TOUGH TIME CONTINUES

Yes its bad!

Management has mislead investors over the last 1.5 years with their bullish commentary and not agreeing an year back that the sales bump up was due to stocking up of ARV (the whole thing is reversing now).

Post 2QFY22 the company had said 3QFY22 will be similar to 2QFY22. Clearly once again they have mislead investors.

7 Likes

Pros

- CDMO (Synthesis) is ramping up well

- qoq margins have been relatively fine especially since Q3 also saw RM inflation

- Mgt commentary around revenue coming back from Q4-FY22

- Significant capex coming onstream in FY23 ( some already done but will need time to stabilise)

Cons

- dont think $1bio/FY23 revenue is a possibility now ! Need 1800 CRS quarterly revenue which is almost 70% increase from current levels

- ARV api segment continues to decline and in this quarter FDF was weak .

To sum up , an iffy result with some good parts and the not so good being the sharp decline in revenue and leaves more questions to be answered by the management . T

Plugging in one of my earlier comments. So the jump was due to stocking? I have missed a lot of things in this thread now.

Disclosure:

I exited 80% of my position around 550-650 due to technical charts not looking good.

Again getting back to FY20 territory.

Capex done, gross block built up, Operating deleverage hitting the Ebitda margins, temporary problems causing further degrowth (FY19 Rm pricing issues), Valuation again becoming favourable.

Perception swings around business performance are much wilder when Business is lumpy.

Short & fast strides in 1-2 years, temporary halt for 4-6 Quarters before the next sprint starts. An investor has to decide whether they are willing to stick with the journey throughout or play around the sprints. Nothing wrong in both the viewpoints.

