Few of the positive points market going to consider are

Total revenue is still better YoY, results are as expected and market already discounted the price in anticipation, that is possibly the reason for reversal and increase in buying volume from 522

Medicines Patent Pool (MPP) and Merck enter into License Agreement for Molnupiravir, an Investigational Oral Antiviral COVID-19 Medicine to increase broad access in Low and Middle-Income countries. Laurus and MPP have a very long and successful partnership in various HIV and Hep-C medicine licenses, and Laurus will approach MPP for Molnupiravir licenses.

Synthesis: Maintaining strong growth momentum (+34% YoY). Signed new CDMO multi-year partnership with leading Global Lifesciences company for niche APIs.

Formulation volume in 10 Bn by the year end, revenue from that is progressively increasing

Laurus bio entered in to alternative food protein business, planning for 1 million reactors volume, which is in thing and possibly next cash cow

It will be interesting to know how big is the growth opportunity from below. May be if some one is attending the concall, this question could be asked.

LSPL signed a multi-year development & manufacturing contract with a leading

Global Life science company

The deal entails complete CDMO for a portfolio of niche APIs

LSPL will use part of the existing capacity and also to set up a dedicated

manufacturing facility to manufacture and supply APIs

Part of the CAPEX to be funded through long term commercial advance by the

Customer apart from sponsoring development cost

Commercial supplies will commence from FY24 onwards

Marks a significant step forward in our evolution as a valuable partner to the global

pharmaceutical industry

Reading between the lines, the CDMO opportunity for Indian companies is very real and will be a great opportunity in upcoming years. Hikal also mentioned on it, also on enquiries from customers diversifying supply chain. Other than the ARV business which went down steep this quarter (I believe everyone was expecting it to under perform anyway), the future is still very bright. The Gross margin hit is only by 100bps, which implies the raw material impact is not terrible as market anticipation.

Just got off from Laurus earnings call. Key points

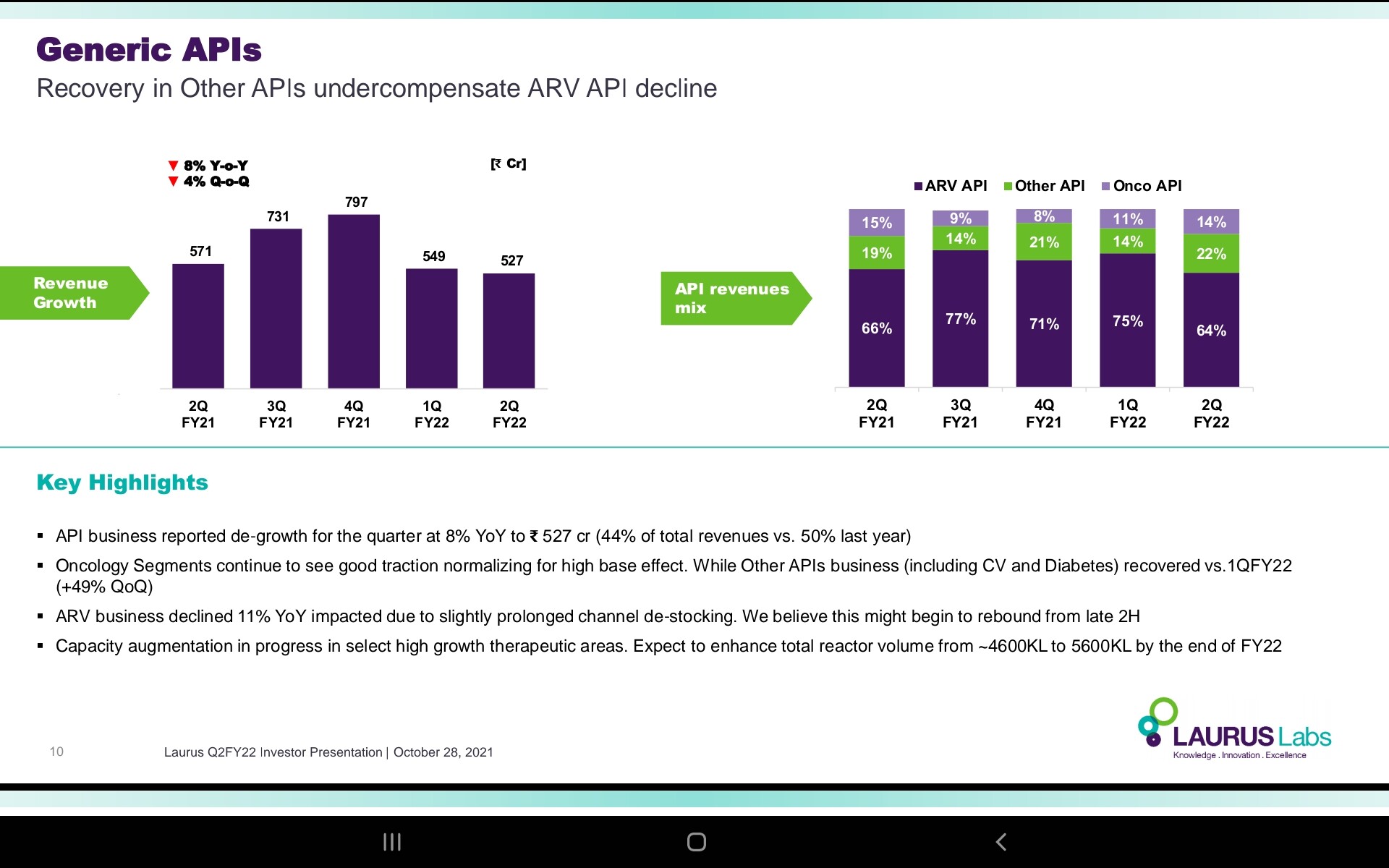

1- API for ARV: channel destocking is the reason behind degrowth. In Q4 this should turn around. No cost, demand or competitive pressure.

