Well said @Simrat . I started in Laurus at 2018 around 460 before the split . I remember the stock trading around 325 even though the management was executing well .Their messaging was clear even back in 2018 , that they wanted to move to CDMO , FDF etc. They transitioned really well to FDF . I think the next phase of transition is to Laurus Bio & Synthesis . The most important thing is they are not holding on to ARV , Dr Chava and team knows clearly there is not much left there . This is a consistent message in every conf call .I believe as long as they keep executing on the right direction , couple of quarter miss is not a big deal . If the share price decline further , this would be a good opportunity for long term investors .

24 Likes

18 Likes

Around 18:00, Did he mention that Laurus Bio margins will be similar to CDMO ? I think that margin is quite good

8 Likes

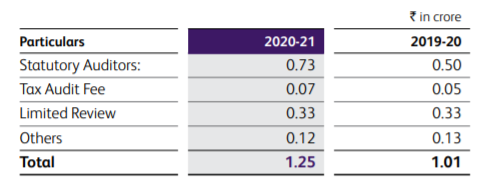

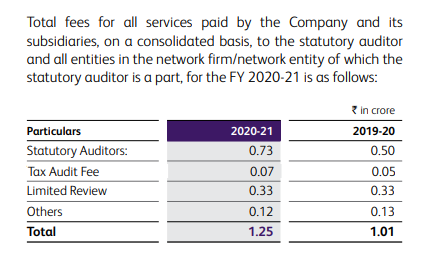

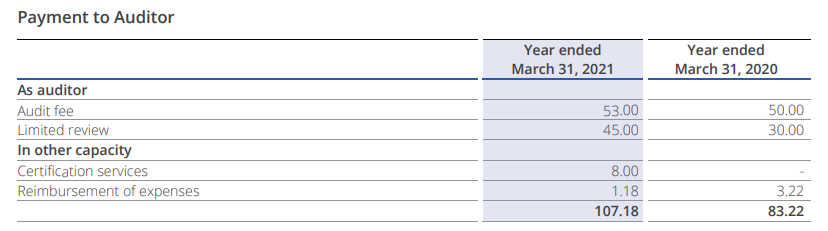

I am going through the annual report and have observed almost 50% in Auditor fees.

Any reason? Am I missing something? Please let me know.

Thanks

2 Likes

This is the break-up of total professional fees paid by the entity towards Statutory Audit and other services. Limited Review is the fee paid to the auditors for quarterly audit of FS. Statutory Audit fee is paid for the year-end Audit. Nothing suspicious about this.

There is a big jump in the auditor fees YOY. Is it ok? In general, a big jump in the auditor fee is considered a red flag. Can someone please help in understanding this?

1 Like

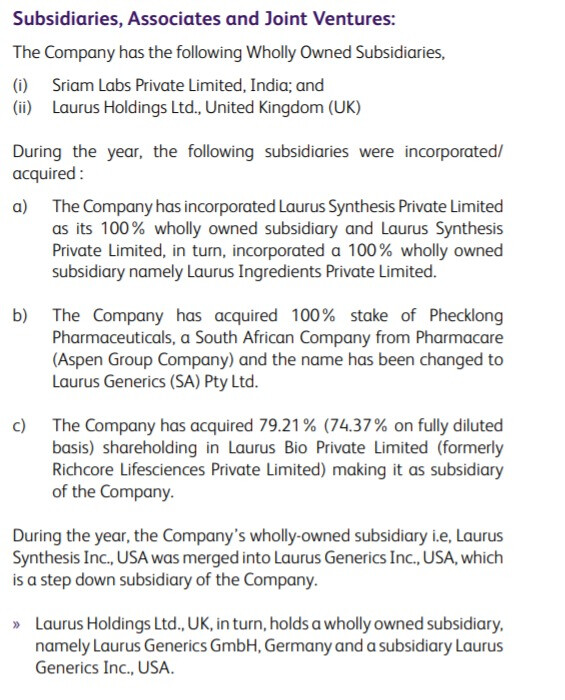

If we consider the jump in auditor fees, we have 3 additional subsidaries in the year. But when I checked with some high level finance persons, usually it would be 10-15% increase in case of subsidiary. But we see about ~50% increase. I am not sure if it is normal or are we missing anything here?

1 Like

Firstly It’s not a very huge amount to grow suspicious abt it.