Cdmo growth is stellar though, Arv as expected is going through headwinds

53 Likes

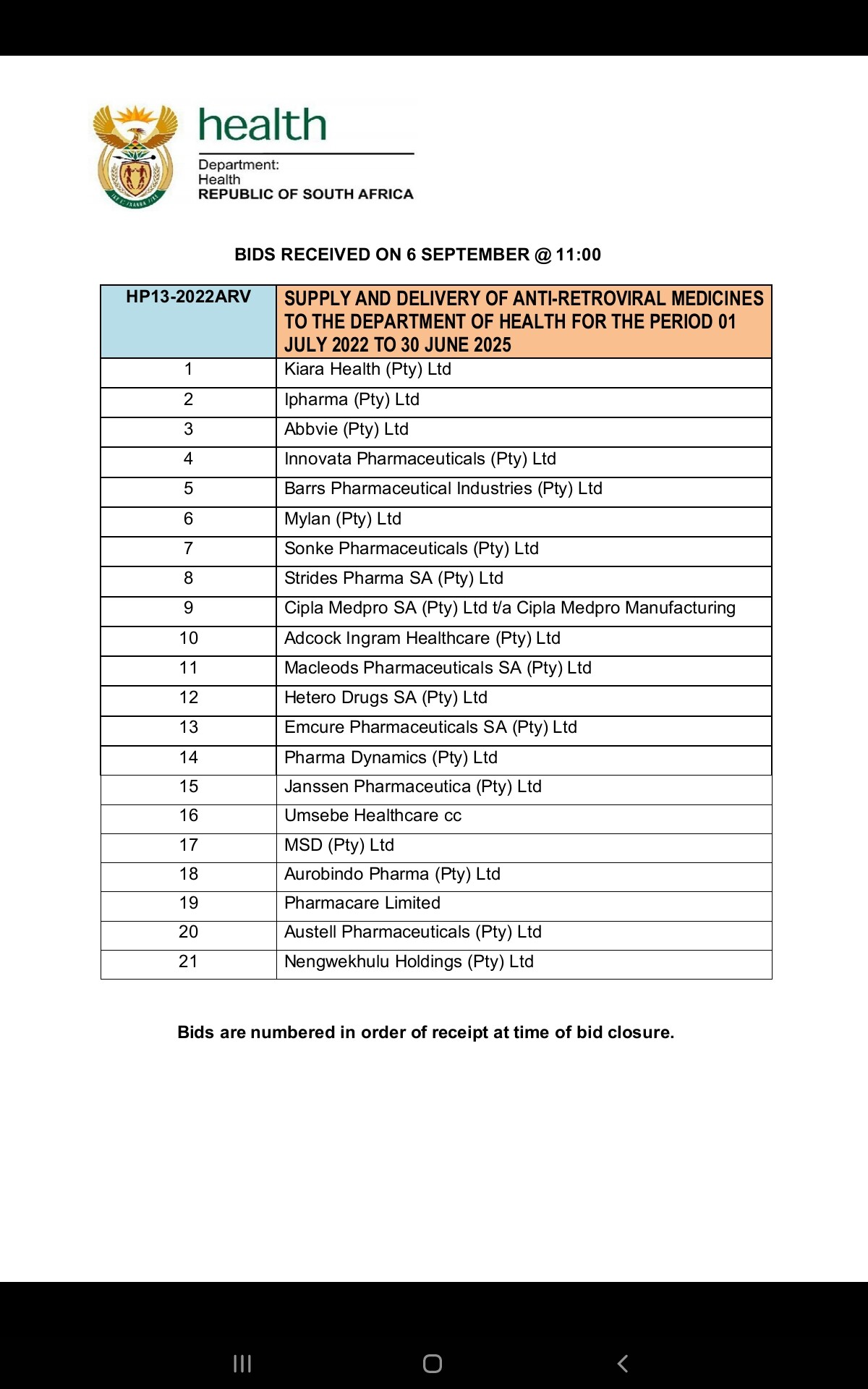

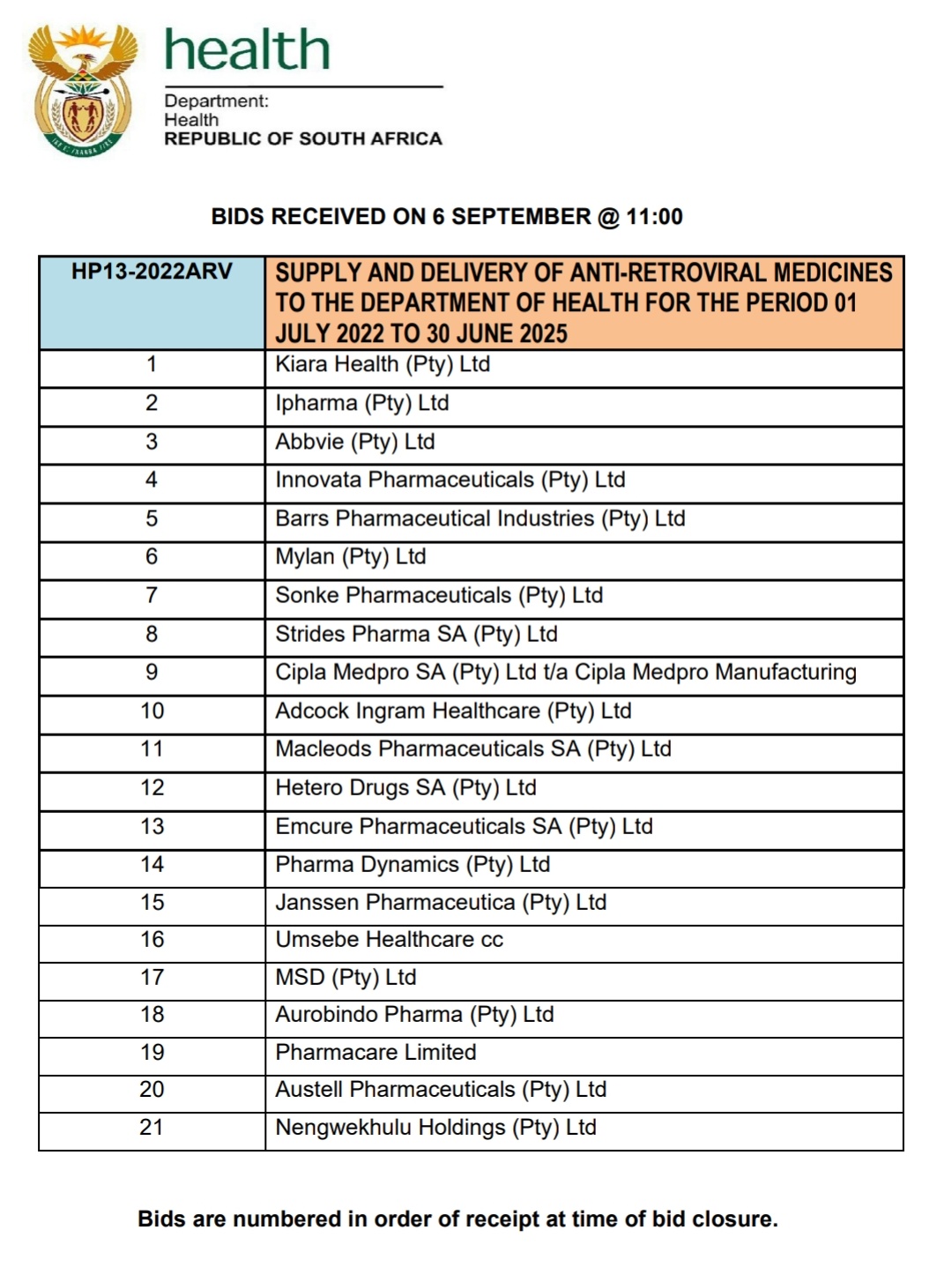

One pointer to validate mgmt stand on future ARV supply

South Africa is relatively larger market, tender was out last year Sept for next 4 year ARV supply ( check for HP13-2022ARVl )

https://www.health.gov.za/tenders/

Here is the list per final bids received- Laurus isn’t there.