2- FDF capacity increased by 1 billion unit is live now. Another 4 Billion by end of Q4. FDF sales remain robust.

3- CDMO doing good and would do better. About 15% of sales. Significant increase from Q1 of FY 24.

4- Laurus Bio will do more topline in H2 than H1.

5- Confident hitting one Billion USD sales in FY 2023.

6- Ebitda to remain around 30%.

7- No price of raw material issue. Solvent prices are high but not to a point to cause damage to margin. Laurus does not import any intermediates from CN; it imports 50% of KSMs and there is no issue with them.

8- No pending FDA audits at this time.

My take - stock price can go anywhere but business seems to be doing fine, and possibly return to good growth in a quarter or two.

Dr Chava has confirmed this on today’s concall. Raw material dependency on China is around 50%. These include Key starting materials, not intermediate chemicals. (They are backward integrated for intermediate chemicals). Solvent prices constitute 5- 10% of raw materials. (May differ with different molecules).

Solvent prices have gone up. Some has increased 10%, while some other solvents have increased 50%, 200%.

They can’t pass down the cost as of now. On API segment, they will continue to offer existing prices (To honour existing contracts. For fresh orders, they will be able to pass down the cost with negotiations)

Passing down the raw material inflation will take 3-4 months.

Q2 concall - Two main issues that reflected in performance

Margin hit and RM issues

While explaining impact of RM prices in near future- following stands out

KSM is not an issue as not much volatility

Intermediate are all in house

Solvent prices are challenge - some have reduced, some have gone up in teens, some have even doubled - however Solvent makeup for 5-10% of RM cost only and they don’t see any major impacts on gross margins( reflects in similar GM nos YoY and QoQ

Then why detoriation in EBDITA/PAT level - answer lies in negative operating leverage as they are producing more and selling less - inventory has gone up sizable to impact GM to EBDITA flow.

Mitigation on RM - built inventory, new set of orders to have price increases

At FY 22 they are confident of 30% EBDITA ( Q1 was 31, Q2 is 29 - H2 need to do 30)

ARV API performance weak

being bulk of their API segment and sizable portion of overall sales, it has weighed on both topline and bottomline ( higher here as they produced but didn’t ship)

Expect Q4 22 to be similar as Q4 21 for ARV API - Q4 21 was highest base for segment- this one seems a tricky claim, IMO need to factor bit lower and key monitorable.

Threat of Injectable as replacement Q was not answered by mgmt.

FDF performance fair

Given majority share is contract manufacturing hence not affected by Generics pricing pressure

FY 22 end will have 4B doses capacities, All are backed by demands and nit contingent to any major dependency - EU client visits scheduled against incremental capacities in Q1 CY22

$1B aspirations by FY 24 hinges on hevaylifting by FDF at total 10B capacities- which in turn have dependency on pending ANDA approvals in next 6-9 months - key monitorable

CDMO

Bullish on segment, large contract win key highlights though this will contribute ftom FY25

** 15% revenue by 2023, increasing as new capacities come online

Capex and debt

** 1500 -1700 cr growth Capex, larger part to be over this year

Debt at 1800 cr , to inch up till year end - come down ftom FY 23 onwards

Merck-MPP opportunity - LMIC API and FDF opportunity for covid oral drug - meeting MPP in Dec, will get outcome by Jan - could be an optionality.

After hyper growth in FY 21, Two back to back Qtr underperformance ( relative as higher expectations were built) reasons to change narrative, which will keep pressure on prices, experienced folks have exited much earlier with tech charts signals + Q1 performance triggers. Sector headwinds visible for min 2 qtrs. Q1 23 onwards trajectory should gain momentum, till then doubt any significant action and it is likely to test conviction with opportunity cost.

I just went thru Navin Fluorine Concall and heard this:

“We indicated last time that there was some issues with the inventory pile up in our customer related to pharma business - that commentary was specifically related to one product for which the end market is ARV’s and this product actually primarily goes into unregulated markets in Africa etc and is primarily financed by this Bill Clinton and Gate foundation etc and because lot of those funds have been diverted to providing COVID Vaccines - so there is no funding available right now for this. We expect that that issue to continue at least rest of this financial year. For our internal calculation, we are assuming that we will actually not see any business from that this financial year and started looking at opportunities to remap those assets.”

So destocking will continue till q4 of this financial year, but in last year concall Dr chava was questioned by an analyst that whether the growth in sales is due to migration from 1 month inventory to 3 month inventory? To which dr chava replied that "growth in sales is not due to the inventory shift from 1 month to 3 month. And they will get the same kind of orders what ever may be the inventory policy at purchasers end. "

Now the sales are affected due to destocking which clearly implies that either the management has misled the investors or they don’t know their business.

Now people may say that Dr chava said this with regard to fdf and their fdf sales grown when compared to last year.

But we need to remember that laurus labs will supply arv api to other fdf suppliers also. If their fdf sales affected then they will not purchase api. Laurus may have grown fdf sales due to other contract manufacturing orders but their arv api sales clearly affected due to the inventory change. The management should have come straight on this in their q4 concall of last year.

I know this is in retrospect at least here, or I don’t know if I posted in this thread before. I somehow could not believe the management because whatever I researched pointed otherwise. This is from late Oct/early Nov 2020

I consequently exited the stock in November and looked a bit of a fool (although I put that money in Tata Motors around 150, but thats how the brain works). I felt 350 was fair price and things were already priced in but the euphoria took it to higher levels as it always happens.

