helping to achieve this aspirational target, first one is capacities, 2nd is approvals & 3rd is customers. We have the additional capacities now, approvals are coming, customers are happy to add. That’s why are confident on this number.

Other api- only added 1 molecule this yr. growth came from contract manufacturing to customer in europe. expecting approvals in diabetes & cardiovascular space- europe & north american markets. Diabetes and cardiovascular space is the driver for other api & formulations business.

Molnupiravir - business & sales are not meaningful.

Q4 ARV sales are expected to be normal.

subsidiary - one of them generating revenue. not one off kind of revenue.

50% revenue is from ARV API& FORMULATIONS now.

In the formulations space, we are expecting 2-3 new players coming in the ARV market. Pricing has corrected in arv formulations. (1-2% reduction). There was 20% decline in ARV formulations revenue.

4 Billion capacity formulations- one inspection has concluded & was successful. One is expected on may and is on track. Revenue may be coming from june this year.

Global arv tender- it will come. (answer was not clear)

gross margin improvement is due to growth in non arv business. reason for ebitda expansion.

ARV demand will come up all of a sudden. 1500 crores is sustainable for next few years. (This is less number than past quarterly revenue of around 550 crores)

Gross margin improvement and ebitda decline YOY- This is because of operational deleverage. Gross margin improvement is due to change in product mix. 25% of gross block is not generating revenue.

Status of debt- by march it will increase. Next year it will decrease. 715 crores now.

Will keep it simple, market is valuing laurus at 18X TTM EBDITA currently , after 3 qtrs of relative subdued growth. Punished on all parameters discounting current performance.

FY23 which is just next 5 qtrs, management still maintains 7500 cr revenue and 30% EBDITA target. Implies 2300 cr EBDITA I.e. 45K cr mkt cap from current 25K cr mkt cap. Can adjust for some buffer.

What makes them think they can achieve abov delta of $350 M from current TTM base , Have capacities and customers, approvals are work in progress.

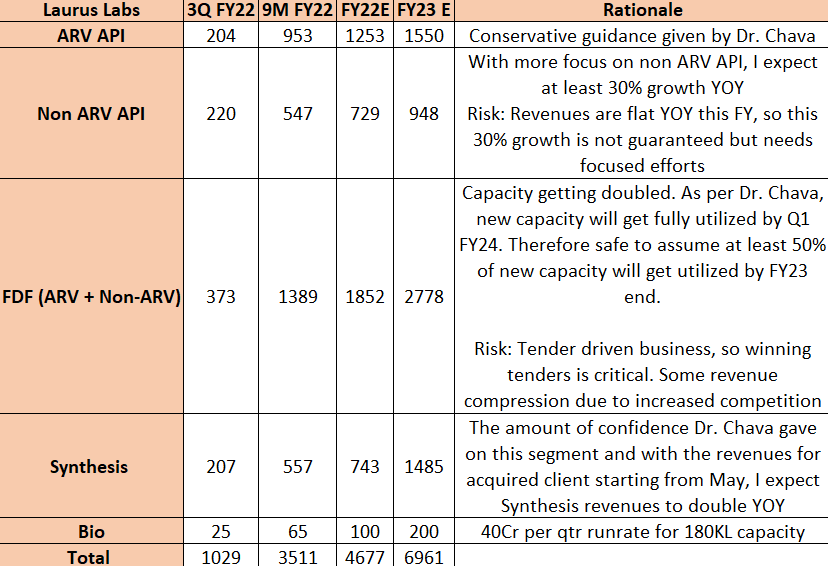

Break up of $1B in FY 23

API at 2500- 2700 cr

*Formulations at 3000 - 3200cr

Synthesis+ Bio at 1200 -1400 cr

Story is already tilting in favor of next leg of journey , Arv to not Arvis already 50:50, Non arv part is only going to increase here onwards, thus GM increase. Synthesis and large CDMO sticky and more predictable.

Lot still hinges on Mr Chava words and pending Formulations approval, usual pharma line risks apply. Should discount a bit from mgmt guidance to be safe.

Invested, plan to add closer to Q4 delivery+charts.

Re-assuring call for Laurus Labs. Based on what Dr. Chava indicated, these are my base case numbers for next FY:

In spite of such high operating de-leverage, Q-o-Q EBITDA margins have more or less held, thanks to higher gross margins from Synthesis business growth. Q3 gross margins are at 59%. As % of CDMO business moves to 25% by FY25, these gross margins can easily inch up towards 65-70%. USD 1bn in FY23 may be a bit of a stretch but falling short of that by a few 100Crs is far from a debunking of the investment thesis.

Key risk in this hypothesis is disruption of ARV business via injectables. Some questions needed to be asked to Dr. Chava today on the call regarding injectables, but I didn’t get the chance:

What will cause me to change my views on Laurus towards the negative?

Right now I think recent price action is a good opportunity to buy in tranches. Post Q4 results, situation needs to be re-assessed again. As I write this, Laurus has rebounded around 7-8% from its low today (Dr. Chava’s words?)

Invested at 500 levels, did not add at 450-460 levels as I was waiting for Q3 concall. Plan to add 10-20% of present holdings between now and Q4 results.

i think u should listen to the bloomberg interview posted above…

He has answered why he doesnt consider injectibles as a threat yet…

What he basically implies is…that since the injectibles have the same efficacy…n require much more challenges in terms of logistics and storage…it all comes down to cost….and cost wise…injectibles may not be able to beat the present therapy available…

The cost being…5 dollars a month…

Very valid questions @sahil_vi May be worth sending email to Secretarial@Lauruslabs.com. It is listed in investor section of the company. You will also know how responsive company is to individual shareholders.

Sahil….these are very interesting questions to get clarified.

Kindly also ask them, if possible,

Whether Laurus lab submitted any interest of application with MPP for Pfizer pill Paxlovid production and are they expecting the sub license for the same?

Thank you.