For a long term investor whether a particular stock is in ASM or not really dosent matter

7 Likes

Dear Friends,

I have a query regarding the below CAPEX and additonal capacity expansion.

Laurus in their call have said that they will be spending 1200crs CAPEX and enhance formulation by 80% and API by 30% (combined greenfield & brownfield ). The greenfield expansion will be commercialized in June’22 and the brownfield expansion will be coming up before next calender year.

Can anyone help me with the data in % terms of increase in capacity for Brownfield alone that would be coming up next calender year ?

Thanks & Regards,

Varun

3 Likes

In recent concall management highlighted that there are 10 companies competing for Tender business in Low and Mid income countries… It would be helpful if one can identify these 10 companies so that we can analyse compitive position of Laurus w.r.t others…especially if there is any other Indian company competing with Laurus.

WHO , have some contact details in this doc, if you want to reachout to find.

1 Like

Q2 2021 Earnings Call (118.2 KB)

3 Likes

Laurus Labs Q2 concall highlights -

- Total Sales at 1139 cr, up 60 pc yoy. Formulations business at 452 cr, up 180 pc yoy. In H1 formulation sales at 800 cr, up 200 pc yoy. Overall sales contribution from formulations at 40 pc vs 22 pc in Q2 last yr. Key drivers of formulations business - LMIC business in partnership with various global funds and PEPFAR.

Launched TLE 400 ( combo drug- tenofovir, lamivudine and efavirenz ) in LMIC mkts during the Qtr. Good growth expected going ahead. Good growth also seen in North America and Eurpean Mkts. TLE also launched in US.

- Leveraging front end in US by in licensing certain products. Mantaining Mkt share in Pregabalin in US. Company has 8 final approvals, 8 tentative approvals out of 26 ANDAs filed. In Canada - company has 5 approvals. 3 products launched, will launch 2 more this FY.

In Europe, contract mfg of certain non - ARV formulations doing very well. Have robust order book for FY21. Also have 2 products in Europe, will launch 1 more this yr.

- Company de-bottlenecking FDF capacities. The brownfield expansion under way will be avlb in a phased manner over next FY.

- Gereric APIs ( ARVs ) grew 20 pc qoq due higher volumes of Tenofovir and Efavirenz. Customers also buying more of Lamivudine and Dolutegravir.

Oncology API sales up 40 pc yoy led by key product- gemcitabine.

Other APIs ( PPI, Cardio, Anti diabetic ) grew 18 pc yoy due higher volumes of existing products and demand from contract mfg partner. Company has higher order book for APIs and has expanded capacities. **Overall - management very optimistic about growth in API business going fwd.**Plan to add even more capacities.

-

Synthesis business up 36 pc yoy. Currently, they have 50 projects, 04 have gone commercial.

-

H1- capex at 262 cr. Some of it should be operational in Q3 and Q4. Earlier budgeted capex for FY 21 and 22 was 700 cr, now revised upwards to 1200 cr due higher demand across various segments. Most of this will be brownfield. One greenfield unit at Hyderabad for FDFs also planned. This 1200 cr also includes another API mfg plant at Vizag.

-

Company doesnt feel that higher API sales are due to stockpiling by customers ( fearing a second COVID wave ). Company expects lower demand from Efavirenz but higher demand for Lamivudine, Tenofovir and Dolutegravir. Company expanding capacities of Tenofovir and Lamivudine.

In the next 2-3 yrs company expects 50 percent business from ARVs ( APIs + Formulations ) and the rest 50 percent form Custom Synthesis + Non ARV ( APIs + Formulations ). Currently, it is 60:40. -

As additional capacities become avlb in late Q3 and Q4 ( as brought out in Para 5 above ), company may see even higher growth than Q2.

Total capacity after capex completion( in 18 months or so ) - additional 30 pc for APIs and additional 80 pc of Formulations capacity.

