Can anyone point out how much is Laurus lab’s dependence on China for raw materials? I couldn’t find that in previous concalls.

13 Likes

As per my understanding for CDMO space the raw materials and logistics are paid for and arranged by innovators. In cdmo segment margins will not be affected much due to the above reason, but for api segment they source the raw materials themselves hence will it affect margins but how much impact will happen will only be clarified in the q2 results commentary.

2 Likes

Can you kindly show any management commentary (or any other resource) regarding this to back your claim?

No I don’t have any specific source for this claim but as per my understanding, by definition cdmo companies offer manufacturing as a service, in cdmo space the innovator transfer the tech and and know how to manufacture a substance/ NCE for clinical trials or for commercial sale. the CDMO’s may not get to decide from where to source the raw materials, their job is to efficiently manufacture and deliver the goods to the innovator.I request experienced boarders to make a comment.

3 Likes

https://www.bseindia.com/corporates/shpSecurities.aspx?scripcd=540222&qtrid=111.00

FII increase holdings

7 Likes

We estimate that Laurus’ dependence on Chinese imports is in the range 50-60%,

which was 70% a couple of years back- Brokerage (FY20 Report)

22 Likes

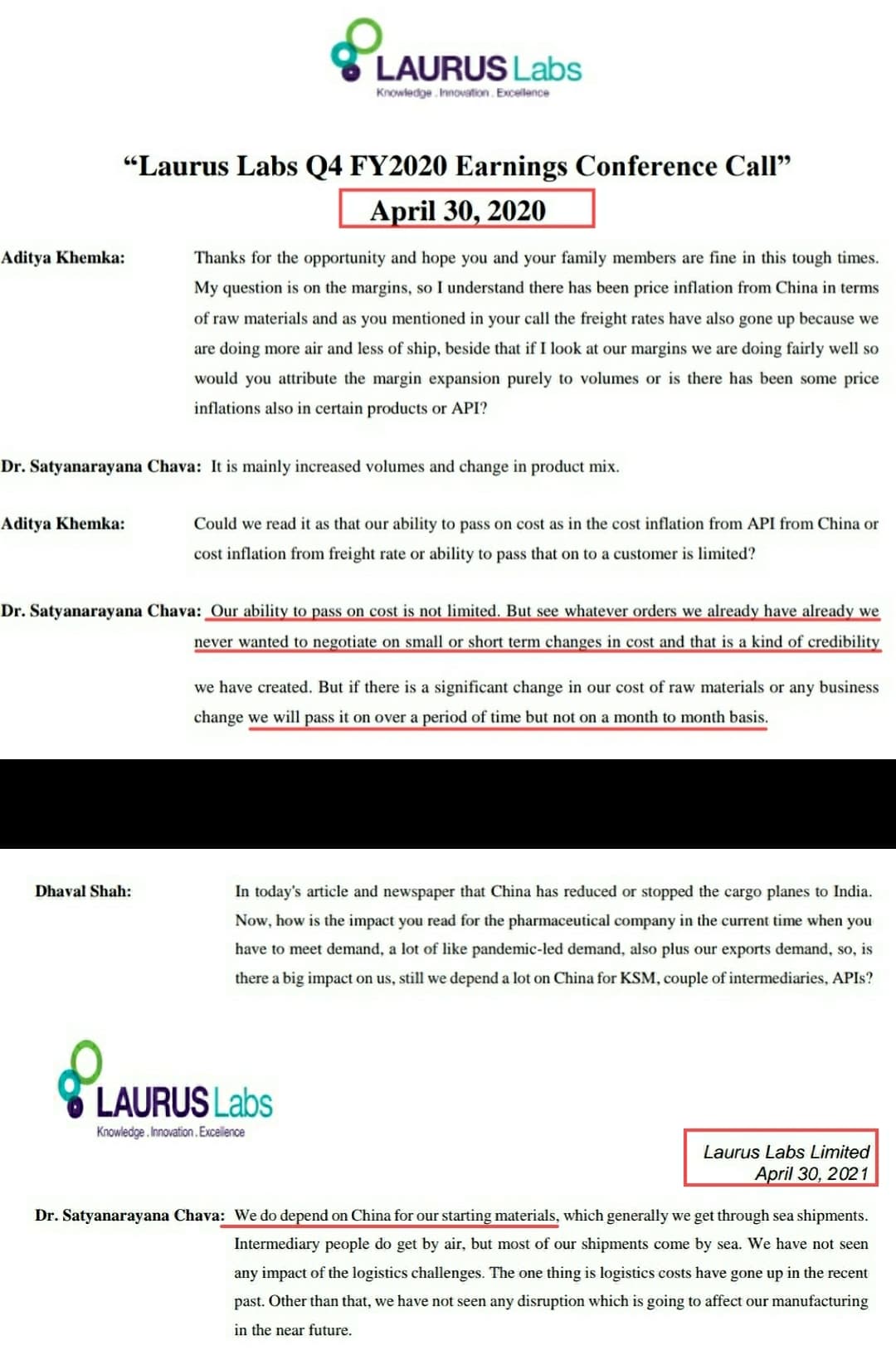

In the above interview of June 23rd 2021 , Dr satyanarayana chava ceo of laurus labs at time stamp 1:50 clearly tells that they don’t depend on china for any intermediaries but they source some ksm but they have also approved enough local suppliers to derisk their supply chain. The current narrative of laurus labs dependency on China for ksm is somewhat blowing out of proportion.

