Board has recommended a final dividend of Rs 14.50 per share

Highlights for FY21 include:

Revenue at Rs 54,497 million; decline of 3%

USD Revenue at $737 million; decline of 6.3%

EBIT margin at 14.5%

Net profit at Rs 6,633 million; decline of 19%

the patents portfolio of L&T Technology Services stood at 650, out of which 485 are co-authored with its customers and the remaining 165 have been filed by LTTS.

L&T Technology Services Becomes First PTC GSI Partner From APAC to Receive Advanced Partner Status. LTTS Recognized by PTC for Excellence in Product Lifecycle Management.

“We started the new fiscal with a strong performance, despite the pandemic related

challenges during the quarter. In Q1, we got our revenue back on the double-digit growth

trajectory and marked four consecutive quarters of operating margin improvement.

The deal pipeline is healthy across segments, and we expect broad based growth to continue.

Our innovation engine is matching the pace of our growth as we filed a record 23 patents in

Q1.

To further scale and strengthen our technology and capability advantage, we have identified

6 strategic investment areas – Electric Autonomous & Connected Vehicle (EACV), 5G, Med-

tech, Digital Manufacturing, AI&ML driven smart offerings and Sustainability. The focus will

be on innovation and solution building in these new age areas that will position us as the

partner of choice for customers in their next generation product development cycle”, said Amit

Chadha, CEO & Managing Director, L&T Technology Services Limited.

Highlights for Q1FY22 include:

• Revenue at ₹15,184 million; growth of 17% YoY

• USD Revenue at $205.7 million; growth of 20% YoY

• EBIT margin at 17.3%; up 520 bps YoY

• Net profit at ₹2,162 million; growth of 84% YoY

During the quarter, LTTS won 6 deals with TCV of USD10 million plus, which includes 2

USD25 million plus deals. Revenues from digital and leading-edge technologies stood at 54%

during the quarter

Patents

At the end of the first quarter, the patents portfolio of L&T Technology Services stood at 719,

out of which 531 are co-authored with its customers and the rest are filed by LTTS.

Our innovation engine is matching the pace of our growth as we filed a record 23 patents in

Q1.

Q1 FY21 was a weak quarter . if we compare results between Q1 FY22 with Q1 FY20 , the results are not that impressive.

Also LTTS capability in hitech,telecom, semiconductor & 5G is not that great . They just supply engineers & have no capability whatsoever by the LTTS themselves. All the spec/design/flow is done by the foreign MNC ( LTTS engineers work as contractors in the company i work for)

So when i look at their presentations & see below lines , i doubt their R&D capability (patents) even in other sectors

• Everest Group has positioned LTTS as a ‘Leader’ in the Semiconductor Annual Engineering Services PEAK Matrix Assessment ™ Report

I guess you know sometimes skilled contractors are getting paid more(and in turn generating higher billing for parent company) than a regular employee, specifically in onsite location.

Anyways you are most welcome to share your own personal opinions, but recent shareholding pattern, price action movement in stock price, today’s number and management commentary is indicating something different.

Most of the contract engineers are fresh out of college. Also most of the product companies eventualy will give permanent offer to good contractors (there is clause in contract preventing this but service companies are rarely in a position to enforce) . So usually most of the engineers (at least in my field) , who works in service company are low skilled or less experienced or are looking to go abroad (people join service company specificaly for US opportunity).

MNC hire contractors for usually 2 reasons

During lean period , they can easily fire contractors without much fuss (this can be one of the reason why results were bad in Q1 & Q2 FY21).

some middle management personnel in MNC gets a cut from service company (dirty secret)

There are lots of companies in any tech region offering contract engineers. Few of my friends even started service company 3 years ago ( play book is same . hire cheap engineers fresh out of college & guide them & sent them to an MNC). My point is there is no moat here .

Also when we compare results , please check my previous post . Results are amazing YOY becuase last year , Q1 was a very bad quarter . if i compare with FY2020 , results are very modest growth in 2 years & doesnt warrant this PE multiple. i have no comments on stock price movement .

