@LaurusLabs suggests its target prices for GFs: $100-500/g, proteins: $1-10/g range. These are below or within the range modeled by CE Delft.

Are we there yet? No, but the point is that precedence for low-cost proteins for non-pharma uses exists.

https://youtu.be/IH1a1wOdCfk?t=614 https://twitter.com/elliotswartz/status/1465807380185325582/photo/1

Building Biotech: India as a scale-up hub for cultivated meat and fermentation

Although video is from last year Oct, has some interesting information from panel members who are from different biotech companies. One of the panel members is Rajesh Krishnamurthy, CBO of RichCore.

From Bench to Billions: Nurturing biotech to mega scale

This video was posted just today (2nd Dec 2021). Among the panelists is Rajesh Krishnamurthy, Director & Chief Scientific Officer of Laurus Bio. I hope to share my notes from of Rajesh’s talking points about Laurus Bio and the innovation they’re working towards. I have noted down what I though was important. Please go through the whole interview if you want more info. (Skip to 36:36 for Rajesh’s inputs)

Laurus Bio, a synthetic bio company, initially targeted its products towards the pharma market where there was a need to replace animal derived products such vaccines, insulin, cancer drugs, etc. Laurus Bio has 12-15 products for that space. Their experience in this space over the past 15 years has translated into having precision fermentation expertise. Fermentation itself is a very old technology but precision fermentation brings in a higher level of detail, where one engineers these bacteria and control the environment to produce the product of interest. Laurus Bio is now at a stage where it can offer these precision fermentation expertise as a service as well (CDMO).

Laurus Bio’s products for the pharma industry can also be used in the cultured meat industry. But for these products to be commercially viable for cultured meat, the price needs to drop by 1000x or more. This is because cultured meat industry is basically competing with the cows and chickens of the world. So cost of per unit cultured meat needs to eventually be lower than organic meat for viability. The customers for the cultured meat are likely to be the vegan market and/or countries with food deficiencies.

Which areas of research & innovation is India best suited for? There are 2-3 things India can do. Firstly, majority of the cost of manufacturing goes into the downstream process. The downstream process is where the protein are separated from it (he didn’t specify what exactly; I’m assuming some intermediaries/solvents) and then purified. Laurus Bio still uses equipment that is fine-tuned for pharma and is working on using food-grade equipment to bring down costs. Also process efficiencies are being looked into, such as using solvent extraction instead of chromatography. Scale is another factor. The next big hurdle will be RM costs. Currently the carbon (RM), is 30% of opex. Once those downstream efficiencies are worked on, the RM will suddenly become 60-70%. Therefore, finding cheaper sources of carbon will be crucial. Ideally we would like to bring down the cost of the carbon source to zero or even negative. For e.g., somebody will pay you to take the waste from the food-processing industry and use that as the carbon source for your manufacturing.

Disc: Invested; Small percentage of pf.

P.S.: Please correct me if I have gone wrong somewhere.

A good article which hints how HIV medicine intake dropped in South africe & how it cud hv possibly led to emergence of new mutations & variants like Omicron.

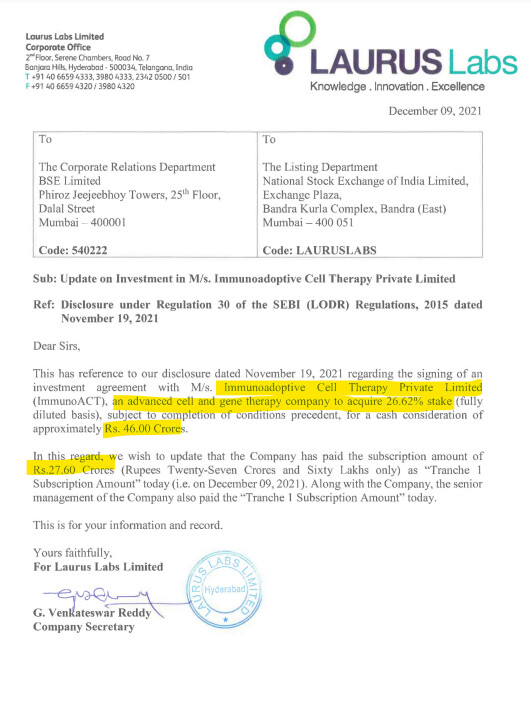

Laurus Synthesis awarding a significant turnkey contract.

Hi all!

