Laurus Labs (NR) - Q4FY20 Concall Highlights

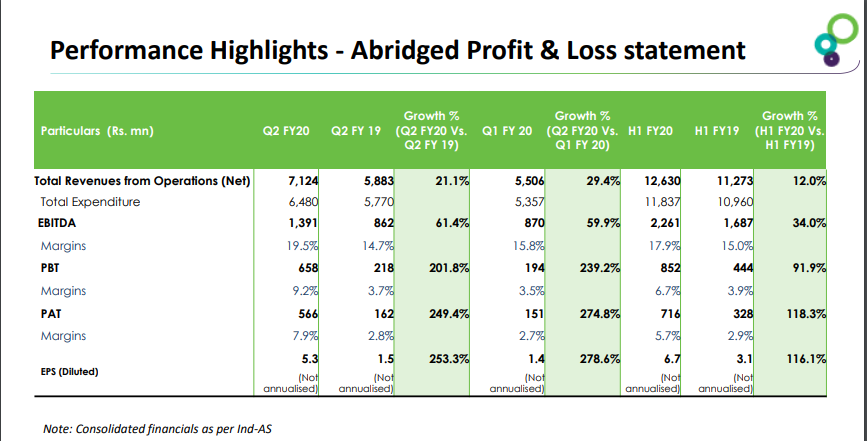

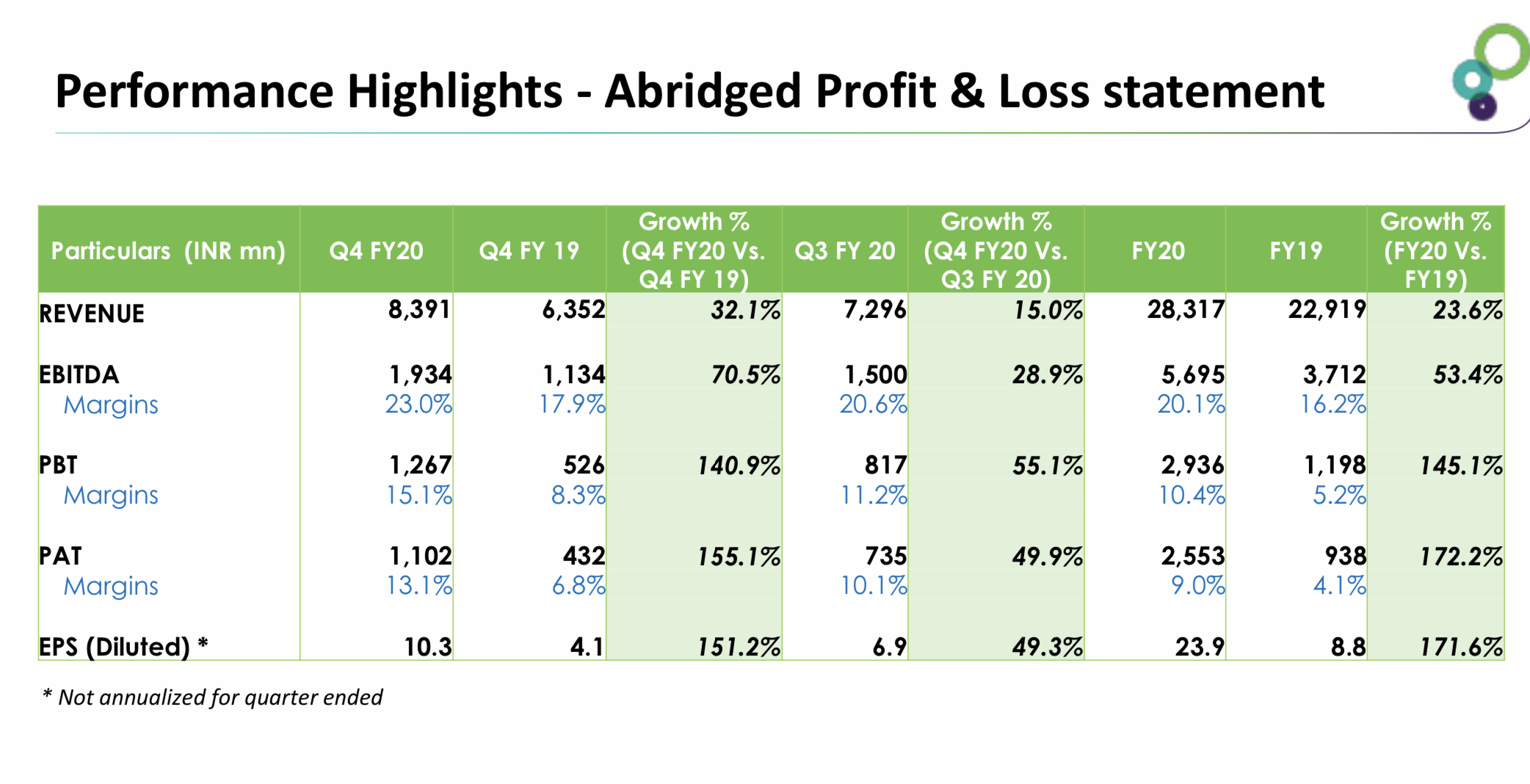

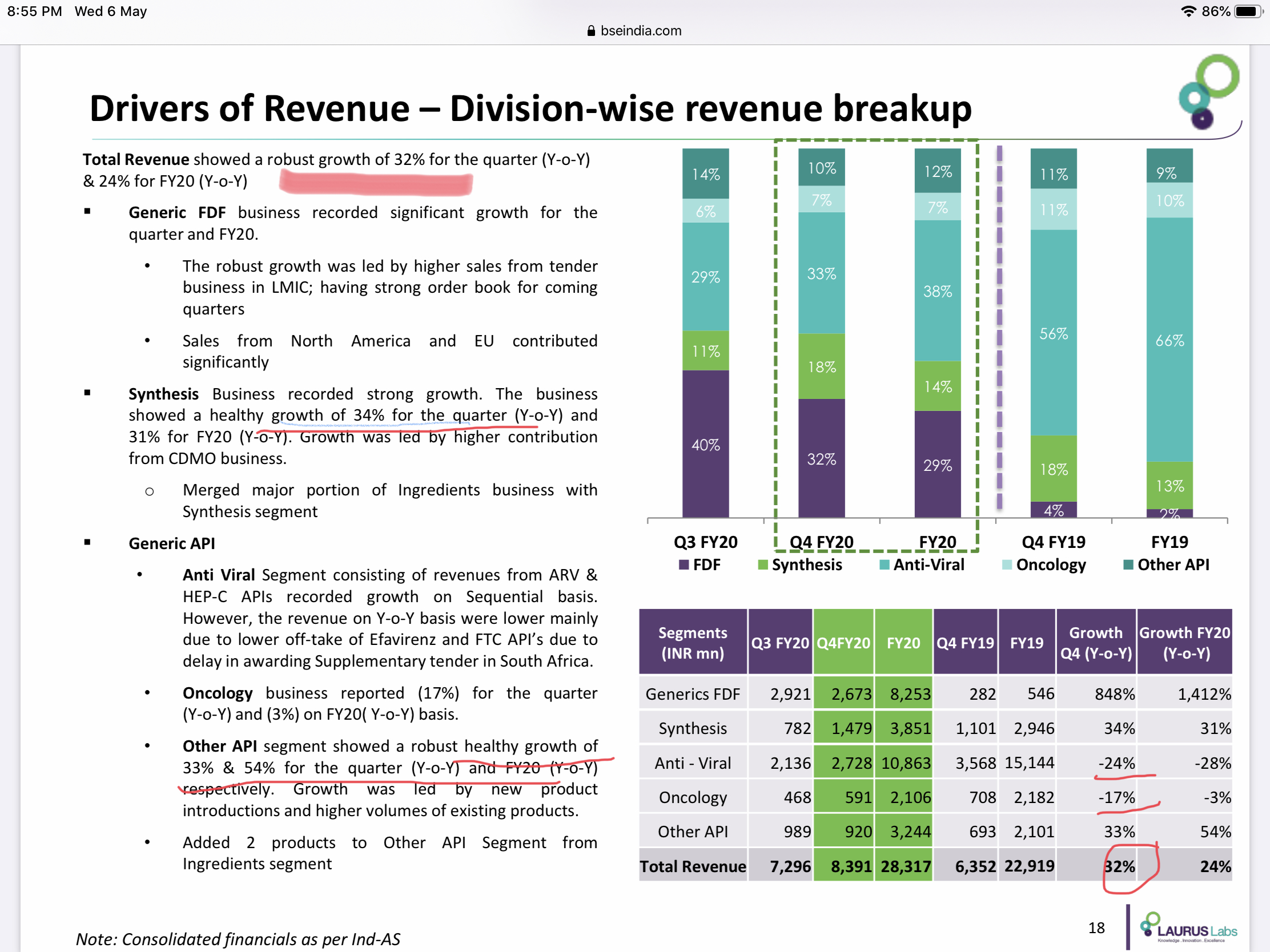

• Revenue for the quarter grew QoQ/ YoY by 15.01/32.11% to Rs 8.3bn & for the year grew by 23.55% to Rs. 28.32bn.Gross margins are consistent at around 50%.