Doesn’t make any sense unless they are working with another bidder

5 Likes

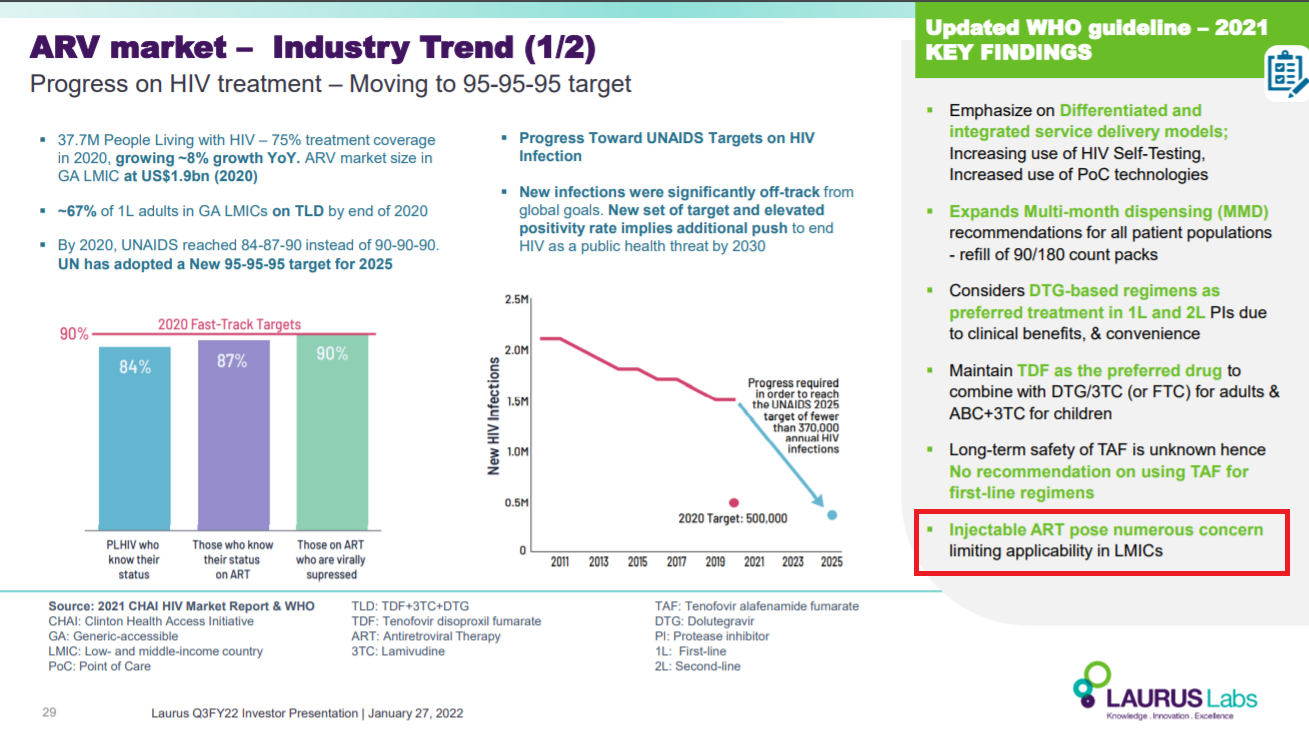

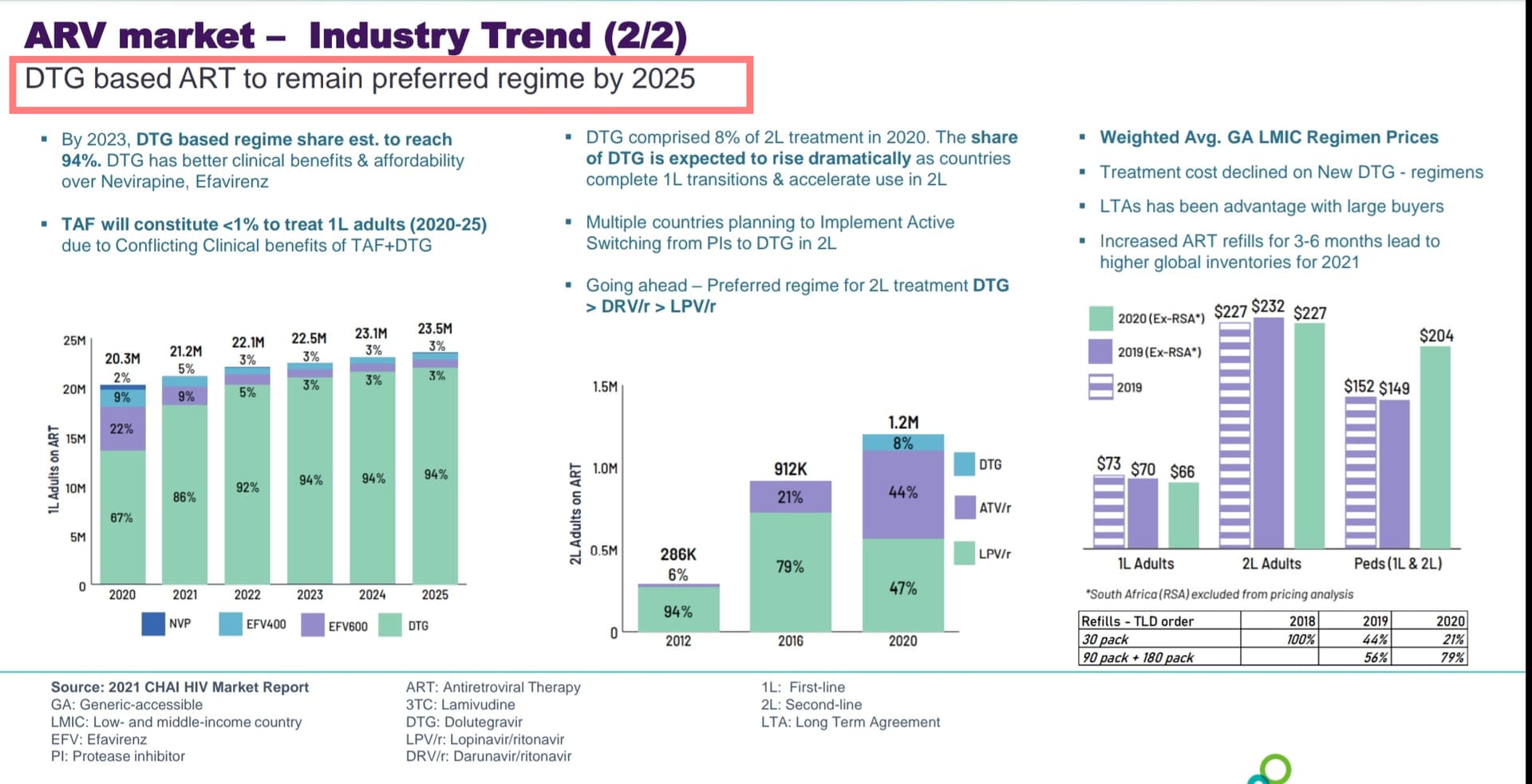

Good explanation on ARV regime - slide 29,30

SCO_IS_KM_322012710280 (bseindia.com)

As they say one should look for downside and thesis should take care of growth. If ARV revenues stabilizes, then Laurus have enough levers for future growth from mainly from FDF, non-ARV APIs and Synthesis.