This is my first post on this thread (In fact, first in Valuepickr). I have spent the last 3 days in reading through many of the posts in this thread. Its been amazing to get so much high quality knowledge on Laurus, Pharma industry and valuations in one single thread!

I am new to the Pharma industry and have been studying the opportunities in Pharma in India for the last 1 month. My broad takeaways have been to look for companies are into CDMO/CRAMS, value-added/specialty generics and biologics and those companies which are making sustained investments in R&D and capex.

Laurus Labs ticks all these boxes in my opinion. I am on the verge of taking a large position in Laurus Labs in my portfolio at this moment, but I have a few doubts in my mind. I am putting them across below, if some of you kind folks can address them, it would be great to learn more and build deeper conviction!

Valuation of Laurus Labs - Its trading at 25x TTM PE and about 5x PS. This is low when I compare it to valuations of companies with similar profile in India. What could be the reason for this?

-

Is it because of relatively high D/E ratio? In my opinion, Laurus has 16X interest coverage ratio and management commentary suggests debt will start reducing from FY23 after present capex cycle is over, so I don’t think this is a major cause for concern. Am I right in this?

-

Is it because promoter holdings have reduced by 5-6% in the last 2 years and in general is low compared to industry standards at only 27%? This was/is a cause for concern for me. But I read in this thread that most of this reduction was due to sale by Dr. Chava to release pledged shares and the rest due to reclassification of an erstwhile promoter as Public. Do these 2 reasons adequately mitigate the concern regarding decline in Promoter shareholding? Or are there genuine concerns among long term investors about the promoter shareholding %? Would love to understand this

-

Is it because market sees 30% EBITDA levels as unsustainable given that this is only a 6 qtr phenomenon and before that EBITDA %s were significantly less around the 17-20% mark? One explanation for increase could be higher % of non API business Q-o-Q which are higher gross margin businesses than API. Unfortunately I could not find even indicative gross margins for various BUs of Laurus - API, FDF, CDMO and Biologics - anywhere. Therefore want to understand from experienced folks on this thread, is the 30% EBITDA margin sustainable in a 3-5 year horizon?

Finally, would be great to hear thoughts/understand what steady state PS or PE multiple can a long term investor (3-5 year horizon) ascribe to Laurus 3-5 years out from now considering by then it would have stabilized its heavy investments in FDF, CDMO and Biologics? What are some companies whose valuations people study to understand industry valuations for FDF, CDMO, Biologics businesses?

I am quite bullish on Laurus Labs and I keenly look forward to learning more about the company and the industry from you good folks in the days ahead! Cheers

Welocme to ValuePicker and congraulations on your first post.

The main reason for LL underperformance are:

They have major revenue coming from ARV business and as per analyst the demand might not be sustinable .Mgmt is aware abt it and hence they are moving to other business divisions

Raw material price impact in last qtr

Rest of the points are all transactory and as per me this has notthing to do with its long term performance or underperformance

Disc - I sold out Laurus Labs completely few months ago

Laurus Labs has almost 70% of the revenue coming from ARV sales and 75% of this revenue is linked to tender. Before the current stupendous run, they had won tender from Global Fund and there was stable pricing regime.

Fast forward 3-4 years to today, Global Fund has given 1 year extension to last tender but that there is no clarity on when next tender will come through. For some of the other country specific tenders, some of the competitors have quoted lower prices. If you listen to Aurobindo conf call, their expectation is that these new lower prices would be the norm. I don’t know whether it will happen or not, but this is one of the possibilities. When 75% of your business has a possibility of margin compression and no clarity on next global fund tender allocations, it is prudent for investors to wait and watch and see how things unfold.

There are a lot of exciting things happening on non-ARV side - two of which deserve special mention. First one is launch of 2 molecules with EU partner sometimes in FY23. These are non-ARV molecules (*gliptin, *gliflozin) and my expectation is that these would have higher gross margin than ARV molecules. Another one is growth in CDMO, where management sounded quite bullish and this business can reach 4 digits.

So the question that really needs to be answered is - can business grow in terms of bottom-line at healthy pace while ARV business structurally moves to lower margin and capital efficiency. While management goes through this business reconfiguration, there would be some flat quarters, degrowth quarters etc. So as investors, one has to choose for himself at what point of business cycle and stock price cycle - it makes sense to act upon for oneself.

Psychologically - there are a large set of investors who have made a lot of money and a lot of expectation is built in. When business is going through adjustments, a lot of investors would be disappointed and would start selling. There would be a sense of betrayal from optimistic and visionary promoter in Dr. Chava as pendulum swings the other way.

