A refresher on the basics. Please point me if there is a thread to post all such basics related to Pharma.

Courtesy : Nirmal Bang

A refresher on the basics. Please point me if there is a thread to post all such basics related to Pharma.

Courtesy : Nirmal Bang

You can post at this thread, I guess.

DIIs/FIIs have increased stake by 1% in Q1 as per latest SHP

Does any one have inputs regarding the outcome of AGM ??

held on 15 July, 2021")

Dr satyanarayana chava didn’t participated in the voting of his bonus resolution. Infact Mr ravi kumar and laxman rao also didn’t participated in their respective bonus resolution voting. There was a clear risk of non passing of resolution still they stayed away from voting. Uploading: Screenshot_20210718-093604_Adobe Acrobat.jpg…

The remuneration paid to Directors is not at all unreasonable and is in line (actually less as a % of profits) with what is paid to Directors of Divis, Granules etc. The voting notice makes it clear that it is actually same in comparison with peer companies.

The respective Directors not participating in the voting when the item relates to their interest may be by operation of law, which bars their participation. Some one having knowledge of Companies Act (some recent amendment) may educate (I have no idea).

When there was revision of remuneration in the case of a Director of Divis. There was full participation and indeed it was required. The resolution marginally sailed through.

If there is no bar under the law from participation and still they did not vote, then it reflects high on the conduct of the person as it shows their mindset that they dont want to exercise their right in matters which relates to them and leave it to others to decide. Small Small things but helps us in determining the character of person.

Directors compensation of 24.5 Cr in case of Laurus is nothing compared to 83.88 cr compensation of Granules family director’s (only 3 members). Laurus net profit is almost double of that Granules.

Granules promoter director’s could have hired so much talent by limiting their compensation to 30cr and spending remaining 50 cr on talent acquisition…but they want to use all 10% of profit ceiling to distribute maximum salary among family members?as per company act nothing wrong but is this ethical? Even Devi’s management don’t draw this much salary

Laurus Labs results look not so good from initial look. Though there are some very good points too. So mixed results overall.