Even now Laurus might be a good stock for a long-term investor but it is still an overpriced stock for someone with a short/medium-term view.

Problem happens when you enter any stock which is in its growth trajectory, its impossible to get in at cheap valuations as markets always keep them at high untill the growth is over and u need to be Naste Damus to know in advance which quarter growth will be subdued, orice correct by 30-40% in a blink, Laures, Balaji Amines, Deepak Nitrite, Mastek, to name few examples. Its a painful last 6 months avoiding these stocks and seeing them rising like phonix, reality is surfaced in last 10 days which is a sigh of relief and testimony of keeping at bay was right decision. I agree with you views that one time demand coupled with logistics issues has created this export/import demand mismatch hence earnings might get impacted once things normalize, need to carefully select bets.

Can someone please let me know if my understanding from last few messages is correct:

The management is in denial that growth in ARV APIs was because of sudden increase in demand for ARV drugs as patients were prescribed medicines for few months rather than usual practice of monthly prescription? There are few points which indicate otherwise.

If this is true then will need to know if this going to be usual practice in future? If so, then it will result in sort of lumpiness in business. And second thing, why management is not being upfront with shareholders?

And it seems that the company disclosed the life sciences cdmo deal along with the results instead of as and when it is signed. It may have done to support the perception about the stock. The management is more concerned about the share price than the proactive disclosures

Disclosure:invested

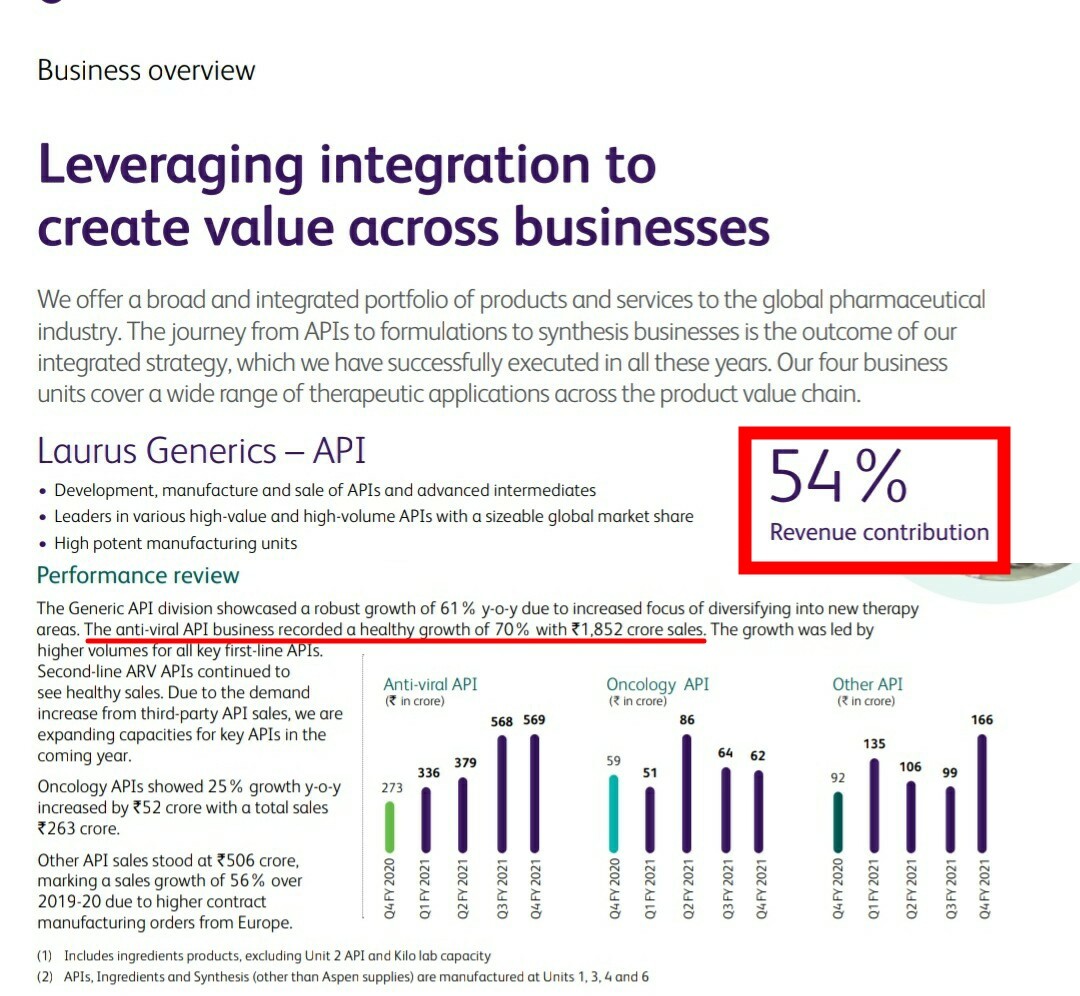

As everyone know, ARV API has been the cash cow of Laurus labs. (They are reducing the dependence on ARV API) They generate significant portion of revenue from Anti-retroviral API & FDF which are used in the treatment of AIDS.