The best thing to do is stay grounded, dig up data on recent tenders (Kenya, South Africa, Global Fund etc.), track all the competitors in ARV side (SMS Pharma, Mylan, Aurobindo, Hetero etc.) and evaluate if bottom/stability is reached into ARV side of things. Track scale up on non-ARV side of things and also CDMO and see if these businesses are ready to overshadow troubles in ARV business.

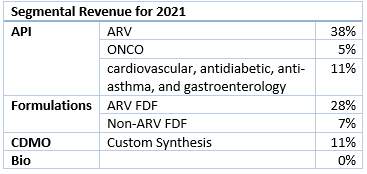

FDF formed 35% of the revenue for FY21 (28% ARV FDF and 7% Non ARV FDF)

ARV Sales was 66% of the total sales.

Thanks a lot for the detailed response. I now understand the valuation and margin risk much better. Will start tracking ARV developments also now (Was also tracking non ARV developments in Laurus).

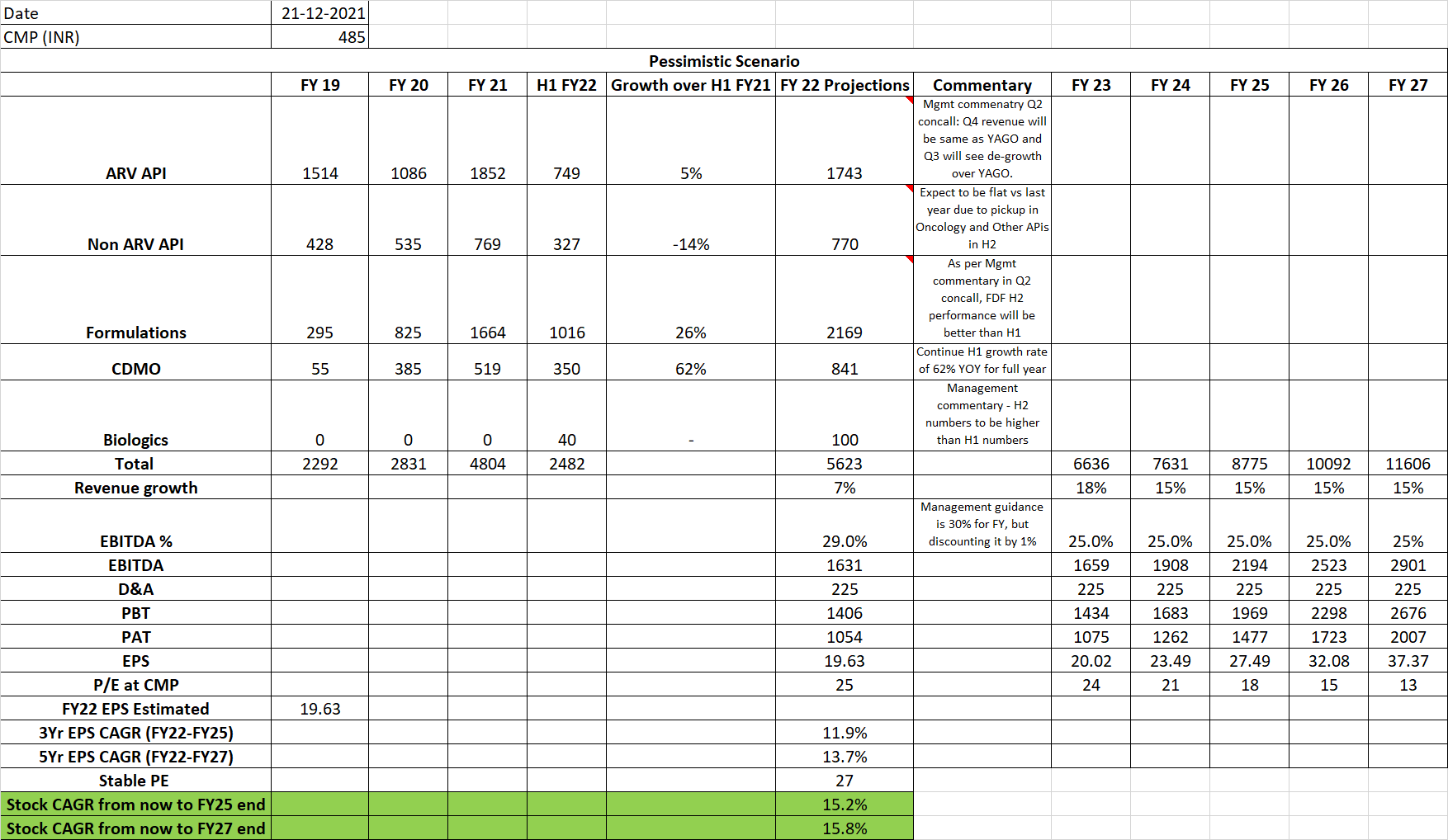

I tried to incorporate your feedback and that of others into a price forecasting Excel sheet which tries to model stock price 3 and 5 years out. Presenting that below. It appears to me that even if we factor in a reduced EBITDA of 25% and moderate YOY revenue growth of 15% from FY22-FY27, return investment in Laurus stocks are expected to cross 15% hurdle rate both for 3 and 5 year horizons. I have considered a PE of 27x while arriving at the prices in FY25 and FY27 to calculate the return on investment.

Would be great to have yours and others’ thoughts on this. Is this a good modeling of a likely bearish scenario in Laurus or could it be even worse?

this seems very useful….i think u should keep updating this routinely…

Downturn of API is global phenomenon, specially in case of ARV Bill gates foundation fund has been diverted to covid treatment, also management knows it pretty well only ARV won’t serve their purpose, what Mr Chava is trying to do is to create back integration in fermentation , where huge opportunity in Biologics is coming, they can’t match expertise like Biocon but what they can do is to create huge volume for fermentation with recombinant protein(Not from Animal cell) or enzymes which is a China+1, also enzymatic route create more yield in API with max purification than chemical route which is a Global trend , Laurus is more than a management play rather than qoq statistical play, any inputs on this view is most welcome

While I understand these are bearish projections, I am expecting much higher nos. even in a base case scenario.

The commercialisation of brown field capacity expansion for formulations will be done by Q4’ FY 22. This will add 4 bn units taking total capacity to 10 bn units… Hence, revenues just from formulations would be in the range of 4000 crore by FY’23. They are adding another 5 bn units by FY’24