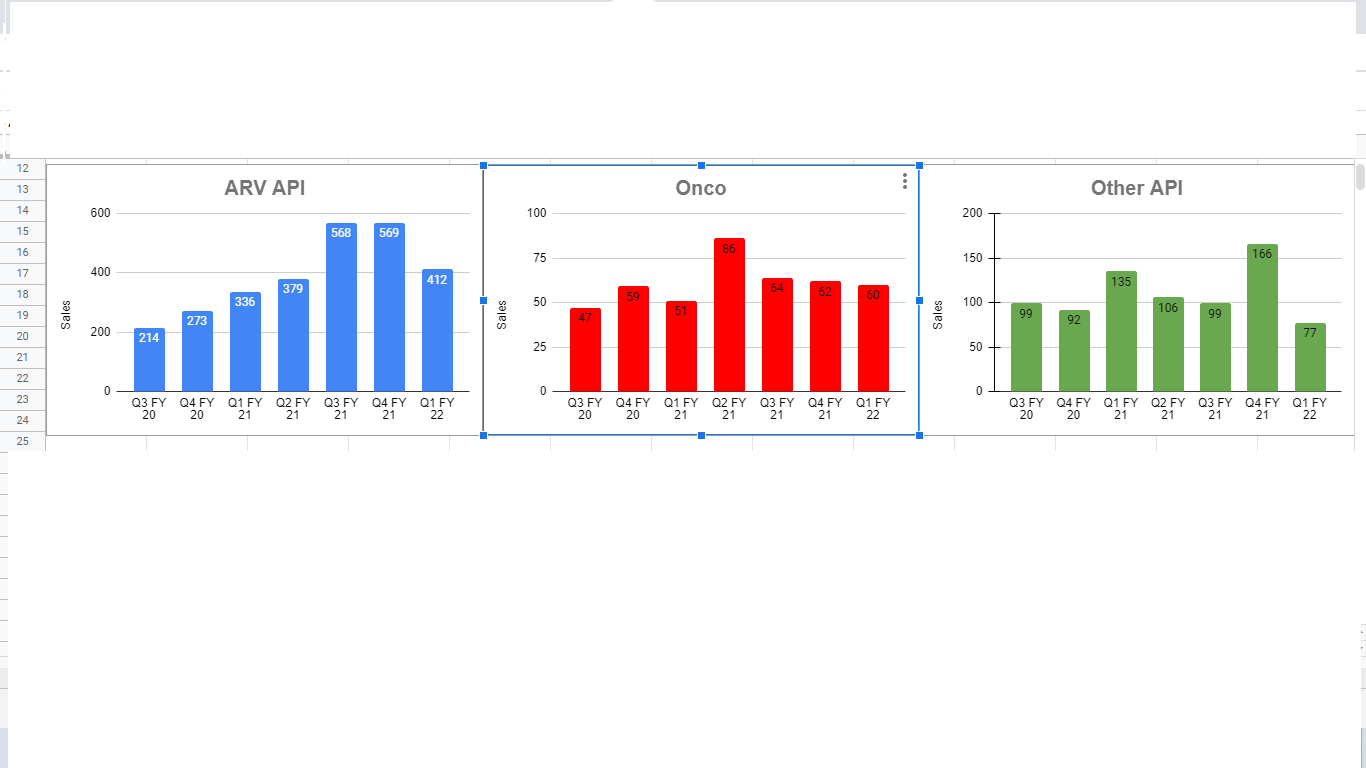

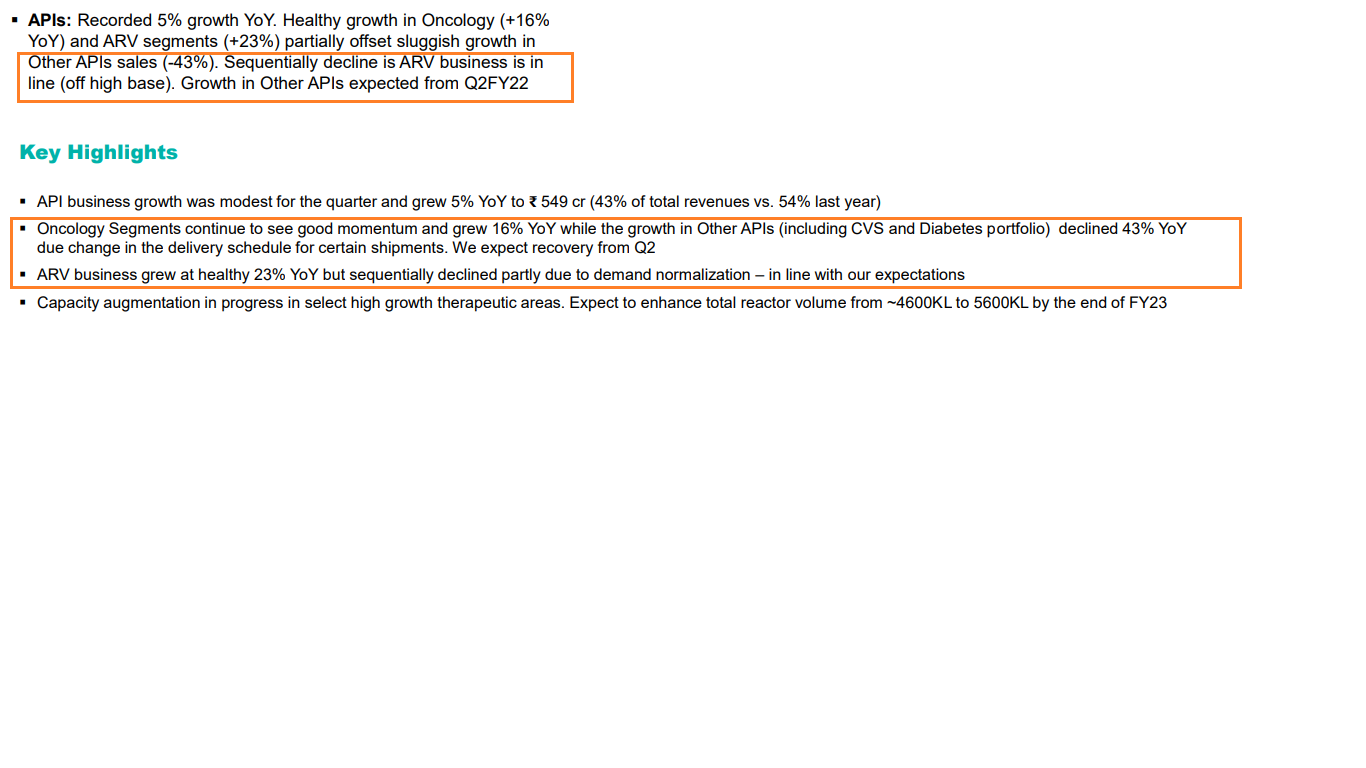

Bad part is revenue decline QoQ from 1412 to 1278 Cr. Major contributor here is API segment which de-grew 21% QoQ.

ARV API figure is 413 Cr this quarter from 569 Cr for last quarter.

Diabetes and other API is 77 Cr this quarter vs 166 last quarter.

According to management, other API de-growth was due to change in shipment schedule and they expect recovery in Q2.

They did say ARV API numbers are because of demand normalisation. So don’t expect recovery to previous levels here. Though we can expect normal growth like 10% YoY.

There are 2 good things in result. FDF segment growth was superb at 21% QoQ. This is great from high base of last year and quarter. Their brownfield expansion in FDF is complete and gives 20% higher capacity. The Greenfield expansion is expected to be completed by Q4 which will give another 80% capacity addition.

CDMO number is too good at 95% YoY growth and 11% growth from high base of last quarter. Note that in this segment YoY comparison is important since it’s seasonal. Usually Q4 is best quarter. So to beat last Q number is great.

Overall I think going forward, we should expect other API business to normalise but ARV API figures less than last year. FDF and synthesis doing great.

This year my expectation for revenue has come down to 15-17% growth as opposed to 25% thought earlier. Though Capex and business momentum say growth of 20+ will continue for next FY.

Need to see how market reacts. Stock has already broken 50 SMA but not with good volumes. Need to see price action and volume tomorrow and in coming days. I will hold on unless stock breaks 100 SMA with big volume. I expect sideways to downward movement till next Q result comes out.

ARV down 27% QoQ.

Q1 FY22 - 414 and Q4 FY21 - 569.

Also the fall in Other API is by 53%.