-

TLE mkt moving towards TLD mkt. Company has absolute leadersip in Efavirenz but Evafirenz mkt is moving towards Dolutegravir. Now the company is strong in Dolutegravir as well. And because of backward integration in all molecules, there is great cost advantage with the company.

-

Broad capex split of 1800 cr - 40 pc on APIs, 40 pc on formulations and 20 pc on custom synthesis.

-

CDMO - currently working on 50 molecules, 04 commercialized. Company has interesting molecules in various clinical stages. Not all would be successful. Company also doing contract manufacturing of certain APIs and Formulations but they are not considered under the Custom Synthesis division.

Overall Revenue split -

Contract Mfg of APIs - 10 pc

Contract mfg of FDFs - 10 pc

Custom synthesis - 10 pc

-

Company has 7 APIs where their global mkt share is > 25 pc. Company intends to take this number to 15 APIs.

-

Future growth drivers -

APIs - new APIs in Non ARV and Onco space

FDFs - ARV, Non ARV in LMIC mkts, US and Europe

Custom Syntheseis - High potent steroids and Hormones

Disc : invested

22 Likes

Any view on how this going to affect Laurus?

6 Likes

If at all this is approved then it is advantage GSK, VIIV healthcare is subsidiary of GSK

1 Like

Laurus Labs has executed Definitive Agreement for acquisition of majority stake (72.55%) in Richcore Lifesciences Pvt Ltd

(Richcore).

Conference call on November 26, 2020 at 11.00 AM IST

Press release, which has more details on rational

5 Likes

With this transaction Laurus is trying to position itself as significant CDMO/Biotech player (pure play CDMO/Biotech firms generally command much higher PE multiples in current times). Although overall revenue contribution from this new venture might just be 1-2% of overall revenues for 1H-2021.

Overall, this new development sounds great on paper (actual execution remains to be seen), though I will give to the management for having transformed themselves out of ARV API’s in the past.

Disclosure: Not invested

8 Likes

Isnt laurus labs entering into uncharted territories?? Shouldn’t they focus more on the chemical drugs side instead of venturing into biotech? Laurus labs may be trying to do too many things in too little time, they are expanding capacities in api, fdf, and synthesis almost 80% and entering into biotech. Hope dr chava will be able to focus on all verticals and there wont be any execution risk.Hope they would succeed in this new venture but fingers crossed.

Disclosure: invested

7 Likes

Are they trying to take some small market share of Biocon who have been getting huge investments ?

Keyman risk has been brought up so many times in laurus labs thread. Do we have any information about their next level of management? Have they grown in the company? How many have worked for laurus for long time?

I recall a good discussion in the bandhan bank thread were folks mentioned a lot of middle/upper middle management are employees that have grown from lower levels.

4 Likes

Laurus Labs buys bangalore based biotech firm, adds another revenue stream.

2 Likes

Picked these up from google reviews about this company. Seems they were not paying some of their suppliers.

1. Rohan Hegde - 5 months ago

Claims to manufacture but it purely trading. Go see import data on Zauba. Obviously he is not paying suppliers and cheating customers by mixing.

First three transactions I did I eventually got paid very late. On fourth order he took triple the material paid me 10 % advance and disappeared. Now not taking call also. SAD!

2. Bharatiya Sena - 6 months ago

He stole my money! Must have used it to shine his bald head.

A real slimebag. Don’t give him any credit, advanced payment only.

3. Gand Sung-Lee - 5 months ago

Chinese suppliers have blacklisted Richcore. We all know his cheating ways.

He owe me 100000 USD for buying Trypsin and Chymotrypsin but never I see any money. Only lies lies lies.

I request to Indian govt. to do something about this man.

4. Nathaniel Jenkins - 5 months ago

How about show us the “factory” instead of your face.

Rich-core is an apt name. Wants to be rich to the core off other peoples money. Can’t trust him.

A bit dated rating report by Acuite on Richcore Lifesciences - https://www.acuite.in/documents/ratings/revised/18001-RR-20190607.pdf

- Has been a loss making entity since FY17

- No growth for the 3 years presented - FY17-19.