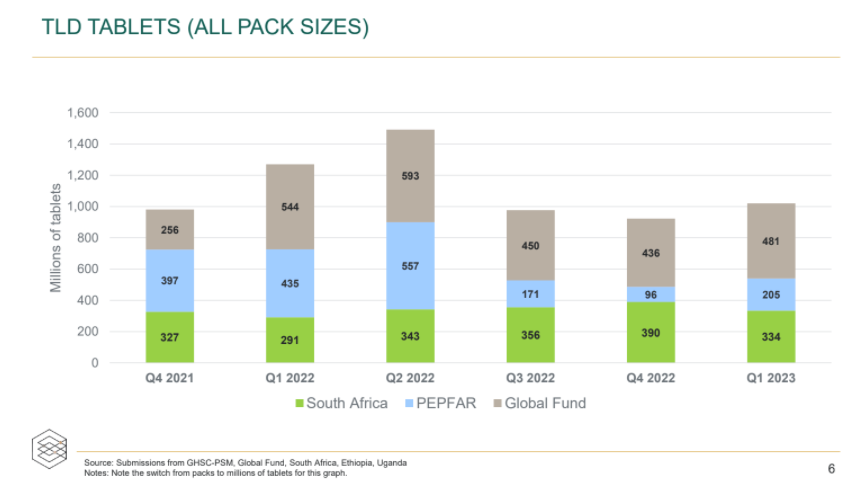

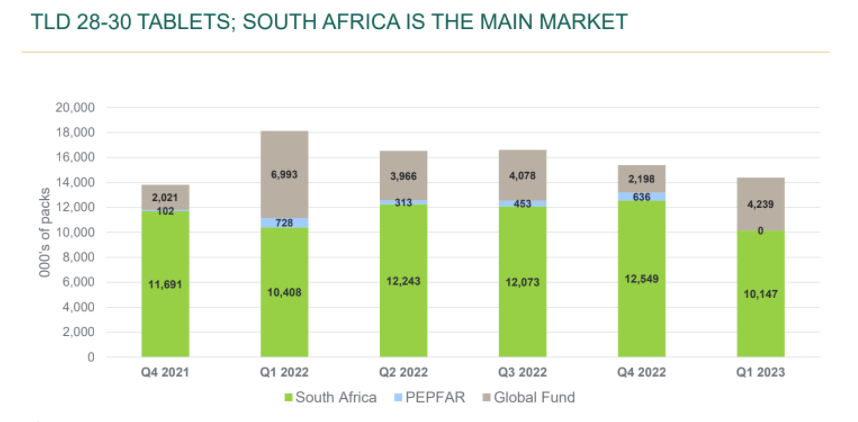

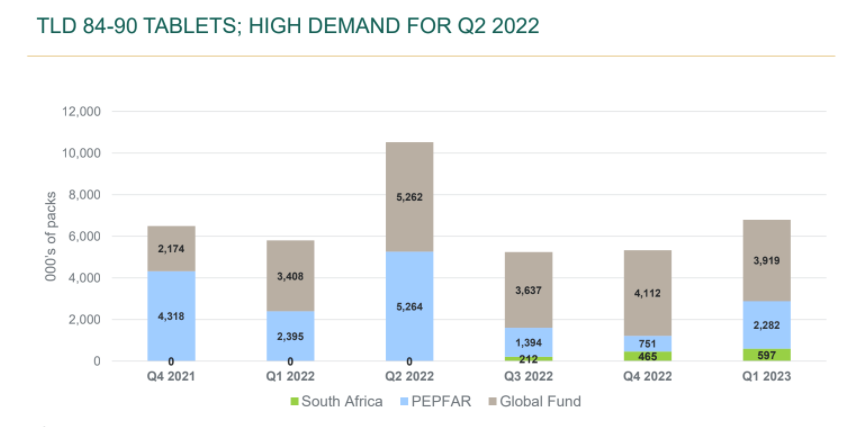

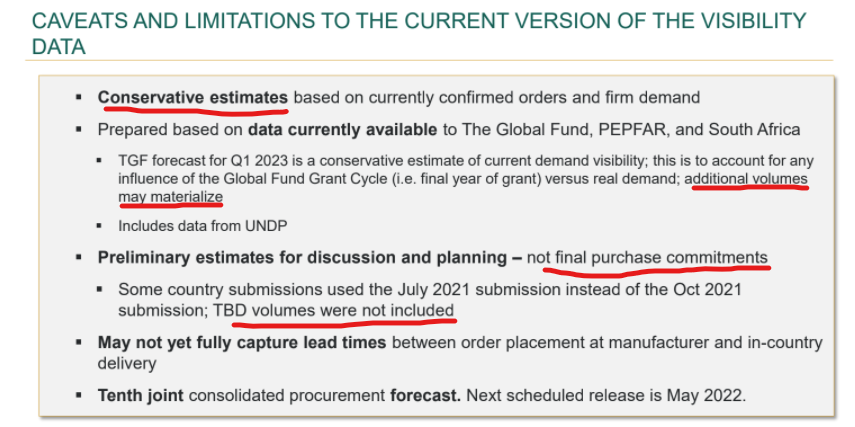

Following on from @Dev_S’s brilliant find, I noticed that the presentation is from an annual ARV buyers/sellers summit. I found an updated deck for the summit held in October 2021, with forecasts for 2022 and 2023:

As before, quarters are measured in calendar terms.

From this, it looks like Q4FY22 and Q1FY23 should see growth, but these are exceptional quarters, and demand becomes muted from Q2FY23 onwards.

The breakdown shows us that South Africa is more important to the TLD market than the Global Fund:

Q1FY23 will have an exceptionally high order of the 90 day regimen:

Note:

This should be treated as the base case, with estimates having a possible upside revision.

Finally, there’s no hiding from the reality that @Dr.Midhun has highlighted:

I can’t attach the full deck due to size limitations, but it’s available at this link:

https://drive.google.com/drive/folders/1SGUvOhKlPNfKGa2lEhSdQf06LRH6mU6E

Inviting comments ![]()

Disclosure: invested

18 Likes

Results aren’t stellar because business is going through its transitionary phase. Gross margin and EBITDA margin were maintained. As per its plans, Q1 and Q2FY23 are much more decisive quarters to look at