I think the market was anticipating QoQ decrease in revenues and profits. The share price started moving down from 680 to 690 levels probably based on this. Current price has discounted the QoQ degrowth. No business can continuously grow QoQ. Laurus did many quarters of solid QoQ growth and this quarter it couldn’t. Some capacity expansions kicking in and new products will add to growth from Q2 FY 22 onwards. Price will be moving sideways for sometime and will pick up steam after consolidation for a few weeks. If tomorrow’s concal indicates high growth business growth trajectory from Q2, it maybe move up and then go sideways.

Today 42 large deals happened, and as per stock edge amansa holdings sold 3361007 shares on 15th july 2021, it seems amansa is exiting laurus labs and it may be the reason behind the price fall from 690 levels to 600 levels.

disclosure:invested from lower levels

Great Analysis. My question is on operating leverage. If the company clocks 20% revenue growth what can be expected EBITDA growth and EPS growth?

Also, you mentioned that API growth can be modest at 10% but they has very strong sales in q3 and q4 last year. Do u think api sales can grow 10% in q3/q4?

Thanks

Laurus Labs Management On Q1 Report Card & More :

Chava here says:

We sold $10 million worth of API to China. We are thinking differently, we are seeing China as an opportunity to do business. We have leadership position in many products. We set the trend in these leadership products.

Sharing my takeaways from Dr. Chava’s interview with Bloomberg, and the earnings call. Please check all figures against the transcript when released.

Instead of chronologically writing down my notes, I’ve compiled them thematically.

API business is dependent on partners winning tenders and maintaining inventory. We can’t see ARV QoQ but YoY. We expect to do very well on YoY basis. Single digit growth for ARV API this year expected.