20 Likes

Exactly… Their topline should not get impacted much but KSM is critical starting point if they have to source from alternates (India) its going to be highly priced. Hence impact on margins. Only Results will show the magnitude.

But at the end of the day even franchise like Asian Paints not able to pass on inflated RM cost post a limit to customers. With that hypothesis Laurus competitivness and vision is Not broken in any possible way. Just an aggravated panic.

Disc-25% of portfolio from lower levels.

12 Likes

Dear Wordlywiseinvestors …. kindly provide some data or credible source/ explanation to support your claim.

Dr Chava clearly says they don’t depend on any overseas suppliers for intermediary, since they are fully backward integrated. They approved enough suppliers for KSM, as a de risking strategy.

Recent update by company secretary says there is no constraints for logistics and Raw materials, at least no more than they were during the same time last year and company had taken all necessary precautions to address the same.

13 Likes

Not directly relevant to Laurus but helps with a peer commentary on KSM+ solvent scenario - listen at 44:00 onwards.

Will remove post in some time as Laurus own results to be out soon.

8 Likes

Navin Flourine makes a point on ARV, Kindly check transcript after 1:01:10

15 Likes

If this is true then there will be impact on laurus labs api business, but as per my understanding hiv infected people won’t be able to manage if they stopped taking medicine. One can’t divert funds fight another pandemic. Ultimately its human lives.

3 Likes

This issue of ARV tender postponement was explained clearly by Dr. Chava in Q1 Concall.

There will be no impact on companies who are present suppliers of existing tender received in 2018. Due to Pandemic new tenders will be delayed by one year, that is till next year. Present suppliers will continue to supply till new tender. Inspite of these issues Laurus expect growth in single digit, even in ARV business. This issue will possibly affect new aspirants like ? Navin Fluorine …or others.

Here is the part of Concall transcript, page no. 17……

Question: My question is for Dr. Chava. I guess the approvals for global tenders in FDA formulation is valid for three years. And I think approval you got in 2018 for this global tenders would be expiring this year. Can you please let us know if this approval is getting renewed now?

Answer:

So the global fund tender was for three years, you are right. And due to this pandemic, they extended the tender period from three to four years.

Question :So still next year 2022?

Answer: Yeah, these tenders are valid until end of next year.

Question: My question is regarding ARV API revenue. May I know whether you anticipate any growth in FY’22 compared to FY’21? I’m asking because in last concall, you guided for a single digit growth for FY’22 for ARV API. Is this guidance stil valid?

Answer: we would expect so.

10 Likes

The raw material cost pressure on companies which are mainly dependent on china will be here to stay for some time, may be few quarters. Whether the companies are able to pass on the cost and to what extent will determine the pricing power they have. This will be a real test to watch out for in Laurus too. In any case, the surge in raw material prices will surely impact margins in the short term as normally it takes time to re-negotiate prices with customers, which wont be immediate. Further, the regulators wont allow sourcing RMs from different suppliers and though can be done, is a gradual process and wont happen overnight.

Next which has been a big concern for importers is the rise in sea freight. I know a few manufacturers, who claim this quarter the rise in sea freight has been exponential. Laurus is not immune to these factors and will be impacted in the short term. The market is already aware of these issues and it can be seen in the stock price. Whether all the above is already factored in the current stock price is a wait and watch. Still it doesn’t guarantee brakes on any further downside as market has its own wisdom.