There has always been attempts to develop vaccine against HIV. Past attempts were unsuccessful, yet couple of new clinical trials look promising. (Moderna’s mRNA based vaccine is one of them.They are also in very early stages, to comment)

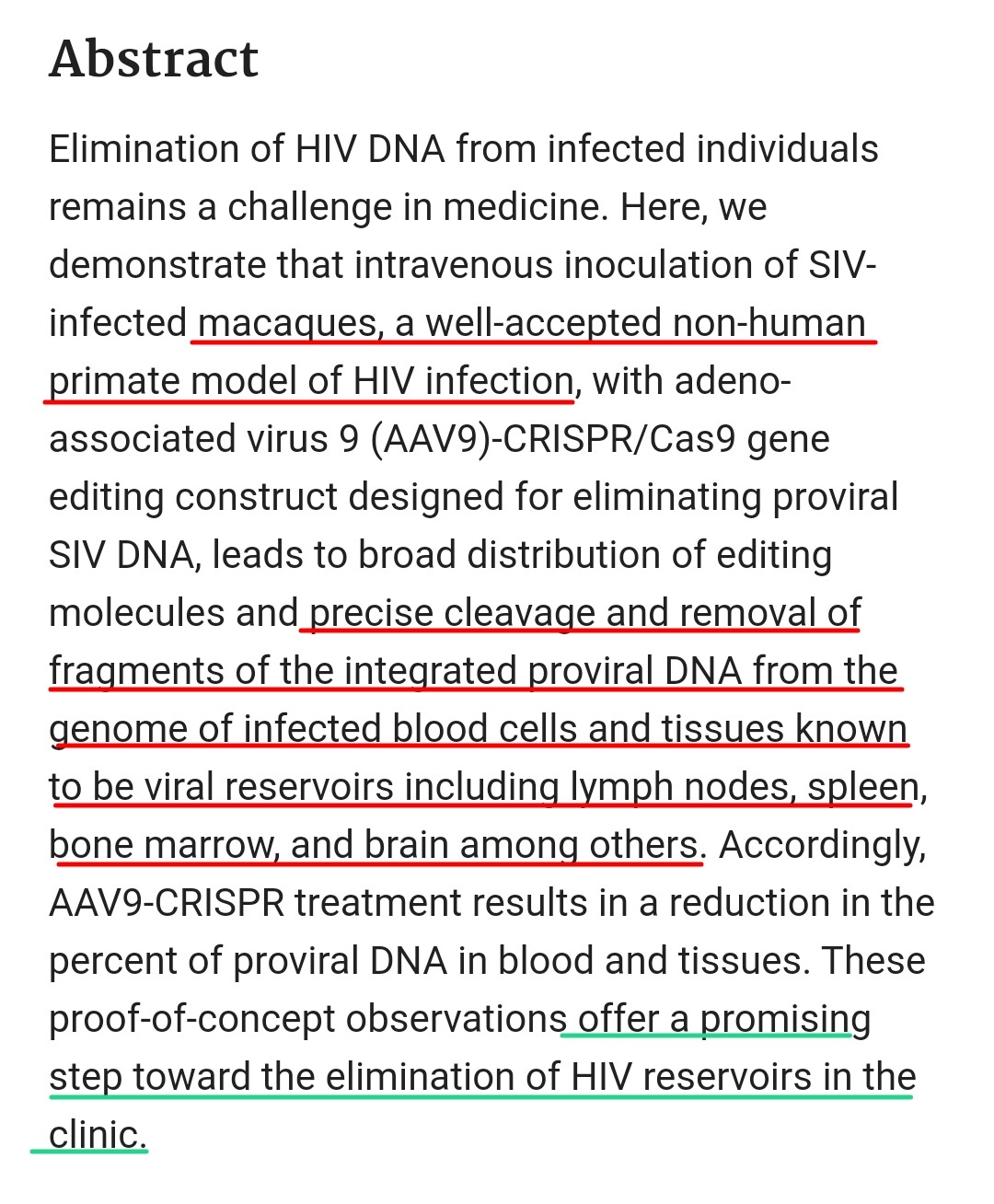

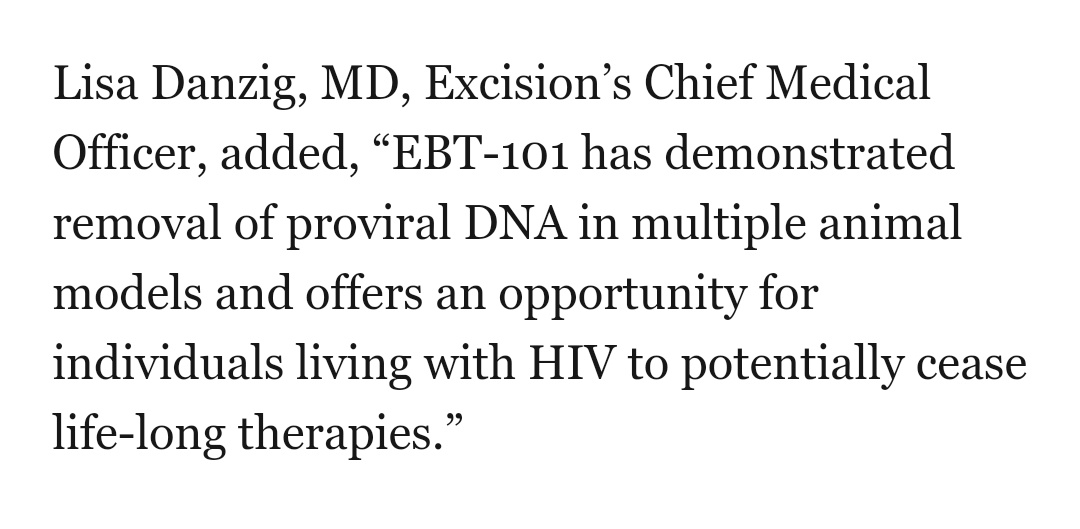