The dip was not due to lack of order book or opportunities. There was a schedule agreed between us and partners. We have not lost any opportunity, it’s just shifted from one quarter to the next quarter. We know how much volumes to make, and what prices to sell at. All are clear, no loss of quantity/price. Inventory is higher as customer intends to take it in the next quarter. Price is stable, there is no erosion. It is only movement of goods.

Notes: Fears of price erosion are unfounded and revenue should be made up in the next quarter. Dr. Chava explained it to be a delay in delivery rather than any change in demand.

We have filed 5 DMFs in Non ARV Non Onco category. We have initiated validations for a few API and expect to see significant growth from Q4FY22 onwards. Good orderbook visibility. Investing in capacity enhancement to meet demand.

API expansions are on track. We lost no time due to covid.

Total of 66 products in R&D pipeline. The overall addressable market size is over 37 billion dollars. Only 20% of the basket is ARV and 80% is non ARV. This is to diversify our revenue base by FY25. We don’t expect to launch these until 2024-2025.

In anti-diabetes → the new class of drugs will go off patents from next year onwards. We have a full basket of products, and have created capacities for both API/formulations.

In cardio-vascular segments, the nitrosamine impurities disrupted market share for the sartans. We have invested during this crisis to enhance capacity to make best quality product. We see opportunities to be a fully integrated player in both CV and anti diabetes. Capacity + Quality demands are high.

In second line, the product line is limited and competition is limited. Not many have integrated second line offerings. We are developing ANDAs to capture market not only in LMIC but EU/US. We offer the least cost due to being integrated.

Formulation sales in LMIC were outstanding. First time where formulations contributed more than 40% of our revenues.

Our major expansion in Vizag is formulation where we’re expanding to 4 billion tablets. We were on track to make first line in October, now it’ll be November. We’re running 5 weeks behind schedule on formulations. By the end of FY22, we’ll have 10 billion units of capacity.

We expect to maintain this run rate and do better than how we’ve done, going ahead in FY22.

CDMO has grown significantly, contributing 15% of our revenue. This was driven by sustained new client addition and improved revenue from current clients.

We are pursuing several active projects in the late stage clinical programmes. Capacity expansion to support growth plans. Commercialised Laurus Synthesis Unit 1 in Q1FY22. Dedicated R&D facility in Hyderabad and 2 units in Vizag will be operational in FY23.

750 Cr. of the capex plans will be in CDMO to meet demand. Will announce the nature of these late stage clinical trial deals by the end of FY22.

CDMO depends heavily on revenues from generics + API. In the next 24-30 months, it’ll be self sufficient.

In EU we validated 2 additional products as part of our CDMO partnerships. We expect a significant upside in FY23 in these products.

50% of the new capacity will be utilised in Q2, 100% will be used in Q3.

We are not happy with the 4 fermentation plants. We are looking at land to expand beyond 1 million litres.

Commercial fermentation opportunities for Laurus Bio are enormous. Looking for land parcels to build 1 million in the first phase. We will take land enough to take capacity over 2-3 million litres.

We have also seen growth in NA/EU markets. To leverage our front end, we’ve commenced marketing of in-licensed products. We have done 6 in-licensed products. Launched 3, 3 will be launched in FY22.

Filed two ANDAs in Q1FY22. With those, we have a total of 28 ANDAs with USFDA, 9 final approvals, 9 tentative. Two are Para IV, 7 FTF with a big addressable market.

Out of 7 FTF, we have tentative approvals for 3 of them, expect tentative approvals for 2 more in FY22. Current brand value for these products is around $5 billion. These launches will happen after 2025.

10 product approvals in Canada 5 have been launched, 5 more will be launched in Q2/Q3.

We have embarked on Capex plan of 1500-1700 Cr. of Capex for FY22 and FY23. All are on track except a 4-8 week delay. Invested 200 crores in Q1 for Capex.

