What is the advantage a pure-play ER&D co like LTTS or Altran have v/s a diversified IT services co such as TCS or HCL Tech?

One observation I had was that the number of co’s above USD 1 BN revenues were far and few in ER&D space this is a contrast v/s IT services which has a quite a number of companies with that scale. Now this could be because ER&D is still a nascent industry when compared to IT services which has matured in the last 3 decades or it could also be due to overall spends in ER&D are much lower that when compared to IT services. Or is it because of competition (captives?)

In the listed space there have been many co’s which are/were catering to this space but somehow not many have been able to scale- infact LTTS is the largest among them, despite being the newest co. The co’s I am referring to are Sasken (Semicon - flat revenues for 10+ years), Onward - gone no-where, Cyient, KPIT, Tata Elxsi while they have grown, however still very small. What is the reason? Is it focus on one specific vertical which makes it difficult to scale - sector/customer concentration ?

What are the barriers to scale in this business? What makes it difficult to scale?

Management in their con-calls has mentioned that unlike IT - this space doesn’t have that many players and thus the competition is lower- why is that- given the attractive economics of the business, why will this not change going forward?

Co specific

Given you have won many large deals in the last 2-3 years- what has enabled you to win such deals ? Were these won through a bidding process? Sales engine has worked very well - what has enabled it to work so well in the last 10-12 quarters?

Annuity v/s Project deals? How long are the project durations? Large Deals v/s other deals?

Status of SEIS beyond FY21?

Within the customers that we serve - how much of the outsourced Engineering services spend will be captured by us v/s competition, how has this changed in the last 2-3 years?

I dont think Happiest mind will compete with LTTS because its more product development and huge Engineering R&D company which is not available newly listing company.

Texas-based Orchestra Technology Inc., a specialist technology solutions provider for the telecom industry.

Orchestra will help bolster LTTS’ offerings in the areas of Network Engineering & Enterprise Mobility and open up new opportunities in next generation digital systems for 5G and IoT networks.

I have been seeing that LTTS employees and directors have been selling their equity for past 1 year. There has been significant net selling of ~1.64 lakh shares (Excluding a Gift of 5 lakh shares).

What do you infer from this?

@kshitijb

I think these are very insignificant quantities.

Employees are generally eager to sell shares and get money out of it.

Unless any director or ceo is involved in selling shares that too with a meaningful quantity, this should be ignored.

Any company which gives ESOPs to employees at many levels (even below senior management) does experience this frequently

Of the total quantity sold in the last year by employees and directors, 45% was sold by directors!

Also, the sold quantity in TTM represents ~0.165% of total outstanding shares and in terms of free-float market shares, it is ~0.64%.

The above calculation excludes 5 Lakh shares gifted by AM Naik (Director). Is there more information to whom and why these shares were gifted?

LTTS margins are less compared TCS almost 2/3rd , For that matter LT Infotech margins are also subdued. LTTS have employee cost similar to TCS but in addition they also have manufacturing costs (~12%). I guess it’s going to be linear story not an exponential growth like product innovation. Though they keep doing more and more innovation but it is not reflecting in the results.

Agree results do not reflect - so far. How do margins and manufacturing costs compare with Tata Elxsi? Say TCS/LTI vs LTTS Vs Tata Elxsi?

Earlier I used to also think that patents etc not contributing to results. Then I digged deeper and see that the areas and technologies LTTS work in is way different than LTI/TCS. Not saying that LTI/TCS are anything less but what I feel that over long term they may turn out to be not comparable.

It is if we believe in the type of work that LTTS does and see growth, demand for that kind of work and market leadership from LTTS then it can probably chart the course which will be different than LTI/TCS.

I see two scenarios -

One, where these niche areas remain niche - then growth is surely less than LTI/TCS but still decent growth.

Two, where these niche areas become mainstream in due course of time - Chances of significantly higher growth than TCS/LTI.

As a humble investor, I do not know which Scenario would pan out.