Plus Audit fees are usually quantified as a percentage of revenue, & the company’s revenue has increased 60-70% in FY21.

So I think it’s totally justified.

2 Likes

Audit Fees can never paid as a percentage of increase in revenue or profits and that is against the Professional Ethics issued by ICAI to Chartered Accountants. Maybe the increase can be attributed to additional audit procedures performed for the newly incorporated subsidiaries along with Group Review.

I have noticed the same thing with another listed entity where they have conducted Audit for all the subsidiaries for FY-21 for the first time and there was a similar increase in the fees paid.

3 Likes

@sai_sirish I think you are misinterpreting my statement.

I never said it is “paid” as % of revenue (It may depend on multiple variables, I don’t know), I used the word “quantified”, which means "to express the quantity in terms of ".

Let me give you a example to make it more clear :-

So as an analyst I would quantify it i.e express it in terms of Revenue or maybe even Assets, to check how significant the number is.

I would become cautious if the audit fees becomes 0.5 -1% of the revenue, but really wouldn’t mind if it is like 0.02 % of the revenue which is here in the case of Laurus.

I hope this clears everything.

My comments/thoughts after listening to the management interview.

- Q3 will be same as Q2 and we can expect revenue in range of 1200+ cr. It will not be in range of 1400cr as Q4 2020.

- Q4 2021 could be same as Q4 2020. So we can expect 1400+ cr revenue in Q4 2021. Annual revenue for 2021 could be between 5000-5300cr.

- Now in order to reach FY 2023 guidance of 7400cr revenue, company has to grow 50% in FY23. Management mentioned that there is growth of 50-60% every few years and we can expect same growth in FY23 too.

- Overall with Formulation capacity increasing, Covid slowly going away and life coming to normalcy, ARV demand can come back in future(may be Q4 2021 or FY23). My personal thoughts are that people have high expectations from the company that it will grow every quarter. As long as long term growth story doesn’t change, it could be buying opportunity. Only challenge is that most of people like me already have enough allocation in the company(10% range) and I personally find it risky to allocate 20-30% in one stock.

29 Likes

a well-written message If there are any hints about the EPS growth forecast?

"Ecker predicted that biologics manufacturing volume will grow by circa eight per cent per annum, reaching approximately 3,900kL [up from 2,700kL in 2020]. However, during the same period, global biological manufacturing capacity will increase to 7,500kL [up from 5,200kL], but significantly, the location and type of companies that have capacity will show a marked change from five years prior.

In 2025, nearly half of all capacity (44 per cent) will shift from in-house manufacturing to CMO/hybrid companies."

The comments in here on recombinant proteins read in conjunction with Dr. Chava’s clarification on Pharma versus Food recombinant proteins gives a clarity on Dr. Chava’s vision, ambition and execution strategy in line. Laurus for sure is heading towards becoming a giant and from the look of it, at a furious pace.

