Just see in listed history only the sales and PAT CAGR haven’t been 20%+ which current valuations are demanding. Shallow cyclicality comes from its major revenue base being US market which has seen economic slowdown due to China trade war and other reasons. Read concalls to know more

There are degrees of cyclicality, every business has it.

Currently it is in upcycle because of the tailwinds that can come in because of global economic revival and US govt planning to spend 1T on infrastructure.

The jewel of Indian markets and Tata’s crown, TCS, also has major revenue from USA since it started operations…is TCS also shallow cyclical then?

I understand that the engineering, R&D aspect may have some cyclicity but this business does not deserve to be called shallow IMO

Disc. Invested & biased. Not a buy/sell recommendation. Views only for academic purposes

L&T Technology Services partners with Microsoft to

offer IIoT-based smart manufacturing solutions.it has

entered into an agreement with Microsoft to offer LTTS’ Energy & Sustainability Manager

Solution on Microsoft Azure to digitally transform and create sustainable factories of the future.

L&T Tech Partners with NVIDIA and Mavenir for AI adoption in 5G technology.The company seems to making all the right noises and market is loving it.Hope it cashes on the new technology boom and meets market expectations.

Current Market cap of 60K crore can reach 100k crore pretty quickly if everything is on the right path.

@Sudhakar_Subramanian, It looks like a subscriber only premium article. Is it possible for you to share the excerpts/summary if you have access to it? Thanks.

When compared on multiple metrics, both companies look equally good.

Tata Elxsi perhaps looks better due to higher operating margins, excellent dividend profile, and an impressive ROE.

However, high debtor days and client concentration is a red flag that investors should pay close attention to.

LTTS has more than 300 clients making its revenue mix highly diversified as compared to Tata Elxsi. The company is also trading cheaper when compared to Tata Elxsi’s valuations.

E R&D services ratings by Zinnov.

This applies to many companies including LTTS.

Some takeaways:

HCL is ahead of TCS, in fact, HCL is 2nd for scale and scalability. In press release HCL announced no.1, Capgemini includes Altran – else they are No 1.

LTTS is much ahead of Tata Elxsi

In mid-cap persistent systems & Cyient seems better on E R&D

The scale of KPIT improved from 2020 to 2021.

Hello all. Recently started studying this company. Some questions, if someone can please help answer:

Their cross-pollinovation seems interesting. It seems like a reusability factor in IT product companies, where the additional client revenue does not incur costs in the same proportion and leads to operating leverage. Are there any examples of this? I read that they had made an automatic welding robot for one client which they re-used for another client in a different vertical. Any more such examples?

LTM attrition rate seems high around 17%. What are the advantages on this side? Seems to be same as peers and no differentiation on attrition.

In 2019 they had lost a client due to client switching for an in-house preference rather than outsourced. What prevents something similar from happening in the future too? Any steps being taken to mitigate this?