They are also setting up one Greenfield R&D center in Hyderabad by FY’ 23 and two mfg units by FY’24 in the CDMO division to cater to the tie up with the global life sciences player that they announced in the previous quarter,

Not to forget, in Laurus Bio, two additional reactors of 90,000 litres each will be operational by this month end.

I think we will see Laurus in a completely new avatar by FY’ 24 with formulations, CDMO and Bio at the forefront.

Disclosure: Invested from lower levels.

My thoughts…as per Dr Chava. Laurus of 2021 is very different compared to Laurus of 2017 , and Laurus of 2024 will be way different compared to 2021… And we all can see the transformation viz … The sale of onco Api , other Api constantly increasing, cdmo- Synthesis growing year on year, signing multi year contract plus by FY23 to become self reliant subsidary plus the expansion here as all know…fdf capacity by 10 billion units by FY22.

As per him his aspirational Target revenue by fy 2023 is approx 7500 crores, depending upon approvals… Even if he achieves 90% we are talking of minimum 30% growth, and he said they take gross margins very seriously and as sales grow due to operational leverage they can cross 30 ebitda, minimum they want to keep is 30 % ebitda margins

What i want to highlight here is what jack Welch says Change before you have to… Just trying to understand Dr Chava sensed it early Arv sales will slow down diversified to other Apis , fdfs, crams, Bio and now immuno, and this is just the beginning they have a beginner’s mindset and want to invest in more disruptive technologies atleast in few of these they will overshoot.

Global funds for hiv /Aids are for 5 years, as said 1 year is left… Think it is a must must medicine, so I don’t think, funding can divert or stop, Laurus is one of the lowest cost producer of Arv due to its scale, it will continue in sales even if market shrinks atleast for coming 4 years till injectibles will be more mainstream affordable for hiv, till then Laurus will be in a very different trajectory in fact just yesterday read a article in India today … Saying omicron origin may be having an HIV connection… Can google it… It says… It is possible that omicron took birth in an hiv patient, who either left treatment midway or did not under go medication at all , hiv can make human body perfectly suitable for a Sarc cov2 mission can throw up omicron like new variants , so world will see it all the more necessary to check the advance of Hiv or Aids , to avoid future problems not solve them, thus demand for retrovirals.