• EBITDA Margins is around 23% for the quarter which had increased due to strong FDF business performance.

• PAT for the quarter grew QoQ/ YoY by 101.39/76.66% to Rs 1.65bn & for the year grew by 47.52% to Rs. 3.83bn.

• Final Dividend of Rs 1 Declared.

• Capex for the year was around 230 Cr. Capex for FY21 wil be more the Rs 3bn.

• Currently, 4mn ltr reactor vol which will be increased to 5mn ltr. Half of its completion will be done on Oct 20 and rest on Mar 21.

Formulation biz

• FDF growth was driven by TLD supplies.

• Healthy growth in North America. Contributed 9% to total FDF revenues.

• Expect approvals for TLE400 & TLE 600 in the coming quarters

• RD is 5.7% of revenue. Till date, Laurus has 26 ANDAs in the US (2 Para 4), 6 in Europe, 5 Canada, 8 who, 2 SA, 2 India & 11 in ROW.

• Have received 1 final & 2 tentative approval in q4 FY20 totalling to 6 final approval & 5 tentative approval from US FDA for the year

•Canada - 5 approvals of which 3 are launched 2 will be launched this year.

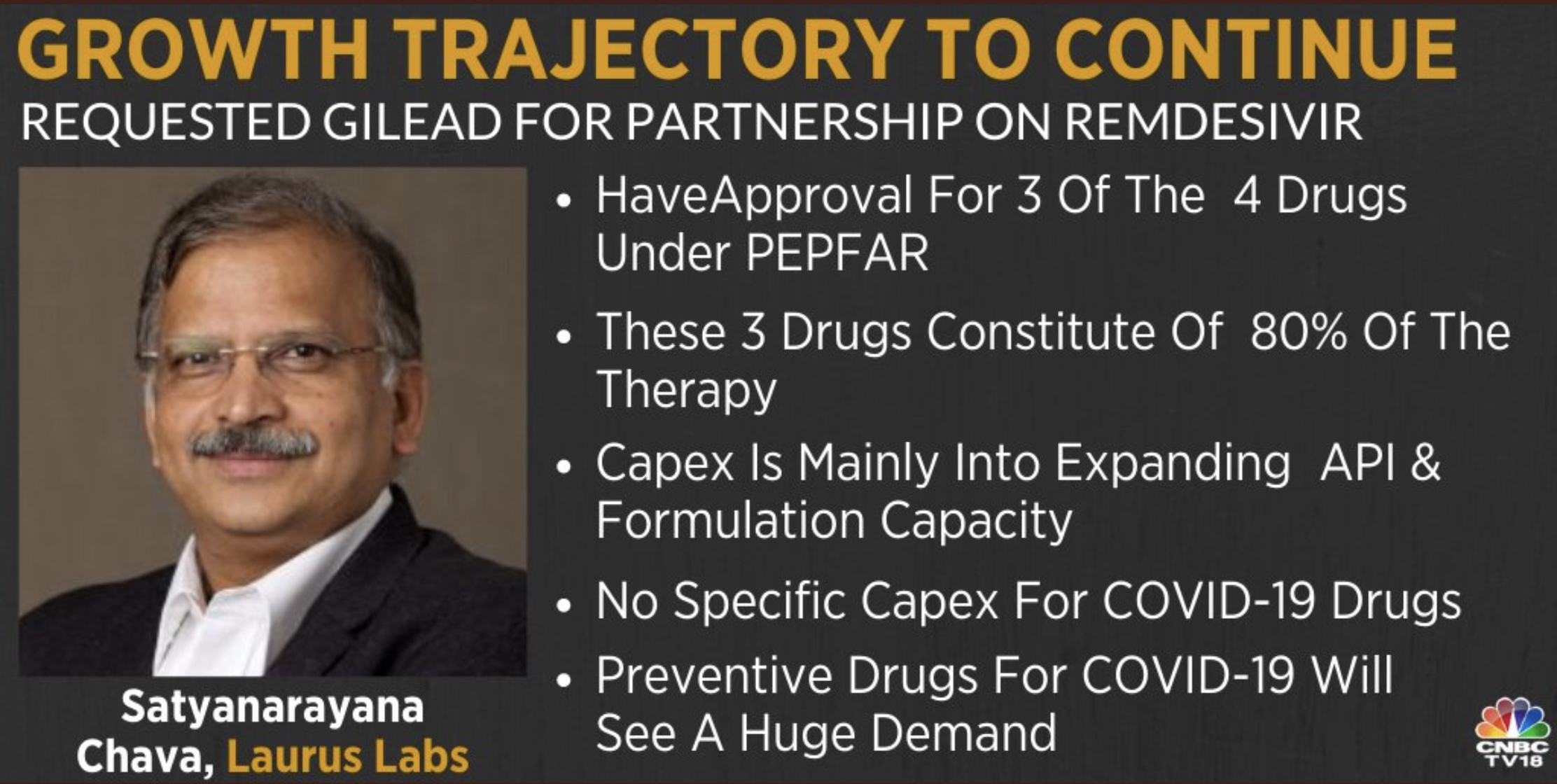

• Favipiravir – Currently completing the laboratory work and also working on the licence for the same. They will be selling the API and work with a partner for the formulations.

• If Gilead gives a voluntary licence, they will make Remdesivir.

• Most of the logistics problems were solved but Air freight rates have shot up significantly. The raw material from China now arrives in 5-6 weeks.

HCQ

• Launched HCQ in Q4FY20.

• Contribution from HCQ was insignificant in Q4. It will be supplied to the US, South Africa currently. Have increased capacity for API & Formulation to capitalise on any opportunity.

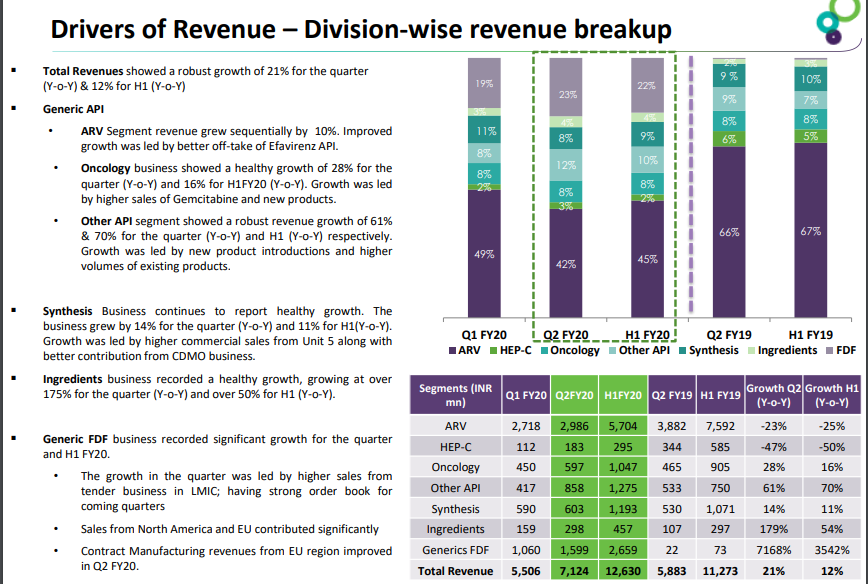