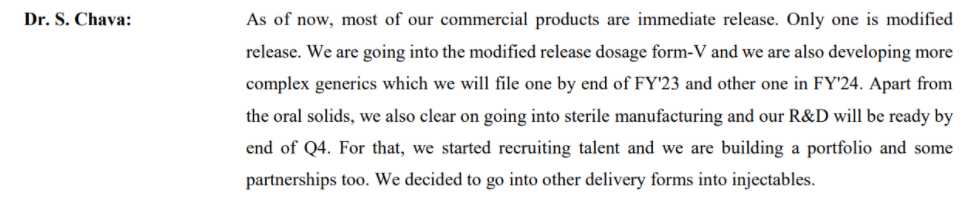

API’s degrowth. while expected, was a bit of a shock. FDF, still not yet worried since I am hoping to get more information on the MPP/Molnupiravir deal. Add to that, capacity expansion of 10bn tablets is around the corner. CDMO results were great. It seems that this part of the business will need to be analyzed on YoY basis rather than QoQ. LSPL’s Unit 2,3,4 have yet to commercialized. Bio is still in nascent stage and results show likewise. Q4 will be very interesting for Bio since they v recently fully commissioned their 180kL facility.

Will money be transferred from impatient to patient hands in near future? Let’s see.

Disc: Invested

5 Likes

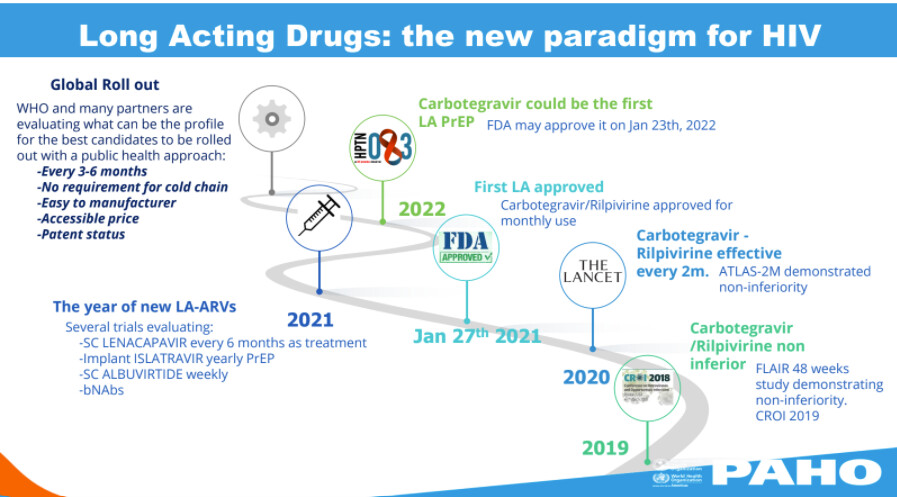

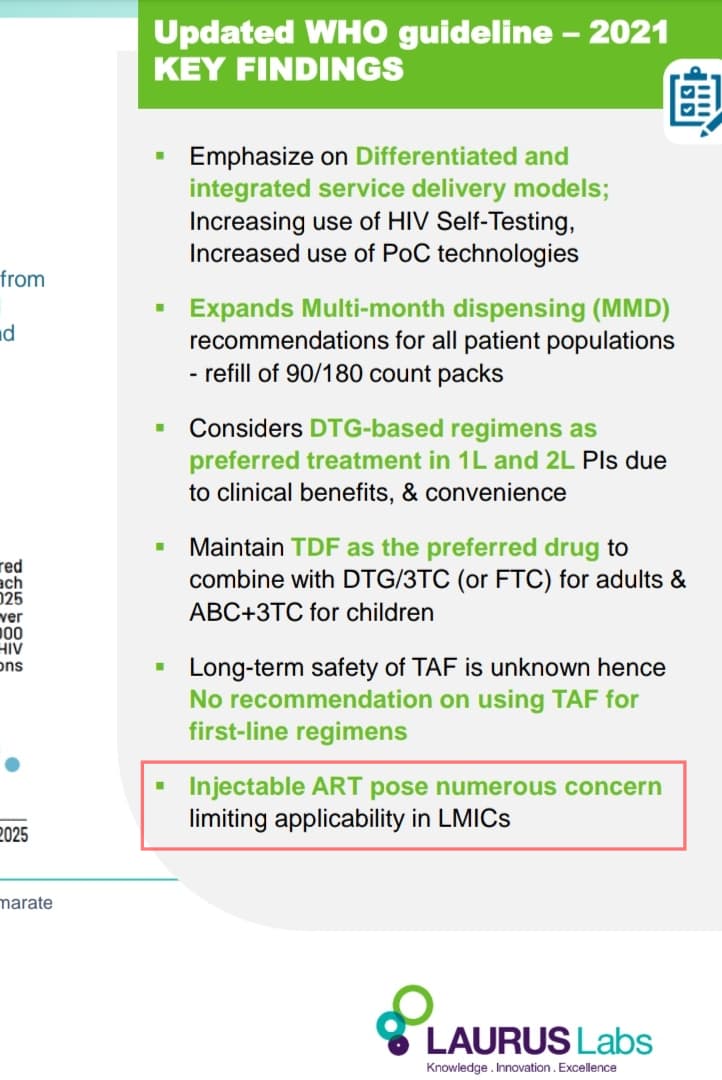

Is management ignoring the threat of long acting ARV injectables? Their comment in the presentation seems dismissive to me.

in their Q2 Concall, Dr. Chava mentioned that Laurus is looking into injectables. As per my understanding, there seems to be a case against injectables with regards to its economic viability in LMIC countries. I might be wrong but will have to check management’s response about this in the upcoming Concall. Thanks for pointing this out!