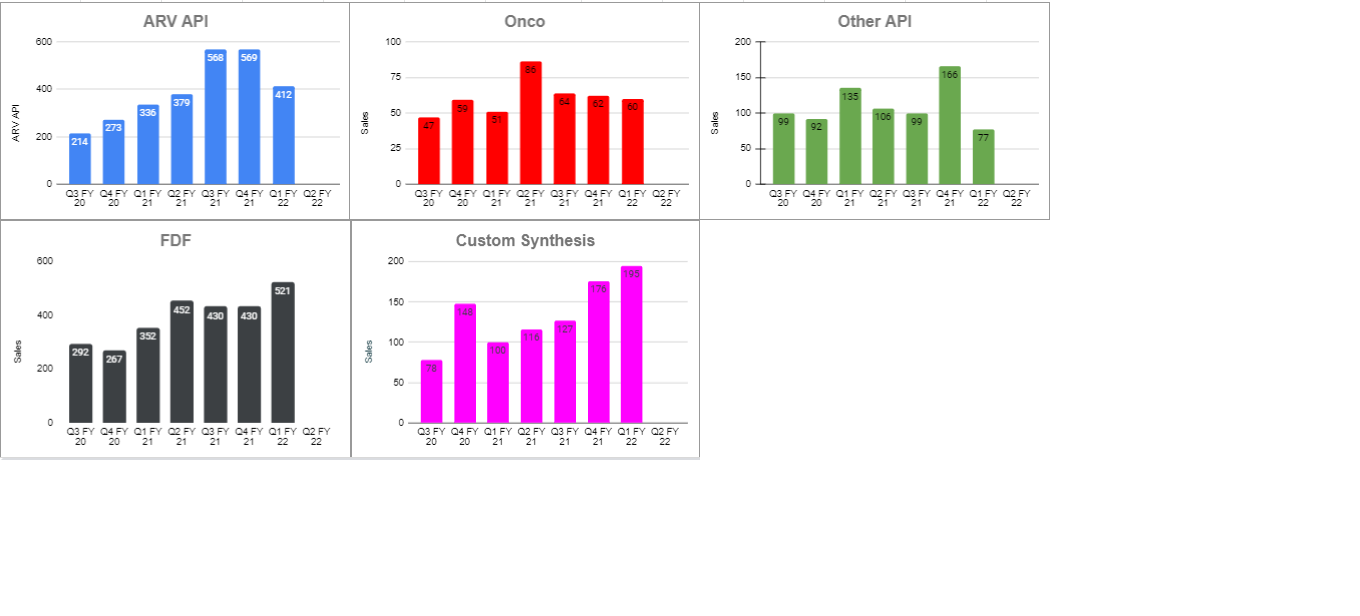

But what one doesn’t need at this stage is any de-growth in top-line on account of disruption in sourcing raw material prices and logistical issues. The ARV API growth is already tapering and much cant be expected from it. The Bio division is too small to make any meaningful contribution. The other APIs have always shown erratic numbers quarter on quarter and we are unsure whether this quarter is going to be big. So the growth mainly has to come from CDMO and FDF. If by any means the top line remains sluggish, then the tail winds atleast temporarily for the company seems to be over and the stock may see much downside. However, this may give good opportunity for making fresh entry considering the valuations vis-a-vis the problems being temporary for the entire industry.

25 Likes

Thank you Worldlywiseinvestors.

As you said, this report got published by Ambit capital on 03-08-2020. So 50-60% was possible dependence on China by Laurus lab both for Intermediate Raw materials and Key Raw materials….that was 15 months back. Much has changed since then.

As of now, as Dr Chava says…Laurus is not depending on any overseas suppliers for Intermediate RM, since they are fully backward integrated. And approved several suppliers for KSM.

Ambit capital Report on 03-08-2020 goes like this……

China supply issues of the past and current COVID-19 outbreak: We estimate that Laurus’ dependence on Chinese imports is in the range 50-60%, which was 70% a couple of years back. It appears that the company has inventories for the next 4-5 weeks, but an elongated shutdown could considerably impact sales in 1QFY21. On a structural note, the company has backward integrated further into intermediates and APIs following supply and pricing disruption in FY19.

6 Likes

This was management’s communication 21 days back.

- Laurus Bio could contribute meaningfully from FY23.

- No meaningful impact of CRO problem on their numbers

- Non ARV APIs will recover in 2QFY22

- ARV APIs will normalize in 3QFY22

- Not worried on ARV pricing as cost reduction and volume growth can make up for the same.

I dont think the ARV business has deteriorated so much in 21 days for the stock price to fall. It is more like the tail wagging the dog. Some large holder/ holders decided they have made enough money in Laurus and sold out, causing the stock price to tank and everyone is trying to attribute the reason for the fall.

It is very possible that the seller/ sellers dont even know about the Navin Flourine comments.

25 Likes

Completely agree to the point of ascribing reason to an event which may or may not have any causation. My view is ARV API + FDF which is large part of business growing at slow rate plus tender nature will continue to weigh on upside to valuation till the time other business becomes significantly large so that any fluctuation in ARV does not swing overall performance wildly. Good part is that they already have this as part of strategy and looking at history i believe they should be able to execute it as well.

Discl - Invested

8 Likes

Very Informative 2 videos on the business of Laurus. Learnt few new things about Dr. Chava and Laurus Labs

8 Likes

Q2 results,

3 Likes

As per my view the result is inline with the market expectations, everyone is looking at margin which came about 29% and I don’t think laurus has passed on the input costs to customers in q2( will get clarity in tomorrow concall), but 29% is still excellent margin if you consider the current supply chain issues.

Like hikal , laurus also announced cdmo partnership with a big pharma, seems this is a big trend and laurus , hikal will invest lot of energy to develop this business.

Overall pretty decent result if you consider the commoditised nature of arv space.

Disclosure:invested since last 18 months.

20 Likes