Segmental highlights

Formulation

• Revenue for the quarter is Rs 2.6bn (32% YoY) and for the year is Rs 8.2bn (30% YoY) which has underlined a significant shift in the business model.

• Had undertaken a debottlenecking project and increased the capacity in the existing building. This will be completed in the FY21.

• Also have undertaken brownfield projects in the current site which will be in operation in Mid of FY22.

• Have added capacity which will be in operation on Sep 20 and new large capacity will be operational by mid of Next year.

Have merged HEP – C and ARV API to Anti-Viral.

• Business has grown sequentially but has de grown for the year due to change in treatment regiment and the uncertain South African Market.

·• Have large Capacities for 1st line API. Will begin commercial supply of 2 such APIs after regulatory approvals forms their partner.

• 2nd line ARV APIs have seen good traction and expect healthly revenues from H2FY21 onwards.

Onco APIs did Rs 2.1bn in FY20.

• 1st half year, faced supply shortage for Intermediates thus they have done backward integration. Revenue should normalise from this year.

Other APIs

• Revenue came to Rs 3.2bn in FY20 with is a growth of 54% in FY20. Growth in the sector was driven by contract manufacturing in the existing products.

• Growth rate should be maintained in the coming quarters. Have a healthy order book for several generic APIs.

Synthesis business contributed Rs 3.8bn for FY20.

• Growth was led by heathly performance in the CDMA business. Also added new customers.

• Have incorporated a wholly owned subsidiary – Laurus Synthesis Pvt Ltd. This is done to increase its focus and a dedicated R&D & manufacturing site for the same.