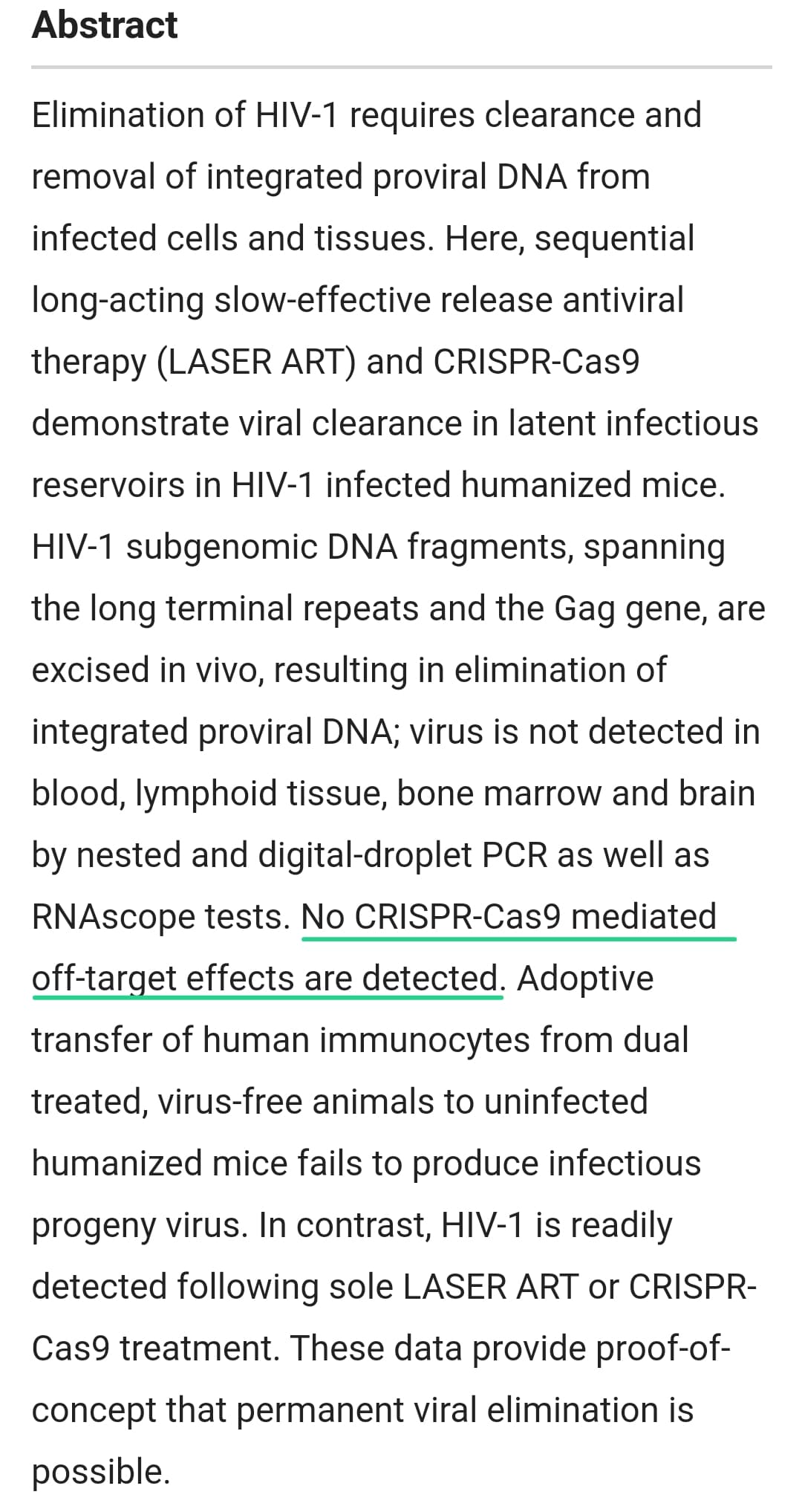

Why does this look groundbreaking to me is, because they were successful in eliminating HIV on multiple animal models including humanized mice and non human primates, that too with a one-time dose. This is the first time HIV is cured on an animal model.