Management guidance on the latest investor presentation says there will be no change in treatment regimen until 2025.

For the first time, investor presentation also points the threat of long acting injectables. But there is not much data on the presentation about it.

Thanks @Dev_S for your research.

South Africa tender also indicates there may not be any change in regimen until 2025.

But Laurus’s name is not there on that tender. That looks surprising to me.

3 Likes

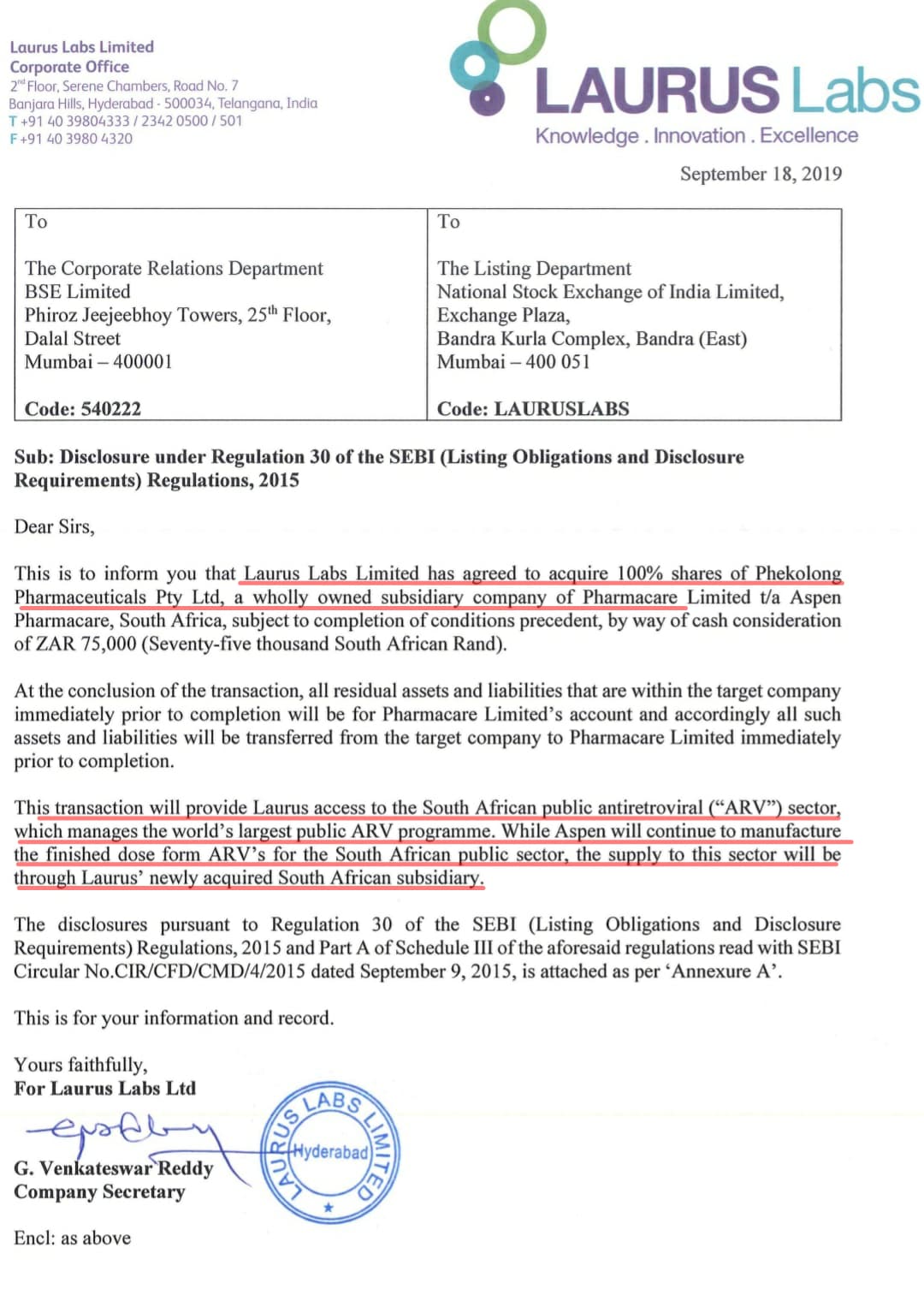

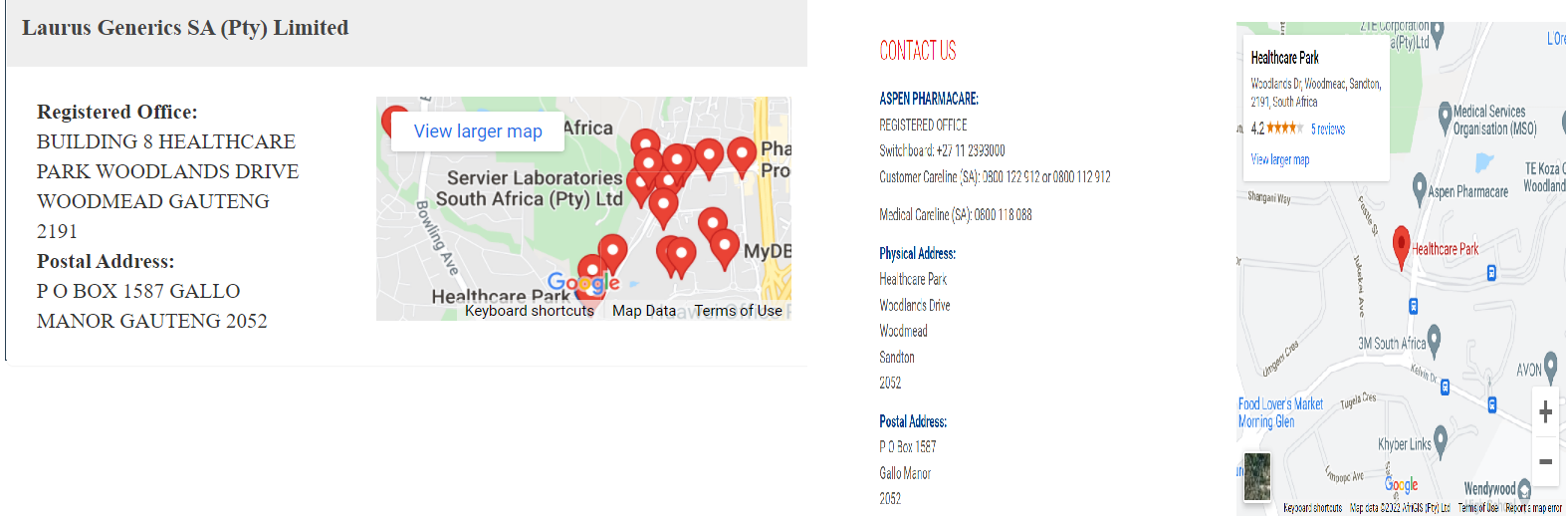

Is Pharmacare Limited, Laurus’s subsidiary in SA?

This announcement by Laurus in 2019 seems to be indicate that - https://www.lauruslabs.com/Investors/PDF/Disclosures/LaurusLabsDisclosureReg30AcquisitionofForeignentityinSouthAfrica.pdf

13 Likes

Thanks @nirvana_laha.

That explains it.

5 Likes

Does it make sense to invest in injectable if target to have less than .5 M new cases post 2025?

I guess subsidiary of Pharmacare was acquired by Laurus not Pharamacare itself. Laurus acquired Phekolong from Pharmacare and renamed it to Laurus Generics SA (Annual report FY21)

1 Like

@nirvana_laha

The reference here is Aspen Pharmacare, South Africa. In the earlier attachment they are referring to Pharmacare Limited which is an Australian company and I am afraid they both are different entities.