11 Likes

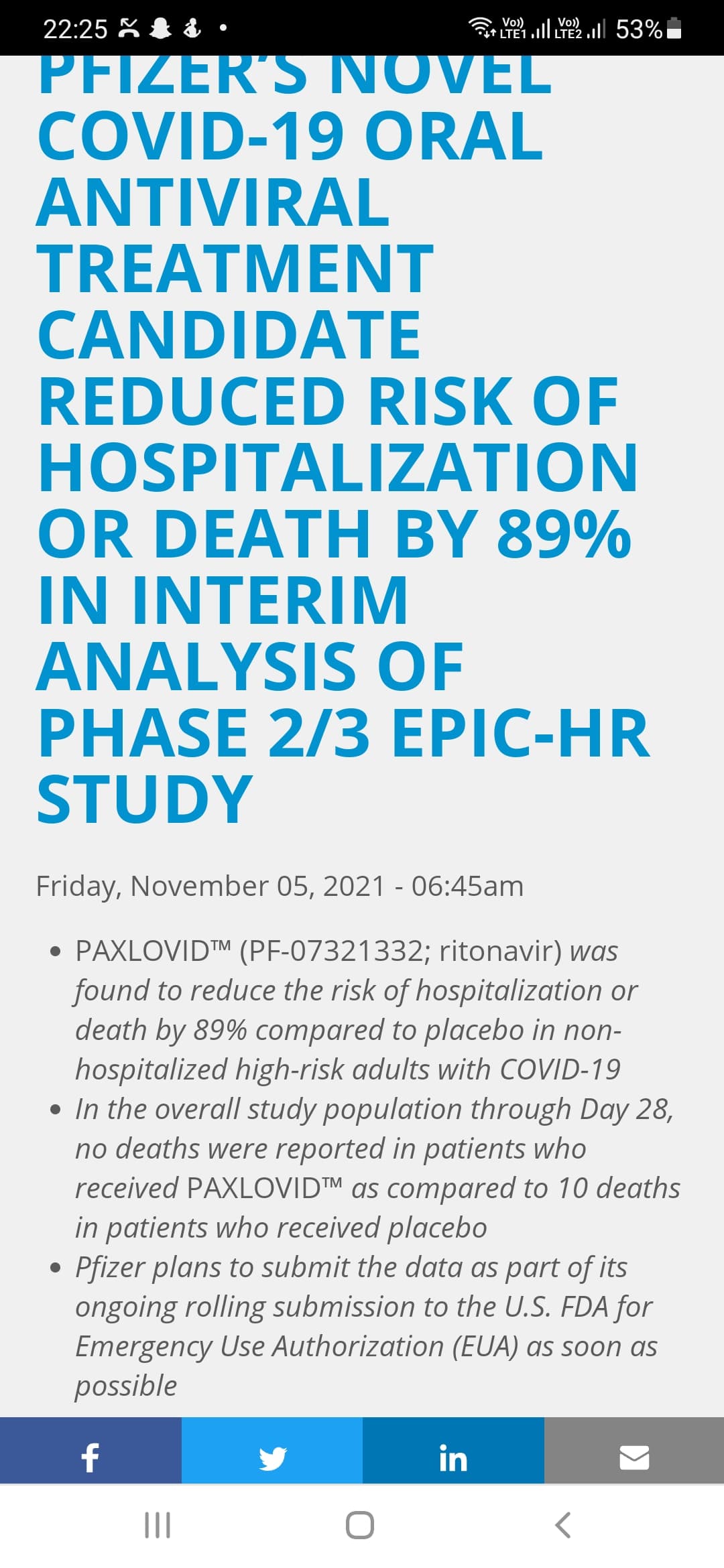

due to proven expertise of laurus labs in HIV Pills a very positive development for the co?

3 Likes

Ritonavir api demand will get a boost. Shot in the arm for laurus labs. ARV api sales should pick up.

https://www.pfizer.com/news/press-release/press-release-detail/pfizers-novel-covid-19-oral-antiviral-treatment-candidate

8 Likes

If pfizer covid pill gets approval from FDI then it will be a game changer for hiv drug producers, because their earlier addressable market was limited to hiv infected people now the market will be 100X. And more importantly if covid doesn’t vanish and becomes an endemic, then the pfizer pill would become standard treatment.

10 Likes

Please refrain from such aggressive remarks. Vikky9995 has just put a possibility and no where he has shown what he wants and doesnt want. This forum is for collective learning and respecting other’s views, let’s not make it a place to debate.

13 Likes

It really gives moral dilemma to own Pharma stock, when we take pleasure in our gain calculating that if the disease increases then it will lead to increase in sales of the medicine…

Its true that the medicines made by the company helps in curing the very disease but then the disease will have to spread which will lead to increase in sales of these medicines and thereby leading to your profit… I therefore personally do not like to calculate addressable market because at that calculation you would always like/wish to increase the addressable market… which means…

Just my personal thoughts and may not be relevant to this post and would also not mind deleting if any objection is raised.

Disclosure : I own this stock and have decent exposure across pharma company (Biocon, Shilpa,Neuland,divis, Stride, Sequent and others)

11 Likes

I just put out a possibility of covid becoming endemic and it’s implications on the revenues of hiv drug producers, in noway I’m wishing for covid to become endemic

8 Likes

Please refrain from attacking each other. This forum has taught us great things. If i don’t like any other views, I refrain from comments and let the things die out.

As for as laurus is concerned, I have brought small portion of laurus in my wife portfolio on muhurat trading day as an anniversary gift for her.

I am very optimistic about Laurus future and consider this as buying opportunity.

Will add more if it falls further.

Dis. Buying price is 498.

4 Likes