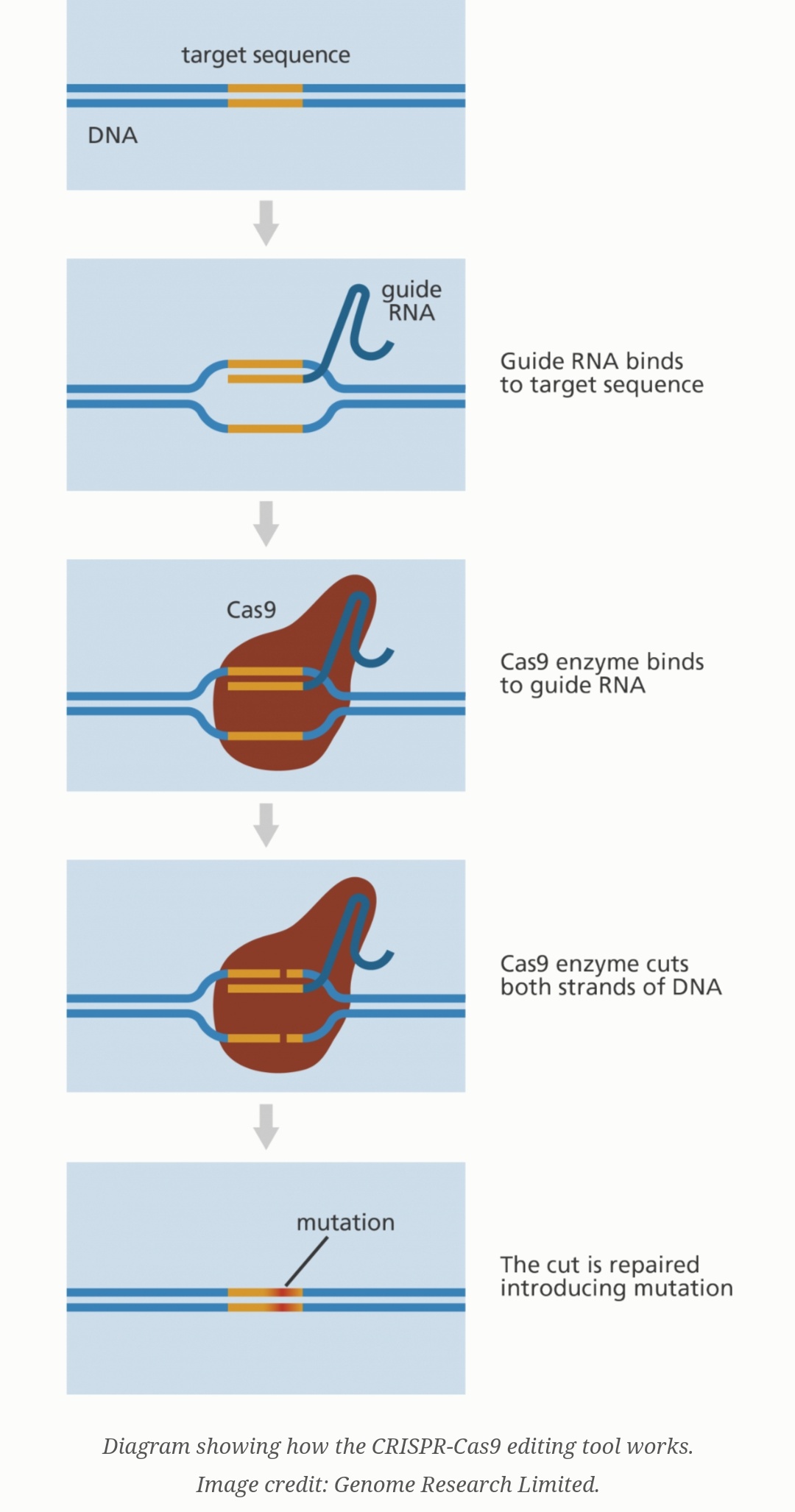

Talking about CRISPR-cas9, it is a nobel prize winning(2020) discovery, first found in bacteriae, through which bacteriae avoid virus(bacteriophage)infection.

CRISPR are basically DNA fragments which the bacteriae collects from the viruses that previously infected them. Based on these CRISPR sequence bacteriae develops complimentary RNA sequence (guide RNA) which can attach to these CRISPR sequence. cas9 is an enzyme which can break the DNA strands with the help of guide RNA.