Most of the companies in this space have faced RM prices challenge…but in Laurus the topline growth has been affected…I think Q4 data and comparison and sectoral results will give an idea if it is going in the right direction or not…

Not sure, but appears that Laurus SA and Pharmacare (Aspen) have the exact same listed address in the Contact us sections of their websites. Even the PO box number is the same ![]()

Laurus Contact Us link - CONTACT US | Laurus Labs

Aspen Pharmacare SA Contact Us link - https://www.aspenpharmasa.co.za/contact-us/

Reasonably sure this is the bidding entity for Laurus. If its important enough, might make sense to ask it to Dr. Chava tomorrow.

5 Likes

Given the drag in ARV since mid last year, one would expect Laurus to use every opportunity, esp when they did an acquisition just to participate in this south africa tender( one of biggest market for ARVs supplies for 3 years ), snapshot from Q1 21 call

Unless there is a rational explanation from mgmt(e.g Partnerships with shortlisted players/ API supply conflict if any) , it’s clearly a missed opportunity that will only add to uncertainty of future. Evokes the thought if management walking the talk?

Edit - @nirvana_laha post indicates interesting find

There is another contact info for Aspen pharma address

https://www.aspenpharma.com/contact-details/

Better to try and clarify in call given a large tender for next 3 years.

1 Like