9 Likes

That’s why they bought it at a discount. Laurus can used their existing research and significantly add scale to the company. They are even getting rid of the name and changing it to Laurus Bio Pvt Ltd.

9 Likes

Talking Point With Laurus Labs’ Satyanarayana Chava:

14 Likes

Few important takeaways for me from the talking point video in as simple terms as I can write:

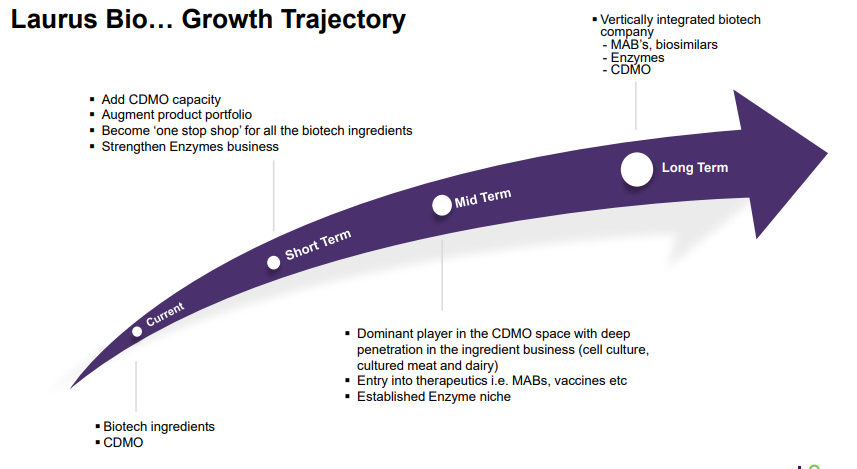

- Richcore will have a few synergies with laurus current mix. Overall it will be adding a brand new growth driver in cdmo. Richcore will be funding its own capex(new facility march 2021 and another one end of 2021) via internal accruals and debt. Laurus won’t be spending any more money on richcore next 2 years. In the medium to long term this will be a big growth driver.

- Current Growth rate in all areas is sustainable up to atleast FY 22. From FY 23 non ARV(generics) will be the main growth driver.

- Shift from China hasn’t shown fruits yet. They are seeing benefits in Custom synthesis as of now due to China but we LL need to wait for a year to see benefits in other segments. Fully expecting benefits in 9 to 12 months.

- Pricing pressures don’t seem to be an issue. Dr .chava explains this about each segment in detail in the video. When asked about risks there really don’t seem to be any is what he said though he did state that there are risks in general with any business and spoke about covid and how it cost them 30 Cr etc. With pharma when you build capacity for years their growth is basically locked in the way they operate.

So in short: over the next 2 years expect current extraordinary growth to continue and get an even bigger boost when China benefits kick in in a year. When stagnation in growth begins occuring non ARV will kick in with higher margins. And in the long term Richcore will kick in. So the investment horizon and visibility is huge. Risks look nominal though there’s always some risk with businesses. No obvious headwinds though.

Disc: Invested heavily. Not a sebi advisor. Please do your own due diligence before investing.

Btw sharing the concall conducted today for anyone interested in a detailed understanding of richcore. It was a long concall and I must confess I drifted off in-between and dint take notes. Was quite happy regards a new growth driver long term from what I did hear though. If anyone took notes please share(on a side note how awesome is it having a small cap company giving us shareholders so much information. A press release would have sufficed but they conducted a concall for the same. Some may not like the fact that management does so many interviews and gives us so many updates but I quite like it ![]() )

)

16 Likes

Laurus is my biggest position and I add to it every month and at every pullback. The only thing I didn’t like about the promoter updates on this acquisition is that they keep on mentioning there aren’t any risks. There are always risks in the business. Still I believe in their growth story.

4 Likes

No, he clearly said, “No business is insulated from risks”.

1 Like