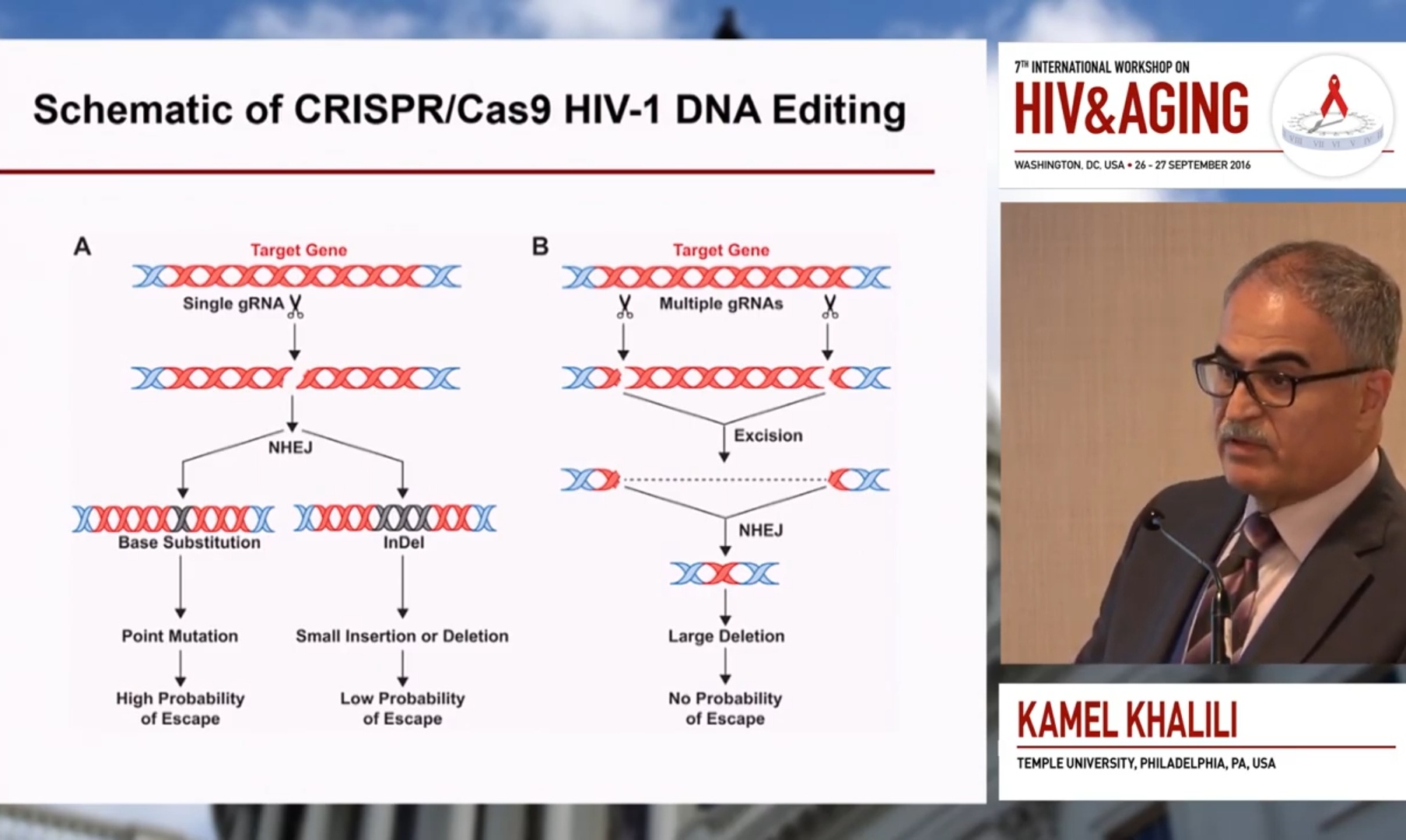

When bacteria encounters the CRISPR sequence again, the guide RNA will attach to it and cas9 enzyme cleaves both the DNA strands at that site. The cut is repaired introducing mutation, which makes the virus inactive. (This is the basic principle of CRISPR)

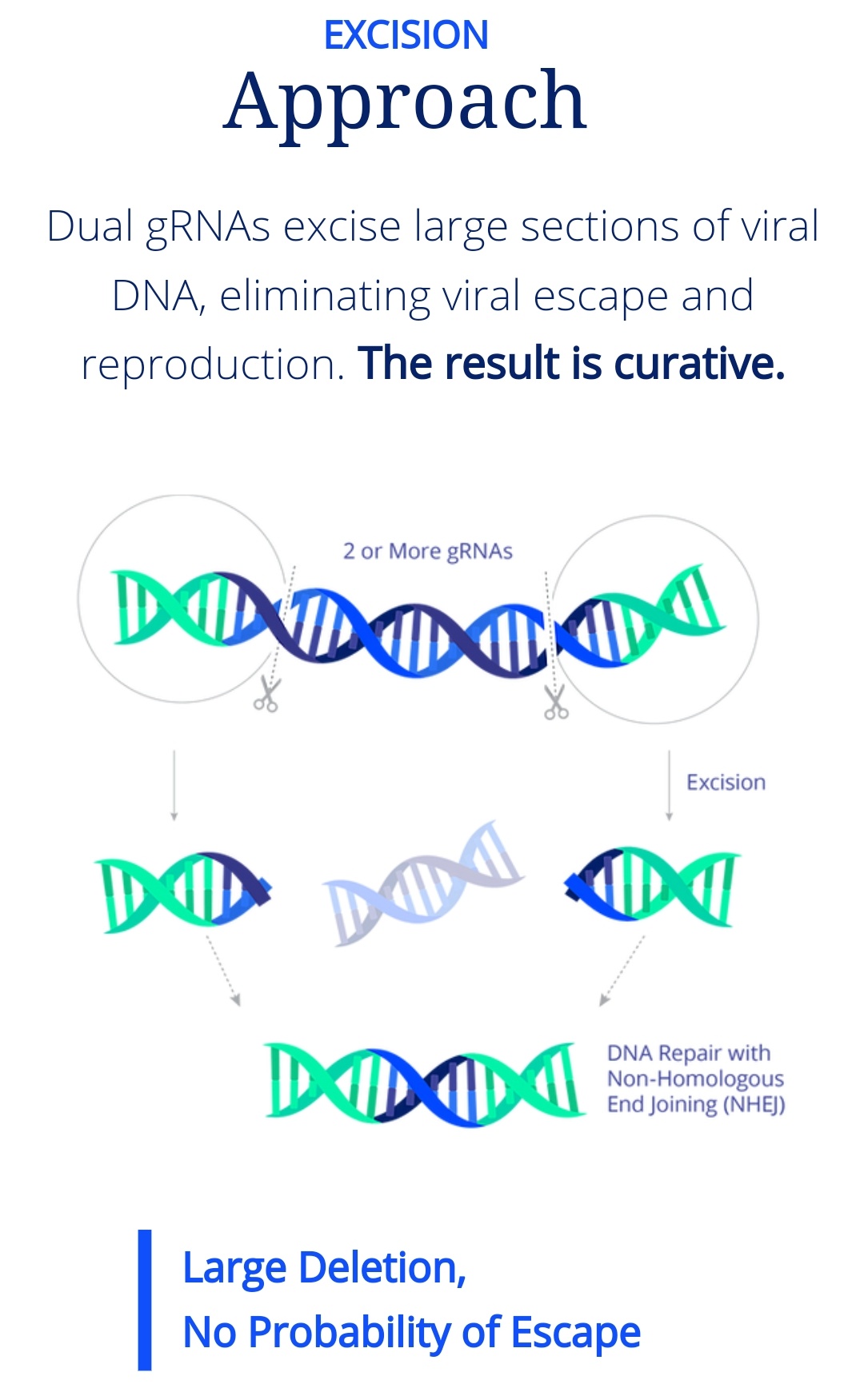

Coming to excision bio’s approach, they use 2 guide RNA to cut 3 sites of HIV genome making deletion of large portion of HIV genome. (It doesn’t cut human genome).This deletion of large portion of HIV genome makes it unique with no probability of escape. They have demonstrated it on animal models.

There has been similar gene editing studies in the past which were unsuccessful. Difference here is, instead of making a single cut in viral sequence, excision bio is making 2 or more cuts which thus delete a very large portion of HIV genome.