Disc: Invested and hence biased. Not a buy/sell recommendation

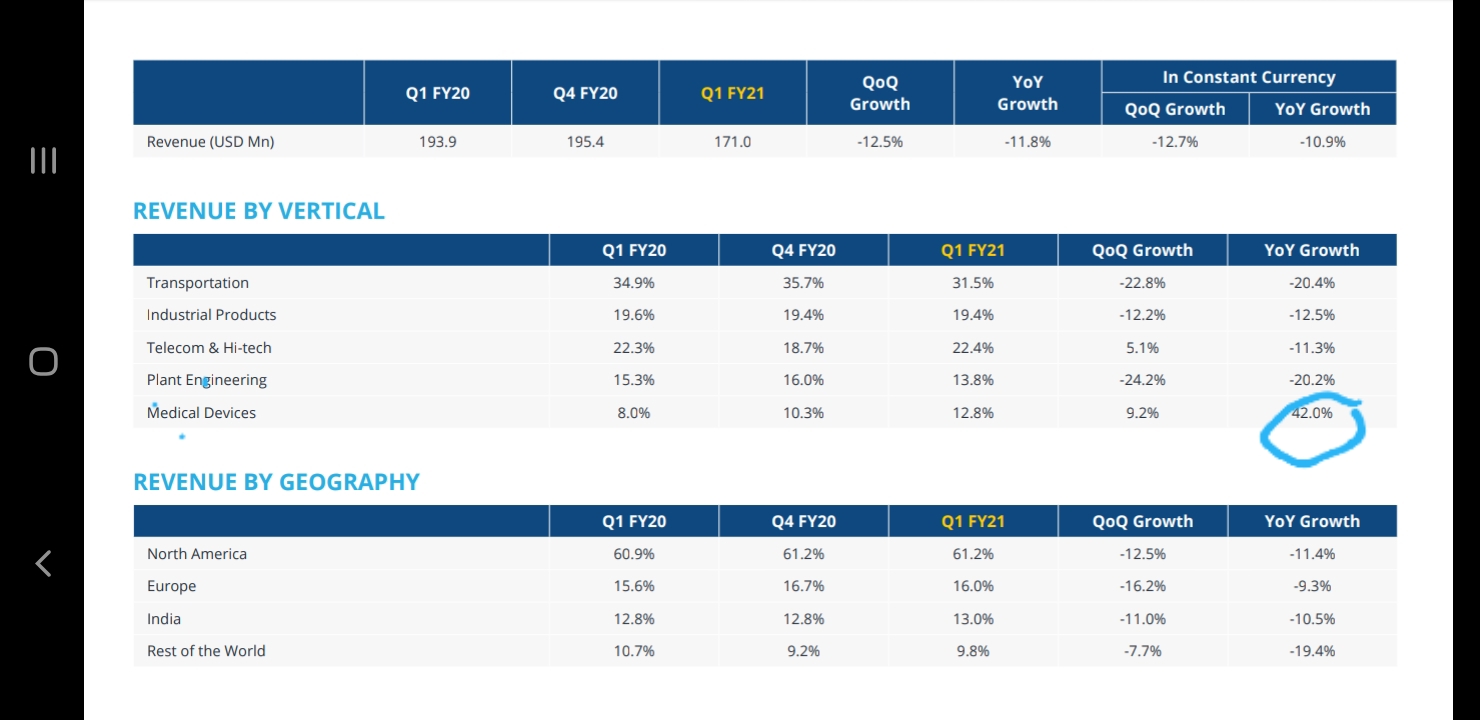

If you see the Q2 results, their platform and solutions business has started contributing. Platforms are nothing but some of the patents/solutions they have developed. ER&D is very much different from typical IT. We can’t compare LTTS with LTI, TCS or for that matter any other pure play IT company. Yes, the margins are less here but that is due to the mix of verticals they have. I think medical and plant engineering are the highest margin verticals for them. And if you listen to Kesab Panda’s recent interview, he sees medical in Top 2 divisions (out of 5 they have) in next 2-3 years so that can help to sustain or increase margin.

As far as growth is concerned, deals in ER&D are always very small in size compared to IT. But see how LTTS mined one of their existing customers to win their largest ever deal of USD $100mn+. In fact, its probably the largest ER&D deal won by an Indian company in O&G segment. This should help LTTS to get more larger deals in future.

This is as recent as yesterday. Here also Mr. Panda highlights Medical as a growth driver for LTTS going forward. The big order win of USD$ 100mn+ should start contributing to revenues from Q4 FY21 onwards.