Not sure about the MOAT of service contractors or the % that this contributes to LTTS earnings. On the topic of FY20 vs FY22 results however while the EPS growth seems modest this is partially due to the increase in depreciation. If we look a little closer -

June 19

June 21

% Change

Rev

1348

1518

12.61%

Op Profit

273

318

16.48%

PBT

277

296

6.86%

EPS

19.6

20.58

5.00%

I am not looking at this as 2 year growth due to washout 2020, but basically as YOY. So 15-16% operating profit growth yoy is pretty decent result. Considering that Q1 also witnessed a lot of lockdowns due to the 2nd wave the results to me are a pleasant surprise as LTTS cannot transition all work to WFH type consultancy. Regarding valuation agree it is looking overvalued but I have not yet gone through con-call for forward looking statements…

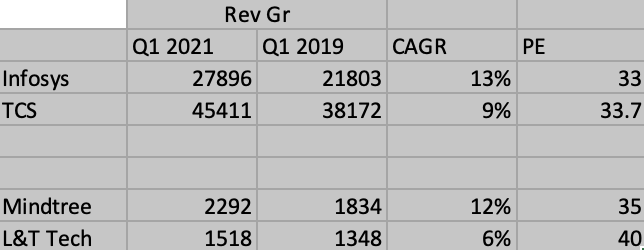

Ideally you should use CAGR formula as it is growth over 2 years , That way the Revenue Gr is just 6% against large cap IT like Infosys which is 13%

Unlike other sectors large cap IT players are actually global Midcap / microcap players in their market as this market is highly fragmented …

Unlike companies like Asian paints , HUL etc which enjoy 40%+ Mks , Infosys will be < 3% Mks in global IT services in relevant market … which means all strong IT service players have long runway from growth esp in vendor consolidation happens

With all due respect to all other views, lets look at two important things and we will get our answers on valuations etc. -

Next FY guidance

QoQ new deal wins and order pipeline

Today, these are two things which is driving valuations of most tech firms…If someone wants to do an exercise to compute, compare and share with us - it will be great and most welcome!

Disc: Invested & biased. Not a buy/sell recommendation. Maybe wrong in my assessments

(i) Large diversified clientele

LTTS client concentration risk is low as per FY21 and also reduced as compared from FY16. The dependency on Top 10 clients for the FY16 stood at 36 % which reduced to 27%. Moreover the company is not dependent upon one major client like closest peer Tata Elxsi which is greatly dependent upon JLR. Thus the performance of one major client does not affect the performance of company.

The company has a presence in engineering and research and development (R&D) services. Which are certainly new segments. Consequently there is growing interest in the past few years from clients across sectors. For instance, global telecom, automotive, aerospace, industrial products, heavy machinery, construction, and consumer appliances source their engineering and R&D requirements from India.

Certainly this enabled the company to withstand the slowdown pressures as exposure is not restricted to a particular end-user industry.

ii) Strong financial risk profile

The company’s financial profile continues to be strongly supported by healthy cash accruals, almost debt free balance sheet as well as robust liquidity.

(iv) Growth in FMCG and O&G sector (Oil & Gas)

As CAPEX is increasing in O&G sector certainly management is seeing some good opportunities in that sector. Moreover the FMCG segment has done reasonably well. Some of the learning the company had in FMCG segment, have taken into oil and gas segment also. The large deals we won, that is because of that

Hi, Overall company looks good considering L&T parentage, having larger number of patents, diversified among different domains like 5G,Industrial,Autonomous vehicles, Medical etc. But valuation wise company is trading at 63PE. It may be still cheap as comparative to Tata Elxsi. But 10 year PE is around 22. Considering company is growing at 10% or so, do you think it is still at reasonable valuation?

Disc - invested

“In terms of revenues, the transportation vertical grew 22% at Rs504cr, plant engineering grew 30% at Rs246cr, industrial products grew 25% at Rs322cr and telecom & Hi-Tech grew 21.4% at Rs340cr. Revenues in constant currency terms were also up 22% yoy at 6% sequential.”

It is on expensive side considering the shallow cyclicality of the business. Size of opportunity is big but buying at current valuations can be risky or at least mediocre returns must be expected in near to medium term.

Can you pls suggest in its listed history so far, which cycle was in progress last few years? Also, is currently an up cycle or down and where we are in this cycle?

Plant engineering maybe somewhat cyclical and capex dependent…what about medical devices, transportation, hi-tech, retail, telecom?