Safety is a major concerning factor. They should demonstrate there is no “off target effects”. If cas9 complex cuts any genome other than it’s target, it can cause side effects. In previous animal model studies, there was no off target effects. This is very promising and point towards a likely successful human clinical trial.

If you are curious to know more about excision bio’s approach, check this interview of Daniel Dornbusch(CEO of Excision Bio) by ARK Invest

This new approach looks groundbreaking to me.This may take 4-5 years to reach commercial stage. (If efficacy and safety is proven, accelerated approval can occur given it’s spectacular benefit) If it is found successful, it can replace the current anti-retroviral therapy. The problem with ART is, it is life-long treatment,with lots of side effects. CRISPR approach can avoid all these providing a cure with one time treatment.

This is a great risk for Laurus probably after a few years. By that time, Laurus may reduce it’s dependence on ARV API. Still, there might be significant dependence on ARV API & FDF.

One can’t say whether the new CRISPR approach would be successful at this stage. (It looks great for me)

You should monitor the progress on this field if you are heavily invested on Laurus.(Personal opinion)

A similar case played out in Neuland labs - pattern seems similar here as well -

Short term past performance pattern for Laurus stock price and biz is - FY 21 Q2 to Q4 mega rise on back of exceptional performance both YoY and QoQ 》 extrapolation leads to froth building by Q1 results 》2 Qtrs underperformance in Q1 and Q 2》Thrashing by mkt with 30% from top and possibly more 》 what happens next?

Given high base of remaining quarters in FY 21, YoY beat is far fetched - IMO A QoQ improvement is first sign of stabilization, before there is YoY beat which will most likely come in Q1 23 supported by low base and expectations.( currently happening in Neuland)

Can Q3 be a beat to Q2 revenue with margins holding/improving a bit? IMO this will drive stock price performance in short term. If one is a long term investor, it doesn’t matter much as Q1 23 onwards market will see what it likes to see, given base will normalize and multiple capacity triggers.

Going by stocking theory and inventory sitting in market - destocking at some point will normalize - overstoking logically has reflected in Q2 to Q4 21 numbers for laurus( high ARV pie growth against single digit normal) - Good part is that FY21 Q1 and Q2 have elapsed as well as part Q3, logically patients would also run out of 3 or 6 months quota Given in Corona times and bringing back normalcy in demand.

Q3 could be better than Q2 and Q4 better than Q3( even if ARV stays flat , rest of API are doing well QoQ)

FDF and CDMO has also seen QoQ drop - FDF supported by new capacities is likely going to be better with each quarter, CDMO is lumpy QoQ but have done very well at HoH hence for next 2 qtrs could be flattish but good on YoY.

Above is speculation at best, can be completely wrong.

One additional sign on lighter note is that activity in this thread will slow down significantly as well as social media discussion - can take a month or two, At this point there are more reasons to be Pessimistic on near term performance but that is precisely what long term investor and believers need.

Great insights, thank you for sharing the details. I have one question here, Cost of this vaccine. Given that Laurus is mainly supplying to LMIC countries, I doubt if this vaccine will be available in LMIC market before the patent expires. So I would expect this vaccine to not hit Laurus markets before 2030 or 2035.

Neither vaccine nor CRISPR gene therapy for HIV is commercial. They are in early phase 1/2 stages. Once it is commercial, cost wouldn’t be a major issue for low income countries as there are various organisations providing funds for HIV treatment. It would be global objective to eradicate HIV as early as possible once the cure has been found. So funds will flow in, as it is everyone’s objective.

Is it just a coincidence that the numbers and narrative have changed/ become more realistic after Dr Chava sold his equity at elevated valuations to reduce his pledging to Nil.

Laurus has been a case study in looking at investor expectations from a company. Right from Sep 2019, there has been consistent quarter on quarter growth in profits till March 2021. And since past 2 quarters there has been consistent de growth quarter on quarter.

After seven quarters of consistent q on q growth, investor and analyst expectations are often high and there is a lot of extrapolation happening for next few quarters. So when numbers do not meet expectations, or in fact actually disappoint and stink, there is a rush to exit by majority of investors. That is usually reflected in sharp price cuts in stock price. And on the way down it keeps appearing more and more attractive to those who compare valuations of the company on the way down as compared to peak valuations when stock price was close to its peak. But one thing that needs to be kept in mind is that many a times the peak valuations are often difficult to be accorded to the company even after the slide in performance of the company halts and it starts showing improved performance. So even though the company does perform well, there are opportunity costs involved with holding on to a stock undergoing de-rating. Many investors have the mindset to sit through these periods of time without getting perturbed. But a vast majority start getting jittery after the slide in price intensifies and start first blaming the management or whoever is at hand and then at the fag end start questioning their conviction. These are the very guys who throw in the towel at the precise time when its an attractive bet again.

This cycle repeats itself on and on. Only the name of the stock changes. We have quite a few well discussed former market and VP darlings like Kitex, Avanti, Mayur uniquoters etc to learn from.

In case of Laurus this is how scenarios look like -

Consolidation phase from FY22 to FY23, while cash flows are being diverted to grow non ARV business and CDMO + bio business.

Management succeeds and market cap of FY24/FY25 is 2x of today

Management fails due to various reasons like CDMO business does not scale up, non ARV business is more competitive for Laurus than ARV, they do not enjoy same moat there, FDF business faces pricing pressure etc etc.

So next steps for long term investor who is business focussed is to track the thesis periodically, if it seems to be going in right direction stay, else find something else.

“Stay detached from one specific stock and focus on portfolio level returns”