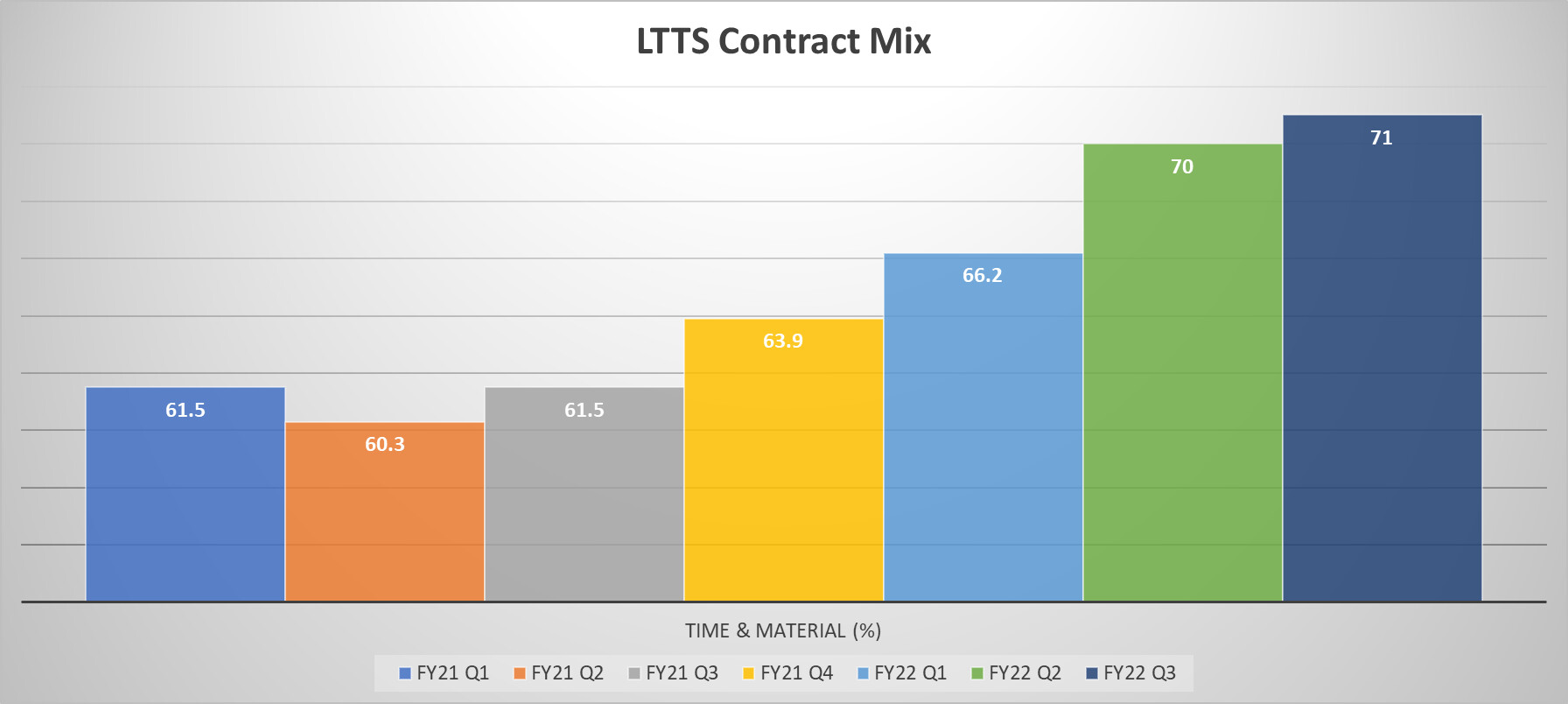

Generally in IT services T&M is considered less risky than fixed price contracts. Is this even more important for ER&D given the relatively more capital intensive nature of ER&D?

What are the steps they are taking towards account mining?

It is interesting to see their T&M % consistently rising:

Attrition in ER&D is more vital than IT Services as engineer skills cant be learned next day. So I guess they are next to maybe TCS only in terms of attrition in whole IT landscape

To me client mining hasn’t happened yet, and sales/client number has dipped at times. In last call they mentioned that they are actively hunting down this path. Only numbers can confirm this in future

T&M vs Fixed costs. T&M is hourly based implying that client has constant eye on the hours billed, resources utilized. Tata Elxsi number might be low for T&M since they are heavily in auto space (one vertical) and maybe doing projects which do not require lot of involvement from R&D team of the client and specification of end deliverable is well defined, while LTTS being a diversified player requires lot of collaborative R&D between clients and workforce to deliver projects and scope/requirements may not be as defined at the start of the project.

Given the importance of the quality of embedded software (and negative impacts of software failure), are we seeing some trend where the share of outsourced ER&D spends is increasing as compared to in-house?

How much time to market (turnaround time) is saved (quicker) by outsourcing the ER&D vs inhouse?

Do clients prefer pure play ER&D companies over integrated (IT co doing ER&D)?

Its not correct to say client mining has not happened yet. In general, no business can thrive without client mining as you can’t get deals from new customer regularly due to competition.

Coming back to LTTS, if you have noticed the $45 mn EV deal they announced in Q3 was result of client mining. Same customer stared giving them work in Q1, Q2 and eventually the mega deal in Q3. In total, that customer gave them work of close to $100 mn in the EV space in 3 quarters.

The recently announced engagement of Airbus EMES program is also another example of client mining. LTTS was selected as partner for Airbus’ “Skywise Partner program” last year. After detailed assessment by Airbus of LTTS capabilities they got the recent multi year deal.

Someone with ER&D industry expertise, can you please explain whether it is really the case that clients prefer pure play ER&D companies over integrated (IT co doing ER&D)? What would the difference be for the client? Is being pure-play really an advantage?

Most of the IT biggies like Accenture, TCS, Infosys, Wipro etc have their own ER&D divisions. In fact Accenture is betting big on Industry X (They call ER&D as industry x i guess) since last few years. Pure play ER&D and Traditional IT both have their own advantages.

While IT biggies have the money power and scale, Niche and Pure play ER&D players are more focused and agile. They can adjust quickly based on customer requirements which may not be the case for IT biggies. IT companies are more interested in large contracts while the pure play players fill in the relatively smaller contract space. IT companies have been in acquiring mode since last few years in ER&D spaces to build their scale and expertise where as pure play will have to rely on small scale acquisitions to build scale in a specific area.

In general, both have their own USPs and the market is big enough for everyone to get business.