In ARV/Formulation business, tenders are split quite evenly. The lowest bidder is not awarded 100% of the tender. Instead, awarded across the price band. If someone wants to crash the price, he won’t get 100% of the tender, but only 40%.In corollary, we can’t garner 100% market share, but can get the lions share.

Pre operative expenses will drop off after capex is done, leading to better return ratios post FY23. 1% of the EBITDA margin contraction is due to R&D reinvestment. Gross margin is up due to better mix from formulations.

Disclosure: invested, added a further position after the recent decline and commentary.

Overall looks like the fears for price erosion didn’t play out according to Dr. Chava’s commentary. They’ve got a visible pipeline not just for their target of 1 billion dollars in FY23, but the Para IV and FTF filings after. Their investments in CDMO, the late stage clinical trial news are all really positive.

I may have missed important information, inviting others to fill in gaps and post their own commentary.

Big takeaway (cherry on the cake) , move to 18:30 , a question on de-merger.

Dr. Chava didn’t rule out the possibility and the entire stage is being setup towards that direction

Three entities (Demerge and value unlocking is the modern Mantra in the industry, latest example is Glenmark Life Sciences )

But my understanding from his statement, Laurus Bio is already a demerged entity and too small to list right now and CDMO to become standalone, it will take more than 2 years.

So near future, there wont be any listings

Was looking at the API Revenues for the quarters and what I find is that the growth in Onco API and Other APIs (i.e.Non ARV Non Onco) has never been linear and there has been two down quarters after a good quarters. However, this didn’t gain much attention because on a sequential basis, the overall API business was always growing till FY21 mainly due to ARV API was continuously growing. It is for the first time, overall compared to previous quarter, there has been a de-growth.

| ARV API | Onco | Other API | Total API | |

| Q3 FY 20 | 214 | 47 | 99 | 360 |

| Q4 FY 20 | 273 | 59 | 92 | 424 |

| Q1 FY 21 | 336 | 51 | 135 | 522 |

| Q2 FY 21 | 379 | 86 | 106 | 571 |

| Q3 FY 21 | 568 | 64 | 99 | 731 |

| Q4 FY 21 | 569 | 62 | 166 | 797 |

| Q1 FY 22 | 412 | 60 | 77 | 549 |

Both the ARV API and Onco did better than previous quarter (yoy) and it is the other API which did 77 crore business against 135 crores (yoy), a fall of 43%. The management in the presentation says -

With regard to Other APIs, the management says Growth in Other APIs expected from Q2FY22 and the present de-growth by 43% is due change in the delivery schedule for certain shipments.

In the recent past, there has never been a single quarter where even one of the API segment de-grew on yoy basis. In the Other API segment, the Q3 FY 21 was flat against Q3 FY 20 at 99 crores and the management had given similar reason for the flat revenues i.e. change in delivery schedule, in its Q3 FY 21 concall.

“In the other APIs, our sales remain flat from Q3 FY’20 to Q3 FY’21. But for nine months, we achieved a sales growth of over 45%. The sluggishness in the segment in Q3 was due to changes in delivery schedule from some customers. We have initiated discussions with one of our key generic partner for contract manufacturing opportunities where we have several APIs, and we expect to build a dedicated block to accommodate these generic API contract manufacturing. We are also creating a lot of capacity for non-ARV APIs.”

“The Onco APIs will have revenues around Rs. 300, because we are not adding the oncology sales related to a CDMO business. This is a generic oncology APIs. And in other APIs, because significant revenue in other APIs is coming from contract manufacturing, so the sales will be bulky. So you might have seen in Q1, we have done Rs. 135 crores, in Q3, we’ve done Rs.100 crores, but in Q4, the sales will be bigger than Q3. So it is a timing of deliveries in other APIs. The products what we’re validating in other APIs, will see commercial sale in FY’22 and there are a good number of APIs commercial suppliers in FY’23. The growth in other APIs is also very good attractive rate right now.”

The next quarter Other API came strong and recorded 166 crores revenue in Q4 FY21.

It remains to be seen whether other APIs will make a strong comeback even this time. The management seems to be bullish in this segment as well when they say growth in other APIs is very good attractive.

Disc: Invested and biased