FDA is expected to Authorize Pfizer and Mercks COVID pill this week itself, as MPP have a licencing deal with both companies that will allow generic versions to be produced for LMIC countries…Laurus has very good chance 1, due to its close relation with MPP and 2 due to its expertiese in antivirals to produce fdf or provide APIs for merks antiviral Molnupiravir or pfizers ritonavir ,

There is huge huge scope and win win here as COVID pill will be a game changer both for companies and patient’s suffering from COVID

Just last month HDFC and SBI bought into Laurus Labs, and as laurus has a very high fii holding & fiis are relentlessly selling Indian shares since last few months, could have been affecting the shares

Coming to Laurus Bio my favourite, as I see lots of scope in fermentation and bio, sales are roughly doubling Quarter on quarter, by this month end 180Kl capacity to be functional… What surprises me is in Q2 Dr Chava says we are planning for 1 million liters and if you check interview of Director Rajesh of Laurus bio he says we are already in process of building 2 million liters

precision fermentation facility for novel protein for food not therapetics one of the largest in the WORLD and the rational behind it… They want to reduce the cost 100 times as most start ups for cultivated meat industry are their customers, and lab based meat can only go mainstream if the cost is reduced of growth factors and recombinant proteins… Rest if you check Richcore capabilities and Subus reputation they will surely achieve, infact overshoot and much other feats before deadline thus huge scope here.

precision fermentation facility for novel protein for food not therapetics one of the largest in the WORLD and the rational behind it… They want to reduce the cost 100 times as most start ups for cultivated meat industry are their customers, and lab based meat can only go mainstream if the cost is reduced of growth factors and recombinant proteins… Rest if you check Richcore capabilities and Subus reputation they will surely achieve, infact overshoot and much other feats before deadline thus huge scope here.

This is Dr Chava for you…like him or not… Think he is the Dhirubhai Ambani of pharma always thinking big, fast , very bold, focusing on research, very adaptive, but not taking risks where quality and regulatory things are concerned, think there is a trend here similar to Dhirubhai … Take a field produce in scale with quality and reduce the price… .say Api, fdfs , crams, food protiens, now carT therapy with immunoact for affordable cancer treatment… And it will continue .

Benefits both producer and consumer … Reminds me of what max healthcare cmd Abhay soi said … In his latest interview to udayan we Indians are the pharma for the World, with aging population and rising costs around the world, indian healthcare sector will do what IT sector did in the past

Think the worst for Laurus is behind us…fy23 onwards will be very good for it, think this is a decadal story need to moniter every quarter… And change only if fundamentals change if we focus on trees we will surely Miss the woods…see Laurus in totality

Imagine if Today Laurus would come for ipo, seeing the frenzy think only Laurus bio would get this valuation forget other areas of api,crams,fdfs,etc… As they say familiarity breeds contempt…sadly

also Laurus labs is in top 5 finalist out of so many companies for corporate governance award by moneylife foundation…remember the old hero honda add …fill it …shut it… Forget it😊

Relatively new to this company so can be wrong please advise where I am wrong , biggest holding not sold a single share no reco DYOR take care stay safe.

Difference between autologous and allogeneic stem cell therapies in terms of how they are manufactured clinically

All stem cell therapies should be manufactured under Good Manufacturing Practices (GMPs). The primary difference between allogeneic and autologous are the source of the cells for the therapy. Allogeneic therapies are manufactured in large batches from unrelated donor tissues (such as bone marrow) whereas autologous therapies are manufactured as a single lot from the patient being treated. For some autologous therapies, the cells from the patient are processed on site at the clinic or hospital. These therapies are not regulated as a biologic product and not produced under GMP but rather the devices used are regulated.

While both therapies use similar technologies common to the growth of cells, the scale is different. Allogeneic therapies are “off the shelf”, used to treat many patients (sometimes thousands) and more time is available to quality control the product prior to administration. Autologous therapies are “custom” products for each patient and the chain of identity of the patient samples is critical to assure the right product is returned to the patient. Scale up of manufacturing for allogeneic cells is similar to techniques used to make protein drugs and other large scale cell derived materials while autologous cells require scale out, the production of many individual products at the same time.

Moneylife article on LL

Both Pfizer’s Paxlovid and Merck’s Molnupiravir have received emergency USFDA approval in the last 2-3 days. I am seeing reports that multiple Indian generics manufacturers will compete to produce this. Does anybody know how many licenses will be granted to Indian manufacturers, is there a cap? And if Laurus does get a chunk of the pie, can we expect revenues to start flowing from Jan itself?